The Federal Reserve System (the Fed) was created in 1913 and consists of 12 regional Federal Reserve banks plus the Board of Governors in Washington, DC. Jerome Powell is currently the chair of the Board of Governors. While the Fed has many duties, including bank regulation, monetary policy is by far its most important task. This brief will explain the basics of why the Fed is so important, how it operates, and what it is trying to accomplish with monetary policy. The brief will explain the Fed in four steps:

- What is the medium-of-account role of money and why is it important?

- How does the Fed control monetary policy?

- What is the role of interest rate targeting?

- What are the Fed’s objectives and how does it try to achieve them?

1. Money as a Medium of Account

Money plays a special role in the American economy owing to the fact that almost all wages, prices, and debt contracts are priced in terms of US dollars. This means the dollar is Americans’ medium of account, the asset in which all other prices are measured. Furthermore, the Fed has a monopoly on the issuance of the most highly liquid of all types of money, which is called the monetary base. The base consists of both currency in people’s wallets and also reserves that commercial banks have on deposit at the Fed. When the media talks about the government creating money, it is referring to the monetary base.

Unlike with stocks and bonds, which have values that fluctuate in the marketplace, the nominal price of a dollar is always one dollar. But money is not immune to the laws of supply and demand. Its real value (purchasing power) can change over time, just as with any other asset. When money loses value, the loss shows up as a rising price level for goods and services (inflation). In the rare cases where money gains value, the gain shows up as a falling price level (deflation). Thus, if the price level doubles, the value (or purchasing power) of one dollar falls in half, and vice versa.

Fed policy is extremely important because the Fed’s policy tools allow it to determine the average rate of inflation and influence variables such as real GDP, unemployment, interest rates, and exchange rates.

Economists often use the supply and demand model to explain changes in the value of a good, service, or financial asset. Fed policy can also be explained using this model. All the various actions the Fed takes to implement monetary policy, including quantitative easing (QE), interest on bank reserves, and forward guidance, affect the price level by impacting the supply or demand (or both) for base money. Many pundits take shortcuts and overlook the supply and demand implications of monetary policy actions. This can lead to serious misunderstandings regarding the effects of monetary policy.

2. How the Fed Determines the Supply and Demand for Base Money

Throughout the first 95 years of Fed history (until 2008), monetary policy consisted primarily of Fed actions that increased or decreased the supply of money. When the Fed wished to inject more money into the economy, increasing the supply, it generally purchased Treasury securities with newly created money—an open market purchase. These injections of new money are referred to as expansionary monetary policy or “easy money.” QE is the name given to unusually large open market purchases, generally conducted in an environment of near-zero interest rates.

In an accounting sense, these open market purchases are quite simple. If the Fed wishes to increase the monetary base by $120 million, then it purchases $120 million worth of Treasuries. The person or institution selling bonds to the Fed receives the newly created base money. This new base money initially goes into bank reserves, but most of it eventually goes out into circulation as currency held by the public. When the Fed wishes to increase the monetary base for only a limited period of time, it will often engage in a repurchase agreement, or repo, where the Fed buys Treasury bonds from the public with a promise to later resell them at a slightly higher price.

If the Fed wishes to reduce the monetary base by $40 million, then it sells $40 million in Treasury bonds, and the money received by the Fed is pulled out of circulation. These open market sales are the primary method by which the Fed implements a contractionary monetary policy, or “tight money,” and are generally aimed at reducing inflation. A “reverse repo” can be used to temporarily reduce the monetary base; the Fed sells bonds to the public with a promise to repurchase them at a specified later date.

As with any other asset, an increase in the supply of money tends to reduce its value. Recall that since the price of a dollar is always one dollar, the value of money can only fall with an increase in the overall price of goods and services. Thus, expansionary monetary policy, which increases the supply of money, tends to increase inflation, other things equal. Contractionary monetary policy, which reduces the supply of money, tends to decrease inflation, other things equal.

After 2008, monetary policy became more complex. The Fed added policy tools that primarily impact the demand for base money, not just the supply. One particularly important new tool is interest on bank reserves (IOR), where the Fed pays interest on reserves that commercial banks hold at the Fed and adjusts this interest rate to impact monetary conditions.

When the Fed seeks a more expansionary monetary policy, it reduces the IOR rate, which makes it less attractive for banks to hold reserves. The resulting fall in the demand for bank reserves is expansionary because less demand for any asset will reduce its value. Recall that a fall in the value of money means a rise in the overall price level. If this relationship seems unclear, consider that a fall in the demand for money is much like an increase in the supply of money. In both cases, members of the public temporarily hold more money than they prefer, and in trying to get rid of these excess cash balances, they boost their spending on consumer and investment goods, which tends to push the price level higher.

When the Fed wishes to adopt a more contractionary policy, perhaps to reduce inflation, it seeks to encourage an increase in the demand for money. Thus, it might pay a higher rate of IOR, encouraging banks to hold onto their reserves. An increased demand for reserves will tend to increase the value of money. Recall that this occurs through a fall in the overall price level.

The Fed can also impact the demand for money through forward guidance (that is, creating more bullish or bearish expectations regarding the future path of policy). A promise to keep monetary policy expansionary for a long period will tend to encourage spending today, boosting the price level.

