- | Government Spending Government Spending

- | Federal Testimonies Federal Testimonies

- |

Assessing the Department of Energy Loan Guarantee Program

Testimony Before the House Committee on Oversight and Government Reform

For obvious reasons, more than any other recent events, the waste of taxpayers’ money due to Solyndra’s failure has attracted much attention. However, the problems with loan guarantees are much more fundamental than the cost of one or more failed projects.

In his famous book Economics in One Lesson, economist Henry Hazlitt wrote, “Government encouragement to business is sometimes as much to be feared as government hostility.”

In 2009, renewable energy company Solyndra received $535 million through the federally backed 1705 loan guarantee program of the Department of Energy (DOE). Two years later the firm filed for bankruptcy and had to lay off its 1,100 employees, leaving taxpayers bearing the cost of the loan.

For obvious reasons, more than any other recent events, the waste of taxpayers’ money due to Solyndra’s failure has attracted much attention. However, the problems with loan guarantees are much more fundamental than the cost of one or more failed projects. In fact, the economic literature shows that (1) every loan guarantee program transfers the risk from lenders to taxpayers, (2) is likely to inhibit innovation, and (3) increases the overall cost of borrowing. At a minimum, such guarantees distort crucial market signals that determine where capital should be invested, causing unmerited lower interest rates and a reduction of capital in the market for more worthy projects. At their worst, they introduce political incentives into business decisions, creating the conditions for businesses to seek financial rewards by pleasing political interests rather than customers. This is called cronyism, and it entails real economic costs.

Yet, these loan programs remain popular with Congress and the executive. That’s because in general most of the financial cost of these guaranteed loans will not surface for many years. That means that Congress can approve billions of dollars to benefit special interests, with little or no immediate impact to federal appropriations in the short term, because they are almost entirely off-budget.

HOW DO THESE LOAN GUARANTEES WORK?

The DOE Loan Programs Office (LPO) administers three separate loan programs: (1) Section 1703 loan guarantees, (2) Section 1705 loan guarantees, and (3) Advanced Technology Vehicle Manufacturing (ATVM) loans. Here are descriptions of the three loan programs, as explained by DOE:

- Section 1703 of Title XVII of the Energy Policy Act of 2005 authorizes the U.S. Department of Energy to support innovative clean energy technologies that are typically unable to obtain conventional private financing due to high technology risks.

- Advanced Technology Vehicles Manufacturing (ATVM) loans support the development of advanced technology vehicles (ATV) and associated components in the United States. They also meet higher efficiency standards.

- The Section 1705 Loan Program authorizes loan guarantees for U.S.-based projects that commenced construction no later than September 30, 2011 and involve certain renewable energy systems, electric power transmission systems, and leading edge biofuels.

According to LPO’s website, DOE’s loan guarantee authority originated from Title XVII of the Energy Policy Act of 2005 (P.L. 109–58). Under Section 1703, the federal government can guarantee 80 percent of a project’s total cost. The American Recovery and Reinvestment Act of 2009 (P.L. 111–5) amended the Energy Policy Act of 2005 by adding Section 1705. Section 1705 was created as a temporary program, and 1705 loan guarantee authority ended on September 30, 2011.

The dollar volume of loans that can be guaranteed under DOE’s authority is predetermined by congressional appropriations that oversee the program. A simple way to explain how these loans work is the following: If a recipient defaults on its loan, the federal government pays the remainder of the debt to the lenders and repossesses all of the assets from the unfinished projects.

As with other loan programs, to prevent taxpayers’ exposure, the federal government has established a credit subsidy fee. In this case, the cost of the fee is determined by DOE, with guidance from OMB. The lenders usually charge the up-front guarantee fee to the borrower after the lender has paid the fee to DOE and has made the first disbursement of the loan.

This is not the case for 1705 loans, however. Under the stimulus bill, DOE received appropriated funds to pay for credit subsidy costs associated with Section 1705 loan guarantees, which, after rescissions and transfers, was $2.435 billion. As the Congressional Research Service rightly puts it, “Section 1705 loan guarantees were very attractive as they provided an opportunity to obtain low-cost capital with the required credit subsidy costs paid for by appropriated government funds.”

