- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

ANPR Resolution-Related Resource Requirements for Large Banking Organizations

Resolution-Related Resource Requirements for Large Banking OrganizationsAgency: Federal Reserve System

Comment Period Opens: October 24, 2022

Comment Period Closes: December 23, 2022

Comment Submitted: December 2, 2022

Docket No. R-1786

RIN 7100-AG44

Resolution-Related Resource Requirements for Large Banking Organizations

Agency: Federal Deposit Insurance Corporation

Comment Period Opens: October 24, 2022

Comment Period Closes: December 23, 2022

Comment Submitted: December 2, 2022

Docket No. R-1768

RIN 3064-AF86

We appreciate the opportunity to comment on the request for public comment by the Board of Governors of the Federal Reserve System (Board) and Federal Deposit Insurance Corporation (FDIC) (together, the agencies) on their advance notice of proposed rulemaking (ANPR) regarding whether an extra layer of debt within the organization could improve optionality in resolving a large banking organization or its insured depository institution and on the costs and benefits of a simple alternative. The Mercatus Center at George Mason University is dedicated to bridging the gap between academic ideas and real-world problems and to advancing knowledge about the economic effects of regulation, and our comment does not represent the views of any affected party. Rather, it is designed to help the agencies as they consider various means to address financial stability by limiting default risk and protecting insured depositors from suffering loss while keeping options open for the FDIC to resolve a firm while minimizing the long-term risk to financial stability.

The proposed ANPR explores adding total loss absorbing capacity (TLAC) and long-term debt as part of a broad, prescribed resolution strategy for Category II and III banking organizations, like those strategies currently in effect for global systemically important banks (GSIBs). The ANPR’s well-meaning intention is to facilitate the resolution of large banking firms to assure that the failure of a large banking firm can be resolved with less loss to insured depositors and the FDIC and to mitigate systemic financial disruption. However, its unintended consequence may be less financial stability, given that increases in debt increase the holding company’s leverage. Requiring banking firms to increase their reliance on debt relative to equity may undermine the very financial stability sought by the policy.

Our response to the ANPR focuses on the fundamental issue of whether the agencies could be encouraging the use of increased leverage as a tool used only for resolution purposes, given that this tool undermines financial stability. Part I of our response outlines the adverse effects of using long-term debt on the financial strength of a banking organization, it outlines the problem arising from favoring debt over equity, and it proposes that the ANPR consider alternatives that favor equity. Part II addresses only the first two questions within the ANPR, providing significantly more detail to the advantages of equity over debt for financial stability purposes and compares the cost-benefit tradeoff of an alternative policy that relies on more equity rather than debt. Our response does not address the remaining questions, which focus more on the mechanics of requiring more debt.

Part I: TLAC and Bank Resiliency

Bank Resolvability, TLAC, and Bank Resiliency

Long-term debt under the TLAC rule is not designed to enhance the overall financial strength of a banking firm. Under title II of the Dodd-Frank Act, it is to enable single point of entry (SPOE) as the means to resolve the failure of a large bank holding company headquartered in the United States. Under the SPOE solution the top tier of a failed bank holding company would be put into an FDIC receivership, reorganized, and reconstituted as a new company with its subsidiaries remaining in place and operating normally. To facilitate this process, the holding company would be required to have sufficient long-term debt in addition to TLAC consisting of common equity Tier 1 capital, measured relative to risk-weighted assets, to absorb losses remaining after its equity is extinguished and to recapitalize the subsidiaries sufficiently to enable their operations to continue under a new holding company. The presumption is that this solution could be accomplished without financial panic or significant government funding. The subsidiary could include insured banks, broker-dealers, and asset managers. The agencies’ ANPR requires further that the holding company be “clean” and engage in no other activities at the parent company to remove “obstacles to an orderly [SPOE] resolution.”

