- | Corporate Welfare Corporate Welfare

- | Policy Briefs Policy Briefs

- |

Ex-Im Bank: A Comparative Analysis of Pre- and Post- Quorum Lending

The charter of the Export-Import Bank of the United States (“Ex-Im Bank” or the “Bank”) requires the approval of at least three of its directors to allow transactions greater than $10 million. With three director signatures, the Bank can issue lending products of up to $100 million. Directors are appointed by the President of the United States, confirmed by the Senate, and serve four-year terms. However, these terms may be extended until a replacement is confirmed, up to a maximum of six months. Since 2015, the Senate has blocked every nominee and the Bank has operated with fewer than three board directors.

This situation allows one to assess the performance of the Bank before and after it lost the ability to underwrite loans of significant size. This brief analyzes the impact of the lack of a board quorum on the Bank’s financing and beneficiaries, comparing and contrasting the agency’s performance before the policy change (FY 2014) and after it (FY 2018).

Elsewhere, one of us has argued that the optimal economic policy regarding the Ex-Im Bank is to have no such bank. The subsidies distort markets by shifting capital toward well-mobilized industrial interests and away from unsubsidized exporters. This distortion also increases consumer prices, exposes taxpayers to unnecessary risk, and misallocates lending. Nevertheless, in a world of second-best policies, one still can determine if this change in the Ex-Im Bank’s policy improved its performance over the status quo.

The impact of the lower transaction cap is most telling on new loans, loan guarantees, and working-capital approvals. In 2014, these were on the order of $21 billion, while in 2018 they were $3.6 billion (adjusting for inflation to 2012 dollars). Clearly the vast majority of the Ex-Im Bank’s lending activity before the operating change involved deals greater than $10 million. This fact raises two questions: who was benefiting from the Bank’s financing before, and who is benefitting now? The first question has been aptly answered and documented: it was well-connected giant manufactures that benefited. The answer to the second question is offered in what follows.

The lack of a quorum has been decried by advocates of the Ex-Im Bank. Many politicians and interest groups fear that the much-smaller lending cap would have deleterious effects on American exporters and their sales. Yet we find these fears to be unwarranted.

We find, first, that big-ticket beneficiaries of the Ex-Im Bank have easy access to capital markets, and therefore they still have the ability to finance their exporting activities. Second, small and medium-sized exporting firms continue to receive loans from the Bank, and their share of the Bank’s portfolio has grown. Third, contrary to the fears of many, US exports have not collapsed. We also find that the Ex-Im Bank has reduced significantly the financing of foreign companies in stable economies and of companies heavily subsidized by their own governments.

Section 1. The Current State of the Ex-Im Bank

Ex-Im Authorization

In its currently authorized but quorumless state, the Ex-Im Bank faces a nominal limit of $10 million per deal. This cap is only 10 percent of its prior capacity. As a result, the amount of money the Bank has appropriated has gone down considerably (see figure 1). This owes to the fact that a nominal $10 million cap limits large firms’ incentive to pursue Ex-Im Bank financing. In FY 2014, the Bank authorized $21 billion (in 2012 dollars) in deals, including loans, loan guarantees, working capital, and insurance. By FY 2018, that amount had decreased to $3.6 billion (in 2012 dollars).

The nominal $10 million cap has resulted in a dramatic decrease in the average size of Ex-Im Bank approvals between FY 2014 and FY 2018, from $6.7 million each for 3,157 transactions to $1.9 million each for 1,968 transactions. The number of companies served by the Bank decreased by 1,189.

Impact on Taxpayers’ Exposure

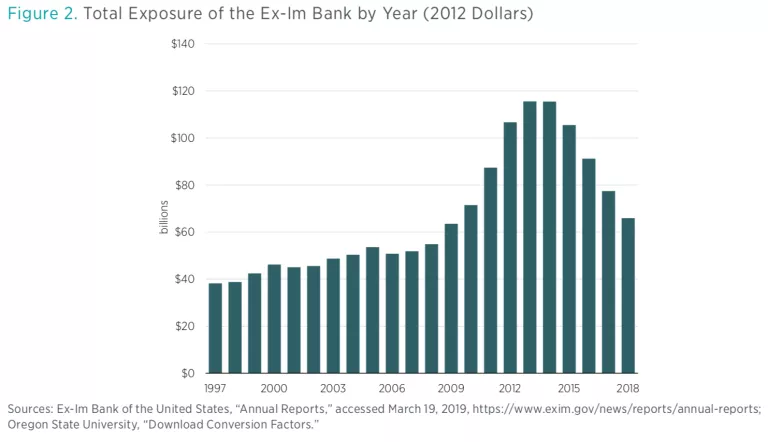

To dispense loans, working capital, and guarantees, the Bank necessarily exposes taxpayers to risks of losses. From 1997 through 2008, the Ex-Im Bank’s exposure hovered at approximately $60 billion each year in nominal dollars. This means it grew from $38 billion in 1997 to $55 billion in 2008, adjusted for inflation (see figure 2). In the postrecession years until 2015 the Bank’s exposure skyrocketed, reaching $116 billion in 2013. While this annual risk exposure began decreasing slightly in 2014, the rate of the decrease greatly accelerated in 2015, the year the Ex-Im Bank lost its quorum.

