- | Policy Briefs Policy Briefs

- |

The Five Channels of Debt Reduction: Economic and Policy Tools for Reducing the Debt-to-GDP Ratio

A few months ago, one of us (Kling) predicted that by 2030 the United States would be in a dilemma in which rising inflation could no longer be controlled by higher interest rates, owing to the large national debt:

"A scenario that I find plausible is that by 2030 the United States will have transitioned to a high-inflation regime. The Federal Reserve will be powerless to prevent such a transition. If it attempts contractionary policies, the interest rate on government debt will go up. With the debt/GDP ratio as high as it is, this would threaten a fiscal crisis by sharply raising the amount of tax revenue that has to be devoted to making interest payments. If instead, the Fed seeks to hold down the government’s interest costs, it will have to do so by making massive new purchases of government bonds, thereby putting more monetary fuel onto the inflationary fire."

His prediction turned out to be correct, except the United States faces that dilemma now, not in 2030. Therefore, Congress and the Federal Reserve (Fed) are under pressure to resolve the dilemma and get inflation under control.

It is generally understood that to control inflation the Fed must raise nominal interest rates above the inflation rate, so that real interest rates are positive. Economist Lawrence Summers explains: “The central principle of anti-inflationary monetary policy is that to reduce inflation, it is necessary to raise real rates. Equivalently, it is necessary to raise interest rates by more than the inflation being counteracted and above a neutral level that neither speeds nor slows growth.” Thus, with inflation at 8.5 percent, nominal interest rates must rise significantly for real interest rates to reach positive territory.

Such a development would significantly increase the amount of interest Congress pays on the portion of the national debt that it rolls over. Given a debt-to-GDP ratio of 100 percent, and given that roughly 30 percent of the debt has a maturity shorter than a year, a steep increase in nominal interest rates from their current level to above the inflation rate would increase interest payments quickly.

Higher interest payments crowd out other spending and effectively impose “fiscal consolidation”—that is, austerity—which is politically unpopular. In addition, higher interest payments would themselves likely be deficit financed, which could throw more oil on the inflation fire. This outcome would be dangerous and expensive. However, failing to raise interest rates risks accelerating inflation, at least until all inflationary pressure has dissipated. With inflation at 8.5 percent, this risk is significant, especially given that even the Fed’s promise to raise interest rates to 2.75 percent leaves the inflation-adjusted cost of borrowing at a stunning −5.75 percent.

These unappealing scenarios create substantial political pressure for the Fed to accommodate fiscal outlays. Deciding monetary policy on the basis of fiscal concerns is called “fiscal dominance” and usually entails keeping interest rates constant despite inflation so interest payments do not increase.

The United States may avoid fiscal consolidation and fiscal dominance if inflation subsides after the Fed raises the federal funds rate moderately as it plans to. However, this is not a reason to be complacent about US debt levels. The good news is that although reducing the debt-to-GDP ratio is difficult, painful, and politically unpopular, it can be done. The United States has done it three times since World War II. Other countries have too.

International Monetary Fund economists Carmen Reinhart and M. Belen Sbrancia have catalogued the five main channels through which countries have achieved this goal: (1) economic growth; (2) substantive fiscal adjustment or austerity plans; (3) explicit default or restructuring of private debt, public debt, or both; (4) a surprise burst in inflation; and (5) a steady dose of financial repression accompanied by an equally steady dose of inflation.

In this policy brief, we look at the different channels for debt-to-GDP ratio reduction and assess their desirability for the United States now.

