At this 2023 midpoint, let’s look at the US economy and see how it has evolved following the 2008–2009 Great Recession, the COVID pandemic, the steps taken to cushion pandemic effects, and then the Russia–Ukraine war and America’s ongoing war with inflation. Just writing this first sentence causes me to realize more fully that these are surely challenging times. Of course, the list could go on and include the ongoing political struggle over the debt limit and the cold war involving China and Russia, which are both factors affecting the tone and character of the economy, one in the very short run—I hope—the other, longer term. But enough!

On reflecting on the list of shocks and responses to them, I think we can conclude

- The US economy now reflects a dominant administrative state where every major sector and industry is subject to significant political directive and control. We should no longer speak of government intervening in the private sector. In a very real sense, there is no free-wheeling private sector. Government is now an integral part of the functioning economy.

- The combination of shocks and responses, especially from the Great Recession, ended what had been enthusiastic support for globalization. Globalism has been replaced by nationalism, which emphasizes domestic production and deemphasizes international trade beyond North America and long-standing trade partners—what is now termed nearshoring.

- US fiscal actions have significantly enlarged federal deficits and debt at a time when rising interest rates that are designed to slow inflation have caused the interest cost of the federal debt to become burdensome, especially when politicians seek to expand government welfare activities.

- The Federal Reserve’s anti-inflation actions, which have led to a runoff of federal debt instruments from the Fed’s balance sheet, have contributed to a sharp decline in the money supply and reductions in the market value of bank assets. This situation puts vulnerable banks at great risk and predicts a slowing economy.

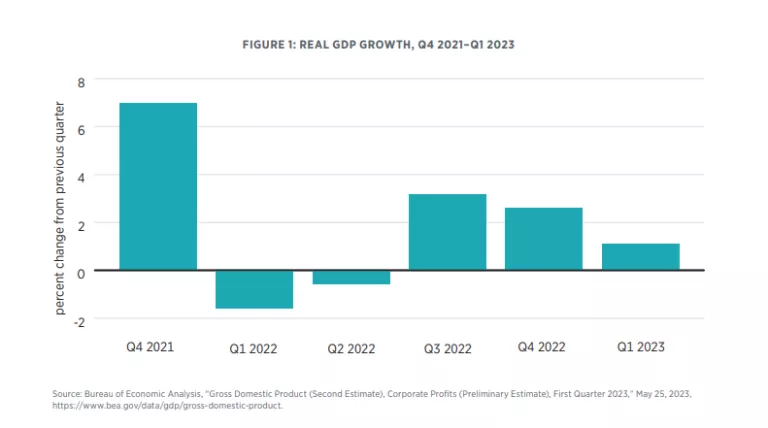

Since the 2008–2009 recession, the conditions just summarized have contributed to a rollercoaster economy, with large recent swings in real GDP (gross domestic product) growth, which are shown in figure 1. Now, data for the second estimate for 2023’s first quarter indicate an almost disappearing 1.3 percent growth, and most major forecasters call for a recession in the next six to nine months. The weak first quarter performance was associated with falling inventory investments, declining residential construction activity, and lower imports. Unfortunately for inflation-weary consumers and the effort to curtail inflation, the first quarter Personal Consumption Expenditure Index increased 4.2 percent, compared with the fourth quarter’s increase of 3.7 percent.

Other Forecasters Are Pessimistic

The Federal Reserve Bank of Philadelphia survey of 37 forecasters in February indicated negative real GDP growth in this year’s third quarter. Earlier, a January Wall Street Journal survey of 79 economists predicted negative GDP growth in 2023’s second quarter and third quarter growth at almost zero. In a more recent survey, in April, that panel moved the recession’s start to the third quarter. And last November, Wells Fargo economists predicted negative GDP growth for this year’s third and fourth quarters, a recession forecast that has not been altered.