With approvals dropping dramatically, the Bank’s risk exposure fell in 2018 to $66 billion, just above its 2009 level. This exposure will continue to decrease as long as the nominal cap of $10 million per transaction remains in place.

Most of its advocates fail to adequately address the issue of the Bank’s risk exposure. In fact, the Bank is often justified as a source of income for taxpayers. This claim is entirely an artifact of the accounting method used to calculate gains and losses, and using a different method yields diametrically opposite results.

In 2014, before the Bank lost its quorum, the Congressional Budget Office (CBO) estimated the budget effects from 2015 through 2024 of the Ex-Im Bank using Fair Credit and Reporting Act (FCRA) standards as well as Fair-Value standards. The CBO found that using the former method showed a $14 billion positive revenue effect of the Ex-Im Bank on the federal budget, whereas the Fair-Value method showed a $2 billion loss of revenue (both measured in 2015 dollars).

The Fair-Value method of accounting is used by the private sector. Shifting to this method of accounting for the Ex-Im Bank would take market risks into consideration, unlike the FCRA method, which doesn’t. Given that the Ex-Im Bank frequently only charges an interest rate of the “prime rate minus 0.5%,” it is unsurprising the Fair-Value accounting method shows a loss. The prime rate is the interest rate banks give their most reliable borrowers. By offering a rate below the prime, the Ex-Im Bank fails to fully charge for the riskiness of the loans that it dispenses.

Impact on Exports

The core mission of the Ex-Im Bank is the promotion of exports. Supporters of the Bank argue that it is an important tool for boosting US exports. For instance, President Obama in 2010 claimed that an expansion of the Bank’s budget authority could help double US exports within five years. The president argued that the Ex-Im Bank paved a sure path to growth and jobs, despite previously campaigning against it.

Under its charter, the Ex-Im Bank should assist US exporters to compete abroad when (1) their customers are not credit worthy enough to get a loan or (2) their competitors are benefiting from foreign subsidies.

Additionally, in May of 2015, John Bolton, who is now national security advisor, wrote that the United States needed to keep the quorum at the Ex-Im Bank as a strategic move to promote US interests. Bolton’s assertion echoes claims from Jeffery Gerrish, former deputy US trade representative and the current acting president of the Ex-Im Bank, who declared that “by restoring the Export-Import Bank’s board quorum, EXIM will be able to help level the playing field.”

As the Cato Institute’s Sallie James reminded readers in 2011, “This emphasis on exports is tied up with the longstanding notion that the Bank helps to improve the U.S. balance of trade. During the Ex-Im Bank reauthorization debate of 2001, the US Chamber of Commerce said that ‘last year’s record $369.7 billion trade deficit highlights the need for full funding for the U.S. Export-Import Bank in order to advance American products overseas and correct the growing imbalance between imports and exports.’”

The implicit assumption of the Ex-Im Bank’s proponents is that the total level of US exports is directly and positively related to the activity of the Bank. If this assumption were valid, it would mean that a significant reduction in the Bank’s financing authority would be followed by a sharp fall in US exports.

Yet the data show that, in general, US exports have not been affected by the significant reduction in Ex-Im Bank financing that started in 2012 and continued through the loss of quorum in 2015. Nor has the US trade balance been much affected.

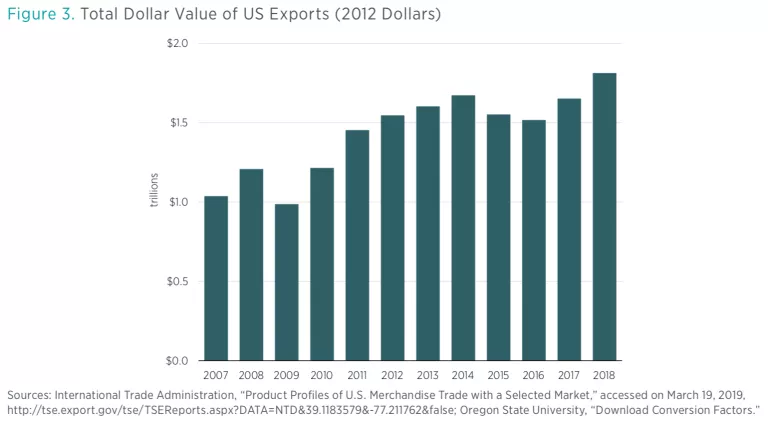

According to the International Trade Administration (ITA), in 2014 the United States exported $1.7 trillion in goods (see figure 3). By 2018 this figure had risen very slightly to $1.8 trillion. This shows no major change despite a 72 percent drop in the Ex-Im Bank’s financing during that time. In fact, the level of exports in 2018, when the Ex-Im Bank’s financing was at a minimum, was $266 billion higher than in 2012, when the Ex-Im Bank’s financing was at its peak.