Getting Out of Debt

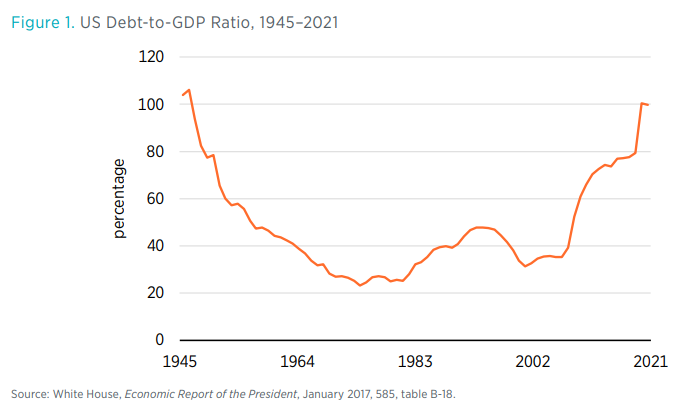

After World War II, the most dramatic reduction in the US debt-to-GDP ratio occurred during 1946 to 1974 (see figure 1), owing largely to primary surpluses during most of that period. The reduction was also aided by rapid real economic growth, a severe inflation shock in 1969–1979, and financial repression. A period of growing debt and high interest rates soon followed as bond “vigilantes” punished the government for its prior inflationary transgressions. The debt-to-GDP ratio again fell during 1994 to 2001, thanks to robust growth and spending restraint, before resuming its growth, which continues today.

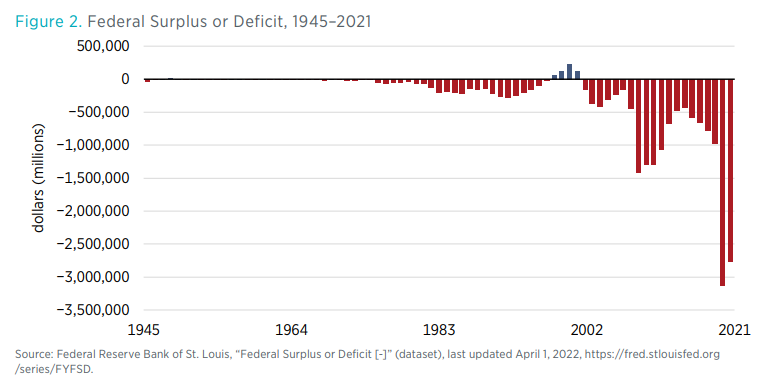

During the reduction of 1946–1974, much federal government spending was rolled back. Economist David Henderson reports how federal government spending on goods and services fell by more than one-third of GDP in two to three years: “The U.S. government did not retain direct controls after 1946, did not taper off war production gradually, and did not provide much work relief. From Samuelson’s list, the only recommendation that it implemented was [to] provide unemployment compensation for out-of-work World War II veterans, and only a small [percentage] of these veterans took advantage of this program." In other words, the United States engaged in a lot of austerity by reducing spending. As a result, in almost every year between 1947 and the early 1970s, the government ran a primary surplus, even though it was reporting total deficits for most of the period (see figure 2).

Because receipts during 1947–1969 exceeded noninterest spending, outstanding principal was reduced. Moreover, while the rest of the budget ran a deficit, Social Security ran a surplus, and government accounting did not combine the two until the end of the Lyndon B. Johnson administration. Had such a combined measurement been in use before then, it would have shown many years of total budget surpluses.

According to the Federal Reserve Bank of Richmond, to keep its interest payments low, the federal government actively used financial repression, especially during the 1960s and 1970s:

"To sustain the peg while maintaining the latitude for discretionary monetary policy, the United States imposed a new type of capital control in 1963 called the Interest Equalization Tax. The measure attempted to stem capital outflows from the United States by placing a 1 percent tax on foreign bonds sold in the U.S. market (the tax was later extended to short-term bank loans to foreigners). This was followed by various executive branch efforts to improve the U.S. balance of payments, including the use of “moral suasion” to put pressure on U.S. firms to repatriate funds and on U.S. allies to forgo converting their dollar holdings into gold."

The government also kept in place interest rate ceilings, prohibited banks from paying interest on demand deposits (such as checking accounts), and implemented a few other measures.

In addition, the Fed assisted the government in keeping its interest payments low: Between 1940 and 1951, it accommodated the enormous increase in deficits (driven primarily by defense spending) to prevent a default on government bonds. As a result, according to the Fed, “between June 1946 and June 1947 Consumer Price Index (CPI) inflation was 17.6 percent, and from June 1947 to June 1948 it was 9.5 percent. . . . By February 1951, CPI inflation had reached an annualized rate of 21 percent.”

The concern over inflation led to the Treasury–Federal Reserve Accord in 1951, which aimed at separating government debt management from monetary policy. Upon signing the accord, participants issued a statement that they had “reached full accord with respect to debt management and monetary policies to be pursued in furthering their common purpose and to assure the successful financing of the government’s requirements and, at the same time, to minimize monetization of the public debt.” The Fed successfully dedicated itself to anti-inflationary policies and sustaining stable exchange rates until at least the 1960s.

