- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Strengthening the Federal Reserve’s Accountability to the US Congress

Congress has a constitutional duty to oversee the Federal Reserve, but the complexity of its monetary policy has outpaced existing oversight tools. This brief looks at approaches for restoring the balance between the Fed’s independence and accountability.

The US Constitution specifically vests Congress with the duty to regulate the value of money. In the modern era, Congress has delegated this duty to the Federal Reserve (Fed), giving the Fed a broad mandate to foster maximum employment and stable prices and granting it wide discretion in conducting monetary policy. While Congress certainly has the power to delegate this crucial duty to the Fed, the Constitution does not permit Congress to abdicate responsibility for overseeing this task. In effect, allowing the Fed to function as a “fourth branch” of government is not constitutionally permissible.

In a forthcoming article for the Vanderbilt Law Review, our analysis indicates that the current regime of congressional oversight is more properly characterized as “undersight.”1 We analyze Congress’s delegation of monetary powers to the Fed, highlight the shortcomings in the current regimen of congressional oversight, and identify options for strengthening the Fed’s public accountability while protecting its independence from political interference. The remainder of this policy brief provides a synopsis of our analysis.

Congress has exempted the Fed from almost all the mechanisms for congressional oversight of other independent agencies, including the Commodity Futures Trading Commission, the Federal Deposit Insurance Corporation, and the Securities and Exchange Commission:

- The Fed’s monetary policy reports to Congress do not provide cost-benefit analysis of its programs and do not provide any assessments of potential risks associated with its policies. The Fed is authorized to issue interest-bearing obligations that are not subject to the federal debt ceiling.

- The Fed sets its own accounting rules, in contrast to other federal entities that are subject to generally accepted accounting principles (GAAP).

The Fed’s monetary policy framework and programs are exempt from review by the Government Accountability Office (GAO), which conducts periodic performance audits of all federal offices and agencies.

The Fed’s inspector general (IG) is a Fed employee, whereas a fully independent IG is in place at other major government entities (offices and agencies with operating budgets exceeding $5 billion).

Many of the congressional decisions that led to the adoption of this light-touch oversight were made in the 1970s and now appear anachronistic. In particular, Congress designed the Fed’s monetary policymaking body, the Federal Open Market Committee (FOMC), to ensure that its policy decisions would be thoroughly debated by individually accountable experts with diverse points of view. In recent years, however, FOMC voting patterns suggest that the Fed’s internal governance has shifted to expand the power of the Fed chair and to diminish the independence of other Fed officials. There have been no FOMC dissents at all in the past two years, and the FOMC acts like a corporate board whose members speak with one voice. The dearth of dissenting views has likely hampered Congress’s ability to raise important and sufficiently specific questions about the Fed’s monetary policy programs and operations.

The Fed did not consult with Congress before overhauling its monetary policy framework in 2020. That framework likely contributed to the Fed’s passivity when inflation surged in 2021, but there were no dissenting FOMC votes regarding the framework revision or the subsequent policy inertia. Moreover, the Fed’s asset purchase program in 2020–22 has subsequently led to unprecedented operating losses and to the suspension of its remittances to the US Treasury. Indeed, this program’s total cost to taxpayers is now projected to be about $1.6 trillion, but the Fed has never provided Congress with any cost-benefit analysis for the program.

The Fed is not the first agency in US history to outpace appropriate congressional oversight. Congress established national security agencies shortly after World War II but did not institute mechanisms for meaningful oversight of those agencies until the early 1990s. In similar fashion, Congress may now wish to revisit its mechanisms for overseeing the Fed.

Shifts in the Fed’s Internal Governance

As the Federal Reserve carries out its monetary policy duties, it is directly exercising Congress’s powers to regulate money and to borrow directly from the public. Article I of the Constitution states that Congress shall have the power “to coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures.”2 The founders specifically granted these powers to the legislative branch rather than the executive branch. Consequently, the Fed has a unique relationship with the president, whose authority to remove Fed officials is tightly constrained, and with the courts, which have consistently abstained from judicial review. In effect, the Fed exercises its power without any of the usual checks and balances, thereby underscoring the rationale for robust congressional oversight of the Fed’s monetary policymaking.