The Ex-Im Bank does not support US service exports, and therefore the portion of all exports supported by the Ex-Im Bank is even smaller than reported earlier. Another measure of US exports—this one from the Federal Reserve Bank of St. Louis—finds that in 2014 the United States’ exports of goods and services were $2.4 trillion, which rose to $2.5 trillion in 2018. This fact leads to a similar conclusion that the withdrawal of Ex-Im Bank funds from the export-financing market did not have a significant effect on total US exports, which continued to follow their historical pattern of increasing. The only exceptions to this pattern were temporary and were generally limited to periods of economic recession or depression.

Monthly trade numbers from the US Department of Commerce show a downward shift in US merchandise exports beginning in January 2015, six months before the Bank’s charter expired (see figure 4). Service exports decreased at the same time. Because the Ex-Im Bank has no interaction with service exports, and because the reduction in service exports coincides with reductions of merchandise exports, the change in Ex-Im Bank funding clearly does not explain the reduction of merchandise exports.

Also, when compared with the same period in 2016, the 2017 data show exports rebounding without any change in the status of the Ex-Im Bank other than the continuing decline in its overall financing. As noted by our colleague Dan Griswold, “the bottom line is that U.S. export growth was decelerating beginning in 2012 and has picked up again in 2017, driven mostly by global growth rates. The Export-Import Bank’s status was simply not a factor.”

These findings should not surprise anyone. First, the share of exports backed by the Bank was always relatively small. As will be discussed in more detail later, Ex-Im Bank activity reached a peak in 2012 at 3.23 percent of exports, but on average from 2007 through 2018 was less than 2 percent. It now stands at 0.41 percent.

Second, the 3.23 percent of US exports backed by the Ex-Im Bank in 2012 includes only goods and not services. According to the Census Bureau, in 2012 goods exported totaled $1.6 trillion, whereas service exports totaled $656 billion. These figures drop the total portion of US exported goods backed by the Ex-Im Bank at its peak of activity to only 1.6 percent of all US exports.

The Ex-Im Bank has never had more than a negligible effect on the health of US exports, so it is not surprising that the Ex-Im Bank’s recent contraction of lending activity followed this pattern.

This finding is consistent with an extensive economic literature that shows that export subsidies do very little to affect the overall level of exports and the balance of trade in a large economy like the United States. A country’s trade balance is driven largely by underlying macroeconomic factors, such as the ratio of savings to investment or by the attractiveness of its investment climate.

While Ex-Im Bank financing has no real effect on the overall level of exports, it does have an impact on which particular exporters get propped up by government funding and which do not. In other words, the Bank distorts capital markets by shifting financing for the benefit of its clients. For instance, as discussed in the next section, a small number of large manufacturers benefit from a vast majority of the funding. In particular, the aerospace industry is a favorite of the federal government when it comes to boosting exports with subsidies. The reduction in Ex-Im Bank financing means that more resources are now being directed by market forces rather than by politics.

Section 2. The New Allocation of Ex-Im Financing

As mentioned earlier, the main consequence of the Bank’s loss of its quorum was to set a limit of $10 million per deal. This reduction resulted in a dramatic decrease in both the Ex-Im Bank’s financing levels and in taxpayers’ risk exposure. It has also permitted us to study the composition of firms and countries that benefit from Ex-Im Bank support under the two lending regimes.

Big Businesses

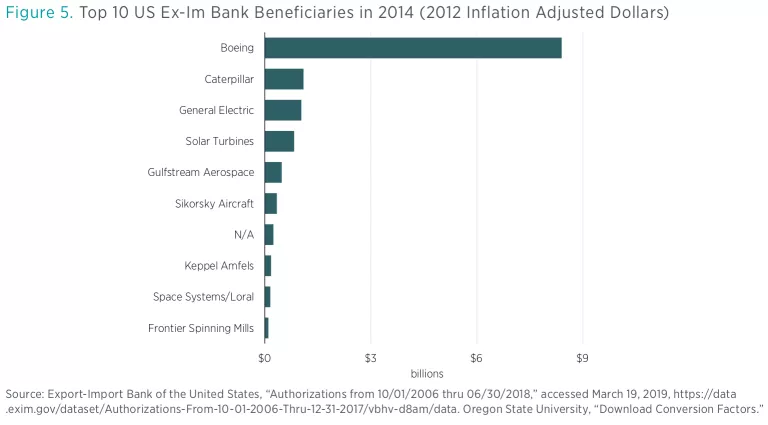

Until 2015, the Ex-Im Bank was known for its steady support of large companies. As the data show in figure 5, on the domestic side, 65 percent of the Bank’s financing benefited 10 giant manufacturers, including General Electric and Caterpillar. But the biggest beneficiary of all was Boeing, which benefited from 40 percent of all the Ex-Im Bank’s financing and 68 percent of all loan guarantees. Owing to this favoritism, critics dubbed the Ex-Im Bank “the Boeing Bank.”

