- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

How to Ensure That Inflation Will Remain at the Federal Reserve’s 2 Percent Target

With year-over-year consumer price index (CPI) inflation in November 2021 at 6.8 percent, inflation is in the headlines. The issue is whether such high inflation is transitory, given that the CPI is dominated by categories of goods and services whose prices reflect only the rapid recovery of the economy and COVID-19 pandemic-related supply disruptions. As such, the Federal Open Market Committee (FOMC) of the Federal Reserve should allow inflation to pass through to the price level and await a return to the longer-term inflation rate of 2 percent. Certainly, there are outsized increases in some categories. In November 2021, energy prices (year-over-year) rose 33.3 percent, with gasoline up 58.1 percent and natural gas up 25.1 percent. Prices of used cars and trucks rose 31.4 percent. Such increases reflect the working of supply and demand and should be accommodated.

Although much of inflation is transitory, determining the level at which inflation will settle down requires knowing the proportion of underlying inflation that is created by monetary policy. And to know that proportion, one must first describe current monetary policy, especially how it changed in response to the pandemic. One then needs a framework (model) that forecasts inflation. Unfortunately, there is no consensus on the nature of inflation. Is inflation a nonmonetary phenomenon whose control turns on how the FOMC controls the amount of slack in the economy? Alternatively, is inflation a monetary phenomenon whose control requires control over money creation?

The monetary policy announced by Chair Jerome Powell in his August 2020 Jackson Hole speech positions the FOMC on the side of inflation as a nonmonetary phenomenon. The policy is a clear break from the monetary policy developed in the Volcker–Greenspan era. Moreover, such an aggressively expansionary policy has not been seen since the 1970s. Given the uncertainty over the nature of inflation and the monetary policy required to control it, I suggest that the FOMC announce benchmarks for nominal GDP growth that over time align with the FOMC’s long-term inflation target. Such benchmarks would serve what economist Scott Sumner calls “guardrails,” which in this case would prevent misunderstanding about the nature of inflation from causing a sustained rise in inflation.

This policy brief first elucidates the dramatic break in monetary policy announced by Powell at his Jackson Hole speech. It then explains how Odyssean forward guidance has locked the FOMC into an aggressively expansionary monetary policy. Next, it highlights the uncertainties associated with success of the new policy. Those uncertainties include the inflationary implications of a sharp departure from the policy developed in the Volcker–Greenspan era. They also include the possibility of underestimating the degree of stimulus of the new policy. The brief then reviews the debate over whether the high inflation in 2021 is transitory. Given the uncertainties associated with the new policy and the high inflation of 2021, the brief finishes by suggesting that the FOMC use growth in nominal GDP as an intermediate target to make credible its commitment to the long-term achievement of its 2 percent inflation target.

Characterizing the New Policy

The monetary policy announced by Chair Powell in his Jackson Hole speech August 2020 relies on the assumption that inflation is a nonmonetary phenomenon. The underlying framework of the policy was first described by economists Franco Modigliani and Lucas Papademos. The central relationship in the framework is a Phillips curve in which changes in inflation are inversely related to the difference between the unemployment rate and a value termed the nonaccelerating inflation rate of unemployment (NAIRU). (This terminology was pioneered by economist James Tobin in 1980.) If the Fed is responsible for controlling inflation, it follows that the FOMC possesses sufficient control over aggregate real demand that it can predictably control the difference between the unemployment rate and the NAIRU, at least if the latter is known.

The Powell policy targets a specific unemployment rate as well as a specific level of inflation. The unemployment rate targeted by the Fed is described as socially desirable, low, and “inclusive,” which in this context means low enough to provide a strong job market in minority communities. More concretely, with the new policy, the FOMC aims to restore prepandemic conditions in the labor market. Powell notes,

"In the later years of the long expansion that ended with the pandemic, the benefits of employment continued to spread more widely and to reach those at the margins of the economy. Prior to the pandemic, unemployment was at 50-year lows. Wages had been moving up, and meaningfully so, especially on the lower ends of the pay scale. Many who had struggled for years were finding jobs. Racial disparities in unemployment were narrowing."

