- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

The Federal Reserve’s Balance Sheet: Costs to Taxpayers of Quantitative Easing

It might seem extraordinary that a US government institution could conduct any program that is likely to incur a cost of nearly $1 trillion to taxpayers. And it might seem equally extraordinary that such a program could be undertaken without congressional approval or even any forewarning about the magnitude of the risks. Yet that is the expected outcome of the Federal Reserve’s securities purchase program known as QE4 (its fourth round of quantitative easing).

In this policy brief, we summarize the results of our quantitative assessment of the costs and benefits of QE4. From mid-March 2020 to March 2022, the Federal Reserve (Fed) purchased about $4.6 trillion in securities and funded those purchases with a corresponding increase in its overnight interest-bearing liabilities of bank reserves and reverse repurchase agreements (reverse repos). In effect, the Fed’s balance sheet now appears similar to that of a hedge fund whose longterm assets are financed by short-term borrowing, except that such funds routinely hedge their interest rate risk, whereas the Fed’s portfolio is effectively naked. Consequently, as the Fed has pushed up the level of short-term interest rates (from near zero at the start of the 2022 to more than 4 percent as of mid-December 2022), the interest expense on its liabilities has far outpaced the earnings on its securities holdings.

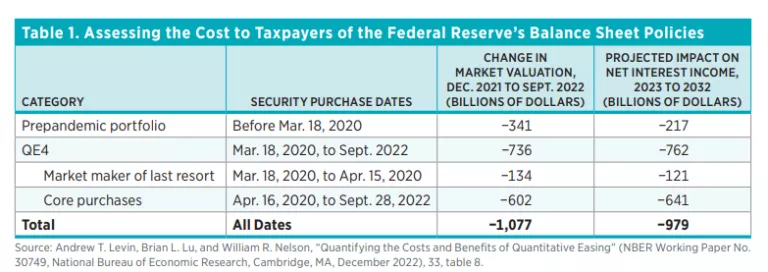

As shown in table 1, our analysis indicates that QE4 will cost taxpayers about $760 billion over a 10-year period. The Fed will absorb that cost by completely suspending its remittances to the US Treasury for the next five years and paying minimal remittances in subsequent years. The Fed’s remittances would have exceeded $100 billion per year throughout the coming decade if QE4 had not been conducted.

The remainder of this policy brief uses a question-and-answer format to address the costs and benefits of QE4.

QUESTIONS AND ANSWERS REGARDING COSTS AND BENEFITS OF QE4

Why Is This Program Called QE4?

QE refers to programs that expand the size of the Fed’s balance sheet without changing the Fed’s target for the federal funds rate or the other short-term interest rates that it directly controls. The Fed’s previous programs are commonly known as QE1 (launched in late 2008), QE2 (initiated in late 2010), and QE3 (conducted in 2012–2014).

Why Did the Fed Initiate This Program?

In March 2020, the onset of the COVID-19 pandemic induced severe strains in financial markets. The Fed promptly reduced the target federal funds rate to zero, launched a host of emergency credit facilities, and provided liquidity through the repo market (in which financial institutions can borrow overnight using safe securities as collateral). Notwithstanding these efforts, there were continuing signs of stress in the market for US Treasury securities, which serve as a core element in global financial markets.

Consequently, the Fed’s monetary policy body, the Federal Open Market Committee (FOMC), decided to initiate outright purchases of Treasuries and agency mortgage-backed securities (MBSs) in practically unlimited amounts. From mid-March to mid-April 2020, the Fed’s holdings of Treasury notes and bonds expanded by about $1.3 trillion, and its holdings of agency MBSs rose by $225 billion. Those policy measures proved effective in mitigating severe financial strains. The markets for Treasuries and agency MBSs normalized by the end of March, and conditions in shorter-term funding markets returned to normal by early April.

Why Did the Fed Maintain This Program over a Two-Year Period?

The evolution of QE4 was opaque and inertial. At the outset, the FOMC indicated that it would “closely monitor market conditions and . . . assess the appropriate pace of its securities purchases at future meetings.” Thus, once financial strains had subsided, the Fed could have considered phasing out these securities purchases while continuing to provide ample amounts of short-term liquidity, but the FOMC minutes provide no hint of such a discussion.

During late spring and summer 2020, the FOMC’s stated rationale for continued securities purchases was “to sustain smooth market functioning.” Later in the year, its statements began noting that such purchases were also intended to foster “accommodative financial conditions.” In spring 2021, Fed officials insisted that they had not yet started discussions about phasing out the program and had not even begun to “talk about talking about it.” The FOMC began tapering the amount of purchases in November 2021, and the program ended in March 2022.