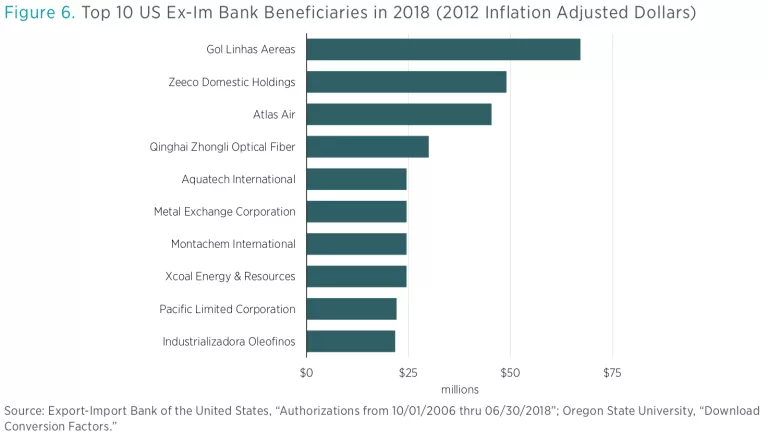

Under the new operating restrictions, things have changed dramatically. None of the top 10 companies of 2014 even appear in the top 10 list of beneficiaries in 2018. By 2018, Boeing disappeared entirely from the Ex-Im Bank’s portfolio (see figure 6).

Boeing has still managed to prosper during the past few years despite this cut to its government largesse. From 2014 to 2017, Boeing’s profits and stock prices increased even though the company had to shop for export financing in the marketplace. This pattern continued after 2017 as well, giving Boeing what was possibly its best ever year in 2018 with sales of $101.1 billion, including an increased number of aircraft exported (from 763 in 2017 to 806 in 2018).

Boeing is now having “its highest-ever level” of backlog orders. It seems that the aeronautical giant did not have difficulty finding other sources for their export financing needs.

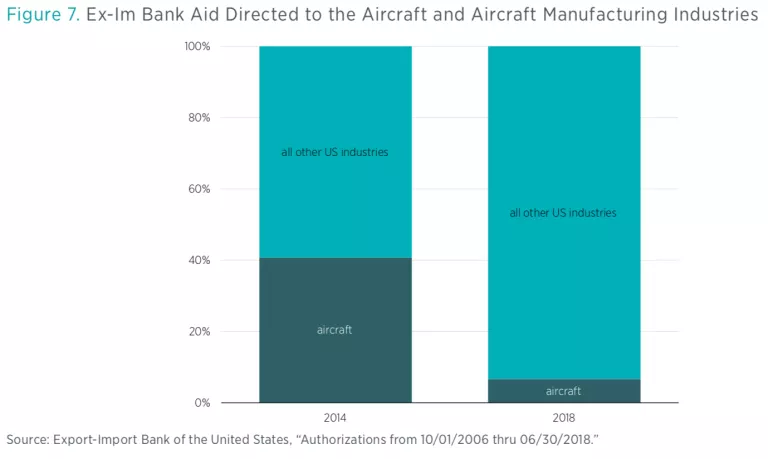

As shown in figure 7, the reduction in government lending subsidies for Boeing also affected the total level of financing for producers of aircraft and aircraft parts: from 41 percent to 4 percent of the Ex-Im Bank’s loans, loan guarantees, export insurance, and working capital. This makes sense given that exports in the aircraft manufacturing industry currently enjoy historically low financing costs.

The same trend is visible with all other large domestic beneficiaries of the Ex-Im Bank. This is true in spite of the fact that some of them, such as General Electric and Caterpillar, experienced financial difficulties not related to the Ex-Im Bank transaction cap.

Small Businesses

One recurring argument from Bank supporters is that export subsidies are needed to support small businesses. These supporters point out that as of 2014 (before the change at the Ex-Im Bank) close to 90 percent of all Ex-Im Bank transactions went to small businesses.

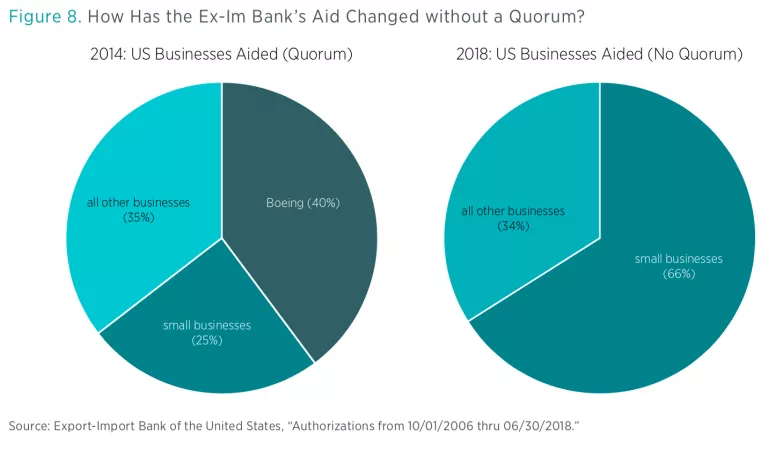

It is true that 3,175 of what the bank labels small companies were the recipients of 90 percent of the Ex-Im Bank transactions. However, commitments to small businesses are often small. Looking at the total share of the Ex-Im Bank’s financial commitments going to small businesses provides a different perspective. In FY 2014, only 25 percent of Ex-Im’s financing went to small firms (see figure 8). In the same year, the top 10 large companies received 65 percent of the Ex-Im Bank’s financing, and (as stated earlier) Boeing received 40 percent.

