- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

The Fed’s 2024–25 Framework Review: Optimizing the Dual Mandate Through Nominal GDP Level Targeting

As the Federal Reserve considers how to implement its dual mandate of price stability and maximum employment, it should adopt—or approach—nominal GDP level targeting as a benchmark framework.

The Federal Reserve (Fed) has commenced its 2024–25 framework review. This quinquennial event will determine how the Fed implements its dual mandate to achieve price stability and maximum employment. The framework review occurs with little oversight from Congress and is not part of the standard federal regulatory process. Nevertheless, the upcoming federal review will have significant implications for the future trajectory of the price level and the business cycle, making it among the most consequential—yet often overlooked—policy events.

During the previous framework review in 2019–20, the Fed’s main monetary policy body—the

Federal Open Market Committee, or FOMC—adopted the flexible average inflation targeting (FAIT) framework. FAIT aimed to address zero lower bound (ZLB) challenges by creating an asymmetric approach to the dual mandate: It would implement makeup policy on misses below the inflation target, and it would respond to shortfalls from maximum employment. These asymmetries, while well- intended, created an inflationary bias that caused FAIT to fail the “stress test” of the 2021–22 inflation surge.

This failure caused the Fed to effectively abandon FAIT in early 2022 and become a single-mandate central bank focused on price stability. These developments indicate that the FAIT approach to the dual mandate is too narrowly focused and stands in need of an upgrade during the current framework review.

This paper argues that any changes made to FAIT should be guided by seven principles: robustness across various scenarios, symmetry in policy responses, resilience to supply shocks, a credible nominal anchor, inclusion of makeup policy, ease of communication, and support for financial stability. These principles should optimize the FOMC’s ability to effectively implement the dual mandate.

This paper is the first of a series of policy briefs by the Mercatus Center for the Fed’s current framework review. The policy briefs make the case that nominal GDP level targeting (NGDPLT) is the framework that best incorporates all seven principles, and as a result, it should be viewed as the benchmark framework by the FOMC during its review. Any revisions to FAIT, therefore, should move the framework closer to NGDPLT because it optimizes the Fed’s dual mandate.

The History of the Fed’s Framework Review

The FOMC has officially stated that it will “undertake roughly every 5 years a thorough public review of its monetary policy strategy, tools, and communication practices.”1 This process formally began with the 2019–20 framework review, but it can be seen as part of a multidecade effort by the Fed to develop and refine its implementation of the dual mandate.

The dual mandate was created by Congress in 1977 and requires the Fed to conduct monetary policy in a way that promotes “stable prices” and “maximum employment.”2 The Fed’s journey toward operationalizing the dual mandate was slow, grinding, and often opaque, since Fed officials were reluctant to define price stability and maximum employment lest they lose their discretion over monetary policy. Over time, however, they came to recognize the importance of the natural rate hypothesis, a credible nominal anchor, and the role of expectations in monetary policy.

These convictions, along with the example of other central banks that adopted explicit inflation targets in the early 1990s, spurred new interest at the Fed to define price stability. By the mid-1990s, the FOMC was actively debating an explicit inflation target while already using an implicit inflation target near 2 percent, according to some studies.3 When Ben Bernanke became Fed chair in 2006, this interest in formally defining price stability gained further momentum and prompted the FOMC to finally approve an inflation target in 2012.4

The adoption of the inflation target led to the first FOMC framework statement in 2012, now known as the “Statement on Longer- Run Goals and Monetary Policy Strategy.” The FOMC recognized both elements of the dual mandate in this consensus statement, but explicitly defined only price stability:

The inflation rate over the longer run is primarily determined by monetary policy, and hence the Committee has the ability to specify a longer- run goal for inflation. The Committee judges that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve’s statutory mandate.5

In contrast, the FOMC did not explicitly define a maximum employment target:

The maximum level of employment is largely determined by nonmonetary factors . . . and may not be directly measurable. Consequently, it would not be appropriate to specify a fixed goal for employment; rather, the Committee’s policy decisions must be informed by assessments of the maximum level of employment, recognizing that such assessments are necessarily uncertain and subject to revision.6

The FOMC, however, did acknowledge its dual mandate and affirm that it “seeks to mitigate deviations of inflation from its longer-run goal and deviations of employment from the Committee’s assessments of its maximum level.”7 This initial framework aimed to avoid overshooting and undershooting on both parts of the dual mandate.

The FOMC reaffirmed this consensus statement in the following years. The statement saw its first significant change in wording in 2016 when the FOMC added that its inflation target is a “symmetric inflation goal” and that the committee would be “concerned if inflation were running persistently above or below this objective.”8 This change, however, did not modify the underlying approach to the dual mandate but rather aimed to clarify it.

The first official framework review in 2019–20, on the other hand, did bring material changes to the implementation of the dual mandate. The resulting framework, which became known as the FAIT framework, introduced two asymmetries to the Fed’s inflation and employment goals. First, makeup policy from below the inflation target, but not from above, was added to the consensus statement noting that “following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”9 Second, the FOMC would now respond to “shortfalls of employment from its maximum level” rather than responding symmetrically to deviations from above or below it.10

Economists Gauti Eggertsson and Donald Kohn show that these changes effectively put greater emphasis on the maximum employment part of the dual mandate and created an inflationary bias to monetary policy.11 Economist Mickey Levy and former president and chief executive officer of the Federal Reserve Bank of Philadelphia Charles Plosser also note that the FAIT framework eliminated preemptive tightening for anticipated inflation, since it forces the Fed to do makeup policy and ignore signals from the labor market about the future path of inflation.12 The changes were motivated by ongoing concerns about the ZLB and by a belief that the Phillips curve was flat.13 FAIT, in short, was a framework designed to raise the average inflation rate in support of the FOMC’s more generous approach to maximum employment in a ZLB environment.