Conversely, in January, the International Monetary Fund (IMF) indicated that there was a chance the United States would miss a 2023–2024 recession, and if a slowdown occurred, it would be mild. The IMF turned more pessimistic in April, but it basically maintained this forecast. In short, the prospects for the year ahead are surely biased toward slower growth, crossing the line to become recessionary. We will explore this and other themes more carefully in remaining sections.

How This Report Is Organized

The report’s next section continues the forecast discussion with a focus on recent pronouncements by the Federal Reserve. The Fed recently conceded the possibility of a recession in the next six months or so; the rationale offered is what is interesting. Instead of looking at its own effort to slow the economy or the ups and downs of stimulus spending, the Fed looks at troublesome bank failures. The section that follows continues to put the spotlight on the Fed by asking, “Has the Fed gone too far?” The section takes a monetarist approach and examines the relationship between inflation and growth in the money supply. As indicated there, the likelihood for lower inflation is high, but so is the likelihood for a slowing economy.

Actions taken by the Fed to raise interest rates and slow the growth of the economy have a direct effect on the value of mortgage loans and bonds held by lending institutions nationwide. When bonds or other interest-bearing assets are on a bank’s balance sheet, interest rate increases in financial markets make existing assets fall in value to provide a yield equal to market interest rates. If all bank assets were marked to market, then higher Fed-induced interest rates could do serious damage to the value of a bank’s assets. Steps taken by the Fed to minimize bank closings and avoid financial panics could lead to embedded reactions that affect the future performance of the financial sector and the larger economy. As intervention continued, what we think of as the private sector would disappear.

Turning to some recent regulatory actions, the section “Bootleggers and Baptists: New EV Subsidies and Tariffs on Aluminum” uses the bootlegger-Baptist theory of regulation to illuminate politically launched efforts to promote the purchase of electric vehicles and to impose tariffs on Russian aluminum. The report ends with book reviews from Yandle’s reading table.

THE FED AND PROSPECTS FOR A 2023–2024 RECESSION

Released minutes of the Federal Reserve’s March 20–21 meeting reveal that Fed economists see what a lot of other analysts have observed for months, only for different reasons.

The economists say the United States could suffer a mild recession later this year. As they see it, this trouble could come if more bank failures lead to sharply reduced available credit in the economy. Astonishingly, no mention is made of reductions in excessive federal spending, the selloff of Fed-owned securities that in turn reduces money supply growth, and higher interest rates.

Let us cut the Fed some slack on this. A full accounting would mean putting the causal spotlight on actions taken by the Biden administration and the Fed itself. Perhaps the Fed can better perform its difficult work if it blames the downturn on failing banks rather than on its own somewhat understandable efforts to offset misguided programs pushed by the last two presidents and Congress.

But aren’t we big boys and girls? Isn’t it time more politicians recognize that errors will inevitably be made, and that sometimes those in the wheelhouse just have to admit it and get on with the business of fixing things?

The Fed report simply says this:

For some time, the forecast for the U.S. economy prepared by the staff had featured subdued real GDP growth for this year and some softening in the labor market. Given their assessment of the potential economic effects of the recent banking sector developments, the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.

The negative outlook was triggered by Fed actions taken to slow the economy following excessive government spending, including such things as ongoing interest rate increases; related reductions in bank credit or money supply and bank instability springing from the effects of high interest rates on bank-held assets; and disrupted energy, food, and other markets caused by the Russia–Ukraine war. Fed economists instead focused on the recent closing of two major banks and the possibility of other banking disturbances.

Counting the Horse’s Teeth

A closer look at the data will help get a better handle on what may be happening. The economic roller-coaster ride began with a sharp increase in money supply growth starting in 2020’s first quarter, coinciding with the explosive expansion of post-COVID-19 stimulus spending. The increase and high ride it triggered was followed by a slowing that began in the first quarter of 2021, when the Fed hit the brake, raised interest rates, and cut money supply growth to offset the stimulus spending. Suddenly, the roller-coaster ride got bumpy. Money supply growth then turned negative in December 2022 and remains negative.