Today, things have changed markedly. In FY 2018, small businesses benefited from 66 percent of Ex-Im Bank financing. This change is hard to reconcile with the oft-repeated defense that the Ex-Im Bank focused on small businesses when it had a quorum.

The numbers reported earlier do not imply that small businesses are actually the true recipients of what the Bank labels “small business financing.” According to the data (see figure 9), in FY 2014, among the top five recipients of what the bank called small business aid were Caterpillar and Boeing! Caterpillar was the top single recipient with $367 million and Boeing was the fourth-largest single recipient with $37 million. It is not readily apparent what definition the Ex-Im Bank is using for “small business.” However, any definition including Boeing, a multibillion-dollar company and one of the world’s leading airline manufacturers, is misleading.

Four years later this situation improved. In FY 2018, without a quorum, neither of these two companies were among the top 10 recipients of small business aid from the Ex-Im Bank (see figure 10). However, Caterpillar did still receive over $14 million in aid specifically for small businesses.

The fact that Caterpillar and other large businesses still receive financing earmarked for small businesses from the Ex-Im Bank indicates that tools have remained in place for the Bank to direct significant funding to large businesses, including through small-business financing. The shift in the Ex-Im Bank’s use of small business funds away from large businesses has not come from more responsible rules regarding small businesses. This change happened because of the dampened incentives from the decrease in the nominal cap on the Bank’s actions.

The increased focus on small businesses did not come at the expense of medium-sized and large businesses. From FY 2014 through FY 2018, the portion of the Bank’s financing for medium-sized and large firms (except Boeing) fell only slightly, from 35 percent to 34 percent of new financing.

Countries Supported by the Ex-Im Bank

As the data show, three of the top foreign countries whose businesses are subsidized by the Ex-Im Bank and the cumulative amounts that firms in these countries received between FY 2007 and FY 2014 (figure 11 shows the amount of support that foreign countries received in 2014 alone) were the following:

- Mexico ($14 billion, with $1.6 billion of that in FY 2014 alone)

- Saudi Arabia ($8 billion, with $225 million of that in FY 2014 alone)

- China ($5 billion, with $2.3 billion of that in FY 2014 alone)

In FY 2014, the top foreign destination for US-backed Ex-Im Bank loans was China. Second was Mexico. Since the Bank lost its quorum, there has been a sharp decrease in taxpayer subsidized lending for Chinese firms that buy American exports: from 11 percent of the Ex-Im Bank’s new financing in 2014 to only 1 percent in 2018. This means the Bank is more compliant with its own charter that includes a “Marxism-Leninism” clause barring it from aiding exports to centrally planned economies. Again, the Bank’s effect on total exports is negligible, as the inflation-adjusted value of US exports to China rose between 2014 and 2017, from $127 billion to $139 billion. By 2018 this figure had fallen to only $131 billion due primarily to the Trump administration’s threat of increasing tariffs on Chinese products and China’s retaliation.

The data also show a sharp decrease in the Ex-Im Bank’s lending to support exports to Mexico, even as that country remains the top foreign destination for the Bank’s financing (see figure 12). In FY 2014, exports to Mexico received 8 percent of all Ex-Im Bank new financing. By FY 2018, this figure had fallen to 3 percent. China is the second-largest economy in the world, and Mexico is the fifteenth. Given the Bank’s mission to finance “risky” exports, it makes sense that the smaller of these two economies now receives more export support than the larger.

One striking feature of the lending cap reduction is that it almost doubled the share of the Ex-Im Bank’s financing directed to companies in the United States as opposed to foreign firms. With rare exceptions, all of the US companies benefited from working capital. Many of them are likely part of the supply chain of large exporters such as Boeing. From FY 2014 through FY 2018, the portion of funds with a destination of “United States” increased from 12 percent to 22 percent. It should be noted that aid to exports where the country of destination is recorded as the United States topped the list in both FY 2014 and FY 2018; something we discuss later in relation to the Bank’s transparency. It can be noted for now that this usually denotes working capital for production of goods to be exported when finished.

Until 2015, the Ex-Im Bank had been extending taxpayer-backed support to companies like Ryanair (nominally $4 billion in guarantee loans over 10 years) and Emirates Airlines (nominally $3.9 billion over 10 years), giving them a large competitive advantage over US domestic airlines like Delta and United. In addition, the Ex-Im Bank subsidized, through its financing, the state-owned Mexican oil company PEMEX (nominally $9.7 billion over 10 years).

