- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Fiscal Dominance: How Worried Should We Be?

INTRODUCTION

When new Prime Minister Liz Truss’s surprise plans to raise fiscal spending and cut taxes were revealed by Kwasi Kwarteng, the United Kingdom’s chancellor of the exchequer, on September 23, 2022, bond markets crashed. Primary budget surpluses are the cash flows that back government bonds. Lower surpluses make bonds less attractive, reducing demand for them. Sterling depreciated 4.7 percent against the dollar, and yields on long-term gilts rose 100 basis points in the days that followed. Five days later, the Bank of England announced that “to restore orderly market conditions,” it would buy long-dated government bonds “on whatever scale necessary” until October 14; after that date, the bank would begin to shrink its balance sheet (Bank of England 2022). Not until the chancellor was replaced and Truss ultimately resigned on October 20 did markets return to preannouncement levels. This is fiscal dominance.

The European Central Bank (ECB) unveiled a new monetary policy tool on July 21, 2022, “to counter unwarranted, disorderly market dynamics.” The tool permits the ECB to buy sovereign bonds issued by a member nation whose bond yields are “not warranted by country-specific fundamentals” (ECB 2022a). Financial reporters immediately interpreted the policy as designed to reduce Italian bond yields, which were elevated during Italy’s summer of political uncertainty, a significant departure from the ECB’s standing policy to buy sovereign bonds of member states in fixed proportions (ECB 2022b). This is fiscal dominance.

From March 2020 to March 2021, the US Congress passed a series of COVID-related relief bills that raised federal government spending by $5 trillion, financed by new borrowing. Legislation was couched as “emergency expenditures,” so the usual congressional budget procedures and haggling were suspended. As White House Press Secretary Jen Psaki framed a subsequent bill, “It’s important to note that we believe this should be provided on an emergency basis, not something where it would require offsets” (White House 2022). The political environment and the “emergency” modifier communicated that the spending and its associated financing were different from ordinary expenditures: the transfers individuals and firms received were “gifts” that would not have to be repaid with interest through higher future taxes. Since the beginning of last year, the Federal Reserve has been raising interest rates aggressively to combat the inflation that the congressional fiscal gifts brought with them. This is fiscal dominance.

The British and eurozone examples are instances in which fiscal developments triggered financial stability concerns for central banks tasked with maintaining smoothly functioning financial markets. The American case entails a fiscal policy that breaks from Hamilton’s (1790b) norm—deficits beget surpluses as future tax revenues adjust to pay interest and principal on newly issued government liabilities—to create an inflationary episode. Their common theme is that some fiscal action forces the central bank to react in ways that it otherwise would not. The examples communicate the flavor of fiscal dominance.

They underscore a critical implication of fiscal dominance: it is a threat to central bank success. In each example, the central bank was free to choose not to react to the fiscal disturbance—central banks are operationally independent of fiscal policy. But that choice comes at the cost of not pursuing a central bank legislated mandate: financial stability or inflation control. Central banks are not economically independent of fiscal policy, a fact that makes fiscal dominance a recurring threat to the mission of central banks and to macroeconomic outcomes.

WHAT IS FISCAL DOMINANCE?

The introduction uses the term fiscal dominance as if its meaning is widely understood. It isn’t. Understanding monetary or fiscal dominance begins by appreciating that at the most fundamental level, monetary and fiscal policies must achieve the prime directive: determine and control the aggregate price level—and its rate of change, inflation—and stabilize the level of government indebtedness to ensure those policies are sustainable. Without first accomplishing this directive, policies cannot achieve any of the myriad other tasks that societies demand: economic growth, high employment, financial stability, desirable income distribution, public safety, national defense, and so on. Though the directive seems prosaic, it is the core mission of monetary and fiscal policies. Look at any historical case of hyperinflation or serial sovereign debt default to appreciate how failure to execute the mission undermines an economy and fractures a society.