DOE does not provide loans directly. Instead, borrowers have to apply to qualified finance organizations. These lenders are expected to perform a complete analysis of the application. Then DOE reviews the lender’s credit analysis rather than conducting a second analysis. DOE still makes the final credit and eligibility decision.

DO LOAN GUARANTEES DO WHAT THEY CLAIM TO DO?

Leaving aside the question of whether the government should encourage the production of certain goods or services, the economic justification for any government-sponsored lending or loan guarantee program must rest on a well-established failure of the private sector to allocate loans efficiently (meaning that deserving recipients could not have gotten capital on their own). Absent such a private-sector deficiency, the DOE’s activities would simply be a wasteful at best, politically motivated at worst subsidy to this sector of the economy.

Yet, many argue that some public policy objectives require the sacrifice of marketplace efficiency. It is an accepted feature of modern American government that some public interests or social policy gains outweigh economic losses. In the case of green energy, the government’s lending programs could fulfill specific public policy objectives that the marketplace on its own would not otherwise serve or would supply at suboptimal levels. But do they?

In describing its role in the economy, the DOE proclaims that its loans help save the plane by helping to secure funding for the earlier-stage technologies or the later commercialization stage—known as the manufacturing “Valley of Death.” It also claims that the loan recipients will generate economic growth and “green” jobs that otherwise would not appear. DOE can thus be judged on its ability to meet these public policy goals—namely, to fill the supply-and-demand gap in the clean energy loan market, particularly for startups.

To measure the DOE results, I looked at the flow of DOE credits to evaluate who receives them and whether the DOE is meeting its stated policy objectives of promoting new startups and encouraging the creation of green jobs.

A close examination demonstrates that neither stated DOE policies nor its actual lending patterns provide evi- dence that its loan guarantees serve any of its defined public policy purpose.

FOLLOWING THE 1705 LOAN GUARANTEE PROGRAM MONEY

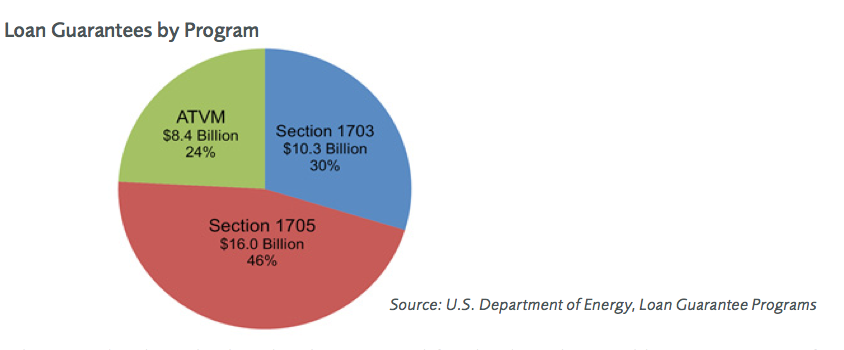

Since 2009, DOE has guaranteed $34.7 billion, 46 percent of it through the 1705 loan program, 30 percent through the 1703 program, and 14 percent through the ATVM.

The 1705 (under which Solyndra received funding) authorized loan guarantees for programs for “certain renew- able energy systems, electric power transmission systems and leading edge biofuels projects that commence construction no later than September 30, 2011.” This program is a product of the economic stimulus bill of 2009. As mentioned before, this program offered borrowers better terms than the 1703—in some cases the government paid for a substantial fee out of appropriated funds, one that is the borrower’s responsibility under the 1703. Also, many 1703-eligible projects were also eligible under the 1705.

The data shows that:

