- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Reforming the Fed’s Toolkit and Quantitative Easing Practices: A Plan to Achieve Level Targeting

The COVID-19 pandemic is a major shock to the American economy. Indeed, we are already seeing signs that the United States will experience a severe recession. Market indicators suggest that a weak economy may persist well beyond the actual pandemic, especially if policy responses are poorly designed.

The pandemic has also pushed short-term interest rates down close to zero. This makes it difficult for the Federal Reserve (Fed) to conduct monetary policy by adjusting its traditional primary instrument, the federal funds rate. On March 16, the Fed cut the federal funds rate target range down to 0 to 0.25 percent, the same range it set during the Great Recession, leaving little room for further cuts.

Contrary to the view of some economists, however, this does not mean the Fed is out of “ammunition” with which to help the economy recover from recession or achieve 2 percent inflation. This policy brief provides a plan for how the Fed can produce effective monetary policy even when interest rates are at zero. Specifically, the Fed should take the following steps:

- Explicitly announce a price level target path (or preferably a nominal GDP level target).

- Reduce payment of interest on excess bank reserves to zero (or preferably even below zero to be comparable with the yields on short-term securities).

- Ask Congress for the permission to temporarily buy a wider range of assets, including corporate bonds and stocks, but only when the federal funds rate is below 0.25 percent.

- Buy as many assets as necessary to raise market inflation forecasts up to the price level target path.

By taking these steps, the Fed will improve the labor market and make it easier for individuals and firms to repay loans. To be sure, no amount of stimulus can prevent a sharp rise in unemployment during the “lockdown period.” Without monetary stimulus, however, there is a real danger that the recession could drag on long after the acute phase of the medical crisis is over. Announcing these changes would calm market concerns about prolonged recession, reducing the likelihood that policymakers would need to resort to other measures such as fiscal stimulus or bailouts, which are much more costly and much less effective than monetary stimulus.

Why Does the Fed Need Additional Tools?

The Fed currently has a congressional mandate to achieve price stability and high employment. For various reasons, the Fed has decided that an inflation target of 2 percent (measured using the personal consumption expenditures [PCE] price index) and an unemployment rate close to the natural rate of unemployment best address this so-called dual mandate.

If inflation is below 2 percent, the Fed may need to adopt a more expansionary monetary policy in order to boost aggregate spending. This monetary stimulus should lead to higher prices and higher employment. Many observers worry, however, that once interest rates fall to zero, the Fed is out of ammunition and will be unable to further stimulate spending. This pessimism is based on the widely held belief that “monetary policy” is equivalent to changes in interest rates.

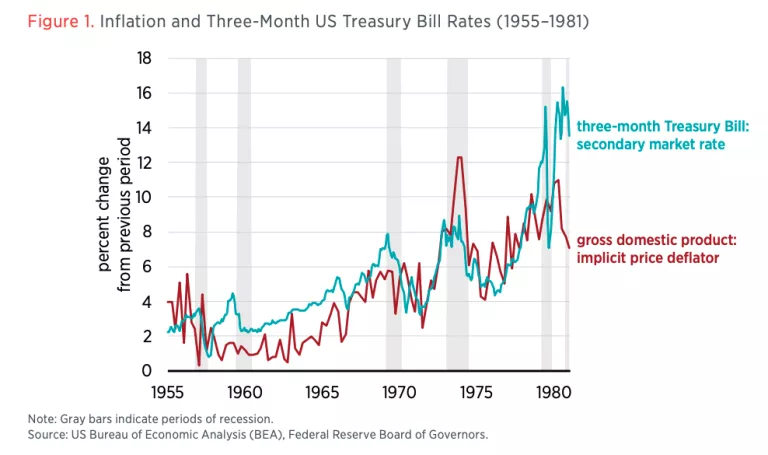

A number of prominent economists including Milton Friedman, Ben Bernanke, and Frederic Mishkin have argued that interest rates do not represent the stance of monetary policy. Indeed, nominal interest rates are often at their highest when monetary policy is highly expansionary and inflation is also very high. (Nominal interest rates are actual market interest rates, not adjusted for inflation.) Figure 1 shows that an expansionary monetary policy that raised inflation during the 1960s and 1970s also led to higher interest rates. Thus inability to cut interest rates below zero does not mean that the Fed is unable to affect spending in the economy, as low interest rates do not equate to “easy money.”