While elegant in theory, in practice the TLAC rule faces challenges and may create its own brand of instability. Some Category II and III banking firms may already carry long-term debt for operating purposes, which they could convert to satisfy current TLAC rule definitions of long-term debt. However, most firms would need to issue long-term debt beyond their immediate needs to meet the mandate, which would increase earnings and cash flow demands for added debt service. Although the agencies might prefer that firms swap out debt instruments, reduce deposits, or issue additional capital to maintain balance sheet strength, firms (as we describe later) would be more inclined to accept higher leverage as demands for industry earnings accelerate.

For agencies to require a Category II or III firm to add debt onto its balance sheet is inconsistent with promoting financial stability. Table 1 in the Federal Reserve Bank of Kansas City’s “Bank Capital Analysis Semiannual Update” shows, for example, that the largest regional banks are systematically better capitalized than the GSIBs they would be required to mimic. The supplementary leverage ratio for US GSIBs was 5.76 percent as of year-end 2021, whereas for the non-GSIB organizations over $100 billion the ratio was 7.48 percent. Requiring the regional banks to mimic the GSIBs and fund themselves with TLAC rule long-term debt could create an incentive for them to rely less on equity funding, with the result being an increase in their vulnerability to financial shocks.

Looking ahead, when an economic recession occurs and bank earnings are insufficient to make debt payments, regulators will face the prospect of having to allow the transfer of scarce earnings from the bank to the parent firm to avoid default. Unlike with dividends, there can be no unilateral suspension of debt interest payments. This outcome would be in stark contrast to the notion of the holding company being a source of strength to the insured bank. The irony of such a result should not be lost on policymakers. Rather than encouraging regional banks to add leverage, the financial system could be served better by requiring the GSIBs to increase equity and moderate their leverage.

We emphasize that the application of a TLAC rule to Category II and III banks would offer no assurance that the amount of debt the agencies require of these banking firms would prove sufficient to avoid failure, avoid financial panic, or indicate a more resilient industry. There is no certainty regarding how much long-term debt is enough to both absorb losses after equity is extinguished and adequately recapitalize the operating subsidiaries. Once losses absorb the subordinated debt, the FDIC or Treasury would find it necessary to provide for any capital shortfall in the subsidiaries. Finally, touting the ability of long-term debt under TLAC rule to reduce losses that would otherwise fall to the FDIC fund is misleading, given that a comparable amount of equity capital would also absorb these losses.

Finally, to appreciate the potential adverse effects of a TLAC rule, it is useful to look at the history of trust-preferred securities (TruPS). Before the Global Financial Crisis, regulators permitted firms to issue these instruments at the holding company and to include them as part of the firms’ capital. Although TruPS are essentially long-term debt instruments, it was argued that they would be available to help absorb losses in a crisis, relieving the firms from having to hold equity. As the crisis unfolded, the weaknesses of TruPS revealed themselves as banking firms moved cash from the operating banks to the holding company to avoid default. TruPS placed significant pressures on insured banks to continue making large debt-service payments, which most certainly exacerbated losses to the banking system. As it turns out, Congress wisely eliminated the use of these instruments as part of industry capital when it passed Dodd-Frank.

TLAC Rule Long-Term Debt and Expanding Subsidies

Although the ANPR does not discuss it, the FDIC currently subsidizes the use of subordinated debt when downstreamed to the insured bank. The FDIC’s assessment rate includes downward adjustments to the initial base assessment rates for unsecured debt. By contrast—and ironically—there is no comparable downward adjustment for banks funding with more equity than the minimum supervisory requirements.

Thus, mandating the use of TLAC rule long-term debt and subsidizing its use to Category II and III banking firms would subsidize leverage for an already highly leveraged industry. It places additional earnings demands on the banking system and, during periods of financial stress, makes default more likely rather than less, which is counterproductive. The agencies should understand that their role is to implement policies that ensure an institution is financially sound on a going-concern basis and that the industry is resilient and able to withstand unexpected shocks.