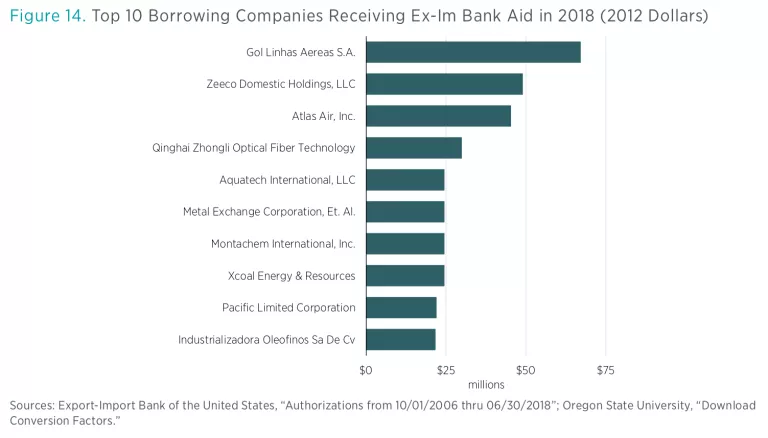

Beneficiaries of the Ex-Im Bank include wealthy foreign companies (often state owned) that are subsidized by their own governments. Notable in this list were Mexico’s giant PEMEX and Air China (see figure 13). Since the change in the Ex-Im Bank’s operations, far fewer US dollars are subsidizing foreign firms in general and foreign airlines and oil and gas companies in particular (see figure 14).

Proportion of Exports Supported by the Ex-Im Bank

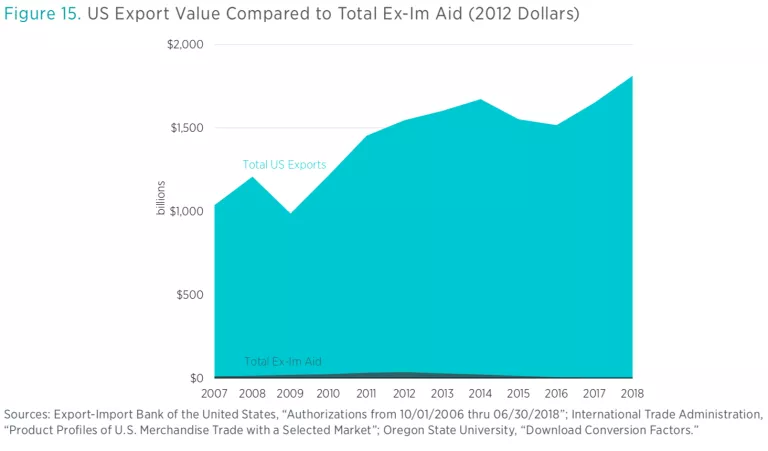

As mentioned earlier, the vast majority of US exporters never sought or received financing from the Ex-Im Bank. As shown in figure 15, in FY 2012 the Ex-Im Bank reached the height of its financing activities, authorizing $35.8 billion in export assistance. The Bank itself estimated that this financing aided $50 billion in exports. That same year, US exports of goods (excluding services) were valued at just over $1.5 trillion. Therefore, at the height of its approvals, in 2012, the Ex-Im Bank supported a paltry 3.23 percent of goods exported from the United States. Notice that the numerator of this ratio is obtained from data provided by the Ex-Im Bank; consequently, however small the Bank’s support is, it should be read as an optimistic measure of the Bank’s effect on US exports.

By FY 2014, which is the last year during which the Ex-Im Bank operated with a quorum, the proportion of Ex-Im Bank aid had dropped to only 1.69 percent of the United States’ inflation-adjusted $1.7 trillion of goods exported (using the Bank’s own estimate of the value of exports supported). Both in nominal and percentage terms, Ex-Im Bank financing decreased; however, exports slightly increased. By the end of FY 2018, using the Bank’s estimates of value of exports supported, the Ex-Im Bank’s new financing had decreased by over nine-tenths from its peak to only $3.7 billion, but total US exports were up to $1.8 trillion, leaving only 0.4 percent supported by the Ex-Im Bank. Again, it seems that the Ex-Im Bank’s financing contraction has a negligible effect on the value of US exports.

Data from the St. Louis Fed show an even smaller portion of US exports supported by the Ex-Im Bank in 2014, in 2018, and in 2012 (the latter year being the height of the bank’s activity). As noted above, the ITA’s trade data measures only goods, whereas the St. Louis Fed incorporates exports of both goods and services into its data. These data make clear that the largest proportion of exports the Ex-Im Bank ever supported was only 2.36 percent, in 2012. In the last year of the bank’s quorum, 2014, this had already fallen to 1.16 percent, and would fall further to 0.27 percent by 2018 (all based on the estimated value of exports the Ex-Im Bank supported).

It is difficult to see how any reduction in the Ex-Im Bank’s financing could have had any major effects on US exports when, on average, more than 98 percent of exports each year were never supported by the Ex-Im Bank’s subsidies.

Section 3. The State of the Export Credit Industry

Private Markets Have Filled in Ex-Im Bank’s Gap

While economic theory leads one to be skeptical of the Ex-Im Bank’s claims of filling a “financing gap,” the Bank’s decreasing role in financing exports provides concrete evidence that there was no gap in the first place. Private insurers are set to come into the export market, and since the Ex-Im Bank’s quorum was lost in 2015, those insurers have created new ways of doing so. The Ex-Im Bank, like most government agencies, is slow to change. On the other hand, private banks have the flexibility to develop new methods to reduce the costs of insuring exports for both large and small exporters.