The 2024–25 framework review is the next chapter in this ongoing story of the Fed refining its approach to the dual mandate. This review will presumably address the shortcomings of FAIT that were made apparent during the inflation surge of 2021–22.

Why Does the Fed’s Framework Review Matter?

The Fed’s 2024–25 framework review is for many observers an obscure event, but it has big implications for the future path of the price level, for the Fed’s responsiveness to the business cycle, and for the democratic accountability of US monetary policy. The framework review, in short, has consequences for all of us, and it should be taken seriously.

Consider first the review’s implications for the future path of the price level. The Fed shapes the trajectory of the price level by picking a numerical inflation target and by deciding whether to do makeup policy. The inflation target determines the desired growth rate of the price level, while makeup policy commits the Fed to correcting past misses of its target. Both policies affect the average inflation rate and therefore the price- level path.

To illustrate these points, assume that the Fed raises the inflation target from 2 to 4 percent, as some have called for it to do in the past. Over the next decade, the price level would end up over 20 percent higher than it would have ended up with the 2 percent target. It is also possible for the Fed to undershoot or overshoot its inflation target. If there are enough misses, the price level could dramatically drift away from its targeted growth path. This happened to the Fed over the 2012–19 period and contributed to the FOMC’s decision in 2020 to adopt a form of makeup policy in the FAIT framework.

The past few years have demonstrated that significant departures of the price level from its expected path are strongly disliked by the public. As a result, the Fed’s framework review and the review’s potential to alter the future price- level path via a change in the inflation target or in makeup policy should be of interest to the public.

The framework review also determines how responsive the Fed will be to the business cycle. Congress has mandated that the Fed must aim for maximum employment as well as price stability, so the FOMC must determine how it will offset swings in economic activity. Under the current FAIT framework, the Fed is supposed to respond aggressively to shortfalls from maximum employment while showing less concern about an overheated economy.

This approach to monetary policy was used in 2020–21 and supported the robust recovery from the pandemic. But it also contributed to the overheated economy that followed.14 Moreover, Federal Reserve Board economist Michael Kiley shows such asymmetric frameworks can worsen the business cycle and, ironically, lead to more shortfalls from maximum employment.15 So how the FOMC decides to refine its approach to maximum employment during the 2024–25 framework review is also very significant.

The final reason that the framework review is important is that it raises questions about the democratic accountability of US monetary policy. When it created the dual mandate in 1977, Congress chose not to define price stability or maximum employment, and thereby delegated broad powers to the Fed. Neither did Congress specify how to prioritize the two parts of the dual mandate. Furthermore, the Fed is not subject to review by the Government Accountability Office or by a truly independent inspector general. As a result, when the Fed revisits how to implement its dual mandate during its framework review, it does so with minimal oversight. Since the framework review can have a significant impact on the future path of the price level and on the business cycle, this is an amazing amount of unelected power at a federal agency.16

Before the adoption of the inflation target in 2012, Fed Chair Ben Bernanke engaged in extensive consultations with Congress to ensure that the FOMC had the support of congressional oversight committees when the Fed released its first official framework.17 These congressional consultations, however, were not required by law and were not pursued as extensively in the lead- up to the adoption of FAIT in 2020.18 That FAIT would be adopted with less oversight than the original inflation target speaks to questions of democratic accountability raised by the framework review.

Seven Principles to Guide the Framework Review

FAIT, ironically, was getting started just as the biggest inflation surge in 40 years was unfolding. The FOMC stuck with FAIT for a little over a year, but eventually the Fed became “a single- mandate central bank” focused on price stability as it began an aggressive tightening cycle to counter the rising inflation.19 Both developments speak to the weaknesses of FAIT.

First, FAIT failed the “stress test” of the inflation surge. Some observers blame the FOMC’s implementation of FAIT—via its forward guidance and asset purchases plans—for this failure, but the asymmetries of FAIT, particularly the focus on shortfalls from maximum employment, create a natural inflationary bias.20 While this feature may be advantageous in a ZLB environment, it proved destabilizing during the inflation surge and suggests that FAIT is not a robust framework.21 Second, the Fed’s willingness to effectively abandon FAIT after only a year and become a single- mandate central bank also suggests that the 2020 framework’s approach to the dual mandate is too narrowly focused.

