Midyear is approaching, stimulus money is flowing, and the share of the US population receiving virus vaccinations is soaring. Finally, the US economy is showing some blue sky. On April 29, the Bureau of Economic Analysis’s first estimate for Q1 2021 GDP growth came in with an exceptionally strong annual growth rate of 6.4 percent. This followed Q4 2020’s 4.3 percent annual growth and the explosive Q3 2020 bounce of 33.4 percent. Though 6.4 percent growth is strong, it would have taken 10.0 percent growth to close the gap between the current GDP level and the prepandemic, Q4 2019 level. But America is getting there. A few days before the GDP growth announcement, the Conference Board’s April consumer confidence index, after gaining across the previous four months, hit 121.7. (A reading above 100 indicates growth.) There was still a way to go to hit the prepandemic, February 2020 132.6. But it felt good.

As table 1 shows, upward revisions of GDP growth forecasts are the order of the day. I note that the Wall Street Journal and Wells Fargo forecasts are the most recent, having been made in April and May, respectively, whereas the Congressional Budget Office and Philadelphia Fed forecasts were made in February. The International Monetary Fund, in its April World Economic Outlook, calls for 6.0 percent growth for the world economy, up from its 5.5 percent January forecast. Powerful annual numbers like these haven’t appeared since 1983, when the real GDP growth tally was 7.9 percent.

After all the pandemic misery, has America somehow entered an exceptional high-growth era that will continue till mismanagement or misfortune brings an end to it? Is the strong GDP growth the result of massive stimulus spending and fear-reducing vaccinations? Or is something else going on? And given the return to far better times, does this mean America will pay for part of the prosperity with inflation?

How This Report is Organized

This report will deal with these important questions and more. The next section looks closely at an economy that seems to be finding a new footing after having been pushed from its growth path by the pandemic and resulting shutdown policy actions. The first main section uses the production possibilities frontier, a common tool in economics, to illustrate what may be happening and what one may expect. Drawing on data, different metrics, and theory, that section also addresses the inflation question. The section concludes with the notion that higher inflation is already here but that one should not expect to see serious Federal Reserve (Fed) braking problems over the next two years.

The report’s second section focuses on how the Biden administration has characterized all the problems and challenges America faces as crises. That section asks, Are Americans a crisis-ridden people, or is what they are hearing and seeing primarily political rhetoric? One way or another, Americans are observing major “Bootlegger and Baptist” forces combining to support high growth in federal regulation. The Baptists call for action to make the world a better place for hardworking families that have been hurt by the pandemic and by growing income inequality; and the Bootleggers look to make money from such things as federal subsidies directed toward electric cars, batteries, an expanded electricity grid, and expanded internet access.

The next section, partly with a wink and smile, offers some advice on how to eliminate the unfortunate behavior of elected and appointed officials who may be tempted to make money using confidential information available to them. I say with a wink and smile, but I hope that my proposal will be taken seriously by those who are truly serious about limiting such behavior. After that, as always, is a state spotlight section—this time looking at Alabama—followed by Yandle’s reading table.

Turning the Corner at Midyear

Yes, the economy is showing strong signs of life. To be sure, most of the projected high growth is being generated by a stimulated economy returning to the path it was traveling when the COVID-19-induced shutdown knocked its engine into a ditch. Powered up by trillions of stimulus dollars, with wheels spinning and then accelerating, it’s ready to quickly pick up speed. It’s just impossible to inject into the economy more than four trillion dollars of purchasing power without making something happen. President Biden’s promised $1.9 trillion stimulus bill was signed in March; the payments included, now on the way, add to the $900 billion passed by Congress in December and the $2.5 trillion sent to Americans by the Trump team in 2020. These stimulus expenditures sum to 27 percent of GDP, more than four times the stimulus applied to counter the 2008 recession.

But there is almost this much again being pushed in the form of President Biden’s $4.2 trillion infrastructure spending proposal, now divided into two packages—the American Jobs Plan and the American Families Plan. Unlike past stimulus actions, which immediately put money into peoples’ checking accounts, the Biden proposal calls for actions to be spread over years, if not decades. Of such dramatic proportions as to be compared with Lyndon Johnson’s Great Society or Franklin D. Roosevelt’s New Deal, the proposal covers massive efforts that deal with everything from highways, bridges, high-speed rail, electric vehicle charging stations, nationwide broadband availability, improved drinking water, upgraded manufacturing, and subsidies for the production of electric automobiles to an expanded electric grid, improved housing, upgraded day care facilities, freely provided two-year preschool programs, and tuition-free community college programs.

Neither the full dollar magnitude nor the extensive list of expanded federal programs will likely survive the legislative battles required for the plans to become law. This said, one can still be certain that a jumbo action will further extend the federal government’s reach into most every aspect of life. The expansion of government programs is huge, and, with greater than 6 percent GDP growth expected for 2021, can no longer be described as necessary for dealing with a national emergency, though national politicians might feel differently.

Enlarged federal government activity is now simply what the country can expect from an expanding welfare state. Facing economic challenges in 1971, Richard Nixon deliberately rejected his avowed free market philosophy and imposed wage and price controls and ended convertibility of the dollar to gold. It was then that he is quoted as saying, “We are all Keynesians now.” With the exception of Ronald Reagan, President Nixon may have been the last White House occupant who wondered about the relative merits of intervening in the nation’s market-driven economy. Indeed, no one speaks of intervening anymore. There is just one large political economy to be nudged, managed, manipulated, and possibly controlled by politics.

Moving beyond stimulus programs and their effects, part of the current GDP growth America is experiencing is akin to experiencing a brief war and then regaining footing in a world that looks different than before. What happens was described by economist Mancur Olson in his 1982 book, The Rise and Decline of Nations. Counterintuitively, as Olson argues, many nations that lose wars come back stronger than those that win. Yes, they are worse off from having lost human and physical capital, so war is not a paying proposition. But once the war is passed, the losers generally rebuild with the latest vintage capital, discover new leadership, and establish new social networks. Prior good ole boys are replaced with a fresh set. Out of necessity, they become more productive.