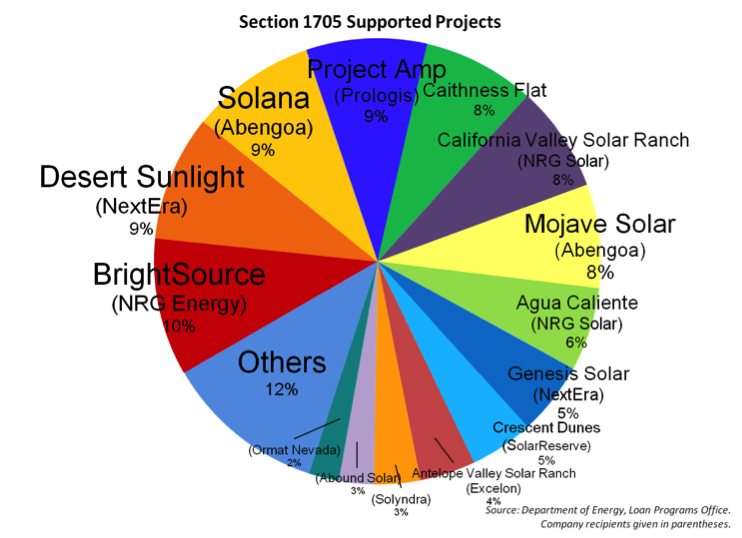

- 26 projects were funded under the 1705, and guaranteed roughly $16 billion in total.

- Some 2,378 permanent jobs were claimed to be created under the program. This works out to a taxpayer exposure of $6,731,034 per job.

- The recipient of the most 1705 loans is NRG Energy Inc. (BrightSource).

- NRG Energy Inc. (BrightSource) received $1.6 billion (11 percent of the overall amount guaranteed under the 1705).

- The top 10 recipients of loans under the 1705 program:

- Are all solar generation companies,

- Received 76 percent of the overall amount guaranteed,

- Received $12.2 billion in loan guarantees, and

- Included NextEra Energy Resources, LLC (Desert Sunlight), a fortune 200 company; Abengoa Solar Inc. (Solana), a Spanish multinational company; and Prologis (Project Amp), a global real estate investment trust. Utility firms like NRG Energy received three separate loans in the top 10 recipient list.

- Prologis received $1.4 billion (8.75 percent of the total).

- Solyndra, the now bankrupted solar company, received $535 million in loan guarantees or 3.34 percent of the total.

- Cogentrix, a wholly owned subsidiary of the Goldman Sachs Group Inc, received a $90 million guarantee from the government.

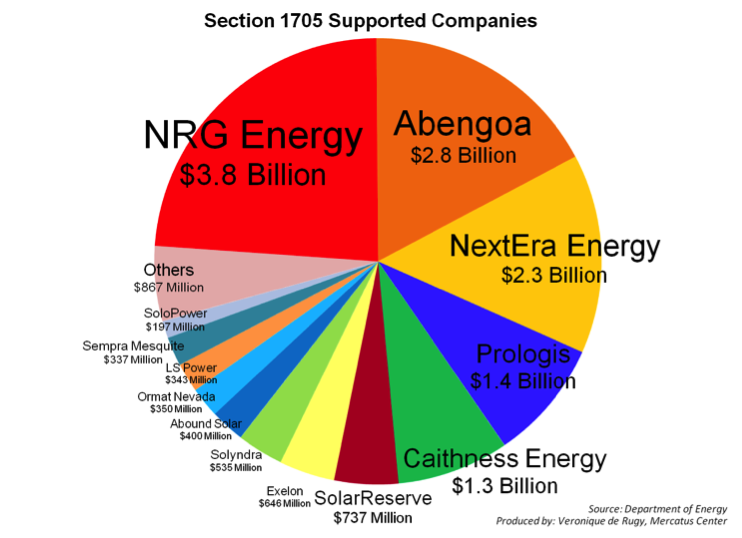

If we organize the data by companies receiving 1705 loans, we find:

- The recipient of the most 1705 loans is NRG Energy Inc.

- NRG Energy Inc. received $3.8 billion (23.7 percent of the overall amount guaranteed under the 1705)

- Four companies received 64 percent, or $10.3 billion, of the total amount guaranteed under the 1705 program. These companies are:

- NRG Energy,

- NextEra Energy,

- Arbogea, and

- Prologis.

First, it should be noted that very few permanent green jobs were created under the 1705 loan program (or any of the other loan programs). The Obama administration had initially pushed these projects as job generators, claim- ing that it could create 5 million jobs in America through investment in green technology.

Also, to the extent that “green jobs” were created, the $6.7 million taxpayer exposure per job is quite spectacular. This trend and number probably dismisses this particular loan program as a job program.