Economic theory tells us that two distinct policy arrangements can deliver the prime directive:

- A monetary policy that aggressively adjusts its policy instrument to keep inflation on target coupled with a fiscal policy that raises primary surpluses whenever real government debt is above some desired level. In this regime of monetary dominance, monetary policy controls inflation and fiscal policy behaves passively to keep debt stable. Many economists believe the United States resided in this regime from about 1982 until the financial crisis in 2007/08.

- A fiscal policy that sets primary surpluses independently of real government debt combined with a monetary policy that ensures interest payments on outstanding debt do not make debt grow too rapidly. In this regime of fiscal dominance, fiscal policy drives inflation, and monetary policy passively stabilizes debt. This regime describes US policies from the suspension of convertibility of dollars to gold in 1933 until the Treasury-Fed Accord in 1951.

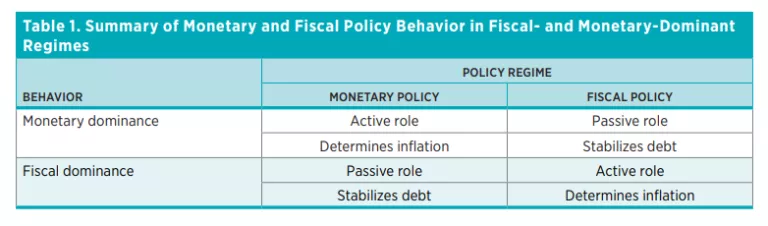

Table 1 summarizes the two policy regimes that determine inflation and stabilize debt. Notice that these arrangements describe joint monetary-fiscal regimes.

If one policy is dominant— what Leeper (1991) calls “active”—then the other policy must be supportive, or “passive.” Two dominant policies cannot coexist indefinitely. One policy must relinquish dominance eventually to become passive.

There is nothing inherently “bad” about fiscal dominance or “good” about monetary dominance, according to conventional economic theory that does not factor in policymakers’ personal incentives. This may be surprising: after all, by creating independent central banks with mandates to control inflation, many countries seem to have revealed a preference for monetary dominance. Countries made that choice to address political incentives, rather than for purely economic reasons. Theoretically, any economic outcomes that a monetary-dominant regime delivers, a fiscal-dominant regime can replicate.

Then why does fiscal dominance strike fear in the hearts of economists and financial markets? Perhaps it does so because we can all point to extreme examples where fiscal policy runs the show and monetary policy is subjugated to fiscal needs. Outcomes are not pleasant.

Germany’s hyperinflation in the early 1920s may leap to mind first. Saddled with large war debts and postwar reparation payments, the Weimar government soon realized it could not raise the necessary resources through direct taxes, so it turned to rapidly printing paper marks to generate seigniorage revenues. With seigniorage came ever-increasing inflation.2 This instance fits well into Sargent and Wallace’s (1981) definition of fiscal dominance as arising when fiscal constraints force the monetary authority to generate seigniorage revenues and sacrifice inflation control.

Turkish policy in recent years offers a modern variant. President Recep Tayyip Erdoğan, who declared high interest rates the “mother and father of all evil,” installed three heads of the central bank in two years in a search for a loyal central banker who would execute the president’s low interest rate policies. Since 2021, when inflation was 19 percent, it has risen to between 70 and 150 percent, depending on whether we use official or outside economists’ measures. Erdoğan effectively converted an independent inflation-targeting central bank into a fiscal ATM. With monetary policy firmly under his control, Erdoğan is now expanding fiscal spending to “soften the blow of hyperinflation,” a move certain to exacerbate inflation (Hubbard 2023). Again, monetary policy serves fiscal needs.

Leaning too heavily on extreme cases can lull us into the belief that as long as monetary policy decisions are independent of political leaders, the economy is insulated from fiscal dominance. This policy brief led with three subtle examples of fiscal dominance to make this point: each case involved an operationally independent central bank. Fiscal dominance need not imply fiscal policy run amok. It can arise anytime policy makes the path of primary budget surpluses impervious to economic conditions such as inflation.