In America’s case, the country is engaging with a new postpandemic (one hopes) economic turnpike. As Fed Chair Powell put it recently, “We’re not going back to the same economy.” While the economy was in the ditch, new discoveries were made about organizing virtual offices, schools, and healthcare provisions. The country saw breakthroughs and huge investment increases in information technology. New distribution channels emerged, and warehousing became more efficient. Some regulations were wiped off the books, and people learned they could accomplish a lot without traveling as much as they did before the COVID-19 collision. For some, the cost of doing business went down.

The Production Possibilities Frontier

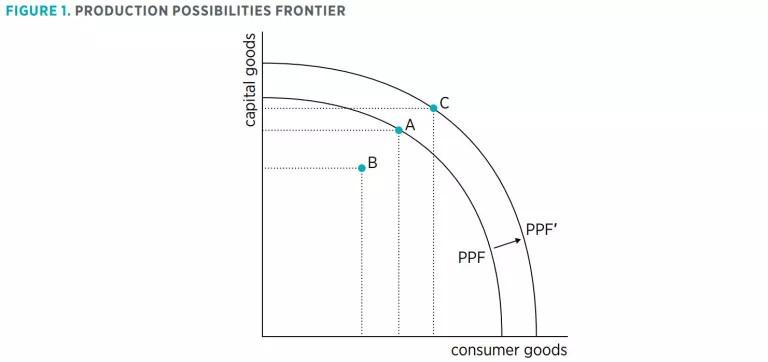

It is helpful to picture the situation by thinking about what economists call the production possibilities frontier (PPF). In figure 1, the curve labeled PPF shows the limits of production for a fully employed economy when viewed in terms of just two goods—say, capital goods and consumer goods. It is possible to move along the line and produce different combinations of the two goods, or to move below the line, from, say, point A to point B, by producing less. But it is impossible to move above the line, to point C, and produce more without a change in the available resources or improved production techniques.

When the pandemic hit, America moved below the line. The economy slipped inside the PPF and continued operating at a lower level of output. But by slipping inside the curve, a lot was learned about how to reconnect a disrupted economy. By necessity, people figured out how to do some things differently and at lower cost.

This means that the entire tragic episode may bring a wee bit of economic sunshine, shown in figure 1 as the curve moving outward to PPF'. Such a scenario would entail significant gains for the United States in labor productivity that will pay off in the future. But there are two downsides to consider. The first is that, because of disincentives associated with continuing income transfers, there will be a slow return from B to A and an unlikely move to C. The second downside applies to unskilled workers with less than a high school education: because of the evolving high-tech economy, they will face an even more difficult challenge in getting connected to a changing postpandemic economy. So while GDP growth may accelerate at an unusually high pace for a while, there will be pockets of frustrated people who will feel left behind, because they are.

Will Inflation Fires Be Fueled?

When an accelerating economy is combined with (or partly caused by) vast increases in printing press money, historically, inflation is the unsurprising result. As a result of stimulus programs and restrictions on shopping, American consumers have built up trillions of dollars in checking accounts. Pandemic fear is being reduced by widespread vaccination programs, retail spending is on the rise, and the economic landscape is peppered with help wanted signs. March employment data showed a remarkable turnaround in food service hiring, and March wages overall were up 4.2 percent on a year-over-year basis. It is not unreasonable to think that rising wages will translate into a growing price level, given the amount of money capable of circulating in the economy, and that is what Americans are beginning to see. In March the Producer Price Index rose—you guessed it—4.2 percent.

There is more than $4 trillion in stimulus money working its way through the economy, with more on the way via President Biden’s infrastructure program. As American Enterprise Institute economist Desmond Lachman points out, this means that the US economy will receive a total stimulus of more than 13 percent of GDP in 2021 alone. Going further, without offering an estimate of what America may expect for inflation, Lachman notes that “this amount of budget stimulus alone is bound to lead to considerable economic overheating later this year that must be expected to result in an unwelcome acceleration in inflation as aggregate demand well outstrips aggregate supply.”

Lumber leads in the materials price increase, but the moves higher are widespread, including diesel fuel as well. As expected, the March Consumer Price Index (CPI) responded with a 2.6 percent increase, the largest since August 2018. Excluding food and energy to reveal the so-called core inflation rate, the number falls to an annual increase of 1.6 percent—but obviously, food and energy are necessary for consumers to live and keep operating. I note that gasoline prices were up 22 percent from the year before. Unfortunately, though, the pandemic has affected inflation calculation. For example, one knows that the January S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index rose more than 11 percent in the past year. But housing prices are not reflected in the CPI because they are a capital investment. With higher-priced housing, one should expect to see higher rents, which are included in CPI calculations. But COVID-19 restrictions on landlords’ ability to discharge nonpaying renters has also affected the numbers used to measure inflation.

Does America have budding inflation that will likely get worse, or is it observing an acceleration that is just offsetting the deceleration that came in mid-2020 with the pandemic, when driving and energy use collapsed and food and other prices collapsed too? The Wall Street Journal’s April economists’ survey offers a 3 percent CPI growth forecast for June, which falls to 2.6 percent in December. However, I suggest that America is observing a growing inflationary trend, not something temporary. Americans obviously need more information to make a firm judgment. Part of that information is interest rates, which tend to capture inflation expectations determined across world markets. But first, one should look closely at some inflation gauges maintained by Fed district banks.

Consider the Federal Reserve Bank of New York’s monthly Underlying Inflation Gauge and that gauge’s “prices only” component, which is based on movement of several hundred domestic prices as well as prices for imports and exports. In March 2021, the gauge registered 2.6 percent inflation, the same as the March CPI but up from 2.2 percent in January. Then there is the Federal Reserve Bank of Atlanta’s Business Inflation Expectations, which estimates based on surveys of what businesspeople expect to see one year ahead. The April 2021 Business Inflation Expectations pointed to 2.5 percent inflation. In January 2021, the respondents expected to see 2.2 percent inflation. I note again that the March CPI was up 2.6 percent.