There is room, therefore, for improving how the Fed implements the dual mandate through its framework. Academic discussions and other recent deliberations about the framework review point to seven important principles that should guide the FOMC as it considers how to refine FAIT during the 2024–25 framework review:22

The framework should be robust in a variety of scenarios. The framework should not be narrowly designed for one scenario—as FAIT is designed for the ZLB environment—but should be able to handle both inflationary and deflationary scenarios.23

The framework should be symmetric. Asymmetric frameworks can exacerbate the business cycle and worsen inflation volatility; therefore, asymmetric frameworks should be avoided.24

The framework should see through supply shocks. The Fed should be able to “look through” the inflationary effects of temporary supply shocks, given that inflation expectations are well anchored. This can be tricky, since it is hard to know in real time what part of inflation is caused by supply shocks as opposed to demand shocks.25

The framework should be a credible nominal anchor. Inflation expectations need to be well anchored via a credible nominal anchor if the Fed wants to successfully see through supply shocks and other cost- push shocks.26

The framework should include makeup policy. Frameworks that promise to make up for past misses in the targeted growth rate of the Fed’s nominal anchor—rather than letting bygones be bygones—create stronger forward guidance and an enhanced ability to escape the ZLB.27

The framework should be easy to communicate. The framework should be clear and easy for the public to understand. Asymmetric frameworks that are not well specified—like FAIT—are not easy to communicate, and this can make monetary policy less effective.28

The framework should enhance financial stability. The framework should minimize the prospect of either deep financial crises or unsustainable booms in asset markets.29

Following all these principles may seem overly ambitious for the Fed framework review, as economist John Cochrane suggested while analyzing a conference panel that discussed the review:

I realized, wow, what we need in a new strategy to replace flexible average inflation targeting is getting mighty complicated. Distinguishing supply from demand shocks from fiscal shocks, dealing with crises, zero bound vs. regular policy, changes in the financial system, fiscal and financial dominance, needing to think about contingencies not forecasts, stress testing monetary policy . . . how do you write this all down?30

Fortunately, there is an approach that incorporates all seven principles into one unified framework: nominal GDP level targeting.

What Is Nominal GDP Level Targeting?

Nominal GDP level targeting is a framework in which the Fed targets total dollar spending in the economy. For every dollar spent in the economy, there is also a dollar earned in the economy. Consequently, NGDPLT is also sometimes called nominal income level targeting. Either way, if the Fed were using this framework, it would aim for a stable growth path for the dollar size of the US economy.31

To demonstrate this framework, table 1 assumes that the dollar size of the US economy is $25 trillion, and the Fed is targeting a nominal GDP growth rate of 4 percent per year, reflecting a desire for 2 percent inflation over the long run and a belief that potential real GDP growth is near 2 percent. If the Fed were able to perfectly implement this framework, then aggregate demand growth would be stabilized and the only remaining disturbances would be supply shocks.

The first set of columns in table 1 shows what happens if there are no supply shocks. Nominal GDP grows by 4 percent ($1 trillion), and the spending is evenly split, as planned, between higher prices and real economic growth. The second set of columns shows what happens if there is a negative supply shock. The economy still grows by $1 trillion, but now three- fourths of that spending ($0.75 trillion) goes to higher prices; only one- fourth ($0.25 trillion) goes to real economic growth. The third set of columns shows what happens if there is a positive supply shock. The economy, again, grows by $1 trillion, but now three- fourths of that spending ($0.75 trillion) goes to real economic growth while one- fourth ($0.25 trillion) goes to higher prices. In all scenarios, total dollar spending or aggregate demand stays the same while the inflation rate is allowed to temporarily move around in response to temporary supply shocks.

In this simple illustration, FOMC members ignore the short-run changes to inflation caused by temporary supply shocks as they focus on keeping total spending growth at 4 percent. Fed officials, in other words, are automatically “looking through” supply shocks given that their focus is on aggregate demand growth. If these shocks are random and evenly distributed, then the implicit 2 percent inflation goal holds over time as well. The FOMC gets a “two- for- one deal”: By targeting nominal GDP in the short run, it also ends up with an inflation target in the medium run.32

So far, we have assumed that the Fed always grows total dollar spending at 4 percent per year. If we relax this assumption and allow for aggregate demand shocks—from, say, financial stress or fiscal policy—then nominal GDP can miss its target. What happens in that case?