What the Fed Can Do Right Now

When setting monetary policy, the Fed can adjust the federal funds rate by buying or selling Treasury securities and other safe assets. When buying securities, the Fed injects new money into the economy in payment for the assets being purchased. This often lowers the federal funds rate in the short run, although the long-run effect may be the exact opposite if inflation increases. Monetary injections also tend to increase economic growth in the short run, and this increase eventually causes prices and nominal interest rates to rise.

In noncrisis times, the Fed adjusts the federal funds rate in order to achieve the inflation target it desires. Since 2012, the Fed has explicitly stated that its inflation target is 2 percent, though inflation has often fallen somewhat short of that target. Nonetheless, the Fed is widely viewed as having sufficient ammunition when interest rates are positive.

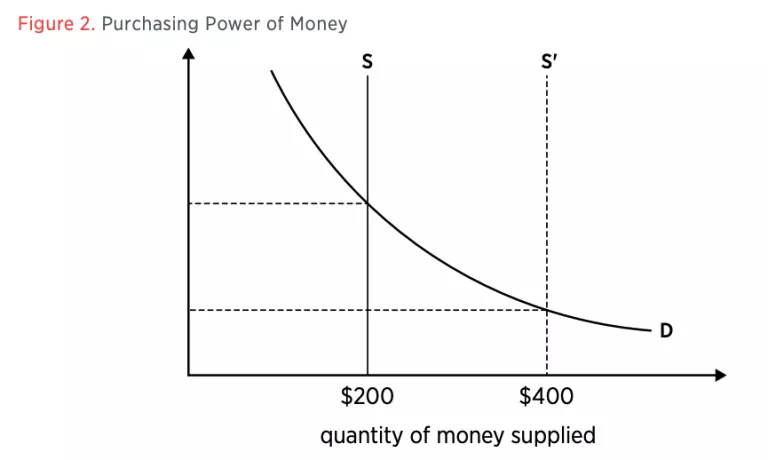

When the federal funds rate fell close to zero during the Great Recession and its aftermath, the Fed resorted to buying large quantities of longer-term US Treasury and mortgage-backed securities. These purchases are frequently referred to as quantitative easing or QE. The Fed will likely need to engage in additional rounds of QE during the current crisis and its aftermath. These purchases increase the money supply, as shown in figure 2. If purchased in sufficient quantity, they will raise inflation up to the 2 percent target.

In addition to altering the supply of money, the Fed can also impact the price level through policies that affect the demand for money. Decreases in the demand for money tend to push prices higher. When inflation falls short of the 2 percent target, the Fed has three methods of reducing money demand to boost inflation: a lower reserve requirement, a reduction in the interest rate on bank reserves, and a switch from inflation targeting to price level targeting.

In October 2008, the Fed began paying interest on excess bank reserves held at Federal Reserve Banks in order to exercise greater control over the federal funds rate. By paying a bank to hold reserves, the Fed gave the bank less incentive to reinvest those funds. Consequently, when the Fed injected new money through its QE program and paid positive interest on those bank reserves, it encouraged banks to hold on to the reserves rather than reinvest them. If, on the other hand, the Fed were to lower the rate at which it pays banks to hold reserves, banks would have more incentive to reinvest the funds into other assets.

In response to the COVID-19 crisis, the Fed has already cut the interest rate on reserves to 0.10 percent, but it should cut the rate to zero before engaging in more QE. This will improve the likelihood that any new QE will be more effective than previous rounds, when interest was being paid on bank reserves. On the same day, the Fed also eliminated reserve requirements, which will also help to reduce the demand for bank reserves. Both actions are expansionary, though neither action by itself will be sufficient.

Moreover, since the interest rates for short-term securities, including one-month and three-month US Treasury yields, have recently become negative, it would actually be sensible to pay a negative rate on reserves. By paying an interest on reserve rate lower than other short-term rates, the Fed would encourage banks to invest funds into those other assets rather than encourage them to keep the funds as reserves.