Congress carefully designed the Fed as an independent agency that comprises individually accountable experts whose deliberations would be well insulated from political interference.3 The seven members of the Federal Reserve Board are presidential appointees confirmed by the Senate to staggered terms of 14 years and removable only “for cause.” In addition, there are 12 regional Federal Reserve Banks that Congress intended to be overseen by but not subordinated to the Federal Reserve Board. Each Fed Bank is overseen by its own independent board of directors, who select its president subject to the approval of the Federal Reserve Board.4 The Fed Bank presidents and the Federal Reserve Board members jointly constitute the FOMC; most of the Fed Bank presidents vote on a rotating basis.5

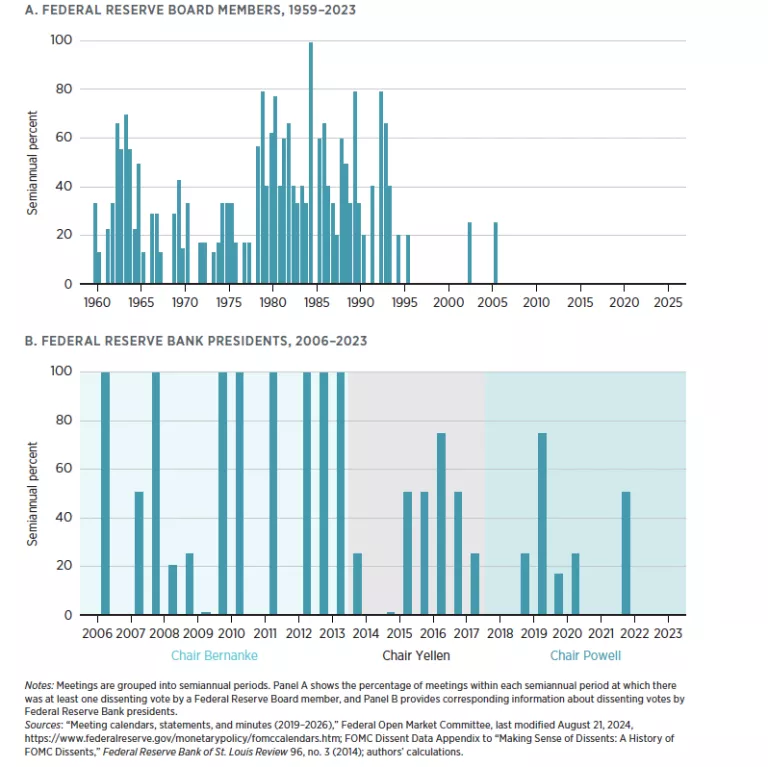

Notwithstanding this design, the Fed’s monetary policymaking has exhibited a growing degree of uniformity in recent years. As shown in figure 1 panel A, members of the Federal Reserve Board regularly dissented on FOMC decisions from the late 1950s until the early 1990s, but there were no such dissents from 2006 to 2023.6 That streak was finally broken by Fed Governor Michelle Bowman, who cast a dissenting vote at the September 2024 FOMC meeting. As shown in figure 1 panel B, dissents by Fed Bank presidents were still quite common a decade ago but became increasingly rare thereafter, with no dissents at all since mid-2022. In fact, none of the current cohort of Fed Bank presidents has dissented from any FOMC decision.

In our law review article, we identify several distinct trends in the Fed’s governance that have contributed to the uniformity in its monetary policymaking. In particular, while the Federal Reserve Board is a multimember commission, the Fed chair is not merely “first among equals” but has an outsize role in determining the Fed’s monetary policy decisions.

The Fed chair serves as the Federal Reserve Board’s CEO, whereas the other six members of the Federal Reserve Board have nonexecutive roles. Thus, the chair effectively directs the entire staff of the Federal Reserve Board, who produce economic forecasts and other background materials that serve as the focal point for the FOMC’s monetary policy deliberations.

The Fed chair is often the most senior member on the Fed Board, further strengthening the centrality of this role. Each vice chair departs after a single four-year term, and other Fed Board members often serve for just a few years before taking a position elsewhere.7 Instead of serving the staggered 14-year terms that Congress intended, new members of the Fed Board often fill vacant seats, serving partial terms that may last just a few years.

It has become commonplace for every Federal Reserve Board member to have been appointed by the current incumbent of the White House.8 These shifts in the Fed Board’s composition could undermine public confidence that its policy decisions are being made on a nonpartisan basis.

The Federal Reserve Board has become increasingly involved in the selection of Fed Bank presidents. For nearly a century, the directors of each Fed Bank carried out this responsibility with little or no involvement of the Federal Reserve Board. Since 2015, however, a Fed Board member has been directly involved in all stages of the selection of each Fed Bank president, and there have been growing concerns that such involvement may effectively dictate the outcome of the process.