When the unemployment rate is an independent target, there needs to be some way of predicting the joint behavior of unemployment and inflation. The Phillips curve, which relates the unemployment rate and inflation, of necessity, becomes the key relationship organizing monetary policy. It was belief in such a relationship that prompted a highly stimulative monetary policy in response to the pandemic. In April 2020, the unemployment rate shot up to 14.8 percent from a low of 3.5 percent in February 2020. The pattern in the post-Volcker recessions had been attainment of a cyclically low unemployment rate through prolonged recoveries. The Phillips curve provided the assurance that stimulative monetary policy could greatly accelerate this process. Inflation would not be a problem until the unemployment rate had fallen below its prepandemic low of 3.5 percent.

Paul Krugman describes the belief that the prior pattern of prolonged, slow recoveries in the labor market resulted in wasteful unemployment:

"Unemployment dipped below 4 percent both at the end of the 1990s and at the end of the 2010s, in each case without provoking accelerating inflation . . . . And if low unemployment doesn’t lead to accelerating inflation, it seems all too likely that we have consistently been running the economy too cold, sacrificing jobs and output unnecessarily. While the Fed hasn’t explicitly admitted this, it’s clearly a regret that weighs on its policy now."

The Powell policy is a revision of the policy used in the recovery from the Great Recession when Janet Yellen was FOMC chair. During that recovery, the FOMC implicitly used the Modigliani-Papademos framework for predicting inflation, as evidenced by the FOMC’s decision to raise the federal funds rate from the zero lower bound at the December 16, 2015, FOMC meeting, even with inflation somewhat below the 2 percent target. At this meeting, FOMC participants, in their summary of economic projections (SEP), estimated the long-run unemployment rate to be 4.9 percent. They considered that estimate to be an estimate of the NAIRU. In the Tealbook produced for the meeting, the staff of the Board of Governors of the Federal Reserve estimate the natural rate of unemployment, the counterpart to NAIRU, at 5.1 percent in Q4 2015, and they predicted that the unemployment rate would decline gradually to 4.5 percent in Q4 2018. The median SEP projection for the unemployment rate in Q4 2016 was 4.7 percent. With the economy forecast to grow strongly enough to push the unemployment rate below the presumed NAIRU and thus raise inflation to the 2 percent target, the FOMC raised the federal funds rate target by a quarter percentage point. In doing so, it stated, “The Committee judges that there has been considerable improvement in labor market conditions this year, and it is reasonably confident that inflation will rise, over the medium term, to its 2 percent objective.”

Inflation did not rise as predicted but remained below the FOMC’s 2 percent target. Given the assumption that the FOMC controls slack in the economy (the unemployment rate) to control inflation, and given that inflation data have, since the Great Recession, lacked a clear relationship with unemployment data, the Powell FOMC has concluded that the Yellen FOMC kept the unemployment rate too high and that the economy was moving along a flat portion of the Phillips curve. The Powell policy thus aims to prevent repeating this mistake by running an expansionary monetary policy to lower the unemployment rate until it discovers the NAIRU, marking the start of the upward sloping section of the curve. At that point, inflation will rise.

In his press conference following the November 3, 2021, FOMC meeting, Powell explained the actions of the FOMC within the new framework in light of the inflation that had emerged by fall 2021. The assumption by the FOMC of responsibility for an inclusive, low rate of unemployment was clear. In response to reporters’ questions about the criteria for liftoff (that is, for raising the federal funds rate off the zero lower bound), Powell stated that the FOMC would need to have reached its goal for maximum employment (a low rate of unemployment). Powell declared “We don’t meet the liftoff test now because we’re not at maximum employment. . . . We didn’t ask ourselves whether the liftoff test is met because, you know, it’s clearly not met on the maximum-employment side.”

In fall 2021, according to the FOMC, monetary policy needed to remain aggressively expansionary to reduce the slack evidenced by the shortfall from maximum employment. Powell stated, “I don’t think that we’re behind the curve. . . . The reason is that there’s still ground to cover to get to maximum employment.” A working assumption by the FOMC is that as a result of the economy expanding, the labor force participation rate will rise to its prepandemic level and draw additional workers into the labor force. Powell stated, “We think about maximum employment as looking at a broad range of things. . . . You could be in a situation, hypothetically, where the unemployment rate is low, but there are many people who are out of the labor force and will come back in. And so you wouldn’t really be at maximum employment.”