Second, as we can see here, under the 1705 program most of the money has gone to large and established companies rather than startups. These include established utility firms, large multinational manufacturers, and a global real estate investment fund. In addition, the data shows that nearly 90 percent of the loans guaranteed by the federal government since 2009 went to subsidize lower-risk power plants, which in many cases were backed by big companies with vast resources. This includes loans such as the $90 million guarantee granted to Cogentrix, a subsidiary of Goldman Sachs. Currently, Goldman Sachs ranks number 80 on the list of America’s Fortune 500 companies.

This probably means that if there were an actual gap between the supply and demand for loans for energy com- panies, startups, or others, this program wouldn’t be filling it. In fact, most of these loans look like government transfers of the worst kind: subsidies to very large corporations very much resembles cronyism.

Third, there seems to be an even more troubling trend of “double dipping” by large companies that received loan guarantees from the DOE program. Many of the companies that have benefitted from subsidized loans under the 1705 guarantee program also received additional grants under the American Recovery and Reinvestment Act (ARRA). For example, Prologis (which benefitted from $1.4 billion in subsidized loans) received a grant for $68,000 for the purpose of “rent for warehouse space” under the Recovery Act.

Green Mountain Energy, a company of NRG Energy, received two grants under the ARRA in the second quarter of fiscal year 2011. Likewise, Reliant Energy and Reliant Energy Tax Retail LLC, two other NRG Energy companies, reported receiving at least 37 grants under the ARRA. These grants augmented the $3.8 billion in loan guarantees for NRG Energy distributed under the Section 1705 Loan Program.

NRG will also be eligible to receive $430 million from the Department of the Treasury. In addition, many com- panies benefited from the Department of Treasury 1603 grants.

Quoted in the New York Times recently, NRG’s chief executive, David W. Crane, explained how his company and its partners have secured $5.2 billion in federal loan guarantees, plus hundreds of millions in other subsidies for four large solar projects. “I have never seen anything that I have had to do in my 20 years in the power industry that involved less risk than these projects,” he said in a recent interview. “It is just filling the desert with panels.”

Examples of companies benefitting from multiple assistance programs initiated during this period abound. For instance, in addition to the $538 million it received under the 1705 loan program, Solyndra benefited from a $10.3 million loan guarantee that the Ex-Im Bank extended to a Belgian company (described in the Ex-Im deal data as “Zellik Ii Bvba”) to finance a sale of Solyndra products.

Solyndra isn’t alone. First Solar’s Antelope Valley project received a $646 million 1705 loan in 2011 through its partner Exelon, and per my calculation from the Ex-IM Bank FOIA deal data information for FY2011, the company also scored $547.7 million in loan guarantees to subsidize the sale of solar panels to solar farms abroad.

More troubling is the fact that some of the Ex-Im money went to a Canadian company named St. Clair Solar, which is a wholly owned subsidiary of First Solar. St. Clair Solar received a total of $192.9 million broken into two loans to buy solar panels from First Solar. In other words, the company received a loan to buy solar panels from itself. Incidentally, First Solar also received a $16.3 million loan from the government in 2010 to expand its factory in Ohio.

This double-dipping by energy companies isn’t new, unfortunately. While there is no doubt that the deals are lucrative for the companies involved, taxpayers have a lot to lose. Further, double-dipping provides evidence that businesses will be tempted to steer away from productive value creation for society and instead work on narrowly serving political interests for financial gain.

THE CASE AGAINST CLEAN ENERGY LOAN GUARANTEES

A great deal of attention has been focused on Solyndra, a startup that received $528 million in federal loans to develop cutting-edge solar technology before it went bankrupt, had to lay off over a thousand workers, and left taxpayers to foot the bill. Obviously, the considerable waste of taxpayers’ money is upsetting. But it is only one aspect of the fundamental problems caused by loan guarantee programs in general, and DOE’s clean energy loan programs in particular.

1. Socialized Losses and Privatized Gains

Historically, loans guaranteed by the government have had a higher default rate than the loans issued by the private sector without government guarantee. For instance, the Small Business Administration (SBA) has a long-term default rate of roughly 17 percent. This compares to 4.3 percent for credit cards and 1.5 percent for bank loans guaranteed by the Federal Deposit Insurance Corporation.

Also, the Congressional Budget Office has calculated that the risk of default on the DOE’s nuclear loan guarantee program, for example, is well above 50 percent. In 2011, the CBO updated its study and replaced the embarrassing default rate with a list of variables affecting the rate. While it doesn’t provide a specific rate, the report asserts that higher equity financing of these projects would reduce the risk of default. However, this is rarely the case, as most loan guarantee programs cover 80 percent of their financing through debt rather than equity.