Level Targeting

A QE program is much more effective at boosting inflation if the bond purchases are linked to an explicit level target. Under level targeting, the central bank no longer lets “bygones be bygones.” If inflation falls short or overshoots the 2 percent target path, the Fed commits to make up any discrepancies over the next few years.

This is currently not the approach taken by the Fed, as it has fairly consistently undershot its 2 percent inflation target without making any commitment to catch up to the previous trend line. This is one reason why the Fed’s previous QE programs did not produce dramatic growth in aggregate spending. In contrast, if the Fed wants 2 percent annual inflation in the long run and achieved only 0 percent inflation in a given year, under level targeting it might aim to achieve 3 percent inflation over the following two years in order to maintain 2 percent inflation on average.

Since inflation often tends to fall below central bank targets during a recession, level targeting would lead to expectations of higher inflation during the recovery. Investors would thus be inclined to spend more today, pushing prices back up to the target path. This approach is called price-level targeting because the price level, not inflation, is the variable actually being targeted. Numerous economists, including Ben Bernanke, have argued that this policy is especially useful when interest rates are at zero.

A nominal gross domestic product (NGDP) level target along a 4 percent growth path would be an even more effective approach than inflation or price-level targeting, especially during adverse supply shocks. NGDP growth is made up of economic growth (i.e., real GDP growth) plus inflation, and it is equivalent to the growth rate for total spending in the economy. If a recession were to cause NGDP growth to fall below trend, the Fed would then commit to higher NGDP growth to return back to the 4 percent growth target path. This sort of policy would be more likely to create the sort of strong “V-shaped” recovery experienced after the deep 1982 recession, when output grew at nearly 8 percent for 18 months, rather than the “L-shaped” recovery after 2009, when output grew at roughly 2.5 percent.

During a recession where total spending contracts, NGDP level targeting would have broadly similar effects as price-level targeting. Under both regimes, markets would expect higher inflation and economic growth in the future. This would also boost the demand for credit, putting upward pressure on market interest rates. Once market interest rates rise above zero, the Fed can move away from QE and revert back to using the traditional federal funds rate target as its primary tool.

Additional Tools from Congress

In order for an NGDP or price-level targeting regime to work, the Fed must convince the public, and more specifically the financial markets, that it can credibly hit its target. Some observers question whether the Fed currently has the necessary tools to be credible. The Fed already has the authority to buy US Treasuries and mortgage-backed securities, but, unlike other central banks such as the European Central Bank and the Bank of Japan, its ability to buy riskier assets such as corporate debt or stocks is limited by the Federal Reserve Act.

Since there is currently more than $30 trillion in US Treasuries and mortgage-backed securities (MBSs) in circulation, it is likely that the Fed already has adequate resources to hit its 2 percent inflation target. Nevertheless, it should seek authority from Congress to purchase these riskier assets during emergencies like the current pandemic in case there are not enough conventional assets available to provide the necessary increase in the money supply. Congress should also instruct the Fed to achieve its congressional mandate even if doing so involves some financial risk, since the cost of a (highly unlikely) Fed bailout is tiny compared to the cost of an economic recession. This sort of clear mandate would assuage the concern that purchases of riskier bonds could cause the Fed losses.

Any additional Fed powers should come with clear restrictions. Purchases of riskier assets must be temporary and only used insofar as needed to achieve the Fed’s price level target. Riskier assets should be purchased only when short-term interest rates fall below 0.25 percent, and the assets should be sold off before rates rise above 0.25 percent. Purchases should not be made with the goal of propping up either the bond or stock markets. The Fed could minimize the extent to which it interferes with stock or bond prices by buying a “basket” of assets representative of what a typical investor might purchase, perhaps an index fund. Finally, such purchases would only take place in the unlikely event that the Fed had exhausted its ability to purchase US Treasuries and MBSs.

Some may be uncomfortable with giving the Fed the ability to pursue extremely large QE programs. Under level targeting, however, any overshoots of inflation targets must be offset in future years, keeping the average rate of inflation close to 2 percent. Although it may seem counterintuitive, giving the Fed unlimited ability to increase the money supply would make it less likely that the Fed would need to resort to purchases of riskier assets, since it would remove any doubts about its ability to achieve 2 percent inflation. As with a switch from inflation targeting to a level targeting regime, an expanded ability during a recession to buy assets would boost the public’s expectation of future growth in the money supply, which would put upward pressure on prices and interest rates. Once interest rates rise above zero, the Fed could once again resort to its traditional use of the federal funds rate.