Monetary policy independence is a bulwark but not an impenetrable barrier against fiscal dominance. The Reagan administration began with inconsistent plans for monetary and fiscal policy (Sargent 1986). At the same time that the administration supported Federal Reserve Chair Paul Volcker’s goal of wringing inflation out of the economy through tight monetary policy (monetary dominance), it announced tax cuts and defense spending increases that implied a persistent path of primary deficits (fiscal dominance). Two dominant policies cannot coexist indefinitely because they cannot achieve the prime directive: each policy requires a different inflation path and neither policy stabilizes debt. Sargent credits Neil Wallace with describing the conflict between policies as a game of chicken. Which policy would flinch to avoid an economic crash? As Sargent (1986, 36) put it, “Reaganomics was not credible because it was not feasible.”

Fiscal policy flinched. After Reagan’s signature Economic Recovery Tax Act of 1981, a series of 11 tax bills followed from 1982 to 1993 whose cumulative effect four years after enactment was to increase revenues by $279.1 billion, swamping the $176.7 billion reduction from the 1981 legislation (Tempalski 2013). Fiscal behavior switched to passively raise surpluses as the tax cut and early 1980s recession raised debt. Although monetary policy did ultimately prevail, it was not without political drama and substantial uncertainty. A fiscal policy that explicitly tied the 1981 tax cuts to subsequent increases in primary surpluses would have reduced uncertainty and avoided the costly game of chicken by placing the economy firmly in the monetary-dominant regime.

Countries that have adopted some form of inflation targeting seek to live in a monetary-dominant regime. That includes most advanced economies and an increasing number of emerging market economies. No country claims to consciously pursue fiscal dominance. Here is the important point: because “regime” embeds both monetary and fiscal behavior, an inflation-targeting central bank alone cannot ensure monetary dominance; fiscal policy must passively respond to monetary actions. Clashes between the two policies can and do occur; those clashes are a central theme of this policy brief.

Before getting into the clashes, we need to explore how fiscal behavior differs between the monetary- and fiscal-dominant regimes.

Under monetary dominance, the accompanying passive fiscal policy is not dormant. It does most of the heavy lifting. When the central bank raises interest rates to fight inflation, interest payments on outstanding debt rise. Today, debt is 100 percent of gross domestic product (GDP). Many analysts believe the Fed will raise the funds rate to at least 5 percent, lifting Treasury yields across bond maturities. Within a couple of years, interest payments will add $1 trillion annually to the federal deficit. Passive fiscal policy supports monetary contraction by raising primary surpluses to cover the additional debt service. Monetary and fiscal policies pull in the same contractionary direction.

Passive fiscal policy also takes care of itself by following the Hamilton norm.3 Budget deficits financed by Treasury borrowing are ultimately followed by primary budget surpluses to pay interest and possibly principal on the new bonds. By acting to stabilize government debt, fiscal policy minimizes its impacts on inflation and frees the central bank to control inflation.

Fiscal dominance is starkly different. In the face of rising nominal debt and interest payments, fiscal policy refuses to raise surpluses. Further borrowing pays the interest, boosting nominal bond growth. Because surpluses are unresponsive to debt growth, bondholders do not perceive that the new bonds carry IOUs—future tax liabilities—so higher government debt becomes higher private-sector wealth. With higher wealth comes higher demand for goods and services and higher inflation. Because fiscal policy is not acting to stabilize debt, that task must fall to monetary policy. The central bank no longer aggressively raises interest rates to fight inflation. Instead, it allows a higher price level to reduce the real value of the government’s liabilities. Higher prices convert growing nominal debt into stable real debt.