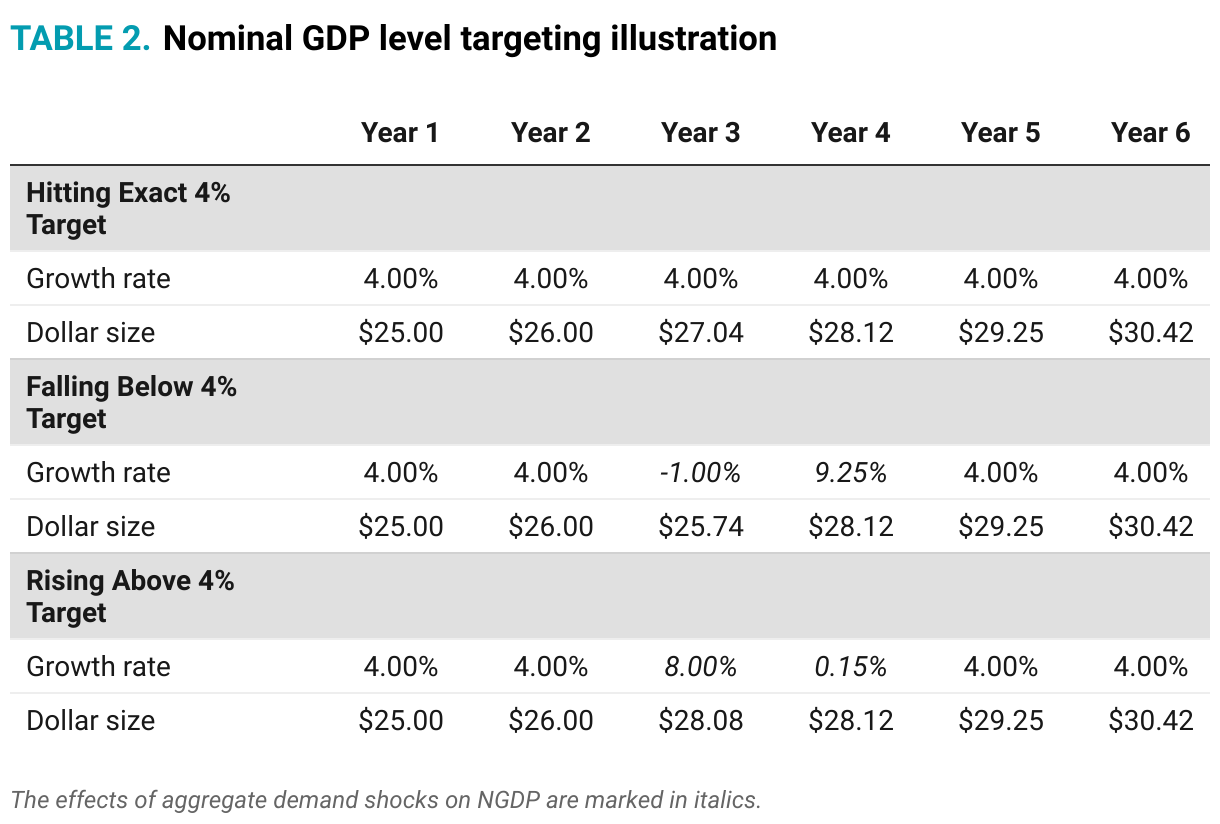

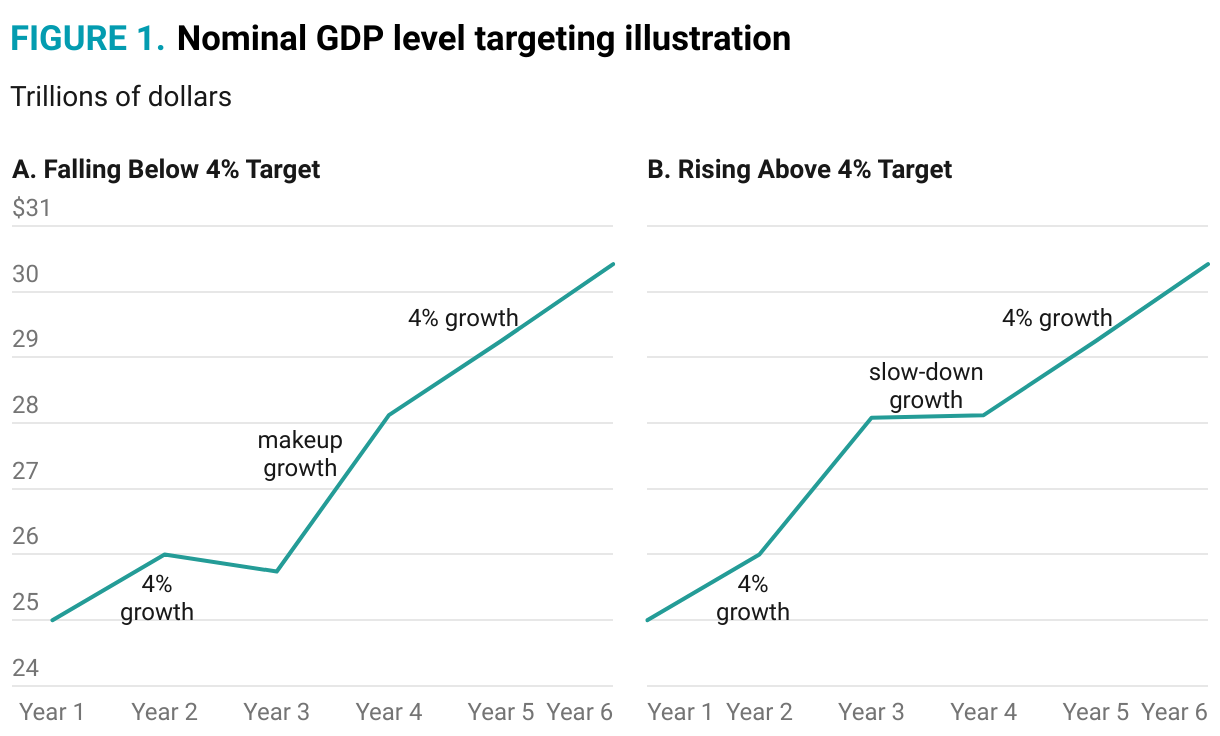

Since this is a nominal GDP level target, the FOMC makes up for past misses of its target. This is illustrated in table 2 and figure 1. Just as before, the Fed is assumed to be targeting 4 percent nominal GDP growth, and the economy starts off at $25 trillion. The first set of rows in table 2 shows what happens when the 4 percent growth objective is hit every year. The dollar size of the economy grows from $25.00 trillion in year 1 to $30.42 trillion in year 6.

The second set of rows shows what happens when negative aggregate demand shocks cause nominal GDP to contract by 1 percent in year 3. Now the FOMC must make up for the year 3 miss by growing 9.25 percent in the following year so that the nominal GDP level gets back on its original growth path and ends up at $30.42 trillion in year 6.

Figure 1B and the third set of rows in table 2 illustrate what happens when a positive aggregate demand shock causes nominal GDP to grow by 8 percent in year 3. The nominal GDP level target corrects for the overshoot by slowing down nominal GDP growth in year 4; it returns nominal GDP to its original growth path outcome of $30.42 trillion in year 6.