Related Fed data show how real GDP growth surged in 2021, lagging just behind the surge in money supply growth, and is now getting weaker. As to inflation, the Consumer Price Index (CPI) accelerated about a year following the surge in money growth and is now weakening in a yearlong lagged response to slow and even negative money supply growth.

This gets us to the present. In recent weeks, we’ve seen an apparent easing in inflation, with CPI growth falling, along with diminished growth in the Producer Price Index. We have also seen weak retail sales data, which suggest that GDP growth is heading south.

Putting all this together, and barring sudden policy or worldwide economic changes, we can indeed reasonably expect a recession by the end of 2023 and early 2024, with or without additional bank failures.

Would that the Fed took a larger, nonpolitical view of situation, opened up, and regularly—at least quarterly—gave us an unvarnished explanation of what’s going on.

HAS THE FED GONE TOO FAR?

The news that the pace of inflation, as measured by the Department of Commerce’s Personal Consumption Expenditures Index (PCE), had risen in 2023’s first quarter after having fallen to a 15-month low must have made members of the Fed’s Open Market Committee more than just a little bit unhappy.

The first quarter PCE, which is the Fed’s preferred inflation gauge, increased at an annual rate of 4.2 percent versus 2022’s fourth quarter’s 3.7 percent, third quarter’s 4.3 percent, and second quarter’s 7.3 percent. There’s still a way to go before reaching the Fed’s 2.0 percent target, but the bouncing index makes it difficult to bet that the Fed will soften pressure on the interest rate brake pedal at this next meeting. Perhaps it will raise rates a quarter of a point instead of a half and provide a more relaxed picture of future interest rate hikes. Indeed, former treasury secretary Larry Summers and other commentators have been urging just that.

While the news on inflation overall looks a bit better, it was not unexpected for those who pay attention to the growth of money in the economy, which, of course, the Fed controls. Practiced money supply watchers are as interested in how the Fed is managing its balance sheet—which is to say what is happening to the runoff of the government debt it owns—as in what the Fed might be doing to raise or lower its federal funds targeted interest rate.

For example, when the Fed sells mortgage-backed securities that it owns to private parties, money is removed from the economy. When it buys, the money supply expands. Of course, interest rate moves make the big headlines, but net growth in the money supply determines inflation’s destiny.

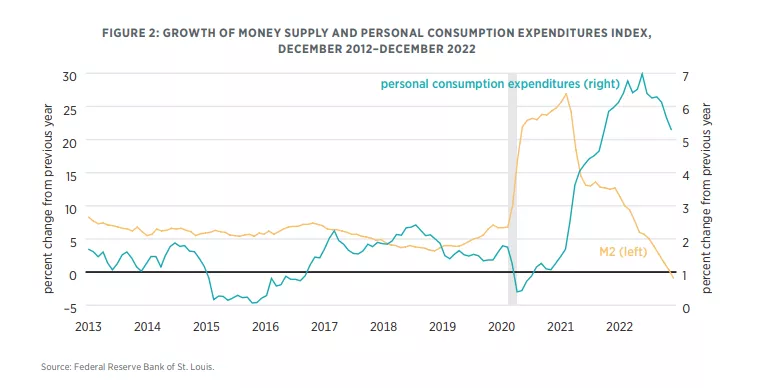

To understand the point, readers should take a periodic look at year-over-year growth in M2, a broad measure of money circulating in the economy. M2 includes cash, demand deposits, savings accounts, and certificates of deposit. Consider the data in figure 2, with the data for M2 mapped next to year-over-year growth in the PCE so that we can view the money supply and inflation side by side.

M2’s growth exploded in 2020 as trillions of dollars of stimulus money hit the economy. But notice the shape and position of the two curves. There is roughly a 12- to 15-month lag between money growth and PCE-measured inflation. Now, with M2’s growth falling and then, much more recently, crossing into negative territory, PCE growth has performed as expected. It has fallen about when we would expect it to.