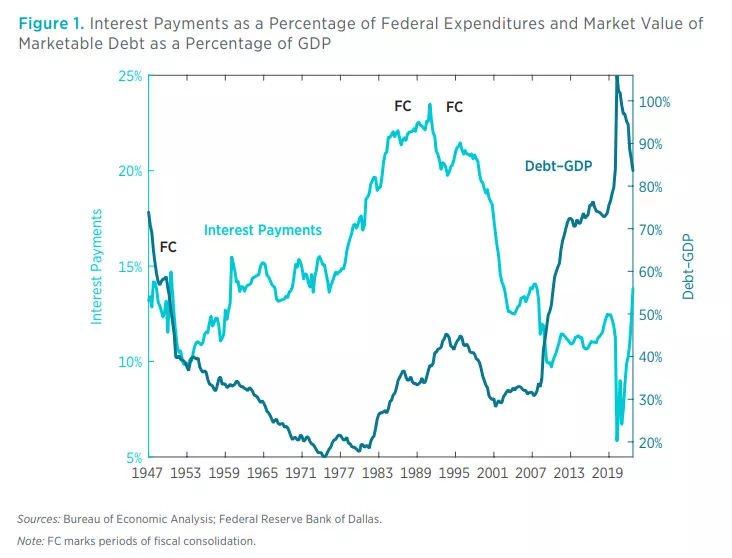

In the United States, interest payments as a share of federal expenditures, rather than the debt– GDP ratio, predict episodes of fiscal consolidation, the sterile term for tax hikes and spending cuts. Figure 1 plots interest payments and federal debt during the postwar era. Interest payments are percentages of federal expenditures, and debt is a percentage of GDP. Three periods are marked FC to denote times when significant fiscal consolidations were undertaken.

The first consolidation helped retire World War II debt. Two consolidations occurred during the 1980s and 1990s when debt was about 40 percent of GDP, but interest payments consumed more than 20 percent of federal spending. Debt service is rising sharply now, from a low of 5.9 percent in the second quarter of 2020 to the latest figure, 13.8 percent in the fourth quarter of 2022. Over the same period, debt’s value has fallen from 106 percent to 84 percent through a combination of a lower price for the government bond portfolio and higher nominal GDP. Absent fiscal tightening, interest can be expected to continue its rapid rise, but if Congress behaves true to form, it may still be years before it undertakes consolidation.

Times of low interest rates are times of low interest payments even when debt is elevated. In 2020, debt peaked exactly when interest payments bottomed out. This observation explains why elected officials like central banks to maintain low rates.

BRANDS OF FISCAL DOMINANCE

Just as fiscal dominance is not necessarily bad, it is also not necessarily good. The point of creating independent central banks tasked with controlling inflation—an idea that dates back to Hamilton’s (1790a) proposal for the First Bank of the United States—was to take money creation out of the hands of elected officials who may be tempted to use it for political gain instead of social wellbeing. Because fiscal policy can have powerful impacts on the price level, it is both ironic and troubling that countries do little to guard against fiscal dominance. Independent monetary policy coupled with politically driven fiscal policy is the policy environment democracies have chosen, but it makes little economic sense. Fiscal actions can still drive monetary policy choices, as the UK, eurozone, and US examples illustrate.

I now describe three brands of fiscal dominance. The first arises when policymakers seek to reduce government debt but unwittingly make fiscal policy dominant. A second brand sneaks up on the economy as policy reaches its fiscal limit. The final category is a uniquely American fiscal lunacy that suddenly imposes fiscal dominance in the pursuit of political leverage.

Unwitting Dominance

Many countries have unwittingly adopted fiscal rules that make fiscal policy dominant. Suppose a fiscal authority deems the current debt–GDP ratio unacceptably high, as many countries did in the wake of the financial crisis. A common approach announces a path for primary surpluses that over some horizon will retire debt to some desired level. If at the same time the country experiences inflation below target, the central bank will lower interest rates to stimulate demand. But lower interest rates reduce interest payments on existing debt. In a monetary-dominant regime, fiscal policy must respond to lower debt service with smaller surpluses: fiscal expansion follows monetary expansion. Because this passive fiscal response seemingly conflicts with the goal of reducing debt, the debt-targeting fiscal authority may choose to maintain its announced contractionary plans. By announcing a path for surpluses that is independent of the central bank’s efforts to target inflation, the fiscal authority adopts a dominant stance that clashes with monetary dominance.