Finally, one might look closely at the gap between the yield on the 10-Year Treasury Note Constant Maturity rate and the 10-Year Treasury Inflation Protected Securities (TIPS) Note, which provides an inflation-adjusted yield. The resulting gap is an estimate of inflation expectations 10 years out. Recent examination of the data suggests that investors expect to see 2.33 percent inflation across the next 10 years. This is up from 2.01 percent on January 4.

In summary, all of these measures of current and expected inflation coupled with the data discussed earlier show that America may see 2.50 percent to 3.00 percent inflation in the next few years.

What Does Inflation Theory Tell Us?

An early theory of inflation focused on the equation of exchange, an identity that says that the amount of money circulating in the economy multiplied by its velocity (the number of times each dollar turns over in a time period) yields the dollar value of the GDP. If the amount of money in the economy increases and velocity remains unchanged, the dollar value of GDP rises, even if the real value of GDP doesn’t budge. That’s what one calls inflation. Put another way, increases in the supply of money form the basis of future price increases. In fact, that is where the term “inflation” originates; it is an inflated money supply that brings a rising price level.

What can one say about the amount of money that has flowed into the economy in, say, the past year? And what can one say about the speed with which the money is flowing? The answers are plenty. A quick look reveals that there are trillions of stimulus dollars being held back, like water behind a dam, sitting in individuals’ bank accounts and in reserves held by commercial banks with the Federal Reserve system. With expanded vaccinations, increased hiring, and rising overall economic activity, those balances will begin to be drawn down. But at this point, the Q4 2020 velocity for a fundamental measure of the money supply, M1 (which includes savings, demand deposits, and currency in circulation), stands at 1.20, this again is the number of times a dollar turns annually in the economy. In Q1 2020, the ratio was resting on the edge of a statistical plateau reading 5.20. The value had fallen slowly from 8.40 in 2010.

So here’s the bottom line: all of the ingredients are in place for Americans to see accelerating inflation across the next year. The early stages of the increase are visible now. As velocity picks up with increased consumer spending, more will appear. Instead of 2.6 percent CPI growth, America should see 3.0 percent by the end of 2021. The important question is, Will the breakthrough continue? Those who say no point to the fact that the pandemic brought falling prices and that the changes today represent a kind of catching up. Those who say yes point to the huge increase in the money supply generated by printing stimulus money and argue that even higher levels of inflation are in the works. At this point, I stand with those who expect to see higher inflation numbers across the next couple of years.

Are Americans a Crisis-Ridden People?

As President Biden sees things, we Americans are beset by multiple crises. Some are existential—we either fix them or get wiped out. How do I come to this dark conclusion? By reading a recent series of statements, speeches, and briefings posted on the White House website. The official rendering identifies what are far more than just serious problems to be dealt with—they are “crises.”

Without discounting any of the challenges America faces, one should consider how Americans communicate with one another. Calling every important issue a crisis can feed into feelings of hopelessness, and can even lead to an excess reliance on federal action and government in general.

According to some of the presidential statements, America faces a “hunger crisis,” an “affordable care crisis,” a “housing affordability crisis,” and an “economic crisis.” To make matters worse, other statements point out Americans must deal with a “global refugee crisis,” a “gun violence crisis,” and, when it comes to dealing with problems along the Mexican border, a “humanitarian crisis.” Americans knew all along that they were facing a COVID-19 crisis. The crisis rhetoric continues to include climate change, microchip shortages, and supply chain problems. From all indications, “we the people” don’t just have problems, disappointments, recessions, depressions, or plain-old tough times anymore. Americans are a crisis-ridden people.

Why is it in a politician’s interest to speak officially and formally in such extreme terms?

First, each problem President Biden refers to is very real. People are hurt when they cannot afford homes, when they cannot afford healthcare, or when they cannot find jobs, to say nothing of violence or disease. When auto producers shut down owing to shortages of computer chips, thousands of workers and auto customers suffer. And of course, those seeking entry at America’s southern border are not just hungry and weary, but in many cases desperate. For each person facing one of the problems just noted, the situation is a personal crisis. Each beset person hopes for a remedy. The question—which is perhaps unanswerable—is where the line exists between personal and industry disasters and a national crisis.

Next, if all such severe problems are crises, how can one differentiate among problems and order priorities for dealing with them? Does every problem get ranked priority number one?

Surely, if enough people agree when a spokesperson says the sky is falling, they will organize to respond. It’s easier to attract others to join the effort by speaking in such terms. Making extreme statements can be politically rewarding.

The fact that crises, real and not so real, prompt citizens to look for and support political solutions is both understandable and concerning. Past national crises have given rise to major federal programs—even departments—that have flourished and expanded long after the originating crisis subsided. We have the US Department of Energy, the US Department of Education, the Consumer Product Safety Commission, the Occupational Safety and Health Administration, and the US Department of Homeland Security.

One can debate their merits, but each finds its origins, at least partly, in the emergence of serious problems that led to calls for a federal remedy—though not necessarily for a permanent White House cabinet position. Of course, once a specialized agency is established and operating, new problems and crises seem to emerge more readily.

For example, the US Department of Energy was formed in 1977, after President Carter referred to the Arab oil embargo as the moral equivalent of war. Immediately, the new agency launched a vast synfuel project, which in 1980 became the Synthetic Fuels Corporation. Until being abandoned in 1986, the costly corporation, which spent nearly a billion dollars, was fraught with its share of crises.

As economic historian Robert Higgs notes in his classic, Crisis and Leviathan: Critical Episodes in the Growth of American Government, politicians have a pronounced tendency to recognize crises as a basis for political remedies that become a permanent part of the government enterprise. In that sense, pointing to every problem the country faces and calling it a crisis can be costly going forward. Indeed, a leviathan tendency may be developing now as result of supply chain challenges that developed partly because of pandemic shutdowns and uncertainties.