Alternatives to a TLAC Rule

As an alternative to the agencies’ requiring banking firms to take on TLAC rule long-term debt, the agencies could instead strengthen industry equity capital rules. Such a shift in emphasis would raise equity capital levels and better assure the public that banks are safe and sound and that the industry is financially resilient. The agencies repeatedly give too little weight to the importance of tangible equity held on the balance sheet. It is well understood among investors that although leverage may boost short-term returns, it is equity that provides reliable long-term performance and industry resiliency. Also, such an alternative would not prevent a banking firm from issuing long-term debt to fund business operations, but such funding would not be a supervisory tool or a sanctioned substitute for bank reserves and equity capital.

Under this alternative, because equity funding provides greater balance sheet strength and firm resilience, the FDIC could change its insurance pricing. It could end its subsidy for debt and apply it to capital levels that exceed minimum standards. Should a bank fail, this excess capital would absorb the losses that the FDIC would have otherwise incurred. It is often suggested that requiring higher bank capital raises the banking industry’s cost of funding and reduces lending. However, this phenomenon may mask the fact that, ceteris paribus, higher risk-based capital requirements tend to favor holding more low-risk-weight assets, such as Treasuries and reserves, while discouraging holding more high-risk-weight assets, such as mortgages and commercial and industrial loans. Furthermore, banks that maintain more capital relative to total assets have greater capacity to lend during both expansion periods and times of economic stress. In our responses to questions 1 and 2, we show that the cost-benefit tradeoff between greater capital and reductions in economic growth shows greater capital to be a viable option, even though we assume for the sake of argument that higher equity capital results in higher borrowing costs.

Finally, the mandate for a higher strong minimum capital requirement could be implemented in combination with the title I resolution planning process and the annual stress test programs. Such an approach is more judicious than a sweeping TLAC rule. Under Dodd-Frank, each title I plan is prepared in detail by management and reviewed and approved by supervisors. Each plan is based on the specific business model of the firm and the bankruptcy strategy that would work best for that firm. The annual stress test would test the ability of the firm to withstand financial shocks and gauge the degree of capital greater than the required minimum needed to remain solvent and operational under stress. Thus, instead of applying a blanket long-term debt requirement to facilitate one resolution strategy—SPOE, for example—regulators could use the title I plan and stress test to tailor long-term funding plans to a firm’s business model, capital structure, and resolution strategy, better assuring a private-sector resolution should it be needed. We next provide answers to the first two questions posed in the ANPR.

Part II: Response to ANPR Questions 1 and 2

In supporting our comment above, we are responding to questions 1 and 2 set out in the ANPR. In these responses, we use a benefit-cost comparison to show the advantages of increasing equity rather than debt.

Question 1: The agencies invite comment on whether and how a requirement to maintain a minimum amount of long-term debt could enhance a large banking organization’s resolvability. How might long-term debt be beneficial for improving optionality when conducting the resolution of a U.S. large banking organization or its insured depository institution?

Fischer Black suggests that capital can consist of equity or long-term debt, whereas Black, Merton Miller, and Richard Posner argue that higher capital could provide a low-cost way for holding companies to offset the risks associated with nonbank subsidiaries. However, if the subsidiaries are well-capitalized, the authors suggest that no need exists to have holding company capital requirements. After all, Paul Kupiec intimated, a holding company may not provide the resources to prevent a bank subsidiary from failing. Black, Miller, and Posner also suggest that a necessary question to ask when designing regulatory capital requirements is whether protecting depositors or preventing bank failure is the goal. If the answer is protecting depositors then TLAC rule long-term debt might be acceptable, but if the purpose is to foster financial stability, then having banks fund with more debt undermines that objective, because it makes the entity in question more leveraged. Because much of the legislative and regulatory language since the Global Financial Crisis concerns financial stability, TLAC works against the objective.