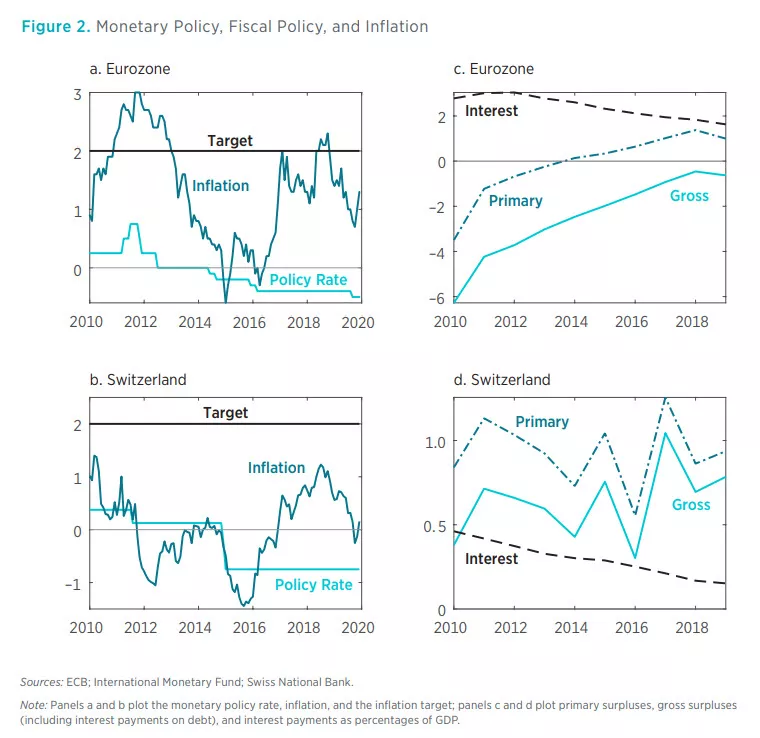

Coming out of the financial and the sovereign debt crises, countries in the European Union agreed to a “fiscal compact” in 2012 that calls for signatories to adopt fiscal rules that deliver general government budgets that are balanced or in surplus (ECB 2012). Country-specific medium-term fiscal objectives needed to be consistent with the balanced budget rule, subject to deviations in “exceptional circumstances.” Figure 2 plots the monetary policy interest rate, inflation rate, and inflation target (panels a and b) and the primary surplus, gross surplus, and interest payments on the debt as percentages of GDP (panels c and d) for the eurozone and Switzerland.

During the four years between 2013 and 2017, when eurozone inflation was below target and even negative, the ECB took its policy rate negative. It also doubled its balance sheet during those years. Eurozone fiscal policy, meanwhile, became progressively tighter even as interest payments on debt fell steadily. Fiscal contraction clashed with monetary expansion, thwarting the ECB’s efforts to raise inflation.

Switzerland’s case is more pronounced. As an early adopter of a debt brake in 2006—which placed severe limitations on structural deficits, even in the aftermath of the financial crisis—Switzerland ran gross and primary surpluses to steadily reduce its debt–GDP ratio. Inflation was chronically and substantially below target for a decade. Despite the Swiss National Bank’s heroic stimulus efforts—interventions to depreciate the franc, a policy rate of −0.75 percent, and a quadrupling of the balance sheet during the 2010s—inflation remained far below its 2 percent target. From 2015 to 2019, nominal yields on Swiss government bonds averaged −0.64 percent on 5-year maturities and −0.19 percent on 10-year maturities. Throughout this period of unprecedented monetary ease, primary surpluses stayed high and debt service declined.