Supply Chain Review

In late February, President Biden—motivated perhaps by difficulties obtaining protective medical gowns and masks during a pandemic and a recent semiconductor shortage that disrupted American auto production—signed an executive order calling for an across-government, 100-day review of supply chain performance for a number of critical items and sectors.

Is President Biden’s order merely about broken links in supply chains from the past year? Or about “reshoring” production now concentrated in China and Russia? Or is it about accomplishing bigger goals, even dealing with global climate change? In any case, it sets in motion a host of federal agencies that can each be a supplier of regulation. Will America look back and see a prelude to a regulatory surge?

When the order was signed, somewhere in the background were rent-seekers who would love to have the White House use its dictatorial powers to shift some valuable resources in their direction or skew the regulatory chess board away from their competitors. For example, Matt Blunt, president of the American Automotive Policy Council, said one way to help with the current chip crunch would be for the government to give priority to the auto industry. Echoing Blunt, Ford CEO Jim Farley called on the government to support battery production and EV charging infrastructure. Blunt said, “We need to bring large-scale battery production to the United States. We can’t go through what we’re doing now with chips.” The Defense Production Act gives the president just that authority, meaning demanders of regulation will be interacting with the suppliers as the process unfolds.

Biden is not the first president to seek to do something about supply chains. It’s a perennial problem. In a trade-enriched world of global markets and extreme specialization, any faction hoping for a more self-sufficient nation—which essentially prioritizes existing jobs and wages over newer jobs and lower prices—will always be engaged in a political struggle. This is part of the reason why tales of the impending doom wrought by unencumbered world trade are ever present.

After all, specialization means that Americans will always need some critical product that is produced somewhere else. The same goes for America’s trading partners. The struggle to upend a robust trading system—where each country focuses on what it does best and uses the gains to acquire the rest—can end up making things worse, or at least costlier.

The Biden review focuses on semiconductors, pharmaceuticals, electric vehicle batteries, and critical minerals used in manufacturing products such as cars and weapons. And if that is not enough to keep government senior executives busy, the major industrial sectors to be examined are defense, public health and biological preparedness, information and communications technology, energy, and supply chains for agricultural commodities and food production. One would be justified in wondering what else is left.

Yet there is still more. Reaching gargantuan proportions, the review “will identify opportunities to implement policies to secure supply chains that grow the American economy, increase wages, benefit small businesses and historically disadvantaged communities, strengthen pandemic and bio-preparedness, support the fight against global climate change, and maintain America’s technological leadership in key sectors.”

Wow!

If this job is done in just 100 days, Americans will arrive in a supply chain wonderland. They will also be forced to carry some excess regulatory baggage once they get there. This, at least, is what past experience teaches.

What about Past Experiences?

In the late 1970s, oil embargoes created a severe US crude oil supply chain problem. In addition to regulating fuel economy standards for automobiles, regulating energy efficiency for appliances, rationing gasoline, and searching for alternative forms of energy, the federal government decided to squirrel away enough oil to counter another interruption. Pumped from the earth in one location and back in another, there are now 637 million barrels stored in Louisiana salt mines—enough to supply America’s consumption for a month. Along the way, America itself became the world’s leading crude oil producer. It turned out to be an insurance policy that did not have to be redeemed. Who knows? In a world longing for renewable energy, the reserve may sit there forever.

In the early 1980s, the supply chain problem had to do with strategic minerals and rare earth elements that came from other countries. America now has a federal stockpile of 37 strategic minerals valued at more than $1 billion.

Later in the 1980s, “Japan, Incorporated,” as it was then called, was the supply chain challenge. Japan’s Ministry of International Trade and Industry seemed to be outsmarting the rest of the industrialized world. They were picking winners and directing large amounts of investment into gigantic factories that, as first movers, would underprice global competitors and gain monopoly power. At least, that was the evening news version. America was thought to be in a losing race.

To fix things, federal coordination was summoned. America, the world leader in chip design, could not be allowed to fail. In 1982, an assistant secretary of commerce for productivity, technology, and innovation was named to lead the effort.

Later, America would learn that Japan wasn’t invincible after all. Instead of picking winners—for example, the Ministry of International Trade and Industry turned away the burgeoning Japanese auto industry as not worthy of support—they ended up with some losers.

America motored on, but not without spending big bucks on SEMATECH, a government-sponsored nonprofit R&D consortium of 14 semiconductor producers subsidized for five years by the US Department of Defense. As some industry insiders see it, the overall effort was successful, but it led US firms to design products domestically and locate their high-volume production elsewhere, especially in Asian countries. It turns out it was cheaper that way. Oops!

No, the Biden administration’s recognition that America has supply chain problems is not in any way novel. In fact, it’s business as usual inside the Beltway. As reported by the Congressional Research Service in June 2019, “President Trump and various U.S. lawmakers have expressed concerns about U.S. reliance on critical mineral imports and potential disruption of supply chains that use critical minerals for various end uses, including defense and electronics applications.” Like President Biden, Trump was specifically worried about China’s strategic behavior.

So, what is one to make of the proverbial White House trumpet blasts announcing that America, once again, faces a supply chain crisis that only an empowered federal government can solve? Is this just another chapter in a decades-long politician’s handbook about the ongoing effort to control industrial policy?

Or could this be a new handbook that shows how alleged supply chain crises can be used to pursue much broader overt goals—raising wages, bringing pandemic relief, reversing climate change, and strengthening disadvantaged communities—while simultaneously warming up the regulatory engine and satisfying rent-seekers’ demand for special-interest regulation?

This is not just about supply chains. Be on the lookout for a regulatory boom.

A Proposal to End Congressional Insider Trading: Invest in the United States!