Aside from increasing leverage, TLAC rule long-term debt applies at the holding company level, and this is justified by the “source of strength” doctrine (Regulation Y), that a holding company will always come to the rescue of a failing bank subsidiary. In fact, Kupiec suggests holding companies have not always come to the rescue of a failing bank subsidiary. Therefore, an alternative approach to fostering financial stability focuses on capital regulation at the bank subsidiary rather than the holding company, and more equity (less debt) would likewise facilitate achieving that goal.

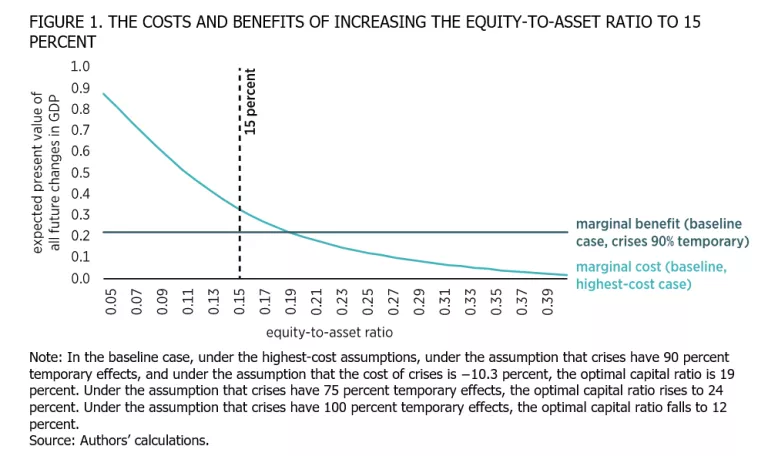

A 15 percent leverage ratio has sometimes been offered as a regulatory minimum. We show in our answer to question 2 that many bank holding companies already meet this minimum threshold. However, the question remains whether the costs outweigh the benefits of meeting this threshold. Next, we summarize an approach, starting with analyzing costs and benefits, to answer this question on the basis of previously published research that finds that the benefits generally outweigh the costs.

To illustrate the benefits and costs, we use a baseline estimate of the benefits based on empirically supported and conservative assumptions about the benefits while making the highest-cost assumptions. The assumed benefits arise from more capitalized banks having a lower likelihood of experiencing default, which lowers the likelihood of the damage of banking crises. The assumed costs arise from the fact that equity funding is assumed to be more expensive than debt, such that banks funded with more equity might pass along their higher funding costs to borrowing customers.

Figure 1 depicts the marginal benefits under the baseline case motivated by reasonable assumption against the marginal costs under the highest-cost case. The figure shows that the benefits of going to 15 percent exceed the costs, with the optimal rate equal to 19 percent.

We use a similar approach to respond to question 2:

Question 2: The agencies invite comment on alternative approaches for determining the appropriate scope of application of a potential long-term debt requirement to the population of large banking organizations. In particular, what criteria would be relevant to determine whether a large banking organization should be subject to the requirement? Should all Category II and Category III firms (including SLHCs, which are not subject to resolution planning requirements) be subject to a long-term debt requirement? Why or why not? What additional factors—for example, the presence of significant non-bank operations, critical operations, critical services outside the bank chain, cross-border operations, or extent of reliance on uninsured deposits—should the agencies consider when determining the scope of application of any long-term debt requirement to large banking organizations? Given the practical and market limitations for selling large insured depository institutions, especially during a crisis, what is the appropriate scope of application for a loss absorbing debt requirement to expand the range of strategies available to the FDIC? How should IDIs that are not part of a group under a BHC be considered?

