Index funds and passively managed exchange-traded funds (ETFs) (collectively “index funds”) have quietly taken control of corporate governance. Growing from 2 percent of total stock market value in 2000 to 17 percent as of 2018, the rise of index funds has been meteoric. As index funds have grown, they have gone from bit players in the corporate governance world to the de facto arbiters of corporate law controversies.

Index funds’ influence over corporate governance derives from their right to vote in corporate elections. Although the people who invest in index funds are the ultimate owners of the economic interest in the underlying shares, the index fund is viewed as the legal owner of the shares, while the ultimate investors own only shares in the mutual fund (or ETF) itself. In this way, index funds hold the legal right to vote massive numbers of their investors’ shares in corporate elections.

Augmenting the sheer size of index funds’ holdings is the fact that the index fund industry is heavily concentrated in the hands of just a few fund families. The “Big Three”—Vanguard, BlackRock, and State Street—control a supermajority of index funds assets. Together, they constitute the largest investor in nearly 90 percent of the S&P 500, giving the trio an unprecedented hold on corporate America. This concentration of power will likely increase going forward. Passively managed funds are expected to overtake actively managed funds in 2020, and a supermajority of those passive funds will likely go to the Big Three.

The situation is such that even the inventor of the index fund, the late John Bogle, has sounded the alarm:

"If historical trends continue, a handful of giant institutional investors will one day hold voting control of virtually every large U.S. corporation. Public policy cannot ignore this growing dominance, and [must] consider its impact on the financial markets, corporate governance, and regulation. These will be major issues in the coming era.”

In just a few decades, corporate governance has gone from being the province of concentrated investors such as hedge funds and activist investors to being the province of index funds. What does this mean for the future of public companies in the United States?

Positive Potential of Index Funds

The growth of index funds theoretically could serve as a victory for the common investor. Because index funds cannot sell the underlying stocks making up the index in which they invest, index funds are uniquely positioned to take a long-term view of corporate performance. The long time horizon on which index funds operate mirrors the way that “Main Street,” middle-class Americans invest—on a long-term, often multidecadal basis as a means of saving for retirement or their children’s education. Main Street investors (that is, the majority of investors) do not care about day-to-day fluctuations in the stock market or even whether a given company might have, say, met its earnings targets for a certain quarter. These investors care about what their nest egg will look like in 20, 30, or 40 years. In this way, the rise of index funds as a corporate governance powerhouse could have the potential to promote the interests and the portfolios of ordinary Americans.

Reciprocally, the rise of index funds has the potential to mitigate perceived corporate “short-termism” (i.e., an excessive focus on short-term profitability metrics at the expense of long-term investment and growth), which has become a source of increasing concern for academics and policymakers alike. By serving as a counterweight to hedge funds, day traders, and activist investors, the rise of index funds has the potential to promote the long-term health of the American economy as a whole.

Problems with Index Fund Power in Practice

However, the potential of index funds to promote sustainable growth and the interests of ordinary investors depends heavily on how index funds wield their voting power. Currently, voting at the index fund giants is subject to only one major constraint: index funds must vote “in a manner consistent with the best interests” of their investors. However, the best-interest standard is so vague as to allow funds to vote as they see fit.

Vividly illustrating this point, index funds routinely vote in opposite ways of each other on hot-button issues. For instance, if voting for climate-related shareholder proposals (such as proposals to adopt and report on emissions targets for greenhouse gases and other substances) is just as valid as voting against such proposals, one may rightly question how much the best-interest standard constrains fund voting decisions. Yet this is exactly what one sees (see figure 1)—among the Big Three, Vanguard and Blackrock supported climate-related shareholder resolutions at rates (12 percent and 10 percent, respectively) roughly one-third that of State Street (34 percent). Other fund families had higher rates still, such as Eaton Vance (85 percent) and AllianceBernstein (88 percent).

Which fund got it right? Assuming that “right” means accurately reflecting the interests of investors, the surprising answer is that no one has any idea, including the funds themselves. The law currently does not require funds to attempt any sort of investigation into what their investors might actually want and instead permits funds extraordinary latitude in divining their investors’ perceived best interests.