The inflation of the 1970s assisted the government in its efforts to keep its interest payments under control, though the inflation did not lower the debt-to-GDP ratio as much as the fiscal restraint and economic growth of the earlier decades. Although economic performance was weak during the 1970s, the unexpected inflation kept nominal GDP growth high relative to interest rates. Bondholders’ losses were the government’s gain, so even though the government started to run primary deficits, the debt-to-GDP ratio edged down further, to less than 24 percent.

Robust growth, reductions in defense spending, and reductions in the growth rate of nondefense discretionary spending drove the final episode of decreasing debt-to-GDP ratio in 1994–2001. The debt-to-GDP ratio fell from 47.7 percent to 31.4 percent, and the US government balanced its budget during 1998–2001.

Reducing the Debt Today

The prospects for repeating the post–World War II decreases in the debt-to-GDP ratio are weak. Of the five debt reduction channels mentioned earlier, the most desirable seem unlikely, leaving the United States with the channels that are problematic, albeit most attractive to policymakers.

Economic Growth

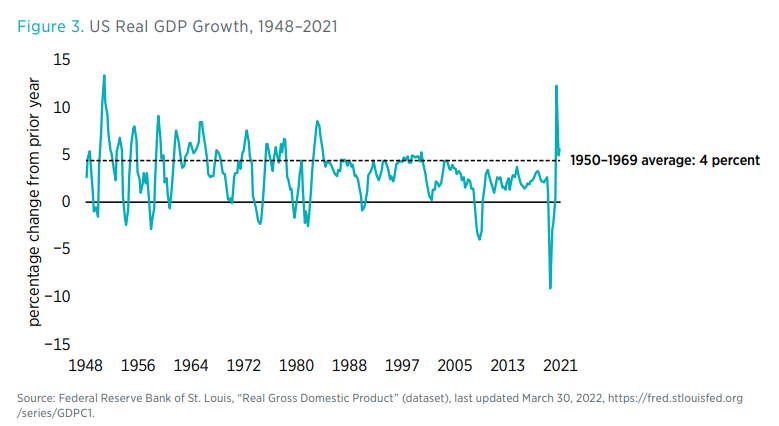

Growing out of the debt would be by far the best option. In addition to reducing the debt-to-GDP ratio, growth has many positive side effects. Unfortunately, without life-transforming economic innovations, the prospect of the United States growing out of its debt is very weak. As shown in figure 3, real economic growth over the past 50 years has remained well below the levels achieved in the 1950s and 1960s, which averaged about 4 percent annually.

Real GDP growth went from greater than 4 percent in the 1960s to around 3 percent in the 1970s to less than 2 percent in the past decade, and this trend of slowing real GDP growth is projected to continue. The Congressional Budget Office predicts an average annual real GDP growth in the United States of 1.7 percent over the next 30 years assuming that there will not be a major recession. In addition, the projected average annual growth rate for 2026–2031 (1.6 percent) is less than that of the past decade (2.0 percent).

There is a debate over the importance of factors such as slowing productivity growth, declining factor utilization, and changing demographics and cultural attitudes toward work in contributing to lower real growth rates. For instance, labor force participation increased significantly from the 1960s to 2001, largely owing to increased female labor force participation. In the early part of 2000–2010, with men leaving the labor force for a variety of reasons, and with female participation flat or declining, overall labor force participation fell. The country also experienced slower growth in the working-age population and in hours worked per worker.

A decline in productivity growth in particular slows the growth in real GDP. Part of the reason for the decline could be the large growth in regulations since the 1960s and 1970s. Also having a negative impact on economic growth is high government spending. Some research suggests that higher debt levels slow economic growth. Other research suggests that economic growth is depressed by high levels of taxation. In particular, studies show an inverse relationship between marginal tax rates and changes in the pace of economic activity.

Unless the trends toward less labor force participation and slower productivity growth are dramatically reversed, the United States will not grow out of its current debt.

Soft Default via Surprise Inflation

A more plausible, though undesirable, mechanism for lowering the debt-to-GDP ratio in the United States is surprise inflation. The higher inflation rates of the past few months have come as a surprise to many Americans, including Fed officials. In addition, even though Americans are now experiencing inflation rates unseen since 1982, the best market estimate of future inflation—namely, the spread between Treasury bonds that are indexed for inflation and nonindexed securities—indicates that investors expect annual inflation over the next 10 years to average close to 2 percent. In part, this indication reflects investors’ confidence that the Fed will act to prevent higher rates of inflation from becoming endemic.