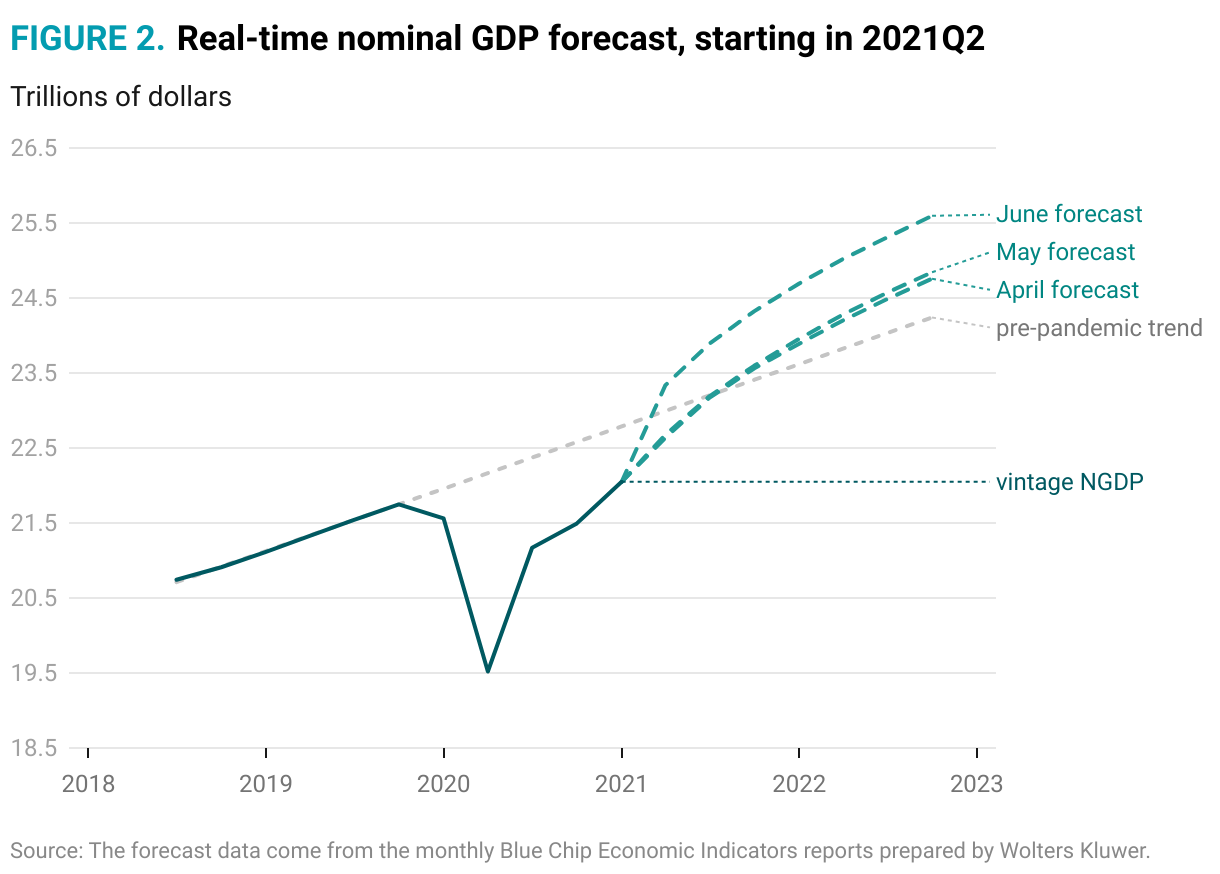

These stylized examples assume that the FOMC responds to deviations of nominal GDP from its targeted growth path ex post. The FOMC could instead adopt a forward- looking nominal GDP level target: The Fed would adjust monetary policy ex ante, on the basis of forecasted deviations of aggregate demand from its targeted growth path. For example, if the FOMC had been following a forward- looking NGDPLT framework in the early 2020s that targeted a prepandemic trend growth path, then it probably would have begun tightening in the late spring or early summer of 2021. Figure 2 shows that real-time monthly consensus forecasts for nominal GDP were projecting above-trend growth by the end of 2021 and would have informed a forward-looking NGDPLT framework during that time to start tightening monetary policy.

Figure 2 provides one example of the type of data the FOMC could draw upon to implement NGDPLT. Economist Patrick Horan and I show how to use such nominal GDP consensus forecast data in a Taylor rule–like way to operationalize NGDPLT.33 Economists Carola Binder, Skanda Amarnath, and Lars Christensen show other real- time data sources could also be used to support versions of an NGDPLT framework.34

NGDPLT Meets the Seven Framework Principles

The discussion in the previous section illustrates how NGDPLT can incorporate the first six principles outlined for the Fed framework. First, it shows how NGDPLT is robust in different scenarios because it can handle inflationary and deflationary situations. Second, it demonstrates that NGDPLT provides a symmetric response to both undershooting and overshooting of the target. Third, it reveals that NGDPLT automatically causes the FOMC to see through supply shocks without having to identify them. Fourth, it illustrates how NGDPLT provides a robust nominal anchor since it keeps the dollar size of the economy bounded to a targeted growth path. Fifth, it shows that NGDPLT, being a level target, employs makeup policy. Sixth, it indicates that NGDPLT can be understood by the public since the FOMC could communicate that it is targeting the growth path of total dollar incomes in a symmetric manner.35

