- | Housing Housing

- | Policy Briefs Policy Briefs

- |

Converting Existing Housing into Affordable Rentals: A Scalable Housing Solution

Washington, DC’s housing strategy blends conversions and construction to expand affordability

The United States is facing a deepening housing affordability crisis. The Joint Center for Housing at Harvard University reports that more than 20 million renter households—over half of renters—in the United States are cost burdened, spending more than a third of their income on housing.[1] Rising interest rates and construction costs are exacerbating the challenge of building new income-restricted housing. With the cost of construction exceeding what affordable housing developers are allowed to recover in rents, building new affordable units is often not financially feasible. Fortunately, governments, nonprofits, and the private sector can help fix this shortfall through a path that has yet to be widely explored: helping affordable housing developers acquire existing housing and convert it into affordable units.

An analysis of development costs in the Washington, DC, region suggests that converting existing market-rate housing into affordable units can be quicker and more cost-effective than developing new affordable housing. In addition, converting existing housing is more likely to boost economic mobility: Building new developments funded by the low-income housing tax credit (LIHTC) often concentrates affordable housing in lower-income neighborhoods. Reusing existing housing also reduces reliance on market cycles. While there are few existing funds available to help developers acquire and convert existing housing, there are several possible tools that governments (and others) could use to expand this underused method of creating high-quality, affordable housing.

This policy brief describes the background and process of the LIHTC, along with its key shortcomings that limit its effectiveness in furnishing affordable housing: lengthy timelines, elevated costs, and failure to build socioeconomically integrated neighborhoods. It then proposes a complementary policy—incentivizing developers to convert existing market-rate units into affordable housing—explaining how this strategy avoids LIHTC’s challenges and how governments and other organizations can put it into practice.

Background

In the United States today, most deed-restricted affordable housing units are created as new development funded in part by the LIHTC. Established by the Tax Reform Act of 1986, the LIHTC program offers two types of tax credit, only one of which can be claimed for any individual project in most cases. The 4 percent credit is awarded to all qualifying projects, while the 9 percent credit is awarded competitively by state, territorial, or District of Columbia housing agencies.

The federal government sets the basic terms of the program by defining what qualifies as an affordable unit. Since 2018, a unit qualifies if it is deed restricted for 30 years at 60 percent or less of the area mean income (AMI). Beyond those criteria, the federal government awards LIHTC funding to states roughly in proportion to their population and allows states to allocate awards to projects through a competitive process. State housing agencies develop qualified allocation plans, which may prioritize eligibility using criteria such as location or affordability mix and may even restrict eligibility beyond the federal baseline requirements for length and depth of affordability. This means that, while the 9 percent credit can often cover much of a developer’s costs, eligibility remains extremely competitive.

The federal government applies the LIHTC credits to a developer’s tax liability once the development project is placed in service. The 4 and 9 percent credits are not annual tax credits equivalent to those amounts. Instead, the credits are assessed over a 10-year period, totaling approximately 30 or 70 percent of the project’s qualified basis, respectively, which tends to be around 4 or 9 percent annually. To finance construction, developers sell these future tax credits to investors in exchange for up-front capital, agreeing to repay the value of the credits plus interest.[2]

Inefficiencies in LIHTC’s Program Design

According to the US Department of Housing and Urban Development, the LIHTC program has produced more than 3.6 million affordable housing units since its inception in 1987.[3] While it remains the cornerstone of the United States’ affordable housing strategy, the program has three key limitations that hinder its ability to meet broader housing affordability goals. As such, it should be supplemented with complementary, innovative policy approaches.

LIHTC’s key drawbacks are as follows:

- Lengthy permitting and financing timelines

- Higher per-unit costs that exceed available subsidy levels

- Limited support for socioeconomic integration of buildings or neighborhoods, owing to incentives that favor development in already lower-income areas and discourage mixed-income projects

LIHTC projects face long permitting and financing time frames

Although development times vary by jurisdiction, planning for any development project, including market-rate developments, typically takes two years if built as a matter of right and four years if zoning changes are necessary. This timeline includes preliminary planning, community meetings (which are more extensive and numerous if rezoning is required), and the local government’s review and permitting process. Once construction begins, it generally takes an additional one to two years to complete, depending on project size.

LIHTC-funded projects also need to match their funding flows with financing timelines. For instance, states have specific periods for competitive financing such as 9 percent tax credit allocations and Housing Production Trust Fund subsidies. The project schedule for an LIHTC-funded project needs to match up with a funding round for these allocations. The longer any project is delayed, the more risk there is that the business cycle or other factors could derail the project—the need to match up the project timeline with the local government’s LIHTC timeline adds more delay and therefore more uncertainty for LIHTC-funded projects, with additional uncertainty piled on top of that if the project’s application for competitive subsidies is unsuccessful. In contrast to the two to four years necessary to build a new market-rate project, the overall time frame to deliver a new construction LIHTC project runs from three to five years.