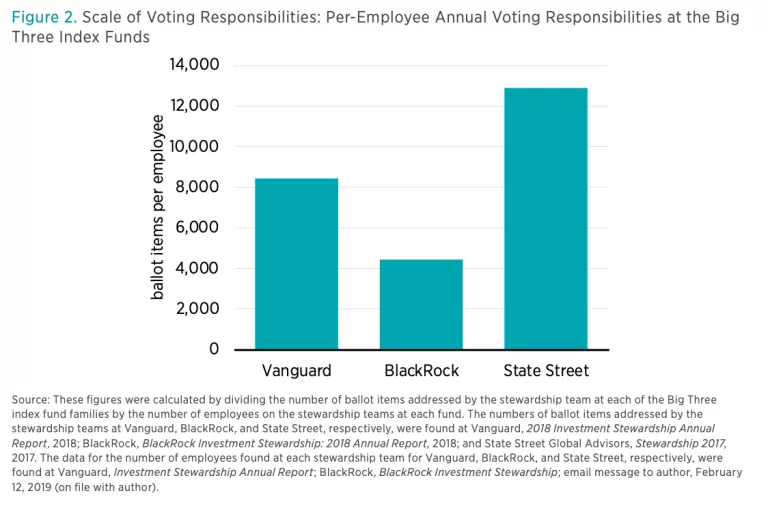

One risk, of course, is that with limited or no data showing actual investor preferences on a host of issues, a handful of individuals (the “investment stewardship team,” in industry parlance) will be consciously or unconsciously biased toward their own preferences rather than those of their investors. Alternatively, such teams could be influenced by pressure from special-interest groups that, while more organized or more vocal than the majority, may not represent the interests of the majority. Finally, some teams may make suboptimal decisions simply because they are overwhelmed by the sheer number of votes they must cast. At the Big Three fund families, investment stewardship teams ranging in size from 12 to 36 share responsibility for determining how to vote on more than 150,000 issues each year, meaning that the potential for individualized attention to the interests of their individual investors is extremely limited (see figure 2).

To simplify the burden of researching and voting on so many issues, index fund stewardship teams craft a set of generic voting guidelines, which they follow closely in individual contests. Technological aids and the support of the two dominant proxy adviser firms, Institutional Shareholder Services (ISS) and Glass Lewis, enable stewardship teams to automate voting decisions according to these guidelines.

On many issues, the Big Three act in concert. The trio’s voting guidelines uniformly support director independence, seek to tie executive compensation to long-term performance, oppose antitakeover provisions, and generally oppose major changes to corporate structure. The similarity in voting behavior between the Big Three only adds to their power over corporate America, given the substantial number of shares they control as a triad. However, despite the similarity in their voting guidelines, there is no true consensus on numerous corporate governance issues and even less of a consensus on environmental and social issues, and many people (and likely many index fund investors) would disagree with the approach these funds have taken in their voting guidelines. To the extent that such votes are cast in concert, index fund investors have little ability to “vote with their feet” and seek out an index fund that votes in a manner more similar to their preferences. Even where heterogeneity exists, many investors are locked into a handful of funds from a single fund family, effectively preventing them from actively selecting a fund with desirable voting habits.

Another problematic feature of index funds’ approach to voting is that index funds vote nearly all shares under their control as a bloc. Ideally, funds would vote proportionately. This would give additional voice to investors in the minority, who otherwise (if they owned the shares directly rather than through an index fund) would have their votes be counted. Not only would such a step would ensure that voting decisions were better aligned with the preferences and priorities of ultimate investors, it would also mitigate the concentrated power of index funds by preventing a handful of fund managers from wielding the voting rights of millions of investors as a unified bloc.

Suggested Reforms

In short, very few people at very few fund families currently control a very large number of shares, subject to very limited constraints on how those shares are voted and with very limited knowledge about the voting preferences of the people who actually paid for the shares. To remedy the status quo, I propose three separate reforms.

The first is implementing pass-through voting instructions. This proposal has two basic components: First, it would allow voting rights to “pass through” the index fund intermediary to the ultimate investors (that is, the person or persons with an actual economic interest in the stock). Second, it would allow investors to issue general guidelines as to how their shares should be voted, just as index fund stewardship teams now do. The guidelines would be set once, when the investor opened his or her account, with the opportunity to update these guidelines annually. Stewardship teams would use the investor-generated guidelines in place of their own, voting proportionally in accordance with the actual preferences of their investors.

The second reform is giving investors the ability to delegate their voting authority to a third party. Under this approach, index fund investors could express a preference to have the votes corresponding to their ownership cast according to an entity of their choosing. The investor may choose to vote in line with the index fund provider’s recommendations, to vote according to a given proxy advisory company’s recommendations, to follow the board’s recommendations, to mimic the voting behavior of another institutional investor, to vote proportionally in line with other investors in the fund, or to abstain from voting altogether. Under this approach, index fund investors would be able to seek out an entity that best represents their preferences and values, giving them an increased say in corporate contests. Such an approach may even lead to increased competition between various entities, particularly proxy advisory firms, to better capture the actual preferences of all investors or a niche subset of investors.

The final reform is also the simplest: index funds would survey their investors to assess their preferences and vote the shares under their control in accordance with those preferences. These surveys would enable corporate stewardship teams to have more information about their investors’ timelines for investment, risk tolerance, and preferences regarding various environmental, social, and governance proposals. Such information would then be used to shape voting guidelines and ultimately ensure that the voting behaviors at the Big Three and other index funds better represented the actual preferences and interests of their investors.

Although any of these three proposals alone would represent a significant improvement over the status quo, a combination of the three proposals would be ideal. Under a combined approach, all index fund investors would have the right to issue pass-through voting instructions on, say, the 10–15 most salient environmental, social, and governance issues, and those with the highest intensity of preference would do so. Those with lower intensity of preference could either select an actor whose votes they would mirror, or they could choose to have the fund vote on their behalf. If they chose the latter, rather than guessing at their investors’ views on various environmental, social, or governance issues, funds would be required to poll their investors to inform their voting decisions. At each level, investors would have the opportunity to make their voices known.