The two curves send a rough, but cautionary, signal. The relationship between M2’s current negative growth and future inflation suggests we may see 2.5 percent inflation in early 2024 and a very slow economy caused by high interest rates along the way. Of course, there are other moving parts to the story, but as former treasury secretary Summers and others suggest, the Fed would be wise to soften its stance. That means more than just reducing the pace of interest rate increases. It means limiting the net runoff of government bonds owned by the Fed.

Government Bank Rescue and the End of the Private Sector

With the nation’s attention riveted on bank safety after federal regulatory action succeeded in preventing a run on suddenly crippled banks, it is hard to remember that just a few days ago, policymakers were worried about the growing use of environmental, social, and government (ESG) factors in mutual funds and bonds developed by financial institutions to attract investors. It is also hard to remember that policymakers worried about whether such activity should be praised, condemned, or even outlawed. But as that debate rolled on, questions were raised about the morality of capitalism itself and what might be happening to the evolving US economy. Hardly anyone seemed to notice that America’s private sector was disappearing and that everything we do is significantly controlled by politics.

Shortly after the failed Silicon Valley Bank was taken over by federal regulators, runs were avoided and depositors were assured that their money was safe. With this, the debate about ESGs, federal involvement in the economy, and the future of capitalism was suspended, at least for a while. Most Americans were probably sleeping better at night, believing that the Federal Reserve was in charge. The irony, of course, is that it was the Fed’s interest rate hikes that caused bank-owned government bonds to plummet in value and thus contribute to the bank failure crisis.

But as economic historian Robert Higgs explained convincingly in his 1987 book Crisis and Leviathan, America’s economic history is filled with a continuum of crises that brought new modes of government regulation to the rescue, and once the crises passed, the regulation stayed. Yes, the government fire trucks came and put out the fire, but instead of going back to the station, the trucks stayed and became a growing part of the community they saved. Community members became less cautious knowing their community was more fireproof than it had been before. As Irving Berlin reminded us, “Cousin Jack insured his shack and now he plays with matches.” Higgs explained that crises cause government to grow in a ratchet-like fashion until government becomes intertwined with economic life. At the same time, moral hazard—the tendency to let down one’s guard because of a feeling of security—enters and things can get worse.

It’s interesting that at a recent annual meeting before the start of the bank crisis, Bank of America CEO Brian Moynihan faced some of these issues head on and tried to assure shareholders that “we are capitalists,” even though his bank would soon be sought as a safe haven by depositors of smaller banks who were looking for banks deemed “ too big to fail” by federal regulators. The safe haven regulatory requirements and accompanying government assurances put smaller regional banks at risk. Meanwhile, questions about capitalism remain on the table.

The End of the Private Sector

The growth of the intertwined economy, where politics influence every major corporate decision, turns free market logic on its head. Instead of competing mainly for customers and lining up inputs, as market-based logic would suggest, profit-hungry firms find they can make a lot of money working the halls of Congress in pursuit of the right kind of regulations, subsidies, and protection from competition. And politicians find they can improve their electability by supplying those regulations to the right folks.

It is naïve to suggest that business firms are opposed to all regulation; they are not. They seek and support regulations that bring them a competitive advantage. If some form of regulation is inevitable, business interests try to get it “right.” And then there are other interest groups, the right folks, who seek regulations to satisfy their interests. The regulation that emerged during the 2008 Great Recession that requires the Fed to pay interest on bank reserves at the same rate as the Fed’s overnight interest rate target is an example. With reserves managed exclusively by the Fed, individual banks no longer work the interbank market to borrow and lend needed reserve and, by doing so, bring market pressure for improved financial performance to bear in the process.