LIHTC projects face higher costs per unit than market-rate development

Projects receiving LIHTC funding are more expensive than either market-rate construction or the acquisition of existing buildings. Interviews with five developers—both for-profit and nonprofit—with projects in the Washington, DC, metro area reported cost figures for LIHTC development from $600,000 to $900,000 per unit over the past three years. (The wide variance reflects differences in land acquisition costs, timing of completion, and local construction requirements.) A Washington Post article cited a cost of $1.2 million per unit for a recently completed 50-unit LIHTC-funded project in DC.[4] Overall, LIHTC development can increases costs by up to 30 percent compared to market-rate construction. The three main reasons are higher financing costs, higher construction costs, and higher compliance costs:

- Higher financing costs: LIHTC projects involve complex capital stacks of lenders and investors. Each project has significant financing fees and legal costs, including costs for the local housing financing agency, tax credit syndicator, construction lender, and others. A typical capital stack for an LIHTC project includes a construction loan that later converts to a permanent loan with a new lender (backed by tax-exempt bonds), federal and state tax credits, and gap financing if needed.

- Higher construction costs: The Davis–Bacon Act requires construction contractors receiving federal funding to pay local prevailing union wages. Section 3 requires additional spending on training, education, and contracting. These costs typically add 15 to 20 percent to an LIHTC project’s cost.

- Higher compliance costs: LIHTC projects require compliance reporting that market-rate properties do not, both during and after construction. During construction, the LIHTC developer must have cost certifications to demonstrate that the costs meet the requirements for tax credits. After construction, the project has ongoing compliance requirements to demonstrate that residents meet the income requirements, as well as ongoing compliance fees payable to the housing finance agency.

Interviews and available data suggest that LIHTC-funded buildings cost at least 20 percent more than comparable market-rate properties. The commercial real estate website Bisnow reported that the Lincoln Westmoreland, a 100-unit property in Ward 5 of Washington, DC, had a total development cost of $82 million, or $820,000 per unit.[5] Interviews with four other DC-region affordable housing developers indicated total development costs over the past three years exceeded $600,000 per unit. In contrast, while public data on market-rate projects are limited, interviews suggest that recently completed buildings at the high end of the market have ranged from $400,000 to $500,000 per unit.

As a result, LIHTC projects often need additional government subsidies to move forward—potentially more than $200,000 per unit over and above what LIHTC can provide. Some local funds are available for this purpose, such as the Housing Production Trust Fund in Washington, DC, but these funds are small, reflecting the budget constraints of local governments.

LIHTC fails to undo socioeconomic segregation

Research shows that growing up in more socioeconomically integrated neighborhoods improves children’s odds of upward mobility in adulthood.[6] However, LIHTC projects tend to be clustered in lower-income neighborhoods.[7] There are three primary reasons: (1) land is more readily available in these areas, (2) land is less expensive than in higher-income neighborhoods, and (3) bonus tax credits are available for developments in qualified census tracts. In middle- and higher-income neighborhoods, market prices for land are higher because of both constrained supply and the potential for profit on market-rate construction. LIHTC projects are often evaluated on overall total development cost and the bonus credits for qualified census tracts, making lower-income areas more desirable for development. In addition to tax credits, projects with lower development costs often require fewer subsidies from local governments.

The LIHTC program also discourages mixed-income housing. Mixed-income projects are eligible for the LIHTC if at least 40 percent of units are affordable at 60 percent of AMI or at least 20 percent of units are affordable at 50 percent of AMI, but many projects end up being 100 percent affordable. Since tax credits are awarded only on the affordable units but the legal and compliance costs of tax-credit financing affect the whole project, developers maximize their return on those costs by creating more affordable units. Moreover, market-rate units expose developers to a different set of risks: Whereas affordable housing tenants are very likely to move in once they qualify, market-rate tenants are more mobile, meaning the development may face higher vacancy rates. Affordable housing developers may be averse to risks like this that lie outside their area of expertise, and they may lack the broad market-rate housing portfolio to amortize those risks.

While many governments pursue inclusionary zoning strategies to encourage mixed-income buildings and neighborhoods, these well-intentioned policies can backfire by taxing new housing production and reducing new supply.[8] An incentive for developers to convert existing housing to affordable units avoids this problem and would genuinely help build integrated neighborhoods.