In an effort presumably to tidy up the behavior of members of congress, Representatives Raja Krishnamoorthi (D-Ill.), Alexandria Ocasio-Cortez (D-N.Y.), Joe Neguse (D-Colo.), and Senator Jeff Merkley (D-Ore.), among others, have introduced legislation that would prohibit members of Congress and their staffs from trading individual stocks. Their Ban Conflicted Trading Act, which has also been floated in past years, was prompted by reports that members of Congress may have traded advantageously on the basis of information obtained in confidential hearings and knowledge of pending actions that could affect future corporate prospects.

The spirit of the proposed legislation—a desire to limit conflicts of interest—may be on the side of angels, but unfortunately the remedy is flawed. That being the case, I have another idea, one which, in addition to addressing the issue, may give politicians a better and more personal sense for the ramifications of their sometimes-less-noble legislating and budgeting. More on this later.

Problems with political appointees becoming engaged with efforts to line their own pockets while serving the public interest have been around a long time. The Teapot Dome case of the 1920s during Warren Harding’s administration sent a secretary of the interior to prison. The Ulysses S. Grant administration struggled with allegations of insider trading, and the Ronald Reagan administration had some 100 appointees investigated for financial misconduct. Recently, controversies involving conflicted activity arose for Senators Richard Burr (R-N.C.), Kelly Loeffler (R-Ga.), Dianne Feinstein (D-Calif.), and Jim Inhofe (R-Okla.), who allegedly sold stocks advantageously after attending specialized briefings on COVID-19 and other matters. In 2017, then-Representative Tom Price, at the time President Trump’s nominee to run the US Department of Health and Human Services, got into trouble for investing in medical and healthcare stocks before moving to his new assignment. He resigned and disappeared from public life.

As Alexandria Ocasio-Cortez puts it in a 2020 press release about her proposed legislation, “Members of Congress should not be allowed to buy and sell individual stock . . . We are here to serve the public, not to profiteer.”

But there’s a problem with the remedy. Reflecting the mistaken belief that mutual funds are less conducive to making money through congressionally gained inside information, the proposed law does not prohibit investing in them. Only investing in individual company stocks is forbidden. But the number of mutual funds is about as large as the number of stocks listed on the exchanges. Those funds can be so highly specialized that they can perform almost in lockstep with the stock of firms that might benefit from congressional action. I think the mutual fund escape valve should be closed.

Because of this problem and the fact that I think Americans should require more of their public servants, I have another suggestion for the bill sponsors to consider, one that I learned about in 1942 when the United States was struggling to fund World War II. For the sake of discussions, consider this: why not require all federal officeholders, elected and appointed, to invest their personal portfolios in US Treasury notes and bonds? Why not require our leading public servants to invest in America?

The idea came to me as I recalled how we World War II children headed off to school every Friday with dimes and quarters we had saved or finagled from our parents to purchase War Savings Stamps. A full book of stamps worth $18.75 could lead to the ownership of a $25.00 US Treasury bond set to mature 10 years later. The effort taught us that saving money was a good idea, and we wanted to do our part to win the war.

Part of our patriotism was kindled by a wonderful 1941 Irving Berlin song, “Any Bonds Today?,” written at the request of Treasury Secretary Henry Morgenthou and made popular by Bing Crosby. The song’s key verse for children said, “Any stamps today? / We’ll be blest / If we all invest / In the U.S.A.”

So instead of getting bent out of shape about politicians succumbing to the temptation to make quick bucks in the stock market using inside information, maybe we should simply require them to invest in America’s debt, of which there is plenty. Then, as an added benefit, our elected officials would become far more sensitive to what inflation-induced higher interest rates can do to depreciate the value of government bonds.

We’ll be blest if we all invest in the USA.

Each quarter, we select one state and analyze its economic and regulatory outlook. Last quarter, we put the spotlight on Ohio. This quarter, we focus on Alabama.

Alabama is located in the Deep South. It borders Tennessee to its north, Mississippi to its west, and Georgia to its east. The Florida panhandle to the south blocks Alabama’s access to the Gulf of Mexico, except for the very southwestern corner, where Mobile Bay serves as Alabama’s main (and only major) port. Despite this limited access to the Gulf of Mexico, Mobile Bay is the 12th most trafficked US port by tonnage. The state is 52,420 square miles in size, with a population of about 4.9 million and a population density of 95 people per square mile. These statistics are all right near the average for the United States. The southern range of the Appalachian Mountains stretch into the northern parts of Alabama, while the center of the state boasts a prairie land with rich fertile soils, which eventually give way to forests and then coastal plains in the south. These soils combine with a temperate climate, generous even rainfall, and an extra-long growing season to make the state excellent for agriculture.

Alabama’s agricultural propensity has shaped both its economic history and its long and painful racial and political history. The territory came into US possession in pieces through various treaties with European colonial powers as well as major deportations of the native population. From statehood in 1819 until the outbreak of the civil war in 1860, Alabama was the prototypical slaveholding, cotton-producing southern state, with roughly half of its population being made up of enslaved black individuals and nearly all of its population being rural. Under the sharecropping system that emerged after the war, Alabama’s economy continued to be dependent on cotton for decades. A major boll weevil blight in 1915, the mass exodus of African American sharecroppers both to escape racial oppression and find industrial jobs in northern cities, the onset of the great depression, and the industrialization encouraged by World War II all contributed to ending the Alabama economy’s reliance on cotton and transitioning it to a more urbanized economy based on primary manufacturing (especially of metal) and defense manufacturing.

The latter half of the 20th century continued to bring changes to Alabama, as the state was in many ways the center of both civil rights action and resistance to civil rights and desegregation. Many pivotal events in civil rights history, such as the Montgomery bus boycott, the Birmingham campaign, and the Selma to Montgomery marches, all occurred in Alabama. This era also witnessed massive growth in nondurable goods manufacturing, growth of the aerospace and technology industry in the state, growth in international auto parts manufacturing in the state, and a general shift of the state’s economy toward the service sector.