By fall 2021, inflation had risen significantly. However, given the presumed slack in the economy and the assumption that inflation is a nonmonetary phenomenon, the FOMC reasoned that the current inflation must be a transitory phenomenon reflecting the shortages arising from reopening of the economy after the COVID-19 recession. Powell stated,

“We don’t think it’s time yet to raise interest rates. There is still ground to cover to reach maximum employment, both in terms of employment and in terms of participation. . . . Our baseline expectation is that supply bottlenecks and shortages will persist well into next year, and elevated inflation as well, and that, as the pandemic subsides, supply chain bottlenecks will abate—and job growth will move back up. And as that happens, inflation will decline from today’s elevated levels. . . . We should see inflation moving down by the second or third quarter.”

Odyssean Forward Guidance

The preceding section characterizes monetary policy in terms of the consistency it imposes on FOMC decision-making over time. Also important for understanding FOMC behavior is the forward guidance the FOMC has adopted to implement monetary policy. Rather than simply articulating a reaction function specifying how it would respond to incoming new information (news) on the economy, the FOMC in August 2020 heavily constrained its ability to change the expansionary character of monetary policy (hence, my reference to Odysseus, who tied himself to the mast to prevent seduction by the sirens).

As evident in the following remarks by Fed Governor Randal Quarles, in 2020, given cyclically high unemployment and below-target inflation, the FOMC considered its targets of restoring an inclusive, low unemployment rate and raising inflation as consistent rather than posing a tradeoff. A return to the kind of expansionary monetary policy not seen since the 1970s then seemed warranted. Quarles explained, “Last December, with inflation running well below 2 percent and unemployment still elevated, we committed to continue purchasing assets at least at the current pace until we had made substantial further progress toward our goals. In most situations, those goals are complementary. That is, high unemployment usually coincides with subdued inflationary pressures. Therefore, at the time, we did not foresee those goals coming into conflict.”

At the same time, the policymaking consensus was that the FOMC knew how to lower inflation but how to raise it was much more uncertain. That view came out of the recovery from the Great Recession, which experienced below 2 percent inflation, a significant interval during which the funds rate was at the zero lower bound, and three quantitative easing (QE) programs that increased significantly the size of the FOMC’s portfolio. As reported by economists Michael Kiley and John Roberts, a common presumption after the recovery was that the funds rate would regularly have to be lowered to near zero.

Odyssean forward guidance, or a commitment for the funds rate to remain low despite conditions that would normally imply raising it, makes monetary policy expansionary even when the FOMC is unable (or unwilling) to lower the funds rate below zero. There are two keys for the FOMC in tying itself to the mast of an expansionary monetary policy. One is QE, which has to be phased out (tapered) before the FOMC considers raising the funds rate off the zero lower bound. The second is renunciation of the Volcker-Greenspan policy of preemption—that is, raising the funds rate before the appearance of inflation to preserve price stability. The purpose of Odyssean forward guidance is to forestall a rise in bond rates before the FOMC has achieved its goal of maximum employment. This purpose is informed by the May 2013 “taper tantrum,” in which bond rates rose when Chair Ben Bernanke raised the possibility of reducing and eventually eliminating the FOMC’s asset purchases. Markets interpreted the possibility of tapering as implying that the FOMC intended to raise the funds rate off the zero lower bound sooner than expected.

The termination of preemption was marked by the policy of flexible average inflation targeting (FAIT) in August 2020. The purpose of FAIT is to raise inflation above target (2 percent in this case) for a period sufficient to make up for earlier shortfalls of inflation from the target. With the announcement of FAIT, the FOMC signaled to markets that either a predicted or moderate increase in inflation would not prompt the FOMC to raise the funds rate without a substantial restoration of the prepandemic low unemployment rate. Abandoning preemption ostensibly allows the FOMC to discover the NAIRU by avoiding premature increases in the funds rate, such as the ones that started with the December 2015 FOMC meeting. (Earlier in the mid-1990s, economist Joseph Stiglitz, who was head of the Council of Economic Advisers in 1996, recommended just such a policy.

As of fall 2021, the FOMC had made up for the shortfalls. However, even amid the announcement of tapering at the November 2021 FOMC meeting, the FOMC remained locked into an expansionary monetary policy; that is, the size of the Fed’s asset portfolio will continue to expand (albeit at a decreasing rate) through summer 2022 while the funds rate remains at zero.