Although there are flaws with the LIHTC, it is unlikely that any other program could fill its role in supplying affordable housing in the near future. However, additional strategies need to be developed. Ordinarily, using existing housing units would be a less attractive option than building new housing, because new housing supply also eases competition for existing units. But the extent of the housing crisis, and the possible benefits for economic mobility, make conversion a more cost-effective option when used alongside existing strategies.

Converting Existing Housing Units to Subsidized Units

While few developers use existing housing stock to create quality affordable housing, converting existing housing into subsidized units provides a significant opportunity—without the disadvantages of LIHTC.

First, acquiring high-quality existing housing is less expensive than building new LIHTC housing today. Even high-quality market-rate properties can be acquired for less than the cost of new construction under the LIHTC, even in resource-rich neighborhoods.

Data from the real estate group CoStar show 89 sales of apartment buildings with 100 to 300 units in the Washington, DC, area over the past three years. The average price was $275,000 per unit, with those rated highest for quality selling for as much as $600,000 per unit.

These figures suggest that converting a high-quality market-rate unit into an affordable one is significantly less expensive than developing a new LIHTC building. In today’s market, all-new development is more costly because of escalating construction costs and rising interest rates. The cost differential is even wider for LIHTC buildings, given the increased financing and legal costs. Acquisition prices are based on market returns on operating income—not on the higher development costs. Subsidizing acquisitions should not increase the prices. The purpose of the subsidy is to enable the purchase at market value while utilizing the subsidy to lower rents on a certain percentage of units.

Acquisitions also move forward more quickly than new construction. Usually, an acquisition and financing process takes six months or less, compared to the three to five years needed to develop a new LIHTC unit. An acquisition process involves marketing a property, signing a purchase contract, conducting due diligence, arranging financing, and closing on the property. In most jurisdictions, there are no regulatory barriers to this process. While some jurisdictions require developers to offer current tenants right of first refusal on a purchase, this generally only delays the process by 3 to 12 months—still much faster than the new development process.

In addition, existing market-rate properties are generally located across a broader range of neighborhoods than are new, all-affordable developments, meaning that acquisitions of existing units can do more to promote socioeconomic diversity than building new. A developer could also choose to convert only some units out of a broader project, creating opportunities for income diversity within a single development. Of course, developers who convert market-rate units to affordable ones forgo profits on those units, so they likely won’t pursue the conversions without some kind of subsidy or incentive—but such a subsidy could be significantly less than that paid out for an LIHTC development.