Moreover, according to the CBO, when the federal government extends credit, the associated risk of those obli- gations is effectively passed along from private lenders onto taxpayers who, as investors, would view this risk as costly. In other words, when the federal government encourages a risky loan guarantee it is “effectively shifting risk to the members of the public.”

Also, if the loan isn’t repaid, then the cost of the investment is to taxpayers. However, if the loan is repaid as expected, the lender will benefit from all the interest payments it collected thanks to a fairly risk-free loan, and the borrower will collect the fruit of its successful business venture. In other words, loan guarantee programs are yet another way that the federal government socializes losses while privatizing benefits.

2. Moral Hazard

Federally backed loans create a classic moral hazard. Because the loan amount is guaranteed, banks have less incentive to evaluate applicants thoroughly or apply proper oversight. In other words, the less skin the lender has in the game, the less likely the lender will effectively vet the quality of the project. Also, the company that borrows the money has less skin in the game than it would if its loan weren’t guaranteed. In addition, each time the government bails out a firm or has to shoulder the cost of a loan guarantee that got into financial trouble, it reinforces the signal to borrowers and bankers alike that it’s OK to take excessive risks.

In a March 2012 report, the Government Accountability Office (GAO) found that the DOE loan guarantee pro- gram was riddled with program inefficiencies, putting the fairness of decisions about what firms receive loan guarantees into question. When GAO requested data from the DOE on the status of the applications, the DOE did not have consolidated data readily available and had to assemble these data over several months from various sources. Inadequate documentation and out-of-date review processes reduce the assurance that the DOE has treated applicants consistently.

These findings do not prove the ability of the DOE to fully assess and mitigate project risks. Moreover, while in the absence of government intervention the private sector builds the infrastructure to assess risk, the federal gov- ernment has neither the expertise nor the incentive to build such a safety net. This increases the likelihood that loan guarantees will be awarded based on factors other than the ability of the borrower to repay the loan, such as political connections and congressional interest in local pork.

The moral hazard of loan guarantees increases when rules intended to prevent the program from being a pure giveaway to companies are removed. This is the case, for instance, when as part of the stimulus bill of 2009, the government lifted the subsidy fees for 1705 loans. This move increases the cost to taxpayers and attracts high-risk companies.

3. Mal-investments

Loan guarantee programs can also have an impact on the economy beyond their cost to taxpayers.

Mal-investment—the misallocation of capital and labor—may result from these loan guarantee programs. In theory, banks lend money to the projects with the highest probability of being repaid. These projects are often the ones likely to produce larger profits and, in turn, more economic growth. However, considering that there isn’t an infi- nite amount of capital available at a given interest rate, loan guarantee programs could displace resources from non-politically motivated projects to politically motivated ones. Think about it this way: When the government reduces a lender’s exposure to fund a project it wouldn’t have funded otherwise, it reduces the amount of money available for projects that would have been viable without subsidies.

This government involvement can distort the market signals further. For instance, the data shows that private investors tend to congregate toward government guarantee projects, independently of the merits of the projects, taking capital away from unsubsidized projects that have a better probability of success without subsidy and a more viable business plan. As the Government Accountability Office noted, “Guarantees would make projects [the federal government] assists financially more attractive to private capital than conservation projects not backed by federal guarantees. Thus both its loans and its guarantees will siphon private capital away.”

This reallocation of resources by private investors away from viable projects may even take place within the same industry—that is, one green energy project might trade off with another, more viable green energy project.

More importantly, once the government subsidizes a portion of the market, the object of the subsidy becomes a safe asset. Safety in the market, however, often means low return on investments, which is likely to turn venture capitalists away. As a result, capital investments will likely dry out and innovation rates will go down.

In fact, the data show that in cases in which the federal government introduced few distortions, private inves- tors were more than happy to take risks and invest their money even in projects that required high initial capital requirements. The Alaska pipeline project, for instance, was privately financed at the cost of $35 billion, making it one of the most expensive energy projects undertaken by private enterprise. The project was ultimately aban- doned in 2011 because of weak customer demand and the development of shale gas resources outside Alaska. However, this proves that the private sector invests money even when there is a chance that it could lose it. Private investment in U.S. clean energy totaled $34 billion in 2010, up 51 percent from the previous year.