A Radical Change in Monetary Policy Creates Uncertainty over Its Success

The highly stimulative character of the Powell policy and the sharp break of that policy from existing monetary policy creates uncertainty over the long-run maintenance of 2 percent inflation. The discussion in this section highlights areas of uncertainty.

The Powell policy, which is organized around Phillips curve tradeoffs, is a radical departure from the Volcker-Greenspan policy, which allowed the price system unfettered control over the determination of real variables such as the unemployment rate. With the old policy, making the market’s expectation of inflation independent of the behavior of the economy at a value consistent with price stability became a prerequisite for reestablishment of the credibility for price stability lost in the prior stop-go era. That is, the FOMC did not want the expectation of inflation to rise if actual inflation rose or the economy recovered strongly from recession. The actual average of core personal consumption expenditure (PCE) inflation between 1997 and 2020 of about 1.75 percent reflected an expectation of inflation near price stability. Credibility then required abandonment of pursuit of unemployment as a target separate and independent of the goal of price stability. That is, it required abandonment of any attempt to exploit Phillips curve tradeoffs. The unemployment rate became an indicator useful for inferring whether the economy was growing unsustainably fast or slow. Achievement of maximum employment was considered a byproduct of a healthy economy rather than an independent target.

The hallmark of policy in the Volcker-Greenspan era became preemptive increases in the funds rate on the basis of evidence of overheating in labor markets. Those increases messaged to markets that the FOMC would preserve price stability by abandoning the earlier practice of discretionarily trading off between the independent goals of low unemployment and inflation. As made evident by the term “the Great Moderation,” rather than raising unemployment, the new procedures allowed the price system to work unhindered by causing the real interest rate to track its natural rate counterpart determined by the real business cycle core of the economy. The practice of preemptive increases in the funds rate developed in the 1950s in the early years of the William McChesney Martin FOMC. The Great Inflation started with the abandonment of such increases in 1967 and 1968, when Martin held off in return for an income tax surcharge to eliminate the deficit. Martin used the punchbowl analogy. Martin said, “The Federal Reserve, as one writer put it, after the recent increase in the discount rate, is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up.”

Another concern is that the FOMC has underestimated the stimulative power of monetary policy because of the lags involved. Expansionary monetary policy works through two channels. One is a portfolio balance effect produced by QE. QE increases the bank deposits of the public, and the public’s asset portfolio then becomes more liquid. To make the public willing to hold a more liquid asset portfolio, the price of illiquid assets must rise (their yield, explicit or implicit, must decline). Consistent with an expansionary monetary policy, in 2020 and 2021, the prices of equities, houses, commodities, and consumer durables rose. For example, on an annualized basis, the S&P Case-Shiller National Home Price index rose by 15.3 percent from February 2020 to September 2021. The price index for consumer durables declined at an average annualized rate of 0.9 percent from January 1996 through January 2020. However, from January 2020 through November 2021 it rose at an annualized rate of 10.1 percent. Of course, the price adjustment (the rise in the ratio of the prices of illiquid assets to their income streams) is a temporary equilibrium because this effect, also known as Tobin’s Q, raises expenditure.

A second channel works via reductions in the real interest rate redistributing aggregate demand toward the present. Thus, households save less and spend more. With their emphasis on a portfolio balance effect, monetarists criticized Keynesians for their exclusive focus on how a liquidity trap (or the zero lower bound) limits the ability of the central bank to lower bond rates through money creation. Krugman has revived the Keynesian view. He writes, “Interest rates can indeed hit the ‘zero lower bound’ in the 21st century; in fact, that has been the norm since 2007: This in turn means that while everyone is talking about inflation risks right now, the Fed is also concerned about the risks of overreacting to inflation. If it raises interest rates and that pushes the economy into a recession, it might not be able to cut rates enough to get us out again.”

The FOMC never talks in terms of the real rate of interest. More generally, FOMC communication never characterizes monetary policy in terms of the interaction of its policy instruments (the funds rate and QE) with the operation of the price system. For example, on November 23, 2021, the five-year Treasury bond yield was 1.3 percent. If one calculates breakevens as the difference between yields on nominal Treasury securities and on real Treasury Inflation-Protected Security yields, then expected inflation five years ahead on the same date was 3 percent. Correspondingly, the real risk-free interest rate was −1.7 percent. Moreover, expected inflation was rising. In January 2020, before the pandemic, the comparable figure for expected inflation averaged about 1.6 percent. At a time when labor markets and the economy are overheating, real interest rates are declining, making monetary policy more expansionary.