Positive Effects of Increased Deference to Investor Preferences

Separately or in tandem, the three proposals described herein would entail a number of benefits for index fund investors and society at large. First, and most obviously, increased deference to the actual investors would increase the alignment between the way shares are voted and investors’ actual preferences. Unlike the status quo, where individual investors do not have any meaningful avenue for expressing their preferences and priorities and where index fund corporate stewardship teams are likely unaware of such preferences and priorities, these proposals would give individual investors a voice over corporate decision-making, thereby better fulfilling the promise of representing shareholder interests.

Second, by spreading power for voting decisions to the millions of index fund investors instead of a handful of corporate governance team members, these proposals would limit the power in the hands of index funds and their employees. In this way, these proposals would reduce the agency costs and potential for abuse inherent in concentrated power by decentralizing decision-making.

Third, not only would these proposals increase the number of decision makers, they would also diversify the pool of decision makers. Indeed, solicitation of input from actual investors would include the voices of a far greater swath of society, including the voices of those Main Street investors who currently have little influence on corporate governance. Such diversity would likely increase the heterogeneity of voting guidelines, voting behaviors at the index funds, or both, which could in turn spur increased competition in the index fund sector.

Fourth, these proposals would provide a mechanism for addressing the rational apathy thought to typify Main Street investors. Only 28 percent of shares held by individual investors were voted at annual meetings in 2018, at least partly because such votes must be cast on a burdensome, case-by-case basis. Although it may not make sense for Main Street investors to expend the time and effort to engage with hundreds or thousands of ballot items each year, given the small size of their holdings and their correspondingly limited ability to impact voting outcomes, it makes far more sense for them to engage in a one-time or annual analysis of key corporate governance issues. In this way, reforms to index fund voting would enable Main Street investors to be far more involved in corporate decision-making than they have been in the past.

Potential Costs of Proposed Reforms

Although there are a number of benefits to solicitation of input from ultimate investors, these proposals entail some costs. In particular, it may be more burdensome and therefore more expensive for index funds to solicit their investors’ input and then act on such information. These proposals may require index funds to hire additional employees or to contract for additional support from proxy advisers or other service providers. There may also be some initial costs, such as those entailed by modifying existing technology to support investor involvement or those required in setting up a survey to identify investors preferences.

However, given that index funds already craft voting guidelines and already automate voting decisions based upon those guidelines, the proposals set forth in this paper are unlikely to yield significant cost increases. This is particularly true when one considers the scale of the cost increases at the per-investor level and when one considers the existing infrastructure and the enormous scale of investments in index funds. Ultimately, the costs of, for example, administering a survey or adapting automated voting technology that already exists are likely to be trivial.

Implementation of Proposed Reforms

Because of the unique structure of index funds, wherein the index funds serve as the legal owners of the shares and thus have the voting rights for those shares, there are no legal impediments preventing index funds from implementing any or all of the above proposals. For example, the onerous proxy solicitation requirements set forth by Regulation 14A would very likely not apply to attempts by index funds to seek input about the preferences of their investors, since index fund investors do not possess any voting rights to be solicited. Likewise, Rule 14(a)-4(d), which limits the amount of time in which a proxy can confer voting authority, would again not apply to index fund investors given the current legal structure of index funds.

Despite the fact that index funds would face no legal hurdles in seeking input from ultimate investors, index funds have not made any serious and sustained efforts to do so. One potential obstacle comes from the fact that index fund managers, particularly corporate stewardship teams, may be reluctant to reduce their power or influence, even if such steps better served ultimate investors. Another potential obstacle is the fact that index funds compete primarily on fees, and fund managers may fear that any cost increases, however slight, would discourage investment in their particular fund. Finally, it could just be inertia, with index funds needing a push to alter the status quo.

Several regulatory steps could be taken to give index funds that push to reform their voting practices in a way that better serves the interests of ultimate investors. One simple step would be for the SEC to issue additional guidance on the “best interests” standard and require corporate stewardship teams to solicit input from ultimate investors on voting decisions. Such guidance could also require proportional voting, thus ensuring that index funds used their votes to express investors’ actual preferences rather than voting as a bloc. A related step would be for Congress to enact legislation providing that index fund directors have a fiduciary duty to solicit investor input on voting decisions and perhaps to vote shares proportionally according to the actual preferences of investors. Both avenues would transform index fund voting from the exclusive purview of index fund corporate stewardship teams to a collaborative process between investors and their representatives, a change that would simultaneously empower investors, curtail concentration of power, increase diversity and heterogeneity in voting practices, and improve the alignment between voting behavior and investor preferences.

Conclusion

This policy brief addresses the two problems that form the paradox of index fund power: while index fund families have amassed massive, largely unchecked power, their investors are largely powerless. It proposes to solve both problems by taking power from index funds, as agents, and giving it to their principals, their investors. Such a redistribution of power would vastly improve shareholder representation, serve the interests of ultimate investors, and mitigate the concentration of power in the hands of the few.