FIGURE 1. Dissenting votes at Federal Open Market Committee meetings

Indeed, in its 2019 review of Fed governance, the White House Office of Legal Counsel concluded that Fed Bank presidents are appropriately viewed as “subordinates” of the Federal Reserve Board.9 However, that conclusion seems directly contrary to the original intent of Congress in designing the Fed’s governance.

Shortcomings in the Fed’s Accountability to Congress

In assessing the Fed’s accountability to Congress, our analysis identifies specific shortcomings regarding the Fed’s monetary policy goals and strategy, management of its balance sheet, and cost-benefit analysis of its monetary policy programs.

Monetary Policy Goals and Strategy

Congress has given the FOMC a broad mandate to foster maximum employment and stable prices, but the Fed is not required to provide any regular reporting regarding its quantification of these objectives.10 For example, there are no indications that the Fed engaged in congressional consultations before the 2020 overhaul of its monetary policy framework, when it shifted to an asymmetric tilt toward elevated inflation. Consequently, the operational definition of price stability became more discretionary and more opaque, with ambiguity about the horizon over which inflation would be averaged and the duration over which it might remain elevated. Indeed, some former Fed officials have concluded that this framework revision paved the way for the Fed’s subsequent inertia in responding to the inflation surge of 2021.11

Thus, strengthened reporting requirements might be appropriate to foster appropriate congressional oversight of such changes. Indeed, some prominent economists have urged the Fed to revise its inflation target upward, to 3 percent or even higher.12 Such a change might seem blatantly inconsistent with the Fed’s price stability mandate but could be adopted at any time unless Congress imposes more substantial reporting requirements.

Since 2017, the Fed’s monetary policy reports to Congress have generally included information about the prescriptions of simple benchmarks, such as the Taylor rule, but these reports have provided no explanation for substantial deviations from the policy benchmarks.13 Moreover, these reports summarize the Fed’s baseline economic outlook but do not provide any assessment of material risks or any information about how monetary policy might need to be adjusted if this premise turns out to be incorrect. Ironically, the Fed requires all large and systemically important banking institutions to undergo regular stress tests of their balance sheets, and hence it seems reasonable for Congress to establish a similar regimen according to which the Fed will engage in regular “stress tests for monetary policy.”14

Balance Sheet Programs

The Constitution vests Congress with the sole authority to “borrow money on the credit of the United States.”15 In recent years, however, that power has effectively been delegated to the Fed, which is now funding its own operating losses by issuing interest-bearing liabilities to the public.

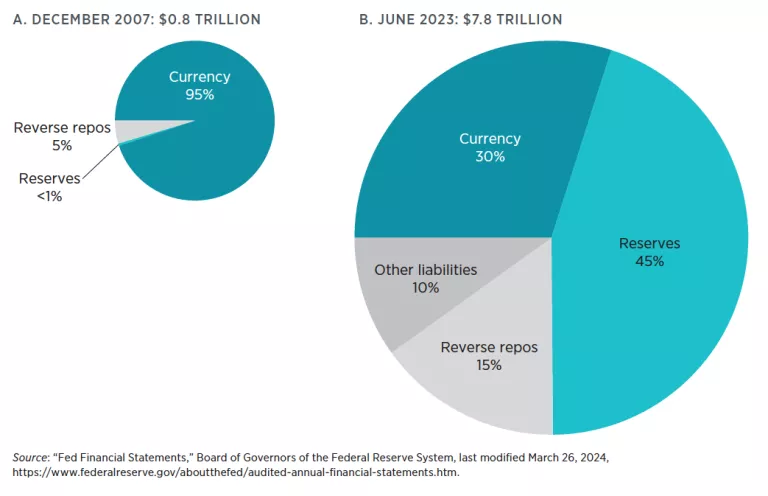

As shown in figure 2, the Fed’s balance sheet in 2007 was very simple and practically risk-free. Nearly all of the Fed’s liabilities consisted of paper currency and bank reserves held at the Fed, which paid no interest, while its holdings of Treasury securities generated a steady stream of interest earnings that were remitted to the US Treasury. Since 2008, however, the Fed’s balance sheet has ballooned by a factor of 10 and has become far more complex and riskier.