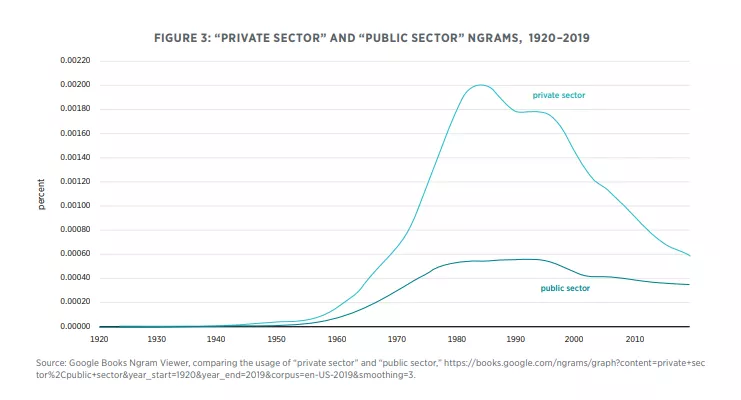

We no longer have an uninhibited private sector. Indeed, the words “private sector” are hardly seen anymore, though at one time, policymakers spoke of the public sector and private sector as distinctly different parts of the larger economy. We get an image of what has happened to the phrase “private sector” in American English usage by way of a Google Ngram analysis (figure 3). Ngrams count the frequency of occurrence of a phrase in the 8 million–book Google collection. If we look at the period from 1920 to 2019, the frequency of the phrase “private sector” is at a low level until about 1940, when the count accelerates markedly and reaches a peak around 1985. After that, the frequency falls dramatically. As shown in figure 3, the frequency for “public sector” occurs in a somewhat similar way, but with a much lower peak.

So what? What difference does it make if the United States no longer has a significant private sector, if banks and their depositors are bailed out, and if all major economic decisions are more strongly influenced by politics than by marketplace activities? Empirical work tells us that prosperity goes down as an economy becomes more entangled with command-and-control regulation. With worries about inflation and a slowing economy, this may be the time to back away from government-provided risk reduction and open the economy’s door to the beneficial forces of more market competition, not less.

BOOTLEGGERS AND BAPTISTS: NEW EV SUBSIDIES AND TARIFFS ON ALUMINUM

In what should be seen as an astounding turn of events by students of antitrust and international trade, President Joe Biden has walled out foreign electric vehicle (EV) producers, initially giving the domestic market, with some meaningful exceptions, to the new EV Big Three—Ford, General Motors, and Tesla. Very soon, VW was added to the approved list. Once again, we have a bootlegger-Baptist regulatory happening. While taking the moral high ground of minimizing the harm of climate change to justify subsidizing the purchase of EVs, politicians are making it possible for some bootlegger US auto producers to earn some extra bucks.

The Bootlegger-Baptist Theory

The bootlegger-Baptist theory of regulation, for the uninitiated, illustrates how this works. In parts of America, both bootleggers and Baptists have traditionally favored laws that shut down legitimate sellers of booze on Sundays while not making drinking illegal. These laws appeal to locals who seek a more moral society, and they provide a politically protected market for canny bootleggers who want to limit the legitimate sale of alcoholic beverages (and not drinking). Parallels can be found in many situations where the public is focused on the right and wrong of an issue and a relative few see that as an opportunity to earn a few extra bucks.

The theory doesn't question the logic or necessity of the political actions being taken, though that might be desirable in some situations. It’s rather about a convenient rhetoric that enables politicians to justify their actions as they gain and keep the support of important interest groups.

Last year’s Inflation Reduction Act established a $7,500 federal tax credit for clean vehicles. In early April, we learned which vehicles will remain eligible as rules took effect sharply limiting the credit to US manufacturers and North American–produced components. While shoppers in China are choosing from hundreds of EV models, the US consumer will likely pick from nine, given the subsidy shakeout.

President Biden intends to electrify twothirds of the US auto fleet by 2032, an especially difficult task if foreign EVs are not competitive options. But there’s more to think about. In addition to limiting the $7,500 credits to qualifying cars, the component requirements directly penalize the importation of batteries and minerals produced in China. In one fell swoop, the US auto landscape has been changed and China has been punished. Nationalism is still on the rise.

Following the dictate of the Inflation Reduction Act, the US Treasury announced the short list of qualifying vehicles. In doing so, it accomplished something that would be unthinkable or ill advised under the Sherman Antitrust Act. Some subsidies remain for certain plug-in hybrid electrics, but where more than a score of cars had previously been entitled to the $7,500, the updated list of fully approved, battery-fired EVs now includes just nine vehicles. There are a couple of other plug-ins that will be approved players.

