- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

COVID-19 Pandemic, Direct Cash Transfers, and the Federal Reserve

The economic fallout from the pandemic of COVID-19 is likely to be large. Entire portions of the US economy are shutting down, and some forecasters are predicting that GDP will contract as much as 10 percent in 2020. Jason Furman, former chair of the Council of Economic Advisers for President Obama, believes the contraction could be even worse and surpass the depths of the Great Recession of 2007–2009. As a result, many are calling for a large government response, including direct cash transfers to households. There appears to be growing momentum for such programs, with Republican and Democratic senators calling for direct cash payments to households for the duration of the crisis. Even the White House is seriously considering this option.

At the same time, the COVID-19 shock has accelerated the decline of interest rates to the point that it is impairing the ability of the Federal Reserve (Fed) to function. The Fed implements monetary policy by adjusting interest rates, both its overnight interest rate as well as longer-term interest rates, via large-scale asset purchase programs. Interest rates were already falling, but the COVID-19 shock simply hastened the decline by pushing the entire yield curve of interest rates close to 0 percent. The Fed’s operating framework, however, was designed for a positive interest rate environment with lots of space to cut interest rates. The Fed, in short, is becoming increasingly impotent at the very moment the economy needs it most.

Ironically, these growing calls for direct cash transfers and the mounting weakness of the Fed may be the very catalyst that brings about a much-needed overhaul of the Fed’s operating framework. Over the past few years, some observers have been warning that the Fed needs to update its operating framework to include a level target and the ability to implement direct cash transfers in special situations like the current crisis. They make the case that it is better for the Fed to provide any direct cash transfers because it is nimbler and more likely to do so in a rules-based manner.

That time has come, and this policy brief shows how to ensure that the overhaul of the Fed’s operating framework can provide powerful countercyclical policy in a manner that is both systematic and based on rules. The overhaul consists of three main steps: First, the Fed needs to adopt a two-rule approach to monetary policy so that it can handle both positive and negative interest rate environments. Second, the Fed needs to adopt a nominal GDP level target so that it can stabilize dollar incomes and make up for past misses in its target. Finally, the Fed needs to be given a standing fiscal facility so that it can do direct money transfers, or “helicopter drops,” to households once interest rates hit 0 percent. This feature cuts out the “middleman” of monetary policy during severe economic downturns. These three steps are outlined in greater detail in this policy brief.

A Three-Step Plan to Overhaul the Fed’s Operating Framework

The Fed’s operating framework—defined here as the instruments, tools, and targets the Fed uses in its conduct of monetary policy—is need of an overhaul, and the overhaul suggested here keeps the Fed as the main institution doing countercyclical macroeconomic policy. Because the public already views the Fed as playing this role, this feature would provide continuity. To make this happen, the overhaul requires the following three steps.

Step 1: The Fed Adopts a Two-Rule Approach to Monetary Policy

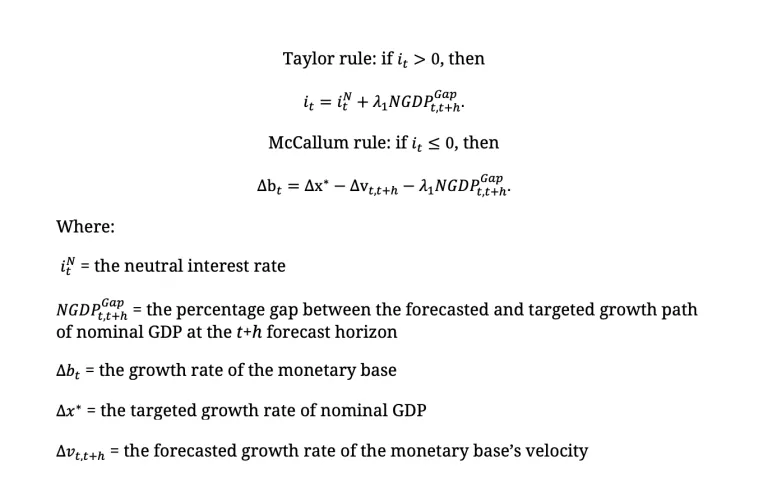

This first step would make the Fed’s operating framework robust to both positive- and negative-interest-rate environments. Specifically, the Fed would follow a version of the Taylor rule when interest rates are above 0 percent, since this rule uses an interest rate target as the instrument. The Fed would follow the McCallum rule when interest rates are at 0 percent or less, since this rule uses the monetary base as the instrument. The McCallum rule, consequently, would govern how the Fed conducts its helicopter drops and when tapping the standing fiscal facility. This two-rule approach to monetary policy would be explicitly added to the Federal Open Market Committee’s Statement on Longer-Run Goals and Monetary Policy Strategy, so that the public would clearly understand when and under what circumstances the Fed would use each rule.

Step 2: The Fed Adopts a Nominal GDP Level Target

The second step would have the Fed switch to a target that aims to stabilize the growth path of total dollar spending in the economy. This approach, known as nominal GDP level targeting (NGDPLT), has several advantages over the Fed’s current inflation target. First, NGDPLT stabilizes the growth of household and business incomes, since for every dollar spent there is a dollar earned. Consequently, by stabilizing total dollar spending, NGDPLT actually stabilizes total dollar income growth. This is an invaluable feature during crisis periods, such as the current one, since it keeps dollar incomes in line with previous expectations of dollar income growth. To be clear, NGDPLT does not prevent the economy from getting poorer. It does, however, prevent secondary spillover effects that can arise from a sudden drop in household and business income, such as an inability to make mortgage payments and payrolls.