Once it is internalized by the public, the NGDPLT framework will create expectations of stable total dollar spending growth that will become self- fulfilling. Households and firms will have less incentive to rapidly spend or hoard money if they believe the Fed will always correct past misses of its nominal GDP target. That is, NGDPLT would lead to the public doing most of the adjustment in spending necessary to keep nominal GDP on its target growth path.36

NGDPLT also fulfills the seventh principle—promoting financial stability—by improving risk sharing between creditors and debtors. To see how, recall that movements in inflation under NGDPLT are caused by supply shocks and are countercyclical. That is, a negative supply shock will cause a decline in economic activity and an increase in inflation given a stable growth path for total dollar spending. Conversely, a positive supply shock will cause an increase in economic activity and a decline in inflation. This countercyclical inflation, in turn, will cause real debt burdens to become procyclical and to benefit debtors during recessions and creditors during booms. NGDPLT, in short, will cause fixed-price nominal debt contracts to act more like equity and to mimic the distribution of risk that would exist if there were widespread use of state- contingent nominal debt securities.37 Such risk sharing would improve financial stability.

In addition to satisfying these seven framework principles, economists Michael Woodford, Julio Garin, Eric Sims, and Robert Lester note that NGDPLT is a way to implement a framework that approximates what is widely viewed as optimal monetary policy: an output-gap- adjusted price- level target.38 NGDPLT, however, does not suffer from the communication challenges and measurement problems associated with targeting an output-gap- adjusted price level.39 NGDPLT, in other words, is a practical way for the FOMC to deliver an optimized approach to the dual mandate.

Conclusion

NGDPLT is a valuable benchmark framework for the FOMC to consider as it contemplates revisions to FAIT during the framework review of 2024–25. The FOMC may not go all the way to NGDPLT during this review, but any step it takes in that direction will be an improvement over the present FAIT framework. The closer the FOMC moves its framework toward NGDPLT, the closer the FOMC will be to implementing its dual mandate in an optimal manner. The FOMC would do well, then, to give NGDPLT serious consideration during the 2024–25 framework review.

The arguments for NGDPLT will be developed further in forthcoming policy briefs that round out a special Mercatus series on the Fed framework review. Contributors include David Andolfatto, Carola Binder, Robert Hetzel, Peter Ireland, Evan Koenig, George Selgin, and Scott Sumner. A special Macro Musings podcast installment will provide further discussions of NGDPLT with Jim Bullard, Gautti Eggertsson, Eric Sims, and others. These contributions will address questions commonly raised about NGDPLT—how to implement it, how to communicate it, how to set the target nominal GDP growth path—and demonstrate its relevance for the Fed framework review.

About the Author

David Beckworth is the director of the Program on Monetary Policy at the Mercatus Center at George Mason University and a former international economist at the US Department of the Treasury. His research focuses on monetary policy, and his work has been cited by The Wall Street Journal, the Financial Times, The New York Times, Bloomberg Businessweek, and The Economist. He has advised congressional staffers on monetary policy and has written for Barron’s, Investor’s Business Daily, The New Republic, The Atlantic, and National Review.

Notes

- Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” January 30, 2024, https://www.federalreserve.gov/monetarypolicy/files/fomc_longerrungoals.pdf.

- The Fed is also required by law to “promote . . . moderate long-term interest rates” (12 U.S.C. § 225a), but this part of the mandate is often relegated to the background of monetary policy implementation. It is often seen as by-product of achieving price stability and maximum employment.

- Peter Ireland finds that the Fed’s implicit inflation target settled around 2 percent in 1993, while James Stock and Mark Watson find similar declines in observed inflation volatility around this time. Peter Ireland, “Changes in the Fed’s Inflation Target: Causes and Consequences,” Journal of Money, Credit, and Banking 39 (2007): 1851–81; James H. Stock and Mark W. Watson, “Modeling Inflation after the Crisis” (NBER Working Paper 16488, National Bureau of Economic Research, October 2010), 173–220. John Taylor, in his seminal study on the Taylor rule, finds that the Fed was systematically responding to the output gap and deviations of inflation from 2 percent by this time. John Taylor, “Discretion versus Policy Rules in Practice,” Carnegie-Rochester Conference Series on Public Policy 39 (1993): 195–214.

- Bernanke championed inflation targeting at the FOMC and allowed the Summary of Economic Projections in 2009 to begin reporting FOMC members’ longer-run forecasts for inflation and unemployment. These longer-run forecasts revealed FOMC members’ implicit targets for both parts of the dual mandate. In the wake of the Great Recession, Bernanke also advocated using inflation targeting as a way to stabilize inflation expectations and bolster the effectiveness of the quantitative easing programs. These efforts helped push the FOMC to adopt an inflation target. For further details on these developments, see Jeffrey Lacker, “A Look Back at the Consensus Statement,” Cato Journal 40, no. 2 (2020): 285–319.

- Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” January 24, 2012, https://www.federalreserve.gov/monetarypolicy/files/FOMC_LongerRunGoals_201201.pdf.

- Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” January 24, 2012.

- Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” January 24, 2012.

- Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” January 26, 2016, https://www.federalreserve.gov/monetarypolicy/files/FOMC_LongerRunGoals_201601.pdf.

- Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” August 27, 2020, https://www.federalreserve.gov/monetarypolicy/files/FOMC_LongerRunGoals_202008.pdf.