However, one should remember that long-term inflation expectations are notoriously bad at predicting sudden bursts of inflation. The actual rate of inflation depends on the interaction between Fed monetary policy and public expectations of inflation. For example, the effect of accommodative monetary policy on inflation will be less if people expect low inflation. If people believe that inflation will be high and variable, then they try their best to protect against it: they will shorten the term of agreements; they will incorporate cost-of-living escalators into labor bargains; or they will minimize their holdings of currency or other noninterest-bearing assets. One saw these behaviors in the high-inflation era of the 1970s; they reinforced the high inflation, and it took the entire decade of the 1980s to return to an era of low and stable inflation.

Investors may be surprised by high inflation at first, but they will soon adjust their behavior. So the interest cost of new debt is likely to rise if inflation persists. The cost savings from inflation apply primarily to the stock of long-term debt currently outstanding. Unfortunately, for this purpose, a large share of the debt is short term (30 percent has a maturity of a year, and over 60 percent has a maturity of four years). In other words, surprise inflation could lead to a fiscal crisis, forcing either a hard default or severe austerity measures before the government can achieve a significant reduction in the debt-to-GDP ratio.

Explicit Default or Restructuring of Public Debt

The government could explicitly pay bondholders less than the full principal and interest owed. Many governments have done this, and some governments are even known as serial defaulters, as noted in the 2009 book This Time Is Different: Eight Centuries of Financial Folly by Carmen Reinhart and Kenneth Rogoff. Explicit default is not a thing of the past, as some believe. According to the Congressional Research Service, since the end of 2019, six countries (Argentina, Belize, Ecuador, Lebanon, Suriname, and Zambia) have defaulted on sovereign debt obligations.

But an explicit default would be unprecedented for the United States, and the consequences of it would be devastating. Although the United States would never pursue this path voluntarily, the country has one important vulnerability that ultimately could lead to a default: surprise inflation. With at least $6 trillion that the US Department of Treasury needs to repay and borrow every single year, the United States could face a short-term debt rollover crisis followed by a run on the dollar and a large and fast increase in interest rates, putting the United States in an untenable fiscal situation or default, owing to its large debt. This situation will come about if short-term investors seriously fear that they will not get repaid—if they fear, in other words, that the Fed will fail to control inflation in the future as a way to reduce the debt-to-GDP ratio.

Financial Repression with Well-Anticipated Inflation

“Financial repression” is a term used to describe policies that artificially raise the demand for government bonds and thus result in lower yields. The goal is to enable government to service its debt. If central banks inflate such that repressed bond yields turn negative in real terms, some government debt gets liquidated, and the real value of the debt is reduced.

Financial repression requires regulators to close off existing alternatives to sovereign debt in domestic and foreign markets. Countries with repressive financial regimes impose stringent controls on capital markets to prevent money from fleeing government debt for private securities and foreign assets.

Some traditional financial repression tools include wage and price controls, a ceiling on interest paid on bank deposits, explicit or implicit caps on interest rates, and mandates that require banks and other intermediary institutions to hold government debt. Other possible measures include high reserve requirements (or liquidity requirements), securities transaction taxes, prohibition of gold purchases, and restrictions on cryptocurrencies. As Reinhart, Jacob Kirkegaard, and Sbrancia note, “financial repression is most successful in liquidating debts when accompanied by a steady dose of inflation, and, like inflation alone, it only works with debts denominated in domestic currency. Low nominal interest rates help reduce debt servicing costs, while a high incidence of negative real interest rates liquidates or erodes the real value of government debt. Inflation need not take market participants entirely by surprise and need not be very high (by historical standards).” Such measures were in place during World War II and leading up to and during the great inflation of the 1970s, until they were abandoned in the liberalization wave of the 1990s.

Thankfully, with today’s sophisticated financial markets providing many avenues for capital mobility, financial repression is more difficult. One tool that has emerged in recent years is risk-based capital requirements that steer banks toward holding government debt. Some scholars have suggested that international bank regulatory standards (such as Basel III) encourage banks to hold government debt by giving it preferential treatment for satisfying capital requirements and act as a modern form of financial repression.