From the standpoint of traditional antitrust readings, which rely on measures of market concentration, walling out foreign producers by lack of subsidy could yield a traditional four-firm concentration of 100 percent for the US EV market. After all, just three producers are full-fledged players. This situation would normally set off antitrust alarm bells and bring government action questioning the EV rule. So far, the Federal Trade Commission and Justice Department’s Antitrust Division have been silent. Meanwhile, auto buyers in China were able to choose from 105 new fully electric or plug-in models last year, and another 155 models are expected this year. By comparison, the US EV landscape looks like a desert.

A somewhat longer list of vehicles is approved to receive subsidies of $3,750 each. For a vehicle to qualify for the full subsidy, automakers must prove that at least 50 percent of their battery components and 40 percent of their critical minerals are sourced from the United States or its trade partners. In a few words, this means these critical components cannot come from China. Understandably, Kia and Hyundai, with large US production facilities, are not happy. They produce the cars but not the batteries. Thus, the Treasury action provides massive incentives for automakers to get in shape for the large US market.

Obviously, an anti-China mood helped facilitate President Biden’s made-in-America auto action. Recent research on the rise of polarized politics across democratic nations indicates that this animus surged following the 2008–2009 recession, when manufacturing employment took it on the chin. According to the evidence across many countries, politicians favoring open ports and borders tended to be voted out of office. Globalization and trade liberalization became toxic, and politicians who favored walling out foreign goods and people gained significantly.

Of course, Beijing’s autocratic leaders have done plenty to deserve this. But few would argue with the point that nationalism often sells on its own, politically speaking.

In any case, we should not forget that the dramatically changed US auto landscape, for better or worse, will be with us for decades. And once again, we are reminded of former GM chairman and US secretary of defense Charlie Wilson’s sentiment that “what was good for our country was good for General Motors, and vice versa.”

Let us all hope so

Tariffs on Russian Aluminum

The Biden administration’s new 200 percent tariffs on Russian aluminum and limits on scores of other metals, minerals, and chemical products took effect recently, adding significantly to the list of economic sanctions placed on Russia since the Ukraine invasion. While no tears will be shed for Vladimir Putin’s regime here, there is a domestic component to the policy that should not be overlooked.

The action provided protection to US aluminum producers, an industry that has enjoyed special treatment since at least 2018, when former president Donald Trump raised tariffs on aluminum and iron. It’s the latest example of how moral suasion—doing the right thing in times of trouble—can be used to line the pockets of aligned special interest groups who might have trouble getting federal assistance alone.

Consider this: the Department of Commerce’s two-part explanation for the expanded tariffs repeated the national defense argument— used earlier by Trump in reference to a different adversary—while adding the politics-as-usual explanation that the action would help American workers. Commerce noted that “President Biden has made it a priority to mitigate the effects of Russia’s invasion on domestic industries critical to our national security, and this includes the American aluminum industry. In imposing these tariffs, we are denying Russia an important market for its aluminum while taking a stand for America’s workers.”

The protected industry seemed happy about the action. “Alcoa welcomes the imposition of tariffs by the U.S. government on Russian aluminum,” one American aluminum producer said. “We continue to advocate for sanctions as the most effective means for the government to take action against Russia and level the playing field for U.S. producers.”

Nothing was said by the Commerce Department or White House about America’s inflation-weary consumers, who ultimately will bear the burden of the tariff. After all, tariffs placed on foreign goods entering the US market provide shelter to domestic producers so that they can raise their prices and earn higher profits, or at least reduce losses. Ultimately, of course, US consumers pay the higher prices. Most likely, though, consumers will not be heard from. After all, they are going about their lives, rationally ignorant about what happens in the cracks and crevices of government.

Not only that, but unlike unions, American consumers are unorganized. That makes the tariff story a classic case of concentrated benefits and dispersed costs: those who get the benefits darn well know it, and those who bear the costs hardly know what is going on.