Implications for Other Policy Areas

The adoption of level targeting would reduce the need for federal intervention in other areas of economic policy. Under level targeting, the case for fiscal stimulus (deficit spending through increased spending or lower taxes) is weakened because monetary policy can accomplish the same goals as fiscal stimulus at a much lower cost.

Targeted fiscal relief may be warranted to help those adversely affected by the pandemic, especially those who have lost their jobs or income, but two considerations make broad fiscal stimulus less effective and more costly than monetary policy in promoting economic recovery. First, unlike fiscal stimulus, expansionary monetary policy does not add to the federal deficit and increase the burden on future taxpayers. Recall that higher taxes tend to discourage capital formation, and hence fiscal stimulus is more likely than monetary stimulus to reduce future growth. Second, the Fed has generally been much better at well-timed countercyclical policy (expansionary during recessions and contractionary during expansions) than the US government. For example, in 2013, when unemployment was at a relatively high 8 percent, Congress sharply reduced the federal deficit. By contrast, the Fed was conducting QE during this time. More recently, between 2016 and 2019, Congress dramatically expanded the deficit at a time when unemployment was falling to historic lows, while the Fed was gradually raising the federal funds rate at approximately the same time.

This history suggests that the Fed is better able to provide countercyclical policy than Congress, which often tends to base decisions more on short-term political considerations than on objective macroeconomic conditions. While fiscal policy measures from Congress such as infrastructure projects can be justified on cost-benefit grounds, such measures should not be justified on the grounds that they will help boost aggregate demand and inflation. Leave demand management to the Fed.

Companies of all sizes are adversely affected by the current pandemic, and many companies (particularly smaller ones) are in danger of facing bankruptcy. We are already witnessing many struggling industries (including but not limited to the airline and hotel industries) appealing to legislative policymakers for relief in the form of either loans or subsidies.

While it may be appropriate to provide government loans to support companies during government-mandated shutdowns, in the longer run the most effective way of aiding firms is to provide faster growth in aggregate demand through monetary stimulus. As national income rises, banks will know that firms are earning more revenue and will thus be better able to service debts.

If government loans are made on a case-by-case basis, there is a danger that politically well-connected firms with powerful lobbying capabilities will be bailed out rather than less politically well-connected firms, giving well-connected firms an unfair advantage over their competitors. Moreover, bailouts amplify the problem of moral hazard, the tendency of certain firms to take excessive risks because they recognize they will be bailed out through either subsidized loans or taxpayer money.

With a level targeting regime in place, there is far less danger that the failure of major firms would tip the economy into a recession. This is particularly true of NGDP level targeting, under which the collapse of even a large firm would not lead to a fall in overall spending in the economy. Stable growth in NGDP is the best way to insure a stable labor market and a stable environment in which to repay nominal debts.

Conclusion

The two most important reforms to improve monetary policy would be the adoption of level targeting of prices (or, better yet, nominal GDP) and a commitment to buy whatever assets are needed to achieve that level target. Congress should remove any institutional constraints on the Fed’s ability to purchase sufficient assets during an emergency.

Even after the current pandemic ends, the economy may experience a prolonged period of weakness. As an analogy, even after the acute banking crisis of 2008 was addressed through Troubled Asset Relief Programs (TARPs), high unemployment lingered for many years. Sound monetary policy reduces the need to resort to other interventionist policies, and can also lead to a faster economic recovery once the health crisis eases. Sound monetary policy can also reduce the burden on debtors by assuring that the flow of total income into the economy continues to grow close to trend.

Monetary policy is not a panacea for the direct impact of the virus, which will cause unavoidable and significant disruption. Rather, it is a way of insuring that the secondary effects of the disruption do not persist for an unnecessary period of time. To use a medical analogy, the goal is to prevent a viral infection like a cold from turning into pneumonia. Consider level targeting to be an antibiotic for the economy.