In FY 2014, before the loss of its quorum, the aid directed to Boeing was nominally valued by the Ex-Im Bank at over $8 billion. By FY 2018, with no quorum in place, the amount of this aid had fallen to zero. Given the claim that the Ex-Im Bank is “filling a financing gap,” one should expect that Boeing would not be able to find the lost $8 billion in export financing without the Ex-Im Bank. Instead, Boeing is, in its own words, “attracting new capital and innovative ways to access new financial markets.”

Since 2015, the year the Ex-Im Bank lost its quorum, Boeing has worked with outside investors, such as Marsh and McLennon, to set up an entirely new financing company for its products. This new organization is called the Aircraft Finance Insurance Consortium, and it offers aircraft nonpayment insurance. To be viable, this initiative must convince a court that it did not steal the business model from Xavian Holdings, who is suing Boeing and Marsh. Not only was there no gap in financing, there was immediate competition to fill what Ex-Im once supplied for Boeing’s financing needs. Boeing’s own market outlook is that “airlines and lessors are expected to have some of their lowest historical costs of financing.”

The 40 percent of the Ex-Im Bank’s aid directed to Boeing in FY 2014 was not the only aid the private market replaced. One example of private sector aid moving in for small businesses is a new project by seven international banks to create a standardized digital platform for export insurance. Twenty more banks and 60 corporations are participating in the development and are ready to join. The platform is intended to reach new businesses and reduce the costs of providing export financing. This response is explained in part by the fact that industry representatives cite the United States as a prime area for expansion owing to how little export insurance is used in the United States. Only 3 percent of US businesses opt for export insurance when it is available, as opposed to 15 percent of European businesses.

Additionally, in 2018, insurers petitioned the federal government to pass the Government Risk and Taxpayer Exposure Reduction (“GRATER”) Act of 2018, which would transfer insurance exposure from numerous parts of the federal government, including the Ex-Im Bank, to private insurers.

Requests from private business to take a larger role in trade finance make sense given the expansion of trade-credit insurance companies in the United States in recent years, such those of Euler Hermes and Markel. In 2017, Euler Hermes began working with Flowcast, an artificial intelligence and financial technology company, to develop new ways of providing credit insurance digitally. Markel, another large credit insurer, has expanded into Chicago to increase the company’s access to middle America. Markel’s trade insurance began in the last year of the Ex-Im Bank’s quorum (2014) and “has grown into a successful business focusing on a broad range of specialist products.”

This influx of private financiers as the Ex-Im Bank has withdrawn provides evidence that the Ex-Im Bank had been crowding out private alternatives, and further supports the notion that the market gap was either nonexistant or smaller than the Ex-Im Bank’s proponents believed.

Section 4. Transparency

The Ex-Im Bank’s financial reporting has grown more ambiguous since 2014. Specifically, the Bank has become even less transparent in reporting the countries to which its clients export, the products those companies export, the exporters’ home states, and the primary borrowers.

We note however that two categories of data have been reported more accurately in the period examined: currently, the Ex-Im Bank explicitly lists the primary lender and primary exporter on all transactions.

In FY 2014 the portion of Ex-Im Bank aid directed to exports to “Multiple – Countries” or a “Private Export Funding Corp.” was 24 percent of all financing provided (see figure 16). By FY 2018, the percentage of such financing had risen to 65 percent of all of the Ex-Im Bank’s export financing (see figure 17). When nearly two-thirds of all aid has unclear reporting about where those exports are going, it makes impossible a clear understanding of the Ex-Im Bank’s financing. This lack of clarity creates problems for assessing the Bank’s compliance with US sanctions on countries such as Iran and North Korea. Also, it has become more difficult to assess the Bank’s consistency in following its own rules, including limitations on financing importers in centrally planned economies. Additionally, the opaque records leave the public wondering how much of its financing supports foreign firms that are subsidized by their own government.

Another transparency issue is that the portion of aid for “exports” that were not actually leaving the country increased. As mentioned earlier, between FY 2014 and FY 2018, the portion of Ex-Im Bank financing to exports for which the US was the destination nearly doubled from 12 percent to 22 percent. With a total of 90 percent of the Ex-Im Bank’s funds either not revealing clearly the export destinations or listing the US as the export destination, any information regarding where the bank directs its funds should be looked at skeptically.

There are two main problems with aiding exports to the United States. First, an American company selling to an American buyer is neither an exporter nor an importer, and the Ex-Im Bank should play no role in any such transactions. Second, even if exports to the United States were within the realm of the Bank’s financing, the United States is one of the least, if not the least risky jurisdiction in which goods are shipped and sold; thus, Ex-Im Bank activity here still would violate the Bank’s mission to support only exports made to risky jurisdictions.