Yet with constant attention being given to inflation (supply-chain driven and otherwise) and with unclear prospects for the Federal Reserve to bring meaningful relief, it is interesting that none of our elected leaders seem willing to connect the dots that link tariffs to higher consumer prices. Is this link enough to worry about? Let’s take a look.

If we go back to the pre-COVID-19, pre-Ukraine, and pre-inflation days—say to 2016—and compare the total tariffs imposed on the US population then and now, here’s what we can see. In 2016’s first quarter, the total tariffs—called custom duties and taxes on production—received by the federal government and paid for ultimately by US citizens totaled $38.8 billion on an annual basis. As of 2022’s fourth quarter, the total was $93.2 billion. It’s not chicken feed.

It seems the proverbial bootleggers are laughing all the way to the bank. But don’t you think it’s time we consumers got a report card on all this, maybe from the White House Office of Information and Regulatory Affairs? Shouldn’t there be a required annual report to the people that tallies total tariffs paid each year and shows which industries are receiving tariff protection? Isn’t it time we put a spotlight on the bootleggers as well as the Baptists?

YANDLE’S READING TABLE

Nicholas Phillipson’s Adam Smith: An Enlightened Life (New Haven, CT: Yale University Press, 2010) is a marvelous report on Adam Smith, the man, the scholar, and the hopeful founder of a science of man. Phillipson is a renowned student of the Enlightenment and Adam Smith’s life contributions. Reading the book was a double pleasure for me. First, the volume is marvelously written; the words flow gently and purposefully. But second, and perhaps more important, I learned a lot about Smith and his life that I had not known before. For example, I was not aware that Smith’s University of Glasgow academic career spanned just 13 years. I just assumed that like many of us modern minions in academia, Smith had spent a career in the classroom. That was certainly not the case, and it was not perhaps as necessary as it is today for an individual to be deeply engaged in scholarly pursuits when not a part of the academy.

For most of Smith’s life, his work, or what we might call his day job, was devoted to his prized appointment as a member of the Board of Customs in Scotland, a sinecure that resulted from the powerful impact of his 1776 Inquiry into the Nature and Causes of the Wealth of Nations, which, though rivaled by his earlier book The Theory of Moral Sentiments (1759), is still Smith’s bestknown volume. Though many others are aware, it was not until reading Phillipson that I realized that Smith sought to create a science of man and all his endeavors. Though he may have recognized that the challenge was too great to be met by one mind, he was not dedicated just to explaining how markets function and how economic life may be organized, and he was surely not working to lay a foundation that might be thought of as an apology for capitalism.

All of this may have come to be, but Smith was after something much larger. He viewed himself as a scientist, not as a man of letters. Along with these key points, the book tells us how important it was to Smith to rub shoulders and interact socially with a cross-section of businesspeople and nonacademics. He was an active member of a number of clubs that met regularly in the cities where he lived and worked. Put in today’s vernacular, Smith would have been an eager member of the local chamber of commerce, Rotary Club, or Kiwanis. Unlike most academics today—but much like one of his later disciples, Alfred Marshall—he apparently believed there was much to learn from the nonacademic population.

Adam Smith is a book to savor slowly and to put down and reread one selected chapter at a time. Doing so, however, may make one realize that Smith will challenge the best of us to become more dedicated to a lifelong effort to understand the wonderful world of which we are a part.

Slouching towards Utopia: An Economic History of the Twentieth Century (New York: Basic Books, 2022), by University of California, Berkeley, economic historian Brad DeLong, is, in the author’s words, a grand narrative of the 20th century. But the reader is warned: This is not a century in the conventional sense of the word. It is a long century that begins in 1870 and ends in 2010. There is more on the end point later. DeLong picks the beginning and ending for solid reasons. In his view, a Schumpeterian revolution begins in 1870 that leads to an incredible growth in income worldwide, and 2010 marks the point where that unusual growth period ends. DeLong’s book does not give what one might call a decade-by-decade rendering of key events that together formed the century’s amazing tapestry. Instead, the author identifies key themes that he believes shed special light on what he terms “the long century” and come together to form a recurring chorus as one reads the book.