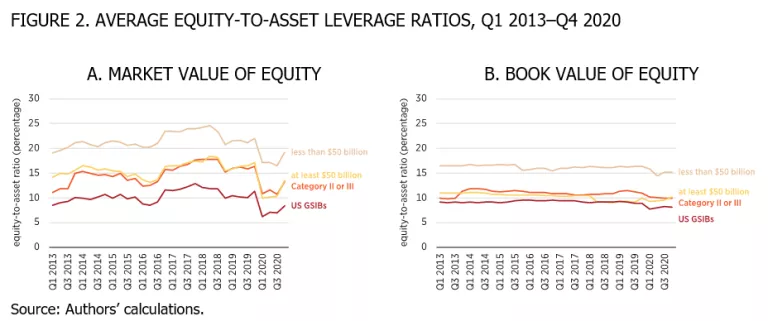

As an alternative to TLAC requirements, we suggest that equity capital, especially at the bank subsidiary level, rather than the holding company, can work well. We would also like to point out that while much of the discussion of too big to fail (TBTF) focuses on size, that focus may confuse the underlying issue, as larger firms also tend to fund with less equity. That tendency suggests that the key issue underlying TBTF is not strictly speaking size, but the fact that the largest entities are the most leveraged. We can demonstrate this idea in figure 2, which compares the average ratios of total equity to total assets measured using estimated market values and book values for the so-called advanced approaches banks, which are the largest in the United States and the focus of Basel III capital regulations, as well as all other banks from Q1 2000 through Q4 2020 using the approach used by Alistair Milne.

The figure shows that the GSIBs on average have the lowest average leverage ratios, whereas those with less than $50 billion have the highest average leverage ratios. The leverage ratios for Category II or III banks based solely on total assets rather than other activities and those with at least $50 billion on average fall in between those of banks less than $50 billion and those of US GSIB holding companies. Average leverage ratios measured using estimated market values tend to exceed the average leverage ratio measured using book values. Also, on average, banks with less than $50 billion in total assets have leverage ratios equal to about 15 percent when measured using book values and 20 percent when measured using market values, whereas the larger non-GSIB banks often have leverage ratios of 15 percent when measured using market values.

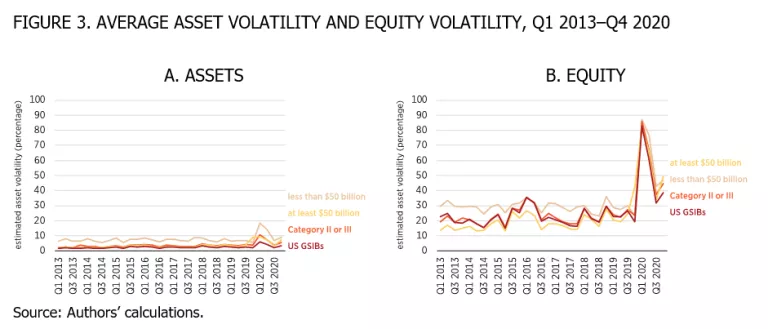

In spite of being less leveraged, figure 3 shows that, in terms of estimated asset risk, the smallest banks on average have a higher estimated asset volatility than larger banks. One way to explain this is that the largest banks tend to have much greater holdings of liquid securities and reserves and have a much smaller fraction of their assets allocated to loans, which would tend to lower asset volatility. But although estimated asset volatility is lower, the fact remains that the largest banking entities are more leveraged. In terms of the equity return volatility, earlier in the sample the smaller banking entities had a higher equity return volatility, but toward the end of the sample, the averages were similar.

Conclusion

In bankruptcy, the conversion of standard debt is often part of a workable reorganization strategy. But banking authorities should be cautious before demanding increased levels of debt for individual banking firms or encouraging an increase in the effective leverage of an industry. Adding leverage to the banking system in the expectation that it enhances financial stability is a gamble. Equity funding enhances resiliency, which is the goal of regulation and supervision.

The proposed rule’s emphasis on higher capital is laudable. However, the focus on TLAC undermines the main goal of the proposal, which is to foster financial stability. As an alternative, a simpler (and higher) leverage ratio of 15 percent at the bank subsidiary level passes a benefit-cost analysis under many plausible assumptions.