The FOMC minutes provide no indication that Fed officials ever engaged in any substantive discussions of the costs and benefits of QE4 at any stage, as though its costs were minor and the benefits were clear-cut. The design of the program and the pace of purchases remained practically fixed over an 18-month period. Indeed, the large-scale purchases of agency MBSs continued during late 2020 and 2021 without regard for the booming housing market.

Is the Fed’s Budget Subject to Congressional Appropriations?

No. When the Fed was established in 1913, Congress gave it sole authority to issue paper currency. (All US currency attests to this fact, bearing the label “Federal Reserve Note.”) Over time, the Fed has expanded the outstanding stock of currency by purchasing Treasury securities from the public. Indeed, for nearly a century, currency made up nearly all the Fed’s liabilities while Treasuries made up nearly all its assets. Moreover, the Fed accrues interest on its holdings of Treasury securities but does not pay interest on paper currency, and hence its balance sheet earned a steady stream of net interest income over that period; a portion of those earnings were used to cover the Fed’s operating costs while the remainder was remitted to the US Treasury.

How Has the Fed Expanded Its Interest-Bearing Liabilities?

The Fed’s securities purchases have been funded by expanding its interest-bearing liabilities of bank reserves and reverse repos, an expansion that in turn reflects dramatic changes in the Fed’s legal authority and its operating procedures over the past 15 years. Before 2008, commercial banks’ reserves held at the Fed did not accrue any interest. Such reserves were usually kept near the minimum threshold needed to satisfy the Fed’s reserve requirements (expressed as a fraction of deposits) and comprised only 1 percent of the Fed’s total liabilities. The Fed engaged in purchases and sales of Treasuries to adjust the total stock of reserves and thereby keep the prevailing rate in the federal funds market close to the FOMC’s target. The Fed’s interest-bearing liabilities were mostly limited to small amounts of reverse repos, and the counterparties to these agreements were a narrow group of financial institutions certified as primary dealers. (In a reverse repo transaction, the Fed lends out one of its Treasury securities and borrows the corresponding amount of reserves.)

The first notable change occurred in 2006, when Congress authorized the Fed to start paying interest on reserves. This authorization was set go into effect five years after enactment.8 The reduction to the Fed’s remittances was projected to be quite modest (less than $1 billion), because reserves stood at $8 billion and short-term interest rates were roughly 5 percent. In autumn 2008, amid the intensifying Global Financial Crisis, Congress made the authorization effective immediately because the Fed’s reserves were increasing sharply as it launched an array of emergency credit facilities. However, market rates were then at historically low levels, and the Fed’s credit facilities were designed to unwind once the crisis subsided, so the cost of paying interest on reserves was still expected to be quite small.

That authorization to pay interest on reserves was a key underpinning of the subsequent expansion of the Fed’s balance sheet, because the Fed funded QE by expanding the quantity of reserves. During 2015–2017, the FOMC raised the interest rate on reserves in parallel with the target federal funds rate, thereby demonstrating that it could push up market rates without having to shrink the size of its balance sheet. Subsequently, the Fed formally adopted an “ample reserves” operating regime and set reserve requirements to zero.

During the initial stages of QE4, the Fed’s new securities purchases were almost entirely funded by further increases in reserves. In early 2021, however, the FOMC began ramping up its reverse repo operations and then established two standing facilities (one for domestic financial institutions and another for foreign official institutions) whereby such operations will continue for the foreseeable future. Consequently, the scale of the Fed’s reverse repos has expanded by an order of magnitude to about $2.5 trillion as of early January 2023—nearly as large as its reserves of about $3.0 trillion.

How Did the Fed Lose Money on QE4?

During 2020 and 2021, the US Treasury was auctioning long-term notes and bonds to “lock in” the historically low cost of financing the federal debt. However, the Fed ended up buying and holding a large proportion of those securities, thereby shortening the maturity of the net liabilities of the consolidated federal government (which encompasses the Fed).

The Fed also purchased a huge volume of MBSs during that period, when mortgage rates were at historic lows. The yields on those securities are now far below the rates that the Fed is paying on its liabilities of bank reserves and reverse repos. Meanwhile, mortgage refinancing and prepayments have fallen off sharply, thereby extending the time horizon over which this mismatch will prevail.

Are Losses to the Fed Essentially Offset by Gains to the US Treasury?

