- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Supplemental Transition Accounts for Retirement

A Proposal to Increase Retirement Income Security and Reform Social Security

Social Security’s inflation-protected lifelong benefits are critical for old-age economic security. These benefits will become even more important in the decades ahead because of rising life expectancies and the shift away from traditional pensions to 401(k)-type plans. Social Security could do more to improve older Americans’ financial security by facilitating later claiming of benefits. Between the ages of 62 and 70, monthly Social Security benefits increase by about 7 percent to 8 percent for each one-year delay in claiming. This increase is reflected in higher monthly benefits for the life of the beneficiary and can also result in higher benefits for surviving spouses.

We propose establishing mandatory add-on savings accounts, which we call Supplemental Transition Accounts for Retirement (START), to provide workers and their spouses the necessary income to delay claiming Social Security benefits. The accounts would be funded by employees, employers, and a government contribution for low-income households fully paid for with revenue from taxing START distributions. Each worker would be required to exhaust START assets before receiving Social Security benefits. STARTs would mitigate the effects of actuarial reductions for claiming early and could allow workers to gain additional monthly Social Security benefits through delayed retirement credits.

Beneficiaries could begin to receive monthly START benefits at the earliest eligibility age but would not be required to do so. The amount of monthly START benefits payable under the proposal would be limited to the Social Security benefits that the beneficiary would have received under current-law claiming rules. At full retirement age (age 67 for people born in 1960 or after) and up to age 70, beneficiaries could use START assets without restriction (e.g., taking a lump sum). At age 70, account holders with START assets would be required to take a full lump-sum distribution, or roll the balance into a retirement account or a beneficiary’s START. Any money remaining in a START at the time of the account owner’s death would go to a designated beneficiary.

Funding

START contributions would be required for all workers who have taxable earnings covered under Social Security and who have not reached their full retirement age (FRA); required contributions would not apply to earnings beginning on January 1 in the year the worker reaches FRA. To enable younger workers to take advantage of compounding of interest and earnings, there would not be a minimum age requirement.

Each worker and employer would contribute 1 percent of earnings (2 percent combined), up to the annual maximum subject to Social Security payroll tax ($125,500 in 2017), to the worker’s START. The self-employed would make required contributions as both employer and employee. For married couples, total contributions would be split equally between each spouse’s START. Employee contributions would be after-tax and employer contributions would be pretax.

The Social Security Administration (SSA) would enroll all Social Security-covered workers in START. START contributions would be collected in the same way and under the same schedule as payroll taxes.

The federal government would contribute to the STARTs of low-income workers. The maximum government contribution would be 1 percent of earnings for married couples ling jointly with adjusted gross income (AGI) less than $40,000, single filers with AGI less than $20,000, and head of household filers with AGI less than $30,000. The government contribution would be phased out over an AGI range of $10,000, $7,500, and $5,000 for joint filers, head of household filers, and single filers, respectively. For example, the government contributions for joint filers with AGI of $42,500 would be 0.75 percent and with AGI of $45,000 would be 0.5 percent. Workers in low-income households would receive a total START contribution of up to 3 percent of earnings. The government contribution would be treated like an employer contribution and would not be included in current taxable income.

Account Structure and Administrative Considerations

STARTs would be professionally managed in a pooled account with an emphasis on keeping administrative fees as low as possible. An independent board would serve as the fiduciary. The board would select the private investment firm(s) responsible for managing START assets and set the investment guidelines for the pooled assets. Individuals would not be allowed to select investments.

Because STARTs would be integrated with Social Security, SSA can take advantage

of existing program systems and bene t from economies of scale in administrating these accounts. SSA’s tasks would include maintaining account records, such as tracking individual account balances and transactions, and educating participants about STARTs.

Results

The Urban Institute analyzed our proposal using its dynamic simulation model DYNASIM. The simulation results reported below are based on the conservative assumption that employees reduce their workplace retirement plan contributions to zero or by the amount of their START contributions, whichever change is smaller. Under the alternative assumption of no savings offset, the increases in income are larger, in particular for higher earners, than those shown below.