Finally, when the government picks winners and losers in the form of a technology or a company, it often fails. First, the government does not have perfect or even better information or technology advantage over private agents. In addition, decision-makers are insulated from market signals and won’t learn important and necessary lessons about the technology or what customers want. Second, the resources that the government offers are so addictive that companies may reorient themselves away from producing what customers want, toward pleasing the government officials.

4. Crowding Out

To some (for example, those lucky enough to receive the loan guarantee), government money may seem to be free. But it isn’t, of course. The government has to borrow the money on the open market too. This additional borrow- ing comes from Americans’ savings, as does the money that Americans invest in the private sector’s growth. There comes a point when there just aren’t enough savings to satisfy both masters. In other words, when government runs a deficit to finance its preferred projects, it can affect private sector access to capital, and lead to a reduction in domestic investment.

Economists use the term “crowding out” to describe the contraction in economic activity associated with deficit- financed spending.

In addition, the competition between public and private borrowing raises interest rates for all borrowers, including the government, making it more expensive for domestic investors to start or complete projects.

Over time, this could mean that American companies will build fewer factories, cut back on research and development, and generate fewer innovations. As a result, our nation’s future earning prospects will dim, and our future living standards could suffer.

5. Cronyism

In a 2003 speech to the National Economists Club in Washington, D.C., then–Federal Reserve Governor Edward M. Gramlich argued that loan guarantee programs are unable to save failing industries or to create millions of jobs, because—he explained—the original lack of access to credit markets is caused by serious industrial problems, not vice versa. If an applicant’s business plan cannot be made to show a profit under reasonable economic assump- tions, private lenders are unlikely to issue a loan. And they would be right not to.

Then why is the federal government still guaranteeing loans? One reason is it serves three powerful constituen- cies: lawmakers, bankers, and the companies that receive the subsidized loans.

Politicians are able to use loan programs to reward interest groups while hiding the costs. Congress can approve billions of dollars in loan guarantees with little or no impact to the appropriations or deficit because they are almost entirely off-budget. Moreover, unlike the Solyndra case, most failures take years to occur, allowing politicians to collect the rewards of granting a loan to a special interest while skirting political blame years later when or if the project defaults. It’s like buying a house on credit without having a trace of the transaction on your credit report.

It is also easy to understand why companies and company executives benefit from these loans and may seek them out. However, this shouldn’t obscure the fact that this preferential treatment comes at the expense of the taxpayer, and ultimately at the expense of our market and political system.

But another potential beneficiary of these loans is the financial institutions that issue them. With other loan pro- grams such as the SBA, there is evidence that lenders may have an incentive to favor borrowers that qualify for a loan with a government guarantee over those that do not. When a small business defaults on its obligation to repay a loan, bankers do not bear most of the cost; taxpayers do. Meanwhile, lenders make large profits on SBA loans by pooling the guaranteed portions and selling investors trust certificates that represent claims to the cash flows.

How profitable is this? Testifying before Congress in April 2006, David Bartram, the president of the SBA Divi- sion of U.S. Bancorp, the nation’s sixth-largest financial services company, explained that “return on equity of SBA loans can exceed 70 percent.” A 70 percent return on equity (RoE) is remarkably high. Right now, the five-year average RoEs for the two biggest banks in America—Citigroup and Bank of America—are 16.2 percent and 14.5 percent, respectively.

More study is required to determine whether a similarly outsized return to financial institutions occurs with the DOE program, but the parallels between the DOE and SBA programs suggest this is a possibility.

CONCLUSION:

The Department of Energy’s loan guarantee programs have been the focus of much public attention since energy company Solyndra went bankrupt last year, leaving taxpayers with a $538 million bill. Of equal concern to the significance of this waste, however, is the distortion and incentives experienced by both lenders and companies that participate in the government loan program, as well as the distortion of market signals. Further looking at where the money is going, the evidence seems to go solidly against the idea that they are achieving their goals. And the systematic economic harm done by rewarding companies that forgo value creation in favor of pursuing financial benefit through the political system creates long term consequences for our economy and our country.