Our analysis has specifically considered these costs in terms of the consolidated federal government (which includes the assets and liabilities of the Fed as well as those of the US Treasury). The Fed purchased long-term federal debt from the public and funded those purchases by issuing overnight interest-bearing liabilities. Consequently, QE4 shortened the maturity of the consolidated federal debt, effectively leaving taxpayers more exposed to the cost of financing that debt in an environment of much higher interest rates.

In principle, QE can have substantial fiscal benefits if it accelerates economic recovery and hence boosts tax receipts and diminishes transfer payments. Such factors were particularly salient when the Fed was launching its previous rounds of QE in the context of a painfully sluggish recovery. For QE4, however, the rapid pace of recovery was facilitated by extraordinary fiscal stimulus as well as the speedy development and dissemination of COVID-19 vaccines. Moreover, our analysis does not find any significant evidence that QE4 was effective in reducing borrowing costs or spurring a stronger economic recovery.

Does It Matter Whether the Fed Incurs Interest Rate Risk or Credit Risk?

There would surely have been a massive public outcry if the Fed had purchased massive amounts of corporate debt and then written off $1 trillion in losses owing to an increase in expected defaults. But such losses would have exactly the same implications for taxpayers as the net interest costs of QE4. That said, the two types of risk are not identical. In particular, capping credit risk also limits the central bank’s involvement in the allocation of credit.

How Big Is the Cost of QE4 Compared with the Profits Made from QE1 to QE3?

Risky investments sometimes do well and sometimes do poorly, but such risk is not mitigated simply by repetition. (In financial economics, this bias toward repeating risky bets is known as the gambler’s fallacy.) During the 2010s, interest rates remained much lower than had been anticipated when the Fed conducted its first three rounds of QE, and hence the interest expense associated with funding those purchases turned out to be very low. Consequently, over that 10-year period the Fed’s balance sheet policies accrued a total profit of about $390 billion (not including the interest income from its assets funded by currency and other non-interest-bearing liabilities).

By comparison, we find that the securities held in the Fed’s portfolio as of February 2020 ( just before the onset of the pandemic) will incur negative net interest income of about $210 billion over the next 10 years. Thus, in the absence of QE4, the net effect of the Fed’s balance sheet policies on its remittances to the Treasury over the entire two decades would have been modestly positive. In the aftermath of QE4, however, the net cost to taxpayers will be nearly $800 billion.

Can the Costs of QE4 Be Dismissed as Being Merely Paper Losses?

Our analysis shows that the Fed’s remittances to the Treasury over the next ten years will be nearly $800 billion less than if the Fed had not conducted QE4. That amount is not just a paper loss; it will substantially affect the federal budget over coming years. This estimated cost is closely aligned with the change over the first three quarters of 2022 in the unrealized losses on the Fed’s current holdings of securities purchased during QE4 (see table 1). Those declines in mark-to-market valuations reflect the drop in the present discounted value of the stream of principal and coupon payments from the securities that resulted from the upward shift in the level of short-term interest rates. In effect, given that the Fed funded its purchases with overnight interest-bearing liabilities, the unrealized change in security valuations is essentially the same as the projected impact on the Fed’s remittances. And that cost will ultimately be borne by taxpayers, even if the Fed never sells any of the securities in its portfolio.

Could the Cost of QE4 Be Reduced by Suspending Interest Payments on Bank Reserves?

The interest rate on reserves reflects the opportunity cost to commercial banks and credit unions of holding funds at the Fed rather than investing those funds into other interest-bearing assets.

If the Fed were to stop paying interest to banks but make no change to its repo offer rate, then bank reserves held at the Fed would diminish rapidly while its reverse repos expand by a corresponding amount. Such an abrupt shift would have practically no effect on the Fed’s overall net interest income but would certainly be disruptive to wholesale funding markets and could potentially threaten the stability of the financial system. Alternatively, the Fed could initiate large-scale securities sales and thereby shrink all of its interest-bearing liabilities (bank reserves as well as reverse repos), but such an approach would likely be very disruptive to the markets for Treasuries and agency MBSs. Neither of these approaches would reduce the ultimate cost of QE to taxpayers. If the Fed were to reduce the interest rate paid on its reverse repos to zero as well as the interest rate it pays on reserve balances, then money market rates would fall to zero and the Fed would be unable to fight inflation.

How Large Are the Benefits of QE4 Compared with Its Costs?