The Ex-Im Bank’s increase in its use of the terms “Multiple – Countries” and “Private Export Funding Corp.” to describe the destination of subsidized exports has followed the same pace as the use of the terms “Multiple – Borrowers” and “Multiple – PSOR” (Primary Source of Repayment) in the Bank’s reporting on who has borrowed the money that the Bank is insuring and who is responsible for repaying the loans. Ambiguity in reporting on borrowers and sources of repayment rose from 23 percent to 65 percent in the four years between FY 2014 and FY 2018. That all four of those rates rose in similar proportions owes to the fact that all of these terms are frequently used in the Ex-Im Bank’s export insurance program, which has come to dominate the bank’s actions since the loss of quorum.

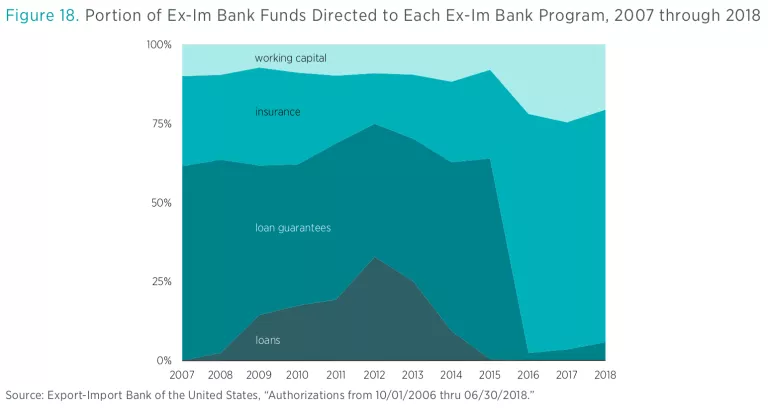

The export insurance program has a history of using vague terms. As this program has become the most dominant one at the Ex-Im Bank since its loss of a quorum (see figure 18), these vague terms have come to dominate the bank’s records as well.

Ambiguity also increased in the Ex-Im Bank’s records about what kind products their financing supports. In the same time period, from FY 2014 to FY 2018, use of the term “N/A” regarding the product in question has doubled from 16 percent to 32 percent of the Ex-Im Bank’s actions. This ambiguity complicates any conclusions regarding how diversified the Ex-Im Bank’s investments are and makes even more difficult the task of determining if the industries being helped are actually in need of aid.

In a similar fashion, ambiguous reporting about which US state an exporter is based in has increased over the period examined. In FY 2014, exporters in the State of Washington received more aid from the Ex-Im Bank than did exporters in any other state or the “N/A” category. This is because Boeing is headquartered in Washington and Boeing was the largest recipient in FY 2014 by a nominal margin of $7 billion. However, that year “N/A” still ranked second as the origin of exports for 15 percent of all Ex-Im Bank financing. By FY 2018, “N/A” was at the top of the list, having more than doubled to 31 percent of all Ex-Im Bank actions.

A few simple changes in reporting would improve transparency. The Ex-Im Bank should start listing the countries or business involved wherever it currently reports “Multiple.” For example, if the PSOR would be recorded as “Multiple – PSOR,” then the companies responsible for repayment should be listed. Additionally, “Private Export Funding Corp.” should no longer be used for specifying the different countries to which American exports are directed. Instead, the list should name each country in question.

Furthermore, the United States is not an export destination for US exports. Working capital provided to suppliers of exporters, such as American manufacturers of parts for Boeing, should report the ultimate destination of the product in question, not the next stop it will make in the United States. Lastly, the use of “N/A” in the Ex-Im Bank’s reporting should be strictly limited. While this term might be the correct or accurate term to use in certain specific situations, its broad use obfuscates the bank’s actions. In particular, the use of “N/A” with regard to which industries the exports in question come from and where in the United States that export originated should be ended entirely. All US exports are in some industry and come from some US state or territory.

Concluding Remarks

In view of the expiration of the Ex-Im Bank’s authorization in September of 2019, legislators should look closely at the current performance of the bank under a board of directors without quorum.

Since the loss of quorum, the Bank has shifted its focus from large businesses to small ones. Instead of a few large companies representing the majority of the Ex-Im Bank’s financing, aid to small businesses is now dominant. Meanwhile, the prior large beneficiaries are nevertheless finding financing, and new methods are being created to serve these companies.

Importantly, Ex-Im Bank exposure to risk is down from its peak. This means US taxpayers are less exposed to the bank’s credit risk. Also, the share of the Bank’s portfolio with foreign firms that themselves receive subsidies from their own governments has decreased. What’s more, the Ex-Im Bank has had a negligible effect on total US exports.

It is important to note, as mentioned earlier, that the changes we examined in this brief correspond exclusively to the $10 million cap. No other rules have changed at the Ex-Im Bank. The moment a third member is assigned to its board, this restriction will be removed.

We reiterate that our preferred policy is to let this agency finally expire in September 2019. Our foregoing analysis shows that the lending cap has had the effect of better aligning the Ex-Im Bank’s performance with its charter, and it would seem prudent to make it standard policy should the bank be reauthorized.