The two channels of the transmission of monetary policy outlined earlier are complementary. Reducing real short-term interest rates below the natural rate of interest stimulates money creation, which sets off the portfolio balance effect. Continued high rates of money creation testify to the stimulative character of monetary policy. M2 year-over-year growth decelerated from 27.1 percent in February 2021 to 13.0 percent in October 2021. Nevertheless, even the latter figure remains high and is basically the same as the two peak M2 growth rates reached in the 1970s. The question arises of whether the purchasing power represented by the resulting monetary overhang will be eliminated through inflation. Alternatively, the FOMC could pursue a reduction in the nominal quantity of M2, which would require some combination of sales of securities from the FOMC’s asset portfolio and an increase in interest rates sufficient to induce the public to repay debt to banks. Both actions reduce bank deposits.

There is evidence that by holding down the short end of the yield curve by keeping the funds rate at the zero lower bound while the yield curve rises, the FOMC is stimulating money creation. Economist Zoltan Pozsar writes, “Since the beginning of the fourth quarter—basically since the backup in yields—large banks have been on an unprecedented buying spree. Over a six-week period ending October 20th, large banks bought close to $120 billion of Treasuries. $120 billion sounds like a lot, but implies a lot of dry powder.” Large banks are arbitraging the rise in the yield curve.

Is 2021 Inflation Transitory?

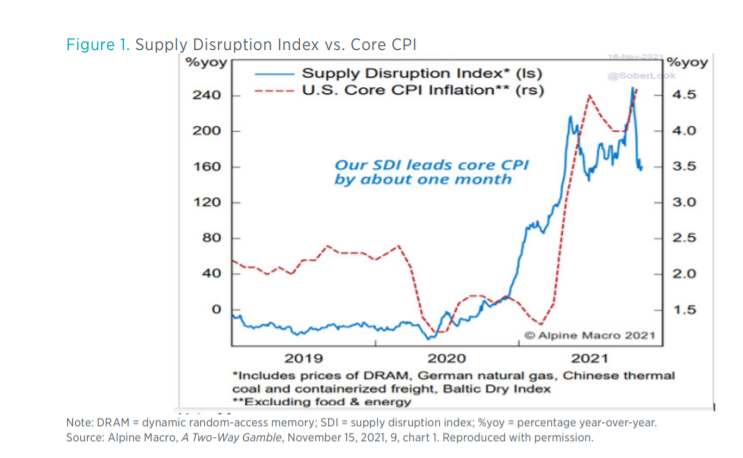

For the FOMC, the assumed significant amount of slack in the economy implies that the high inflation in 2021 is of the cost-push variety that raises the level of the Phillips curve. In the minutes for the November 2–3 FOMC meeting, the board staff forecast of PCE inflation is 2.0 percent, 1.9 percent, and 2.0 percent in 2022, 2023, and 2024, respectively. The relationship between relative prices and the price level is illustrated in figure 1, which relates inflation to supply disruptions. As supply disruptions diminish, the presumption is that so will inflation. However, to be complete, the FOMC’s forecast must explain how monetary policy determines aggregate nominal demand.

One can interpret figure 1 as evidence of an excessive level of aggregate nominal demand created by expansionary monetary policy interacting with an economy suffering from pandemic-created supply constraints. Initially in the pandemic, high inflation originated in the supply-constrained sectors of the economy. As those supply constraints dissipate, however, the excessive growth in aggregate nominal demand will remain, and inflation will remain well above the FOMC’s 2 percent inflation target.

The latter view reflects a monetary theory of inflation. Price stability (achievement of a low inflation target) requires procedures that ensure monetary control. Monetary control requires prevention of destabilizing monetary expansions and contractions. For that control to be achieved, the FOMC must follow a monetary policy that allows the price system to work through a reaction function that causes the real rate of interest to track the natural rate of interest. Evidence from the Volcker-Greenspan era, which produced the Great Moderation, indicates that preemptive increases in the funds rate in response to evidence of overheating in labor markets provide such a reaction function.