Today, the Alabama economy is industrial, with a growing service sector. Industrial production occupations are 78 percent more prevalent in Alabama than in the United States on average, and architecture, engineering, installation, maintenance, and repair occupations are all 28 percent more prevalent in Alabama than in the United States on average. Meanwhile, most professional service occupations such as legal, business, computer, arts, science, healthcare, and management services are all only 60 percent to 80 percent as prevalent in the Alabama economy as they are in the US economy as a whole.

Similarly, when looking at GDP contribution rather than employment share contribution by economic sector: military, utilities, federal civilian, and manufacturing activities contribute 116 percent, 86 percent, 80 percent, and 55 percent more to the Alabama economy than those activities contribute to the US economy as a whole, whereas arts, information (telecommunications and broadcasting), educational services, management, finance, real estate, and scientific or technical services activities contribute only 35 percent, 43 percent, 49 percent, 52 percent, 75 percent, 81 percent, and 83 percent as much to the Alabama economy as they contribute to the US economy as a whole. (Notably, between a quarter and a third of Alabama’s electricity production is based on nuclear power.) Agriculture, once so central to the economy, is now highly mechanized and represents only a tiny fraction of GDP. Since 2005, the contribution of mining, oil and gas extraction, and agricultural activities to the state economy has drastically decreased, while the contribution of federal, state, and local government activities to the state’s economy has drastically increased, and some service-oriented activities have increased as well.

Alabama’s economic policy is positive overall but complicated. Its fiscal policy is generally sound. It ranks 14th in the Mercatus Center at George Mason University’s fiscal health rankings on account of its strong short-term solvency and decent long-term solvency. The state government has plenty of cash on hand to cover its short-term bills and obligations. Its budgetary solvency is also relatively sound, with revenues hovering around 3 percent greater than expenses in any given budget year. Its long-term debts and unfunded pensions liabilities have grown significantly in the past decade but are still manageable and small, compared to the national average. In theory, Alabama also has room to raise income taxes without damaging the economy if it needs to meet a shortfall in its budget, but in practice—as we will soon explain—the state’s already-high sales tax burden could negate this ability.

Alabama’s combined state and local tax burden per capita of $3,893 was 9 percent of state income in 2019. This was below the national average of $5,755 (10.3 percent), which placed Alabama as the 13th least taxed state. The state’s rank in the 2021 State Business Tax Climate Index, however, is very low: its tax climate ranked 41st (with a lower ranking meaning a worse tax climate for business overall). The discrepancy is caused by the fact that Alabama has an interesting combination of hyper-low property tax rates, somewhat-low personal and corporate income tax rates, and incredibly high liquor and state-plus-local sales tax rates. This combination of taxes looks a little unorthodox, but some factors help explain this arrangement. Alabama has a much higher concentration of low-value housing units than does the United States on average. So the fact that more than 70 percent of its residents pay less than $800 per year in property taxes (compared to about 20 percent in the United States on average) is as much a function of low property tax rates as it is of low property values. Additionally, Alabama’s state revenue is significantly propped up by federal aid, which contributes 35.8 percent to state revenue, compared to the US average of 22.5 percent.

It would appear that Alabama uses federal government aid and high sales taxes to cross subsidize its low property taxes and low personal and corporate income taxes. Given that sales taxes are viewed less favorably than income and property taxes by the State Business Tax Climate Index, the seeming discrepancy in Alabama’s various tax rankings makes sense. It should also be noted that Alabama is competing with Tennessee, Georgia, and Florida for residents (individuals and businesses). Each of these states has an even lower effective tax burden and even greater overall economic opportunities, so Alabama’s practical ability to raise taxes in this context is questionable.

In terms of economic performance, Alabama tends to lag behind other states. Although this performance can be disappointing, it is also not unusual for the region, and it in some ways belies the growth and performance of many of Alabama’s urban areas. At the end of 2020, the unemployment rate was 4.7 percent (very close to what it was before the COVID-19 pandemic). 2019 per capita personal income was $47,026, which was less than the US average of $51,424 but very similar to that of neighboring states. Alabama’s 2019 real GDP of $200 billion (in 2012 dollars) made it the 27th largest state economy, bigger than neighbor Mississippi ($102 billion), but much smaller than neighbors Tennessee, Georgia, and Florida ($328 billion, $547 billion, and $963 billion, respectively).

The compound annual growth rate of Alabama’s economy from 2000 to 2010 was about 1.5 percent, which was standard for the region, and which just barely lagged behind the national average. However, the compound annual growth rate of Alabama’s economy in the 2010s was only 1 percent, which was much lower than the 2.3 percent national rate over that period. It was better than the dismal growth rates of Mississippi and Louisiana, but worse than that of neighbors Tennessee, Georgia, and Florida (which all grew between 2 percent and 3 percent annually).

This pattern shows up once more in migration flows. Annual net migration wavered from year to year, but between 2010 and 2019, Alabama experienced an annual net in-migration of 1.7 people per 1,000 each year on average. Tennessee, Georgia, and Florida experienced an annual net in-migration of 3.3, 2.7, and 6.0 people per 1,000 each year on average, respectively, while Louisiana and Mississippi experienced a net out-migration of 1.4 and 1.0 people per 1,000 on average, respectively.

Every time we write a state snapshot, something about the state we are exploring surprises us and challenges our preconceptions. The stereotype about a given state is usually based on a view of that state as it was in the 19th or 20th century. It is only with the help of many sources of data that we come to see what a state is like in the current day. Alabama is no different. Plantation-based, cotton-based, slave-based agriculture defined its economy before the Civil War. These patterns continued even after the war, and they seeded the struggles for civil rights and economic equality that would define the state into the late 20th and even 21st centuries.