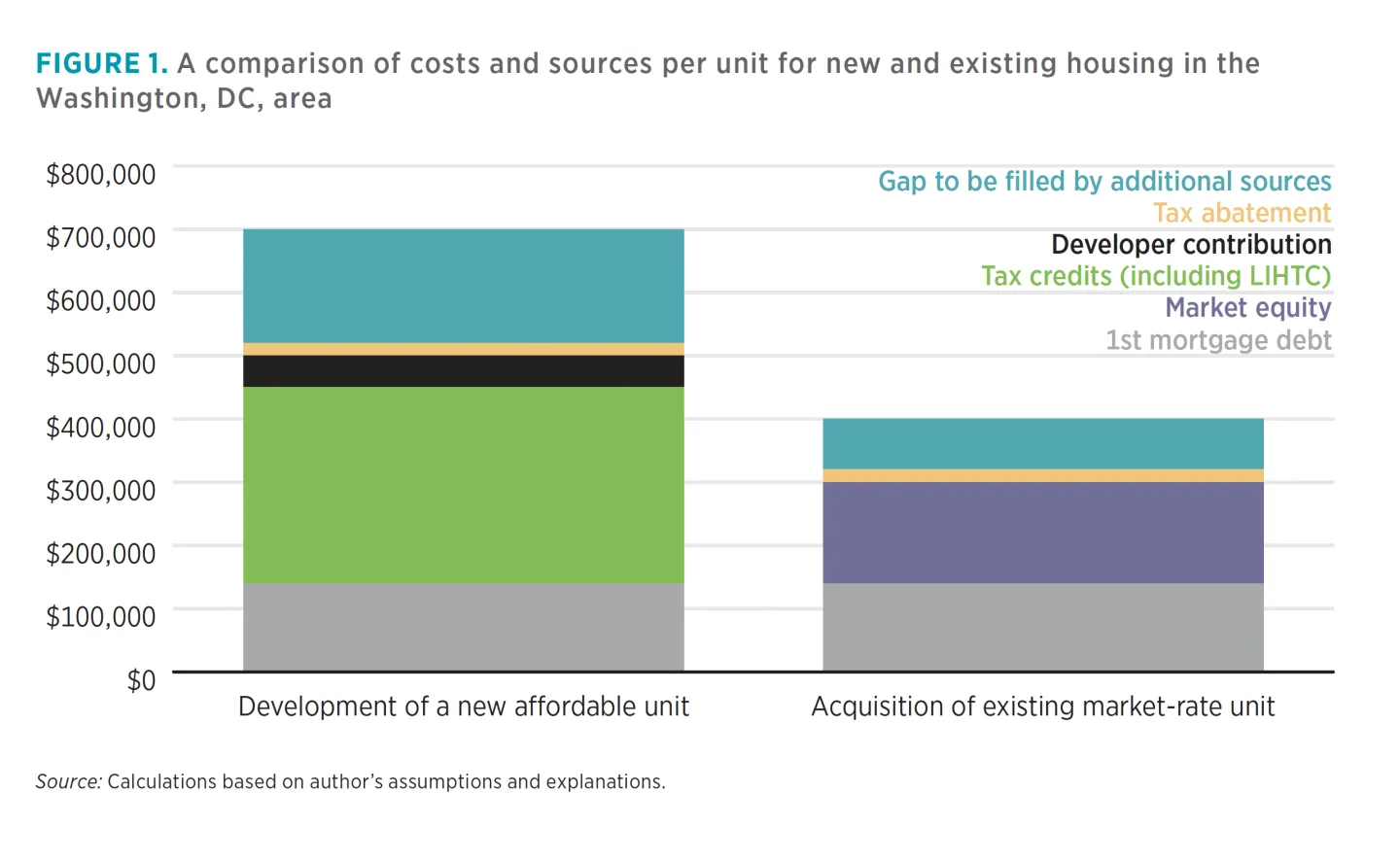

Figure 1 shows that even with LIHTC credits, new development has more of a financial gap to fill than acquisitions. Sources of funding illustrated in figure 1 are as follows:

- First-mortgage debt: Developers receive loans based on the property’s net operating income, with rents at 60 percent of the AMI, covering the debt service payments at a ratio of 1.2. For market-rate acquisitions, loans are typically larger because of higher expected rents. In this example, however, because market-rate units are being converted to affordable units, the loan size remains the same.

- Tax credits: Developers of affordable units may receive LIHTC credits as well as state credits. This example assumes the maximum realistic volume of state and federal tax credits (assuming, for instance, that the property lies within a qualified census tract). However, it also assumes the project is eligible for the 4 percent LIHTC credit rather than the 9 percent credit, which covers a significantly higher share of costs but often goes to only a few projects per year in each jurisdiction.

- Developer contribution: Developers of affordable housing contribute land or offer deferred developer fees, which they recover from future cash flow.

- Market equity: In market-rate projects, a private investor contributes market equity with the expectation of a market return.

- Tax abatement: Many local governments provide real estate tax abatements to nonprofits that provide affordable housing. This type of abatement would also be available to a developer who converted existing housing to affordable units, assuming the units were affordable at the same level as those in the new development.

- Gap financing: This represents the remaining expense that must be covered by government or other subsidized financing to make the project work.

The public sector has several tools to help developers convert existing units into affordable housing. Local governments can provide direct subsidies or low-interest financing, but this is challenging given current budget constraints. Still, governments should consider the possibility that subsidies for acquisitions could create more affordable housing per dollar than subsidies for new LIHTC development. Local governments also have the option to expand real estate tax abatements, also known as payments in lieu of taxes. These can be more feasible for cash-strapped local governments because they don’t require immediate funding. A real estate tax abatement can reduce the required subsidy by as much as $40,000 per unit.

State governments can also raise capital through bonds and lend the proceeds to affordable housing projects. The cost of capital from bonds is significantly lower than the cost of market financing. Bonds are effective tools because lenders on the project will underwrite lower expenses with smaller real estate taxes, which offsets much of the reduced income from the affordable rents.

The private and nonprofit sectors can also help. Private companies may see benefits from affordable housing in the form of more employees being able to find housing near their jobs. Most projects receive first-mortgage financing of approximately 65 percent of the total project cost; historically, financing the remaining 35 percent is a heavier lift because of the higher cost of capital. Private firms and nonprofit foundations can help bridge this gap by providing lower-cost capital. An example of this strategy is Crystal House in Arlington, Virginia. This was a market-rate property acquired by Washington Housing Conservancy. This property is in National Landing within blocks of the new Amazon HQ2. With the benefit of low-interest mezzanine debt—additional financing on real estate already subject to a mortgage—from the Washington Housing Initiative and Amazon, the 800-unit property was acquired by the conservancy, which converted 50 percent of the units to incomes restricted to 50 and 80 percent of median.