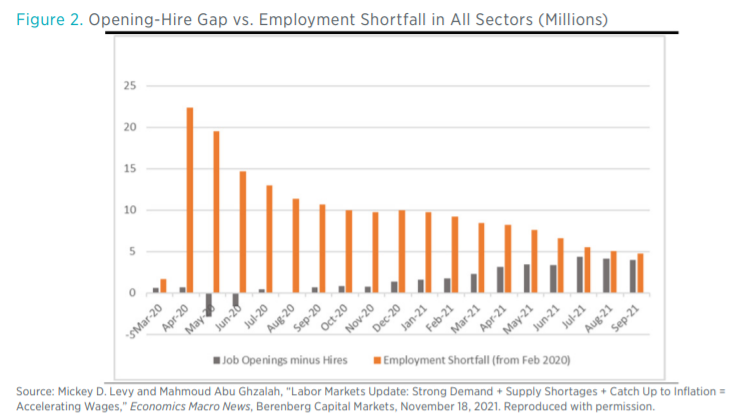

Figure 2 provides evidence of overheating in labor markets. It plots what the source authors call the “opening-hire gap” and the “employment shortfall.” The former is the difference between job openings and hires calculated using results from the Job Openings and Labor Turnover Survey. The latter is the difference between current payrolls and prepandemic peak payrolls calculated using results from the Current Employment Statistics survey of the Bureau of Labor Statistics. The opening-hire gap is a measure of labor market tightness. Figure 2 thus shows that labor markets tightened significantly around April 2021. The figure suggests that, despite labor market tightness since July 2021, firms have struggled to restore prepandemic employment.

In fall 2021, the forward guidance provided to markets by the FOMC about tapering and liftoff rested on a forecast that the 2021 and early-2022 inflation would be transitory. Consequently, as of fall 2021, the FOMC felt no need to end immediately a highly stimulative monetary policy aimed at restoring a prepandemic low, inclusive level of unemployment. (Ending stimulus would require selling assets rather than tapering asset purchases and would require raising the funds rate more than increases in expected inflation.)

The assumption that high 2021 inflation is transitory rests on the assumption that significant slack exists in the economy. Tightness in the labor market challenges that assumption. The upward shift in the Beveridge curve, which plots unemployment (U-3) on the horizontal axis against job openings on the vertical axis, suggests that little slack exists in the labor market for a given unemployment rate relative to the prepandemic baseline. That is, the natural rate of unemployment has risen, and the 4.2 percent unemployment rate in November 2021 could have even been below the natural rate of unemployment. The year-over-year increase of 2.6 percent in October 2021 in the Federal Reserve Bank of Dallas’s trimmed-mean measure, which eliminates outsized changes in inflation for specific categories, does not indicate slack in the economy.

Nominal GDP as an Intermediate Target to Ensure Achievement of the Inflation Target