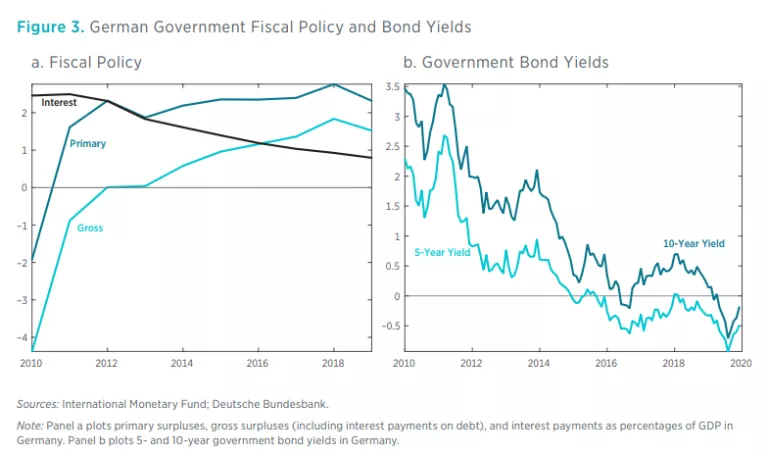

The German fiscal experience is telling (figure 3). After Germany adopted a debt brake in 2009, fiscal policy swung from running sizable deficits during the financial crisis to large primary surpluses in a couple of years. Interest payments dropped quickly to below 1 percent of GDP. With the fiscal tightening came long-term nominal German government bond yields that turned negative at both 5- and 10-year maturities. Negative nominal yields in the face of ever-tighter fiscal policy are prima facie evidence of a contractionary fiscal stance.

Fiscal rules have been developed primarily to solve political problems. These are legitimate concerns. But in addressing political economy issues, the rules may inadvertently make fiscal policy dominant. Dominance creates economic problems by preventing fiscal authorities from appropriately backing monetary policy. Policy conflicts emerge from an enduring belief that monetary and fiscal policy can operate independently of each other even when their objectives may be mutually exclusive. Doubly dominant policies are a frequent source of conflict. It certainly is not providing the fiscal expansion needed to support the ECB’s efforts to reflate.

Insidious Dominance

Policies can gradually approach fiscal dominance. Every economy has a fiscal limit, the point at which it is no longer possible to raise tax revenues or reduce expenditures. Economic behavior may underlie the limit, for example, when tax rates are high enough to reach the peak of the Laffer curve. But long before the economic limit, voters can impose a limit through their limited tolerance for high taxes or low government services. At the fiscal limit, primary surpluses reach their maximum.

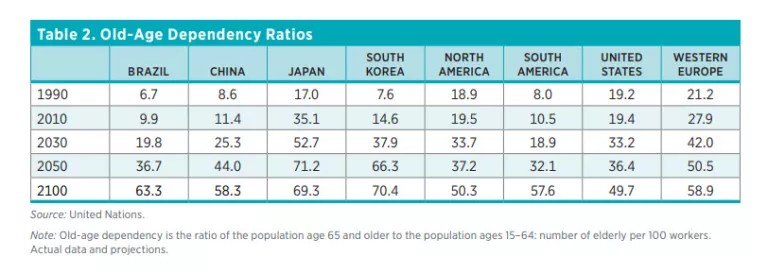

Economies worldwide are aging rapidly. Table 2 reports the number of elderly people per 100 workers for select countries and regions. Japan is aging the fastest, followed closely by South Korea. By 2030, Japan will have two workers per retiree and Korea will have three workers per retiree. Relative to other countries, the United States is in better shape going forward, but this does not mean America is prepared for what lies ahead.

Governments have pledged to support retirees through pension and healthcare plans. With only rare exceptions—such as Norway—promises were made without providing financing. Instead, oldage benefits are funded largely out of current tax revenues. As the benefits grow with the aging populations, it becomes increasingly untenable to rely on taxing the shrinking share of workers: economies will hit their fiscal limits.

At the fiscal limit, policies must change. Government could renege on promised support by increasing retirement ages or cutting benefits. That is a form of passive fiscal policy that would be consistent with monetary dominance and an inflation-targeting central bank. Or government could move to a fiscal-dominant regime in which promised support is maintained by permitting inflation to devalue government debt or by raising seigniorage revenues.10 Most likely, government would adopt the political expedient that mixes some reneging on promises with higher and more volatile inflation.

This brand of fiscal dominance is insidious for two reasons. First, because demographics evolve slowly, fiscal consequences can be stealthy. One study finds that expected inflation rises, but almost imperceptibly, in the period before the economy hits the fiscal limit. Possible inflationary outcomes, though, can be extreme, as there is a small probability of very high inflation rates (Davig, Leeper, and Walker 2011). In such an environment, resources will get diverted from productive uses to create hedges against the costly inflation possibilities.