Our cost-benefit analysis is broadly supportive of the Fed’s securities purchases at the onset of the pandemic, which played a key role in stabilizing the market for Treasuries and thereby helped prevent a global financial collapse. Nevertheless, those purchases will reduce the Fed’s net interest income over coming years by about $120 billion, thereby underscoring the rationale for enacting Treasury market reforms and Fed contingency plans that would alleviate the need for such interventions going forward.

Our analysis indicates that, by contrast, the continuation of QE4 beyond early spring 2020 will incur a cost to taxpayers of about $640 billion, and we do not find any significant evidence that those purchases were effective in reducing borrowing costs or spurring a stronger recovery. Indeed, the Fed’s purchases of agency MBSs may have been counterproductive in that they exacerbated the housing boom during late 2020 and 2021.

Will the Cost of QE4 Impair the Fed’s Ability to Conduct Monetary Policy?

Our analysis indicates that the costs of QE4 will not directly constrain the FOMC’s ability to adjust the target federal funds rate to foster its dual objectives of maximum employment and price stability. However, the Fed’s large footprint in the Treasury market combined with its open-ended reverse repo facility and other factors could unintentionally exacerbate financial stresses in some adverse scenarios.

Did the Fed Recognize the Interest Rate Risks Associated with QE4?

Fed officials may have expected QE4 to have minimal impact on the Fed’s remittances because they anticipated that interest rates would remain low over coming years. However, there is no indication that Fed officials considered the magnitude or asymmetry of the risks to that assessment. The possibility that QE4 would expand the Fed’s net interest income was limited because the yields on those securities were at historically low levels and short-term market rates were close to zero. By contrast, in scenarios involving robust aggregate demand and constrained aggregate supply, a surge of inflation could warrant a far higher path of short-term interest rates that would dwarf the interest income from QE4. Such a scenario emerged as a clear risk by spring 2021 and materialized over subsequent quarters.

In addition, Fed officials apparently held the view that unrealized losses would be irrelevant because any consequences to taxpayers could be avoided by holding all securities to maturity. For example, a report issued by the Federal Reserve Bank of New York in May 2021 incorrectly states that “the SOMA portfolio’s unrealized gain or loss position . . . does not reflect the expected evolution of SOMA net income.” That mischaracterization was not corrected until July 2022, well after the QE4 program had ended.

Did the Fed Alert Congress to the Risks of QE4?

Fed officials in testimony and in speeches did not inform Congress or the public that the asset purchases it conducted throughout 2020 and 2021 and into 2022 could result in significant losses and therefore put taxpayers at risk. In June 2020, shortly after QE4 began, the Fed’s semiannual Monetary Policy Report to Congress included a three-page section on the asset purchases but made no mention of interest rate risk. As QE4 continued, the Fed’s next three semiannual reports to Congress (published in February 2021, June 2021, and February 2022) included further discussion of QE4 but did not refer to interest rate risk. Likewise, the Fed’s semiannual testimonies to Congress over this period did not indicate that the Fed’s balance sheet was associated with an increasing degree of interest rate risk.

Will Congress Have to Bail Out the Fed?

Although the Fed is likely to operate at a loss during 2023–2024, it will not need any bailout funding from the Congress. Rather, the Fed will cover those operating losses by borrowing from the public, and that cumulative amount of borrowing will then be reversed as its operating income recovers to positive levels. Our analysis indicates that the Fed’s remittances to the US Treasury (which were suspended in October 2022) will not resume until 2028 and will remain well below normal levels over subsequent years. In effect, the Fed’s reduced payments to the US Treasury will offset the cost of its balance sheet policies without requiring any new appropriation of funds by Congress.

Indeed, under the Fed’s accounting approach, it will never have to report negative equity. This approach was formulated in 2010, when the Fed’s accounting manual clarified how the Fed would handle any subsequent operating losses. When the Fed does not have sufficient interest income to cover its operating expenses, it stops paying remittances and effectively borrows the amount necessary to cover its expenses by issuing additional interest-bearing liabilities to the public. On the Fed’s balance sheet, those liabilities are matched by a new book entry labeled as a deferred asset. Subsequent losses add to the deferred asset while subsequent gains reduce it. The remittances remain suspended until the deferred asset returns to zero, at which point the extraordinary liabilities have been fully offset by a corresponding amount of positive net interest income. This deferred asset was first recorded on the Fed’s books in the third quarter of 2022.

Citations and endnotes are not included in the web version of this product. For complete citations and endnotes, please refer to the downloadable PDF at the top of the webpage.