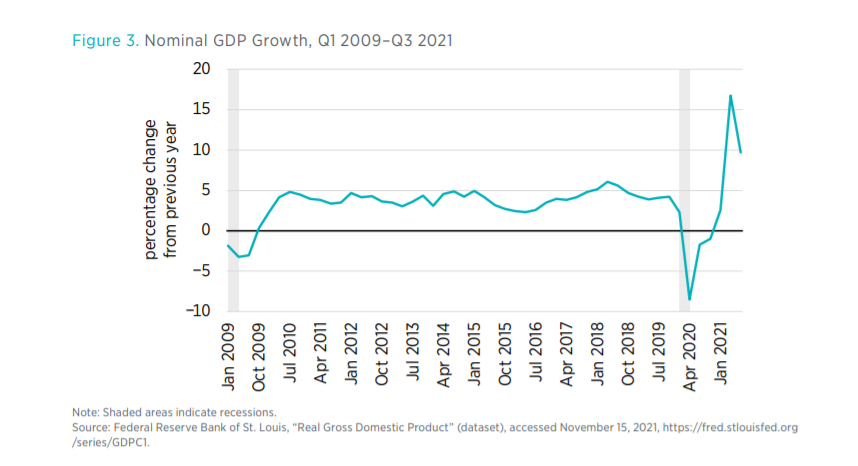

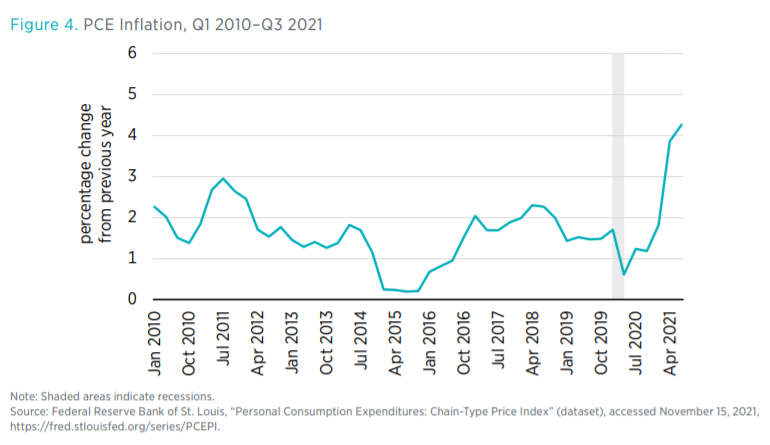

In fall 2021, the FOMC’s willingness to continue with an expansionary monetary policy depended upon the forecast that contemporaneously high inflation was transitory. However, the FOMC’s prior quarterly SEP forecasts of inflation regularly underestimated inflation. The FOMC was also ambiguous about how it would balance its competing inclusive unemployment and low inflation targets if inflation were not transitory but instead were to remain at a level above the long-term 2 percent target. If the FOMC is committed to a longer-term goal of 2 percent inflation, it can make public estimates of the rate of growth of nominal GDP consistent with that target and then commit to a whatever-it-takes policy to achieve those estimates. Figure 3, which displays four-quarter percentage changes in nominal GDP, illustrates the challenge confronting the FOMC. Figure 4 displays the associated behavior of four-quarter percentage changes in the PCE chain-type price index.

Over the recovery following the Great Recession (Q1 2010 to Q1 2020), four-quarter percentage changes in nominal GDP averaged 3.9 percent. Over this interval, PCE inflation averaged 1.6 percent, just below the FOMC’s 2.0 percent target. Presumably, restoration of 2.0 percent inflation, given the supply constraints facing the economy owing to the disruption caused by the COVID-19 pandemic, will require that nominal GDP growth return to roughly the 3.9 percent that characterized the recovery. The 9.6 percent figure for nominal GDP growth in Q3 2021 obviously is well in excess. (The Q3 2021 figure for PCE inflation is 4.3 percent.)

After it begins trying to restore 2 percent inflation, intermediate targets for nominal GDP growth will presumably be relatively high, given the FOMC’s two basic assumptions that there exists significant slack in the economy and that the inflation in 2021 is transitory and should be accommodated to avoid missing the unemployment target. However, the announced targets will have to decline as slack and inflation decline.

Targets for nominal GDP also increase transparency. Sumner advocates that the FOMC target nominal GDP and adjust its instruments (the funds rate or reserves) in response to market forecasts of nominal GDP differing from its target. If it were to follow the proposal in this brief, the staff of the Board of Governors of the Federal Reserve would make public its methodology for forecasting the nominal GDP targets it assumes would achieve the inflation target. A futures market in nominal GDP futures would then serve as a jury on the credibility of the staff’s forecasts. The use of forecasts for the nominal GDP target is necessary because nominal GDP figures become available only at the end of the month following a given quarter. The preliminary figures are calculated using incomplete data. Figures on inventories and the trade deficit only become available a month later. Moreover, subsequent data releases can be heavily revised. The staff’s forecasts would thus generate useful debate among economists and financial analysts.

Conclusion

Not since the 1970s has the FOMC pursued a purposefully expansionary monetary policy. Like the 1970s, the nation is now socially fractured, and an inclusive, low rate of unemployment is desirable to aid social cohesion. The goal of expansionary policy is to achieve that low unemployment target with only a modest overshoot of inflation followed by a return to 2 percent inflation. Given the high rate of inflation in fall 2021, there is a danger that the inflationary expectations of the public could rise undesirably. Moreover, the discretion entailed in juggling dual targets for unemployment and inflation reduces the long-term discipline required to maintain price stability. To mitigate these problems, the FOMC could articulate longer-term intermediate targets for nominal GDP growth estimated to be consistent with price stability. It could then articulate the rule required to achieve those intermediate targets.