A second subtle harmful effect stems from the uncertainty that arises from unresolved policy problems. By postponing necessary adjustments, policy forces both retirees receiving old-age benefits and workers paying for the transfers to speculate about likely resolutions. Will Social Security and Medicare be around when I retire? How high will tax rates go, and when will they rise? What government services will old-age benefits crowd out? The best that even the most informed people can do is attach probabilities to possible resolutions. And wrong guesses can be extremely costly to individuals and society. Economic costs of enhanced uncertainty from policy dillydallying are difficult to quantify, making it hard for voters to hold the dillydalliers accountable.

Political Dominance

Alexander Hamilton’s vision that a secure public debt would acquire many of the features of money—it would be default free, liquid, and widely accepted—to underpin the financial development of the United States has been realized. US Treasury securities are the world’s go-to safe asset. During the global financial crisis that began in 2007, international investors flocked to Treasuries, keeping yields and inflation low despite rapid increases in bond supply. Safe Treasuries are critical to the dollar’s reserve currency status, an “exorbitant privilege” that Eichengreen (2013) estimates to be worth about 2 percent of American GDP.

Three times in 12 years—in 2011, 2013, and 2023—Congress has initially refused to raise the statutory limit on US federal debt, potentially extinguishing Hamilton’s dream and America’s special financial status. Political acts that undermine the safety of public debt constitute a special class of fiscal dominance that simultaneously threatens both inflation and financial stability and forces the Federal Reserve to choose which of its legislated mandates to pursue.

The value of US Treasuries is a fragile thing. It derives from a 200-year-old norm of adopting policies that back new bond sales with primary surpluses. Because those surpluses rise after the bonds have been bought, investor faith that the Hamilton norm will be maintained supports the bonds’ value. Blithe statements by elected representatives about using the debt ceiling as a bargaining chip can erode that faith.

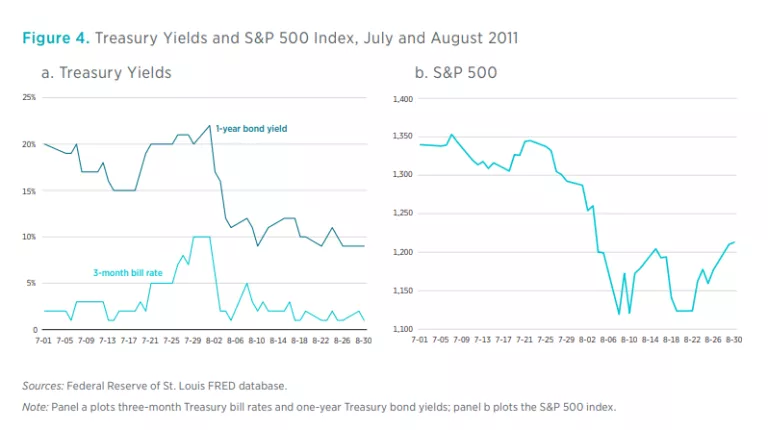

In 2011, the first time the debt ceiling was offered in a bargain, financial markets were rattled. Ebbs and flows in negotiations created uncertainty that raised short-term interest rates (figure 4, panel a) and drove down stock prices (panel b), particularly during midsummer months.

Even if everyone believes the ceiling will eventually be lifted so outright default is a remote possibility, prudent investors have to place some probability on that dire outcome. In 2011, short rates rose as investors shifted from liquid short positions to less liquid long positions. Relatively short-term Treasuries are a key source of collateral in repurchase agreements. If the private sector creates substitutes for traditionally perfectly safe Treasuries, risk rises in financial markets. As it happened, the impacts of the debt-ceiling debacle on financial prices were fleeting, concentrated between mid-July and early August. But the direction of impacts is a cautionary tale for today.

The years 2011 and 2023 differ in important ways. In 2011, the federal funds rate was resting at the effective lower bound near zero for the foreseeable future; today, its target range is 4.75 to 5 percent and likely to rise further. Consumer price inflation was 3 percent; in 2022, it was 8 percent. At the end of 2011, marketable Treasury debt was $9.9 trillion; in December 2022, it stood at $23.8 trillion. Interest payments on the debt—the minimal expenditures necessary to avoid default—are poised to explode. Without higher taxes or lower spending, those mandatory payments can be met only by new bond sales that will need to grow more rapidly than in earlier debt-ceiling episodes.