FIGURE 2. The Federal Reserve’s liabilities

Indeed, since fall 2022 the Fed has been incurring unprecedented operating losses that have directly resulted from the securities purchase program that it conducted from March 2020 to March 2022. As shown in figure 3, the costs of that program will continue to weigh on the Fed’s remittances to the US Treasury for the foreseeable future, and the overall cost to taxpayers is projected to be about $1.6 trillion.16 Among US public institutions, the Federal Reserve is unique in determining its own accounting rules rather than following GAAP.17 Consequently, the Fed’s operating losses are recorded on its financial statements as a “deferred asset” rather than as negative net worth.

FIGURE 3. Federal Reserve remittances to the US Treasury

A private institution in such circumstances might well be faced with the prospect of a takeover, bankruptcy, or liquidation. By contrast, the Fed is covering its operating losses by expanding its interest-bearing liabilities: in effect, the Fed is borrowing those funds directly from the public without congressional authorization.18 Indeed, the Fed’s ability to issue practically unlimited amounts of interest-bearing liabilities, outside the constraints of the federal debt ceiling, may be viewed as making the Fed “super-independent.”19

Cost-Benefit Analysis

With the sole exception of the Fed, every program of every federal department, office, and agency is audited by the GAO, an independent agency that reports directly to Congress. The GAO not only examines these institutions’ financial books but engages in comprehensive performance reviews that foster efficiency and public accountability. By contrast, the Fed is subject only to narrow financial audits conducted by a private accounting firm that has no accountability to Congress or the public.20 Moreover, the Fed’s audits are strictly limited in scope, with the sole purpose of verifying the accuracy of the Fed’s financial statements rather than gauging the efficacy or efficiency of programs, as in a performance audit.

The GAO has a strong track record as an effective congressional watchdog. Every recommendation that the GAO makes to every federal agency is posted on the GAO’s website along with an indication about whether the recommendation was implemented. Thus the GAO can document that, over the past decade, about 80 percent of its recommendations have been followed, and these measures have saved taxpayers nearly $1 trillion.21

While the Fed’s technical and logistical operations are subject to routine reviews, the GAO is prohibited by statute from auditing the efficiency and effectiveness of the Fed’s monetary policy framework or programs.22 Consequently, the Fed’s securities purchases have never been subjected to a comprehensive GAO review. If such a review had been conducted in the wake of previous programs, its findings could have highlighted potential concerns about the efficacy and risks of those purchases.

Though the GAO is an independent agency with an impeccable track record of nonpartisan analysis, a potential concern is whether GAO reviews could exacerbate the risk of political interference in the Fed’s monetary policy deliberations. To mitigate this concern, the GAO could be authorized to conduct comprehensive reviews on a fixed annual schedule rather than conducting reviews initiated by requests from congressional committees or individual members of Congress.

Finally, legislators could consider measures to strengthen the independence of the Fed’s inspector general and broaden the scope of the IG’s authority. The IG could serve as a congressional watchdog for the entire Federal Reserve System, not just the Federal Reserve Board. In fact, every other major office and agency (those with operating expenses exceeding $5 billion) has a fully independent IG who is appointed by the president, is confirmed by the Senate, and may be removed only by the president for cause.23 By contrast, the Fed’s IG is merely a Fed employee who is appointed by the Fed chair and is removable by a vote of the Federal Reserve Board.24

Moreover, current law states that the Fed’s IG shall work “under the authority, direction, and control” of the Fed chair while conducting any audit or investigation related to monetary policy. In principle, of course, the Fed chair could direct the IG to conduct a comprehensive evaluation of the FOMC’s balance sheet policies and programs. If such an evaluation had been conducted in the late 2010s, following the completion of preceding rounds of securities purchases, an IG report might have alerted Congress that such a program could incur significant costs. However, there is no indication that the Fed’s IG has embarked on such an evaluation, even in the wake of the operating losses associated with the latest round of securities purchases.

Strengthening Congressional Access to Internal Fed Information

As they carry out their constitutional responsibility to oversee the Federal Reserve, members of Congress have raised concerns about a range of issues, including (1) the process of selecting the president of each regional Federal Reserve Bank, especially given the role of those officials as members of the FOMC; (2) the FOMC’s management of its balance sheet, especially given recent operating losses; and (3) the FOMC’s complacency about elevated inflation in 2021, which set the stage for rapid tightening and major bank failures more recently. However, constraints on legislators’ access to internal Fed information have inhibited Congress’s ability to carry out inquiries and investigations into such issues.