The importance of world economic forces in understanding the rise and fall of key countries and regions is, in DeLong’s view, of special importance when considering the 20th century. A second key element is recognizing a kind of tension that developed between those who thought unchallenged market forces and globalization should determine ultimate outcomes, such as Friedrich Hayek, and those like Karl Polanyi who argued that social embeddedness would persist (which is to say, the rate of change in the economic makeup of communities and nations was limited by culture, which includes religion and other social forces). Recognizing and elaborating on this tension is an important part of DeLong’s historical treatment. Indeed, giving renewed consideration to Polanyi’s key arguments helps one to understand the rise in nationalism and curtains on globalism now being observed across the world’s democracies.

As suggested by the title, DeLong’s rendering is an optimistic one. Indeed, after getting a recount of the many millions killed in two great wars and being reminded of the systematic and severe hardships and, in some cases, mass murder faced early in the century by people of color and Jews, and then reflecting on the massive increase in income per capita that came with this century, we may be able to believe that, overall, things have gotten better. But saying this must also recognize that the word utopia rests comfortably in the book’s title. Remember? It means nowhere.

DeLong makes reading and reflecting on periods of massive change far more interesting by posing counterfactuals and speculating on how history might have turned out differently. For example, in discussing Germany’s rise to power and Hitler’s systematic move to invade the Rhineland, take Poland, and invade Czechoslovakia, DeLong asks what would have happened if Britain and France had chosen to counter those moves with force, or if Stalin had allied with Britain and France and declared war against Germany. His answer? There would have been no World War II.

Playing out the counterfactual approach, DeLong asks what might have happened if Winston Churchill had not become British prime minister and Neville Chamberlain had remained in power. He surmises that the British would have negotiated a peace with Nazi Germany and Stalin’s regime might have been short-lived. DeLong makes expert use of counterfactuals, and in doing so, he causes the reader to rethink the familiar lines of history and gain by taking a fresh, naïve view of the events that transpired. In a similar way, DeLong sheds light on the Japanese Pearl Harbor attack. He points out that not only had the United States placed an embargo on the shipment of aviation fuel to Japan in response to Japan’s efforts to enlarge its Pacific empire, but also the United States had impounded Japanese bank accounts, making it impossible for Japan to purchase fuel from friendlier sources.

The book’s treatment of the century’s chosen end point, 2010, focuses on the Great Recession, the 2008–2009 collapse that generated high unemployment, failed financial institutions, and an end to globalization and the somewhat reigning high confidence in market forces as a primary force for addressing social and economic imbalances. DeLong goes to great lengths to describe the major forces different people allege to have caused the Great Recession—and, of course, there are many factors at play. He also inserts his own assessment of the situation at the time and how he had been proven wrong on more than one count. Ultimately, we are left with the impression that the Great Recession, which arguably ended an era of high-growth globalization, came about because of deeply embedded social forces that could not be countered by changes in monetary policy or other government actions. But as I have claimed elsewhere, the collapse came because of lost trust: lost trust in rating agencies, which mislabeled the quality of mortgage-backed securities; lost trust in municipal bonds that were backed by weak bond insurers; and lost trust in a government-directed financial system that had gone to absurd lengths to make almost limitless subprime loans in an attempt to democratize the American dream.

At the end, despite all this, DeLong believes we may still be slouching toward utopia, but just how that may be happening is yet to be determined. Near the end of the last chapter, DeLong speaks to the amazing accomplishments that occurred in the 20th century and describes how they seemed to be the working of people with godlike power. But then he asks, “Why, with such godlike powers to command nature and organize ourselves, have we done so little to build a truly human world, to approach within sight of any of our utopias?”

Citations and endnotes are not included in the web version of this product. For complete citations and endnotes, please refer to the downloadable PDF at the top of the webpage.