With new debt issuance frozen, the only feasible fiscal policy going forward is to balance the budget inclusive of interest payments. But that requires congressional and presidential buy-in that no one believes will happen. How should a Fed in the midst of battling inflation behave? So far, the Fed remains focused on inflation reduction. But politically driven fiscal dominance may eventually force the Fed to abandon its disinflationary policies in favor of stabilizing bond markets.

One need not take a stand on the merits of cutting federal government spending—the demand of the opponents to raising the ceiling—to recognize that this is a dangerous negotiating strategy. Politically induced fiscal dominance jeopardizes the things that make the United States the world’s financial center: safe government assets and low, stable inflation. It also threatens to undermine the ability of monetary and fiscal policies to achieve their prime directive.

FISCAL DOMINANCE WORRIES

Conventional economic theory alone gives us little reason to worry about fiscal dominance. But theory doesn’t operate in a vacuum: policy choices are driven by political considerations as well as economic considerations. In fiscal policy, politics generally wins the day. Perhaps political dominance is a more accurate label than fiscal dominance. Societies have largely, though not completely, removed central banks from the threat of political dominance, while keeping fiscal policy firmly tethered to the political mast.

Periodic episodes of fiscal dominance are inevitable. Fiscal dominance in Europe before COVID arose from good intentions to reduce government debt by setting surpluses independently of what the ECB was trying to do to raise inflation. Nothing terrible happened; in fact, many Europeans were happy to have inflation below the 2 percent target. Situations like this can be avoided simply by redesigning fiscal rules to include a component that ties budget surpluses to inflation.

Emergencies are common periods of fiscal dominance. Governments provided substantial relief during COVID shutdowns to help families that were thrown out of work. We can argue about how much help was provided, but the emergency nature of the spending is undeniable. That governments treated the spending as gifts rather than as loans was intentional, geared toward encouraging consumption spending, rather than saving, to keep the economy going. It is not surprising that $5 trillion worth of gifts financed by an equivalent expansion in government liabilities was inflationary. Inflation might even be an optimal source of fiscal finance during emergencies. Because the inflation appears to have been unanticipated, it acts as a nondistorting tax on bondholders. The alternative labor or capital tax financing would distort behavior and reduce economic activity.

Unfortunately, governments want something for nothing: to hand out $5 trillion in transfers financed by creating new “money” but not pay for it with higher inflation rates. The Federal Reserve is now mopping up after the fiscal party. Whether it will succeed in returning inflation permanently to the 2 percent target hinges less on its own actions than on Congress’s willingness to tighten fiscal policy. Even an independent central bank cannot control inflation if fiscal policy is dominant.

Troubling and potentially costly forms of fiscal dominance seem destined to arise whenever elected politicians endanger the safety and soundness of US government credit to gain political leverage. To me, this is the primary source of worries about fiscal dominance for several reasons. First, political dominance recurs and inevitably erodes perceptions of US Treasuries as safe assets, with all the attendant costs of that erosion. Second, the threat of fiscal dominance is not the outgrowth of some external shock like the COVID pandemic. It is homegrown and completely avoidable. One way to avoid it is through the adoption of implementable and enforceable fiscal rules. Economics is one input to the design of such rules, but as a practical matter, without fully accounting for political incentives, economically determined rules are pointless: they have little chance of being adopted; if adopted, they are unlikely to be obeyed. The perennial constitutional amendment for a balanced budget is no answer: it is a political solution that emasculates fiscal policy and precludes its potential beneficial impacts.

But we also cannot ignore this dangerous source of fiscal dominance. Perhaps it is time for a fundamental rethink of how America conducts its fiscal policy. No blue-ribbon commissions, just thoughtful people who recognize we have a problem and are willing to work toward a solution that institutionalizes a monetary dominant regime: fiscal behavior that is compatible with an inflation-targeting monetary policy.

Citations and endnotes are not included in the web version of this product. For complete citations and endnotes, please refer to the downloadable PDF at the top of the webpage.