To facilitate congressional access to sensitive Fed information, it seems helpful to consider how Congress maintains oversight of intelligence activities while ensuring the protection of highly sensitive national security information. In particular, the Intelligence Authorization Act of 1991 instituted the following procedures for congressional oversight of the Central Intelligence Agency:

Routine intelligence activities. The CIA director and other intelligence officials must ensure that both congressional oversight committees are kept “fully and currently informed” about all noncovert activities, including any significant intelligence failures, and must respond to oversight committee requests by providing all information or material within their custody or control.25 A parallel set of provisions requires the CIA director and other intelligence officials to keep the oversight committees “fully and currently informed” about all covert activities “to the extent consistent with due regard for the protection from unauthorized disclosure of classified information relating to sensitive intelligence sources and methods or other exceptionally sensitive matters.”26

Extraordinary covert operations. The president must specifically authorize every covert operation with a written finding that is promptly given to both congressional oversight committees. However, if the president determines that it is essential to limit access to the finding “to meet extraordinary circumstances affecting vital interests of the United States,” then “the finding may be reported to the chairmen and ranking minority members of the intelligence committees, the Speaker and minority leader of the House of Representatives, the majority and minority leaders of the Senate, and such other member or members of the congressional leadership as may be included by the President.”27

Such provisions could serve as a useful template for strengthening congressional oversight of the Fed. In particular, Fed officials could be required to keep both oversight committees—the Senate Banking Committee and the House Financial Services Committee—“fully and currently informed” about the Fed’s internal procedures and operations and to provide prompt and complete information in response to all committee requests. Moreover, to protect the most market-sensitive information, the Federal Reserve Board could be authorized to provide such information solely to the chair and ranking minority member of each oversight committee and to the top officials in each chamber of Congress.

More broadly, Congress has a constitutional obligation to maintain effective oversight of the Fed. Over the past 15 years, however, the scope and complexity of monetary policy has outpaced Congress’s ability to monitor the Fed’s monetary policymaking through existing mechanisms of oversight. In coming years, persistent congressional “undersight” could threaten the delicate balance between the Fed’s independence and its public accountability. Potential methods for restoring this balance may well include strengthened reporting requirements, initiation of external reviews by congressional watchdogs, and assurance of congressional access to sensitive information.

About the Authors

Andrew T. Levin is a professor of economics at Dartmouth College. Levin is currently a regular visiting scholar at the International Monetary Fund and a member of the Bank of England’s academic advisory group on central bank digital currency. He received his PhD in economics from Stanford University and worked at the Federal Reserve Board for two decades, including two years as a special adviser to the chair and vice chair on monetary policy strategy and communications.

Christina Parajon Skinner is an associate professor and codirector of the Wharton Initiative on Financial Policy and Regulation at the Wharton School of the University of Pennsylvania and holds a JD from Yale Law School. Before joining the faculty at Wharton, Skinner served as legal counsel at the Bank of England in the financial stability division of the bank’s legal directorate.

Notes

1. Andrew T. Levin and Christina Parajon Skinner, “Central Bank Undersight: Assessing the Federal Reserve’s Accountability to Congress,” Vanderbilt Law Review, forthcoming.

2. U.S. Const. art. I, § 8.

3. Congress identified the key characteristics of an independent agency in 1887 when it created the Interstate Commerce Commission. In particular, an independent agency should have an uneven number of commissioners who are appointed to staggered terms of a fixed period extending beyond the term of the president and who can be removed by the president only “for cause”—i.e., inefficiency, neglect of duty, or malfeasance in office. In addition, no more than a bare majority of the commissioners should be from any single political party.

4. Each regional Fed Bank’s president is selected by six of its directors, of whom three are chosen by commercial banks within that district and three are chosen by the Federal Reserve Board.

5. The Federal Reserve Board members and the Federal Reserve Bank of New York’s president cast votes at every FOMC meeting; 4 of the 11 other Fed Bank presidents vote on an annually rotating basis.

6. See Federal Reserve Bank of St. Louis, “A History of FOMC Dissents,” September 16, 2014.

7. See Levin and Skinner, “Central Bank Undersight,” figure 2A.

8. See Levin and Skinner, “Central Bank Undersight,” figure 2B.

9. This conclusion reflected the Office of Legal Counsel’s assessment of a number of factors, including the Federal Reserve Board’s influence on the selection of Fed Bank presidents, its scope of control over their budgets and operations, and its practically unconstrained ability to remove them from office. See US Department of Justice, Office of Legal Counsel, “Appointment and Removal of Federal Reserve Bank Members of the Federal Open Market Committee,” October 23, 2019.