- The consensus statement also noted that the “maximum level of employment is a broad-based and inclusive goal” (Federal Open Market Committee, “Statement on Longer-Run Goals and Monetary Policy Strategy,” August 27, 2020). “Broad-based” and “inclusive” are not defined elsewhere in the statement, but presumably this wording implied that the FOMC would be paying attention to subsections of the labor market. Christina and David Romer argue that this change was more consequential than the asymmetries added to the inflation target and maximum employment. See Christina D. Romer and David H. Romer, “Did the Federal Reserve’s 2020 Policy Framework Limit Its Response to Inflation? Evidence and Implications for the Framework Review,” Brookings Papers on Economic Activity (Fall 2024), https://www.brookings.edu/events/bpea-fall-2024-conference/.

- Gauti B. Eggertsson and Donald Kohn, “The Inflation Surge of the 2020s: The Role of Monetary Policy” (Hutchins Center Working Paper #87, Brookings Institution, August 2023).

- Mickey D. Levy and Charles I. Plosser, “The Fed’s Strategic Approach to Monetary Policy Needs a Reboot” (paper prepared for the Hoover Monetary Policy Conference, Hoover Institution, May 2–3, 2024).

- That is, they were motivated by a belief that monetary policy could allow the unemployment rate to drop without triggering a rise in inflation. This belief was seemingly borne out by the 2015–19 period.

- Eggertsson and Kohn, “Inflation Surge of the 2020s.”

- Michael T. Kiley, “Monetary Policy Strategies to Foster Price Stability and a Strong Labor Market,” Federal Reserve Finance and Economics Discussion Series, May 2024; Michael T. Kiley, “Monetary Policy, Employment Shortfalls, and the Natural Rate Hypothesis,” Federal Reserve Finance and Economics Discussion Series, May 2024.

- Andrew T. Levin and Christina Parajon Skinner, “Central Bank Undersight: Assessing the Fed’s Accountability to Congress” (Economics Working Paper 23120, Hoover Institution, February 8, 2024).

- Lacker, “A Look Back at the Consensus Statement.”

- Levin and Skinner, “Central Bank Undersight.”

- Richard Clarida, “Fed Will Raise Interest Rates to 4% ‘Hell or High Water,’ Says Former Fed Vice Chair Clarida,” interview, CNBC, September 9, 2022, video, https://www.cnbc.com/video/2022/09/09/fed-will-raise-interest-rates-to-4-percent-hell-or-high-water-says-former-fed-vice-chair-clarida.html. Fed Chair Jerome Powell acknowledged the implicit shift to the single mandate at the July 2024 FOMC press conference by noting, “When we were far away from the inflation mandate, we had to focus on that.” Jerome H. Powell, “Transcript of Chair Powell’s Press Conference,” July 31, 2024, p. 7, https://www.federalreserve.gov/mediacenter/files/fomcpresconf20240731.pdf.

- The FOMC’s forward guidance from September 2020 to November 2021 said that the federal funds rate would be kept at 0 percent until two conditions were met: inflation at or above 2 percent and maximum employment achieved. Tying these conditions together meant that inflation above 2 percent was not enough to begin tightening monetary policy. The forward guidance was further strengthened by the FOMC’s statement from December 2020 to September 2021 that its asset purchases would wind down only if there was “substantial further progress” toward its goals. Former vice chair Richard Clarida noted that the FOMC “distinguished between the framework and the goals and the implementation of the framework through forward guidance.” Richard Clarida, “Richard Clarida on FAIT, R-Star, and the Future of the Fed’s Framework,” interview by David Beckworth, Macro Musings podcast, April 29, 2024, https://www.mercatus.org/macro-musings/richard-clarida-fait-r-star-and-future-feds-framework.

- Eggertsson and Kohn, “Inflation Surge of the 2020s”; Levy and Plosser, “Fed’s Strategic Approach”; Kiley, “Monetary Policy Strategies”; Kiley, “Monetary Policy, Employment Shortfalls, and the Natural Rate Hypothesis.” Michael Kiley never mentions FAIT explicitly, but his analysis is premised on a FAIT-like framework and is clearly motivated by the Fed’s experience with FAIT.

- For a summary of conference discussions (held at the Brookings Institution and the Hoover Institution) on how to improve the Fed framework, see Sam Boocker and David Wessel, “Advice for the Federal Reserve’s Review of Its Monetary Policy Framework,” Brookings Institution, July 10, 2024; John H. Cochrane, “Hoover Monetary Policy Conference, with Videos,” Grumpy Economist, May 15, 2024. See also the annual economic report of the Bank for International Settlements on the lessons learned from the pandemic for monetary policy frameworks: BIS (Bank for International Settlements), Annual Economic Report, June 2024, chap. 2: “Monetary Policy in the 21st Century: Lessons Learned and Challenges Ahead.”

- BIS, Annual Economic Report, June 2024, chap. 2; Eggertsson and Kohn, “Inflation Surge of the 2020s”; Athanasios Orphanides, “Enhancing Resilience with Monetary Policy Rules” (Economics Working Paper 24109, Hoover Institution, May 2024).

- Eggertsson and Kohn, “Inflation Surge of the 2020s”; Kiley, “Monetary Policy Strategies”; Kiley, “Monetary Policy, Employment Shortfalls, and the Natural Rate Hypothesis”; William B. English and Brian Sack, “Challenges Around the Fed’s Monetary Policy Framework and Its Implementation,” Brookings Papers on Economic Activity (Fall 2024), https://www.brookings.edu/events/bpea-fall-2024-conference/.