The second advantage of NGDPLT is that it makes up for past misses. That is, if total dollar spending were to fall short of the Fed’s target, that shortage would be made up for in subsequent periods. If credible, this target would minimize the tendency for households and businesses to panic in a crisis, since NGDPLT creates expectations of stable dollar income growth. NGDPLT, in short, provides a beneficial makeup policy and has a calming effect on markets.

This policy brief follows the suggestion of economist Lars Svennson that the Fed should target forecasts and calls for a forecast version of a nominal GDP target. That is, the Fed should aim to guide the forecast of nominal GDP to its targeted growth path. Given these first two steps, the Fed’s two-rule approach to monetary policy can be stated as follows:

|

The first equation, the Taylor rule, says that if nominal GDP is expected to rise above its target, then the Fed should raise interest rates, and vice versa. It is only used when the overnight target interest rate is greater than 0 percent. The second equation, the McCallum rule, says that the Fed should grow the monetary base at a pace equal to the targeted growth rate of nominal GDP less the expected velocity growth rate less the size of the nominal GDP gap. That is, all else equal, if nominal GDP is expected to rise above its target, then the Fed should lower the growth rate of the monetary base, and vice versa. It only kicks in when interest rates are at 0 percent or less.

Step 3: The Fed Gets a Standing Fiscal Facility

The final part of the operating framework would establish a standing fiscal facility for the Fed to use when doing helicopter drops. Specifically, the “Stella Fiscal Facility” (SFF) is proposed—named after Peter Stella’s suggestion to institutionalize the US Treasury’s Supplementary Financing Program that was used in 2008 by the Fed to help manage its balance sheet. Stella proposes the SFF as way for the Fed to shrink its large balance sheet, but it can also be used to help facilitate the Fed’s helicopter drops. Its use would be triggered when interest rates hit 0 percent and would be regulated by the McCallum rule, as outlined earlier. Also, I propose that its use should be approved by the Treasury secretary every time it is used. This would make the Fed’s use of helicopters drops, a form of fiscal policy, more accountable to the public.

Operationally, the SFF would create Treasury securities that would be deposited at the Fed. This increase in Fed assets could then be matched by an increase in Fed liabilities that are issued to the public via the McCallum-rule-governed helicopter drops. Since these special Treasury securities would be held only by the Fed, they would not count toward the debt ceiling. The funds would be dispersed to households via the existing IRS tax refund infrastructure. The direct transfer of money to households at 0 percent is a useful feature, since traditional monetary policy transmission through the financial system often breaks down or gets clogged in a severe recession. Helicopters drops, in short, cut out the middleman of monetary policy when it is most expedient to do so.

Advantages of This Operating Framework

This proposal has many advantages over the current operating framework and should be seriously considered by Congress and the White House. First, as noted earlier, it is robust in positive and negative interest rate environments. No matter what happens to interest rates, the Fed can still provide meaningful countercyclical monetary policy. Second, this operating framework reduces the likelihood of recessions because it provides powerful forward guidance through a nominal GDP level target. Specifically, if households and firms believe that the Fed will always correct past misses in its targeted nominal GDP growth path, then they have less incentive to drastically change their spending in the first place. Third, the SFF gives NGDPLT the full backing of the government’s consolidated balance sheet and creates credibility for the Fed’s actions. Fourth, in severe economic downturns this approach cuts out the middleman, and money can therefore be sent directly to households. Finally, the operating framework as outlined earlier would be implemented in a rules-based approach that includes the sign-off of the Treasury secretary when the SFF is tapped. This makes the Fed more predictable, systematic, and accountable to the public.

To be clear, this proposal is a radical departure from the current operating framework and would require congressional approval. Compared to the status quo, though, this approach is a bargain. For if no changes are made to the Fed’s operating framework, the Fed is likely to be ineffective in the current and future recessions and thereby force the use of ad hoc fiscal policy. The proposal outlined here provides a way to employ fiscal policy in an effective and nimble manner while keeping the Fed as the main countercyclical government agency.

Conclusion

This brief outlines a much-needed overhaul of the Fed’s operating framework. First, the Fed should adopt a two-rule approach, so that it can handle both positive- and negative-interest-rate environments. Second, the Fed should implement NGDPLT, so that dollar income growth can be stabilized. Finally, the Fed’s operating framework needs the enhanced credibility and power that comes with granting the Fed limited access to a standing fiscal facility.

This brief also proposes how to accomplish these goals and encourage the Fed to act in a systematic, rules-based, and accountable manner. This proposal is also timely, given the severity of the COVID-19 shock to the US economy and the growing calls by many in Congress for direct cash transfers to households. Such programs need to be conditional and tied to specific goals. This proposal provides a way to do direct cash transfers in a systematic and rules-based way.

The coming recession probably will turn out to be one of the sharpest downturns on record. The Fed is not equipped to handle this crisis in its current state. Hopefully, this policy brief will encourage discussion on these shortcomings and impress upon policymakers the need to upgrade the Fed’s operating framework.