10. The Federal Reserve Reform Act of 1977 and the Humphrey-Hawkins Act of 1978 established specific reporting requirements, but those requirements were practically eliminated by an omnibus bill passed in late December 2000.

11. See Charles Plosser, “The Fed’s Risky Experiment” (Economics Working Paper No. 21116, Hoover Institution, Stanford, CA, June 18, 2021); Gauti B. Eggertsson and Don Kohn, “The Inflation Surge of the 2020s: The Role of Monetary Policy,” Brookings Institution, May 23, 2023, https://www.brookings.edu/wp-content/uploads/2023/04/Eggertsson-Kohn-co…; Mickey D. Levy and Charles Plosser, “The Murky Future of Monetary Policy,” Federal Reserve Bank of St. Louis Review 104 (2022): 178.

12. See Jason Furman, “The Fed Should Carefully Aim for a Higher Inflation Target,” The Wall Street Journal, August 23, 2023; Jeff Sommer, “The Fed Has Targeted 2% Inflation. Should It Aim Higher?,” The New York Times, March 24, 2023.

13. Such information was omitted from the monetary policy reports that were sent to Congress in June 2020 and February 2021. See Federal Reserve Board, Monetary Policy Report, June 12, 2020,https://www.federalreserve.gov/ monetarypolicy/files/20200612_mprfullreport.pdf; Federal Reserve Board, Monetary Policy Report, February 19, 2021, https://www.federalreserve.gov/monetarypolicy/files/20210219_mprfullrep….

14. See Andrew T. Levin, “The Design and Communication of Systematic Monetary Policy Strategies,” Journal of Economic Dynamics and Control 49 (2014): 52; Michael D. Bordo, Andrew T. Levin, and Mickey D. Levy, “Incorporating Scenario Analysis into the Federal Reserve’s Policy Strategy and Communications” (NBER Working Paper No. 27369, National Bureau of Economic Research, Cambridge, MA, June 2020).

15. U.S. Const. art. I, § 8.

16. Gauging the Fed’s remittances in terms of GDP is appropriate because the US economy has grown markedly over the past six decades: Nominal GDP was about $540 billion in 1960 and is now approaching $27 trillion.

17. The Financial Accounting Standards Board determines GAAP for all nongovernmental institutions, including federally chartered enterprises such as Amtrak and Fannie Mae, while the Federal Accounting Standards Advisory Board is responsible for determining GAAP for all federal financial reporting entities, including cabinet departments, offices, and independent agencies such as the Federal Deposit Insurance Corporation and the Securities and Exchange Commission.

18. Since the Fed has authority to issue legal tender, its liabilities are broadly perceived as having the full faith and credit of the US government.

19. Juliana B. Bolzani, “Independent Central Banks and Independent Agencies: Is the Fed Super Independent?,” UC Davis Business Law Journal 22 (2022): 195.

20. The Fed’s combined financial statements were audited by Deloitte from 2007 to 2014 and have been audited by KPMG since then. In recent decades the work of auditing firms has been plagued by recurring performance failures, but analysis of that issue is beyond the scope of this policy brief.

21. Government Accountability Office, Performance and Accountability Report: Fiscal Year 2022.

22. 31 U.S.C. § 714(b). The Dodd-Frank Act added the provision that the GAO may audit such transactions solely for the purposes of assessing operational integrity, accounting and financial reporting, internal controls, eligibility criteria, security and collateral policies, and the selection and payment of third-party contractors. 31 U.S.C. § 714(f)(2).

23. The president must notify Congress about the reasons for such a removal.

24. At a congressional hearing in 2009, the GAO’s General Counsel Gary L. Kepplinger stated, “We believe that the differences in the appointment and removal processes between presidentially appointed IGs and those appointed by agency heads result in a clear difference in the organizational independence of these IGs.” Gary L. Kepplinger, “Inspectors General: Independent Oversight of Financial Regulatory Agencies” (GAO document 09-524T, testimony before the Subcommittee on Government Management, Organization and Procurement, House Committee on Oversight and Government Reform, March 25, 2009).

25. 50 U.S.C. § 3092.

26. 50 U.S.C. § 3093(b).

27. 50 U.S.C. § 3093(c).