Perhaps one could argue that the Fed policy of massive purchases of government debt aimed at keeping nominal and real interests low—or even negative—can act as a de facto form of financial repression because it reduces the real value of existing debt and, therefore, becomes the equivalent of a transfer from creditors (savers) to borrowers, including the government. Looking at the past 50 years, one sees seven notable periods of negative rates: 1973–1976, 1979–1980, 2002–2004, 2008, 2010–2014, 2016–2018, and 2019–present. The first two periods were clearly the product of inflation at the time. However, it is hard to tell if negative real rates since the Global Financial Crisis are the result of financial repression or other factors, such as demographics and lower growth pressures.

Financial repression poses major risks. Attempts by other countries to implement financial repression have created problems of capital flight, with citizens trying to evade regulations by finding ways to send money overseas. The United States has often benefited from capital inflows as a result, an example of the “safe haven effect.” If the United States were to implement strong financial repression, the United States might not only lose its status as a safe haven, but it could even experience outflows of capital.

Substantive Fiscal Adjustment and Austerity Plans

Austerity is a proven way to reduce the debt-to-GDP ratio, provided that any fiscal adjustments are properly composed. The general consensus in the literature is that fiscal adjustment packages made up mostly of spending cuts are more likely to lead to lasting debt reduction than those made up mostly of tax increases. Also, fiscal adjustments based mostly on spending cuts are less likely to be reversed and, as a result, have led to more long-lasting reductions in debt-to-GDP ratios, especially if they were rooted in reforms of social programs and reductions in the size and pay of the government workforce, rather than in other types of spending cuts. These fiscal adjustment packages result in higher growth in the long term. Also, any short-term economic slowdowns that result from spending-based fiscal adjustments are generally mild and short lived, especially compared with tax-based fiscal packages.

After economic growth, austerity seems like the most desirable way to go about reducing the debt-to-GDP ratio. As mentioned earlier, a failure to reduce the debt-to-GDP ratio makes it harder for the Fed to control inflation and increases the chance of fiscal dominance. Unfortunately, the probability that Congress will voluntarily adopt a fiscal adjustment package based on spending cuts to reduce the debt-to-GDP ratio is low, for a few important reasons.

First, historically, only 20 percent of countries that have tried to reduce their debt-to-GDP ratio through austerity have succeeded. One explanation for the low success rate is that even—or perhaps especially—in times of crises, legislators are driven more by politics than by any desire to promote the long-term public good. Countries generally get into fiscal trouble through years of catering to pro-spending constituencies—be they senior citizens or members of the military industrial complex—and these countries’ fiscal adjustments make the same mistakes too many times. As a result, failed fiscal consolidations are more the rule than the exception.

Second, fiscal adjustment would be harder today than it was immediately after World War II. At that time, almost all federal spending was discretionary, and half of that spending was for the military. In addition, after the war, the public did not object to returning to a peacetime budget by shrinking the defense budget. Things are quite different today. Discretionary spending accounts for less than 30 percent of the total federal budget in fiscal year 2023, which makes cutting spending politically difficult. Of course, cutting mandatory spending would be preferrable, but this option presents some political challenges that have so far been insurmountable. Although an opportunity to cut mandatory spending will present itself when the Social Security trust funds run out of money in a few years, politicians, under pressure from special interests, may resort to only smaller reductions in spending and larger tax increases. Unfortunately, such an approach is not conducive to successful debt-to-GDP ratio reduction.

In addition, although fiscal discipline has never been a priority of the Washington, DC, establishment—as evidenced by the United States’ permanent primary deficit since 1969 and the unchecked expansion of programs such as Social Security and Medicare—the willingness of leaders in Washington, DC, to forgo current spending expansion out of a desire to maintain fiscal discipline has completely evaporated.

Whereas vigorous debates about austerity took place in the aftermath of the Global Financial Crisis (National Economic Council Chair Lawrence Summers stated that the stimulus enacted in response to the crisis should be “timely, targeted, and temporary”), no such debates occur today. In fact, several academics have suggested that controlling government debt is unnecessary, because either interest rates are permanently low or the country can print money to escape its fiscal troubles.

Yet, as the dilemma closes in and America faces the choice of either letting inflation get out of control or letting interest rates rise to provoke a fiscal crisis, fiscal adjustment will have to be on the table.