- David Beckworth and Patrick Horan, “A Two-for-One Deal: Targeting Nominal GDP to Create a Supply-Shock Robust Inflation Target,” Journal of Policy Modeling (forthcoming); Jerome H. Powell, “Opening Remarks” (speech at Monetary Policy Challenges in a Global Economy conference, International Monetary Fund, November 9, 2023).

- Jón Steinsson, “Thoughts on Fed Policy and the Fed’s Framework” (paper presented at “Getting Global Monetary Policy on Track,” Hoover Monetary Policy Conference, Hoover Institution, May 3, 2024).

- Kiley, “Monetary Policy Strategies”; Kiley, “Monetary Policy, Employment Shortfalls, and the Natural Rate Hypothesis.”

- Kiley, “Monetary Policy Strategies”; Kiley, “Monetary Policy, Employment Shortfalls, and the Natural Rate Hypothesis”; Levy and Plosser, “Fed’s Strategic Approach.”

- BIS, Annual Economic Report, June 2024, chap. 2.

- Cochrane, “Hoover Monetary Policy Conference.”

- Some observers also view NGDPLT as a velocity-adjusted money supply target. For more on this perspective, see David Beckworth, “Facts, Fears, and Functionality of NGDP Targeting: A Guide to a Popular Framework for Monetary Policy” (Mercatus Policy Research Paper, Mercatus Center at George Mason University, 2019).

- Beckworth and Horan, “Two-for-One Deal.” Michael Woodford similarly notes that “a commitment to a nominal GDP level path is completely consistent with a commitment to a medium-term inflation target.” Michael Woodford, “Inflation Targeting: Fix It, Don’t Scrap It,” in Is Inflation Targeting Dead? Thinking Ahead about Central Banking after the Crisis, ed. Lucrezia Reichlin and Richard Baldwin (London: Centre for Economic Policy Research, 2013), 6. Robert Hetzel has suggested a similar idea, in which the “FOMC announces benchmarks for nominal GDP growth that over time align with the FOMC’s long-term inflation target.” Robert Hetzel, “How to Ensure That Inflation Will Remain at the Federal Reserve’s 2 Percent Target” (Mercatus Policy Brief, Mercatus Center at George Mason University, December 2021), 2.

- David Beckworth and Patrick Horan, “The Fate of FAIT: Salvaging the Fed’s Framework,” Southern Economic Journal (forthcoming).

- Carola Binder, “Nominal Income Expectations of Consumers” (Mercatus Working Paper, Mercatus Center at George Mason University, May 2023); Skanda Amarnath, “Tracking Gross Labor Income in Real-Time without Revision,” Employ America, July 31, 2024; Lars Christensen, “Fed’s Hidden Strategy: Implementing New Dual NGDP Targets,” Market Monetarist, July 5, 2024.

- Households’ expected nominal income growth from the University of Michigan Survey of Consumers has been found to be a good predictor of disposable income and consumption expenditures over the next two years. Mariacristina De Nardi, Eric French, and David Benson, “Consumption and the Great Recession,” Economic Perspectives (Federal Reserve Bank of Chicago) 36, no. 1 (2012): 1–16. One could use this measure for NGDPLT. Binder, “Nominal Income Expectations.”

- Carola Binder argues that NGDPLT could overcome the “deficit of understanding and . . . of trust” that plagues most inflation targeting. Carola Binder, “NGDP Targeting and the Public,” Cato Journal 40, no. 2 (2020): 322.

- For more on the financial stability argument for NGDPLT, see Evan Koenig, “Like a Good Neighbor: Monetary Policy, Financial Stability, and the Distribution of Risk,” International Journal of Central Banking 9, no. 2 (2013): 57–82; David Beckworth, “The Financial Stability Case for a Nominal GDP Target,” Cato Journal, Spring/Summer 2019; James Bullard, “James Bullard on FAIT, Nominal GDP Targeting, and the Fed’s Upcoming Framework Review,” interview by David Beckworth, Macro Musings podcast, July 22, 2024, https://www.mercatus.org/macro-musings/james-bullard-fait-nominal-gdp-targeting-and-feds-upcoming-framework-review.

- Michael Woodford, “Monetary Policy Accommodation at the Interest-Rate Lower Bound” (paper presented at the Kansas City Federal Reserve Economic Symposium, 2012); Julio Garin, Eric Sims, and Robert Lester, “On the Desirability of NGDP Targeting,” Journal of Economic Dynamics and Control 69 (2016): 21–44.

- Michael Woodford, for example, notes that

the nominal GDP target path represents a compromise between the aspiration to choose a target that would achieve an ideal equilibrium if correctly understood and the need to pick a target that can be widely understood and can be implemented in a way that allows for verification of the central bank’s pursuit of its alleged target. (Woodford, “Monetary Policy Accommodation,” 230)

Similarly, Julio Garin, Eric Sims, and Robert Lester find that

nominal GDP targeting typically performs very well, in many instances almost as well as gap targeting. A potential advantage of nominal GDP targeting over gap targeting is that the former is easily observed, whereas the gap is based on a hypothetical model construct that is likely difficult to observe even ex-post, much less in real time. A nominal GDP target is likely also far easier to communicate to the public than a gap targeting rule. (Garin, Sims, and Lester, “On the Desirability of NGDP Targeting,” 40)