Conclusion

The LIHTC plays an important role in providing new affordable housing in the United States. However, given the scope of the housing crisis, local governments should supplement the LIHTC with their own policies, which may be able to make the process of creating affordable housing more efficient and less dependent on the federal government—and less vulnerable to slowdowns in construction such as those seen in today’s economy

One such strategy local jurisdictions can pursue is incentivizing the conversion of existing market-rate properties into affordable housing through tax abatements and payments in lieu of taxes. These incentives are less expensive than the subsidies for new LIHTC projects and better promote economic mobility.

Private companies and foundations also have an essential role to play by providing impact capital on existing properties. There has been an increase in impact capital through larger investment funds. Foundations have a mission focus and benefit from the impact focus, while private companies benefit from increased workforce housing stock for their employees. Properly deployed, this could have a significant impact on creating new, affordable units. Historically, foundations have been less involved in housing, but their needed return thresholds are lower and could be a good fit for affordable housing.

At the same time, local governments must also remember that increasing the overall supply of housing, whether affordable or market rate, is essential to lowering rents. A holistic strategy for housing affordability should also include policies that reduce barriers to new construction, such as simplifying the entitlement process to make it clearer and modifying inclusionary zoning mandates that may limit project feasibility. Encouraging more market-rate development is especially important, as today’s market-rate units often become tomorrow’s naturally affordable or workforce housing.

The affordable housing crisis needs creative solutions beyond historic tools. Public, private, and nonprofit actors all have roles to play. Employing these policies can go a long way in remediating this national crisis.

About the Author

David Roodberg is a recognized leader in affordable and workforce housing and currently serves as CEO of DJR Associates. He previously spent 20 years as CEO of Horning, a multifamily real estate owner and developer, where he led nationally recognized community impact initiatives. He also served as president of the Menkiti Group. Roodberg sits on the boards of the Washington Housing Conservancy, DC Policy Center, Martha’s Table, and Greater Washington Community Foundation. His past roles include board service at Wesley Housing and membership on the Washington DC Housing Production Trust Fund Advisory Board. Roodberg is committed to finding innovative solutions for housing affordability in the United States. He holds an MBA from the University of Michigan and a BS from Duke University.

Notes

[1] Harvard Joint Center for Housing Studies, America’s Rental Housing 2024 (Harvard University, 2024), 3, https://www.jchs.harvard.edu/americas-rental-housing-2024.

[2] Everett Stamm, “An Overview of the Low-Income Housing Tax Credit (LIHTC)” (Fiscal Fact No. 722, Tax Foundation, August 2020), https://taxfoundation.org/research/all/federal/low-income-housing-tax-credit-lihtc/; Corianne Payton Scally, Amanda Gold, and Nicole DuBois, “The Low Income Housing Tax Credit: How It Works and Who It Serves” (Research Report, Urban Institute, July 2018), https://www.urban.org/research/publication/low-income-housing-tax-credit-how-it-works-and-who-it-serves.

[3] US Department of Housing and Urban Development, “Low-Income Housing Tax Credit (LIHTC): Property-Level Data” (dataset), last updated May 5, 2025, https://www.huduser.gov/portal/datasets/lihtc/property.html.

[4] Steve Thompson, “These Publicly Funded Homes for the Poor Cost $1.2 Million Each to Build,” Washington Post, June 6, 2025, https://www.washingtonpost.com/dc-md-va/2025/06/06/these-publicly-funded-homes-poor-cost-12-million-each-develop/.

[5] Emily Wishingrad, “This Week’s D.C. Deal Sheet: 100-Unit Affordable Project Gets Financed,” Bisnow, January 31, 2025, https://www.bisnow.com/washington-dc/news/deal-sheet/this-weeks-dc-deal-sheet-127834.

[6] Raj Chetty and Nathaniel Hendren, “The Impacts of Neighborhoods on Intergenerational Mobility,” Quarterly Journal of Economics 133, no. 3 (August 2018): 1107–62.

[7] Casey J. Dawkins, “Exploring the Spatial Distribution of Low-Income Housing Tax Credit Properties,” US Department of Housing and Urban Development, Office of Policy Development and Research, 2011, https://www.novoco.com/public-media/documents/hud_dawkins_exploring_lihtc_assisted_housing_.pdf.

[8] Emily Hamilton, “Inclusionary Zoning Hurts More Than It Helps” (Mercatus Policy Brief, Mercatus Center at George Mason University, 2019, updated 2021), https://www.mercatus.org/research/policy-briefs/inclusionary-zoning-hurts-more-it-helps.