Today, however, the industry at the center of the state’s history—cotton—is now nearly irrelevant to Alabama’s modern economy. Once one of the least industrialized states in the union, Alabama is now one of the most manufacturing-heavy areas in the United States. Once a state that repeatedly rebelled against federal authority, Alabama now relies on the federal government to fund a large portion of its budget, employ many of its citizens directly, and employ another significant chunk of them indirectly through military contracts to its important aerospace industry. Even Alabama’s relationship with its southern neighbors has changed. Though the Alabama economy is perhaps in better shape than its western neighbors Mississippi, Arkansas, and Louisiana, it has not quite managed to emulate the dynamism that has made its eastern neighbors Tennessee, Georgia, and Florida so much more prosperous in recent years. There is always more to be done.

Alabama’s Regulatory Outlook

Alabama’s regulatory code is published online and can be found on the Legislative Service’s website. The collection of regulatory text is referred to as the Alabama Administrative Code and contains nearly a hundred titles that vary in topic. With such a large regulatory code, natural language processing can be a useful tool for analyzing the code’s regulatory content.

For this report’s regulatory outlook section, the Policy Analytics team at the Mercatus Center is releasing a sneak peek at new State RegData 2021 numbers that were produced with natural language processing and machine learning algorithms. As of 2021, Alabama’s regulatory code contained 111,504 regulatory restrictions. This is a 3.5 percent increase from 2020, when the code contained 107,686 regulatory restrictions. Regulatory restrictions are instances of the terms shall, must, may not, prohibited, and required, which are legally binding in nature. Although this metric does not perfectly capture the restrictiveness of legal text, it does provide a stable baseline measurement for regulatory analysis.

Title 420, chapter 26, part 3 remains Alabama’s largest piece of regulatory text, with 3,144 regulatory restrictions. Title 420 (which covers the Alabama State Board of Health), however, is not Alabama’s most restrictive title as a whole. As of 2021, title 335 (regarding the Alabama Department of Environmental Management) holds that honor, with 18,652 total regulatory restrictions.

Using machine learning algorithms, the Policy Analytics team is also able to associate these regulatory restrictions with different North American Industry Classification System (NAICS) industry classifications. At the three-digit NAICS level, for 2021, chemical manufacturing, petroleum, animal production, waste management and remediation services, and professional, scientific and technical services are the most regulated industries in Alabama. These numbers do not differ significantly from 2020, but the order of these industries has changed since 2019, with animal production becoming relatively less regulated than waste management and remediation services.

2021 also marks the first year that the Policy Analytics team has collected and analyzed state statutes. Alabama’s state statutes contain 47 distinct titles that contain 120,505 regulatory restrictions as of 2021. Alabama’s statutes focus mostly on the animal production and credit intermediation and related activities industries.

A final component of Alabama’s regulatory uniqueness is measured through the Policy Analytics team’s Federal Regulation and State Enterprise (FRASE) index. The FRASE index looks at the industry breakdown of Alabama’s regulatory economy and then determines how regulated the state’s economy is by federal regulations relative to the other 49 states and the District of Columbia. As of 2021, Alabama experiences the ninth highest impact of federal regulations based on the state’s industry breakdown. The EPA is the heaviest regulator for the state of Alabama and is responsible for 44.2 percent of the state’s FRASE score. The EPA regulates 52.6 percent of Alabama’s private-sector industries, with at least 1,000 federal regulatory restrictions.

Yandle’s Reading Table

C. Bradley Thompson’s America’s Revolutionary Mind: A Moral History of the American Revolution and the Declaration That Defined It is an intellectual tour de force; a feast for the mind. Reflective of decades of Thompson’s scholarly and life pursuits—I say this as a close observer for some 15 years—the book seeks to reveal the dominant features of thought that motivated America’s founders to declare independence and form a new nation. Drawing on vast correspondence, publications, and records, Thompson builds a credible case for capturing the essence of parallel thinking among the Founders.

As is the case with many other scholars, Thompson sees the Founders and other influential individuals of the time as enlightenment thinkers; e.g., Thomas Jefferson, Alexander Hamilton, George Washington, Benjamin Franklin, Patrick Henry, James Madison, John Adams, James Wilson, and Thomas Paine. They were educated people—self-educated and otherwise—men of ideas, but not just any ideas. Based on frequent references in their writings and notes, described by Thompson, one can say that these people were heavily influenced by the writings of Francis Bacon, Isaac Newton, and particularly John Locke, but there was a host of other luminaries, ancient and timely, whose thoughts impacted the Founders on thinking.

As Thompson puts it, the core ideas that came from this literature “can be summed up in three words: nature, reason, and rights.” (I point out that Thompson’s discussion of John Locke’s discussion of the operation of the mind is especially noteworthy.) But as Thompson builds his case for an American revolutionary mind, his focus ultimately turns to rights and, with that, natural rights. He distinguishes sharply between rights that might be secured and transmitted to individuals by the state, which might better describe the modern take on the matter, and builds a strong logical and moral case for rights that are natural to man himself, rights that go with the definition of what it means to be human, and therefore rights that must be exercised freely in order for a human being to discover meaning and to flourish through discovery. And it was, according to Thompson, not taxation without representation or other burdensome English interferences that motived the revolution. In a word, the revolution was about an idea, and the idea was freedom, based on natural rights.

Thomas Jefferson’s oft-repeated and therefore familiar words from the second paragraph of the Declaration of Independence provide the moral foundation for the newly forming nation, a foundation based on natural rights: “We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty, and the pursuit of Happiness.” Providing an intellectual history of the formation of thought that lay behind Jefferson’s words, Thompson, while celebrating their philosophical power and beauty, goes on to raise serious questions about the extinct to which the Founders truly embraced the full meaning of these words. How could Jefferson, the owner of 150 slaves, really consistently believe that all men are created equal, that each man—each human—has a natural right to freedom that no state shall take away from him? Was the statement meant to be strictly aspirational, or is it an example of one of history’s greatest hypocrisies?