The Urban Institute’s analysis revealed the following:

- The proposal is fully funded by employee and employer contributions and by crediting the Social Security trust funds with the revenue from taxing START distributions. This last item more than offsets the cost of government contributions, thereby reducing Social Security’s 75-year actuarial deficit by about 12 percent, based on the Urban Institute’s modeling assumptions using data from the 2015 Social Security Trustees Report.

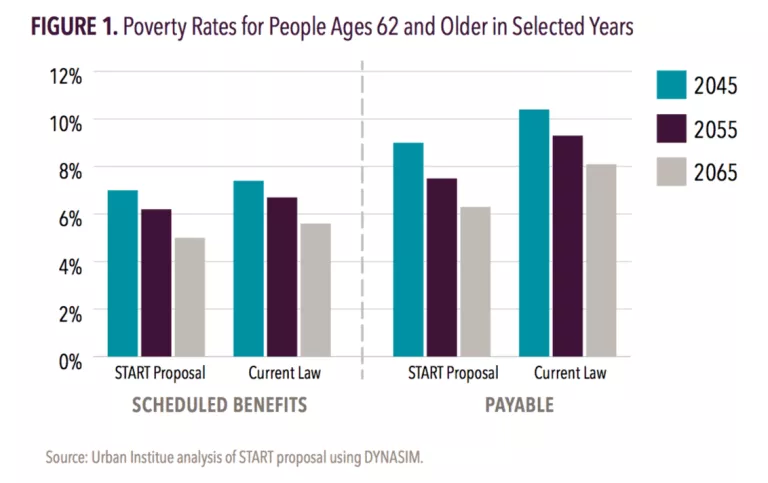

- STARTs would reduce poverty significantly for people ages 62 and over under current law’s scheduled benefits: from 7.4 percent to 7.0 percent in 2045 and from 5.6 percent to 5.0 percent in 2065. STARTs would reduce poverty by even more under the payable benefits scenario (i.e., benefits would be limited to Social Security tax revenue once the trust funds are exhausted in 2034): from 10.4 percent to 9.0 percent in 2045 and from 8.1 percent to 6.3 percent in 2065.

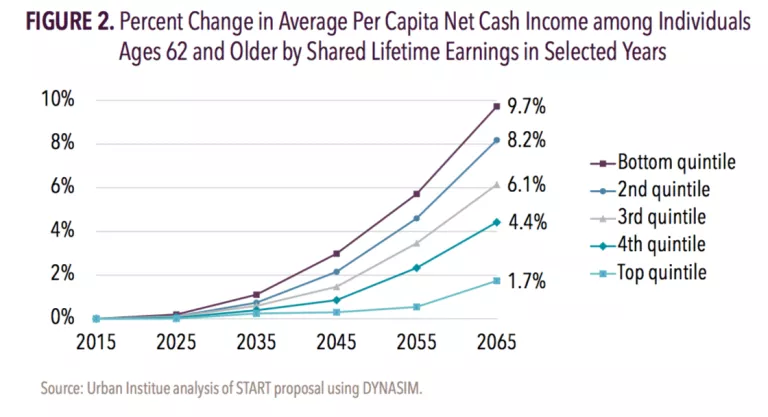

- STARTs would raise the net per-capita cash income the most for older Americans with the lowest lifetime earnings: by 10 percent, on average, and 15 percent at the median in 2065 compared to scheduled benefits under current law. In part, this result reflects lower- income households’ greater reliance on Social Security benefits, which in many cases is their only source of income.

- Among those ages 62 and older, START would raise income the most for the age groups 70–74 and 75–79: about 8 percent, on average, in 2065. The increases for those age groups represent the most accurate picture of the full potential of our proposal on economic security at older ages, given that individuals in those birth cohorts would have participated in START over their whole careers.

START Outcomes

Supplemental Transition Accounts for Retirement would provide the necessary bridge to allow individuals to delay claiming Social Security benefits. And it would do so without limiting access to essential income at early retirement ages. The result would be higher monthly Social Security benefits and income—on average, about 5 percent to 7 percent overall and 10 percent for the lowest-income workers—that cannot be outlived or eroded by inflation.

Additional details

This was originally published by AARP. Click here to read more.