In his buildup of chapters, Thompson takes the reader through discussions of natural rights, self-evident truths, equality, and then equality and slavery, with this destination point forming one of the more powerful discussions in the book. Along the way, the reader encounters important discussions of common law, the community and judge-made law that formed a moral foundation for colonial life. By way of examination of correspondence, papers, and speeches, Thompson illustrates the mental anguish experienced by the Founders as they wrestled with the moral contradiction that existed between their lofty words and thoughts and how they lived as slaveholders. Thompson helps us to realize that those we might called enlightened slaveholders suffered from a severe coordination problem, though he did not state it this way. There was simply no way to, say, pack food and clothing with gold coins for and extend freedom to 150 people who would then have to make their way in a hostile world. As when people at a football game begin to stand to better observe the game such that eventually everyone is standing and visibility is not improved for the weary standing fans, only with coordination can the problem easily be solved. As Jefferson puts it, when describing the slaveholder’s dilemma, “We have the wolf by the ears, and we can neither hold him or safely let him go.” In later chapters, Thompson tells the reader how this horrible dilemma led people enlightened by the natural rights argument to push for emancipation at the local and state levels long before emancipation became a matter of national policy.

Some of the other notable chapters focus on the nature of rights, the consent of the governed, and the notion of revolution itself. But my favorite chapter comes near the end of the book and is titled “Rebels with a Cause.” And what was the cause? Before answering the question, let me offer a bit of background: Thompson approaches my question by noting “why Americans thought it necessary to dissolve a long-standing constitutional, political, and cultural relationship with Great Britain and how they did it.” Put another way, one might ask, Why was the revolution necessary? The answer is provided in four words: the spirit of liberty. Again, it was not about taxes, quartering troops, and navigational interferences, though those things mattered. The revolution was fomented out of a love of liberty, and the spirit of liberty, a cardinal virtue, was more than a popular catchphrase among ordinary people at the time. Chapter 11 of Thompson’s book is built on the notion that the phrase described the character and action of an American people who, left to themselves for more than a century (which is to say, with little supervision and regimentation from Mother England), had evolved successfully into a well-governed, law-abiding people who had flourished. They were no longer Englishmen in a strict sense of the word, but they were surely conscious of their roots.

Thompson ends his book by presenting a choice regarding how Americans today think of themselves. Do they still embrace the highly moral notions that Thompson feels characterize the mind of the founders, especially the notion of natural law? Or do they see a more pragmatic American mind as best describing the American way? Do they feel they have rights endowed by a creator, or do they seek to have rights provided to them and assured by their democratic government? Thompson closes his book with the hope that his book has helped the reader to understand the choice and, I would say, have a keener appreciation of why an order based on natural rights is the better choice, assuming the choice could be made.

Published in 2013, Charles Murray’s American Exceptionalism: An Experiment in History is a logical companion to Thompson’s book; it should be read, savored, and considered in the light of America’s recent turbulent times. Carefully researched and gracefully written, the short, 50-page book begins with a crucially important point: America, a new order of the ages, was described as exceptional by observers throughout the Western world, not just so labeled by proud Americans. Murray adds another important point to this one: saying that America is or was exceptional does not mean that the nation is better or somehow superlative but that it is different from all other nations formed in history.

Continuing with his positive analysis (in the sense of positive vs. normative), Murray identifies what he considers to be the key elements that contributed to formation of this exceptional republic. Protected by oceans and without hostile people across the northern and southern borders, the new nation was naturally defended from enemies that might attack. The Founders shared a common ideology, which of an operational matter was, of course, a reflection of the values and traits of the people. That ideology called for limited government that provided protection, justice, postal roads, and limited public goods. Then, there were the traits of the people. As recognized by the Founders, the people who formed the new nation were industrious and honest. They were egalitarian, which is to say they believed that, if given a chance, they could and should succeed; another way of saying that is that they believed in equality of status, not of outcome. They were embedded in communities where, by looking out for one another, most of their pressing needs were solved. And there was a deep religiosity. Finally, there was political exceptionalism that evolved from a lack of class consciousness that might have shown itself in the emergence of a workers’ or labor party. America was different, and, as a result, it emerged without demands for royalty, aristocracy, or a welfare state.

Murray elaborates on each of these key traits or characteristics of people, place, and ideology and makes the point that America, by virtue of its founding documents and circumstances was exceptional, which is to say it was different. But of course, there is more to the story than just saying America was or is different. America was the land of the free, a nation dedicated to a proposition that human beings have rights that can be secured by their government, a government that human beings themselves allow and support voluntarily. And this proposition implies something deeper than just being different.

Of course, Murray knows this and far more about the deeper meaning and purpose of the new nation. And that is why at the end of his short book he challenges the reader by giving a current assessment of the distinguishing traits and characteristics he so diligently described earlier. In this last section, Murray, armed with data, points out that (1) the oceans no longer can shield America from its enemies; (2) Americans cannot be accurately portrayed as being dedicated to hard work and love of God and family, and they instead depend heavily on welfare from the state; (3) the community life in many locations is often filled with fright; and (4) Americans still have not seen a labor party emerge on the political scene. Along the way, in making his assessment, Murray points out that, thus far, the nation has enjoyed peaceful transfers of power from one nationally elected leader to the next. Unfortunately, the most recent transition to a new president would not be called peaceful.

In concluding a jarring discussion of what may have happened to American exceptionalism, Murray tells a story about an 1838 speech on America’s political future (and questions about exceptionalism) by a young Abraham Lincoln. After raising a question about the viability of the institutions put in place by the Founders, Lincoln suggests that the “silent artillery of time” had weakened the Founders’ stout constitutional walls. Having said this and more, Murray leaves it to the reader to decide about America’s exceptionalism, then and now. Does the spirit of the founding effort, belief, and hope still prevail? Are Americans, as a people, still of a character to lend strength to the new order? Or is this all just a memory, a history lesson about a time and place when a dream of self-government, freedom, and the pursuit of happiness converged to produce something exceptional?

Listen to a conversation with Bruce discussing this Economic Situation Report on the Mercatus Policy Download here.