While all monetary policies work by changing the supply or demand for base money, they can do so through a variety of channels, or transmission mechanisms. An expansionary policy may raise asset prices, increase bank lending, depreciate the dollar in the foreign exchange market, boost inflation expectations, create excess cash balances that spur spending, or cause some combination of those effects. A contractionary policy has the opposite effects.

3. The Relationship between Interest Rates and Monetary Policy

Even though monetary policy is fundamentally about influencing the supply and demand for money, many reporters, and even some economists, discuss monetary policy by referring to changes in interest rates. The Fed’s Federal Open Market Committee usually sets an interest rate target, and changes in this target are frequently viewed as being equivalent to changes in monetary policy. Low short-term interest rates are often viewed as expansionary policy and high rates as contractionary. Unfortunately, this view is often incorrect and the source of a great deal of misunderstanding.

It is true that expansionary monetary policies usually lead to a temporary decrease in the level of interest rates. For instance, an open market purchase of Treasury bonds doesn’t just boost the money supply; it also tends to reduce short-term interest rates by boosting the amount of liquidity in the economy. Contractionary policies often lead to a temporary increase in short-term interest rates. But it is not generally valid to work backwards and make an inference about monetary policy from a change in interest rates.

Those who assume that lower rates are easy money, and vice versa, are engaging in the fallacy of reasoning from a price change. As an analogy, a decrease in the supply of oil will often lead to higher prices for oil, as in 1974 and 1980. But the reverse is not true. It is not always the case that an increase in the price of oil shows that the supply of oil has decreased. For example, global oil prices rose sharply in 2007 and early 2008 owing to a rise in global oil demand, especially from developing countries such as China. Drawing an inference from a price change without first considering whether the price change was caused by a supply shift or a demand shift is called reasoning from a price change.

Interest rates are impacted by many factors, including monetary policy, economic growth, and inflation. An expansionary monetary policy may reduce interest rates in the short run. But it may also boost national output and inflation. Increases in output and inflation often lead to higher interest rates in the long run. Lenders demand higher rates to be compensated for the effects of inflation, and rising output (and incomes) leads to more demand for credit, pushing up interest rates.

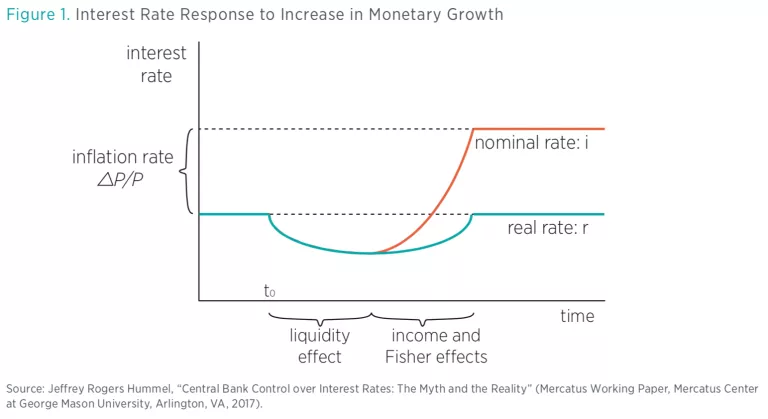

Figure 1 illustrates how monetary policy reduces interest rates in the short run but can lead to higher interest rates in the long run. When the money supply expands, it adds more liquidity to the economy and reduces both the nominal and the real (inflation-adjusted) interest rate. This initial decline is called the liquidity effect. However, the expansionary monetary policy also increases income, which boosts demand for credit, pushing interest rates higher (the income effect). Lenders will also raise rates further in anticipation of the higher inflation caused by the increase in the money supply (the Fisher effect).

Thus, interest rates rose sharply from 1965 to 1981, but not because monetary policy was contractionary. Indeed, this period (called the Great Inflation) saw some of the most expansionary monetary policy in American history. The expanding money supply led to high inflation, which boosted nominal interest rates to a peak of almost 20 percent. Conversely, a very contractionary monetary policy during the early 1930s led to deflation and very low interest rates.

When evaluating Fed policy, one shouldn’t just look at interest rates. Rather, one should focus on changes in variables such as inflation and GDP. If interest rates are low, but inflation and GDP are also falling, then the low rates may reflect broader macroeconomic forces, not easy money.

Because interest rates are not a reliable indicator of monetary policy, many economists (including Ben Bernanke) believe that changes in nominal GDP provide a better indication of whether monetary policy is too easy or too tight. Nominal GDP growth is composed of the sum of inflation and growth in real GDP. To better understand the importance of nominal GDP growth, it’s important to understand the Fed’s congressional mandate, sometimes called the “dual mandate.”

4. The Fed’s Policy Goals and How to Achieve Them

In 1978, Congress gave the Fed a mandate to achieve stable prices, high employment, and moderate long-term interest rates. The Fed believes that it can only achieve moderate long-term interest rates by keeping inflation low and stable. Thus, as a practical matter, the Fed focuses on price stability and high employment—the dual mandate. The Fed interprets price stability as 2 percent inflation and interprets high employment as an unemployment rate that is close to the natural rate, estimated to be roughly 4 percent. However, the natural unemployment rate is not completely constant, and estimates can vary over time.

Notice that 2 percent inflation isn’t exactly “price stability”; indeed, 0 percent inflation would seem to better meet that definition. For a variety of reasons, the Fed prefers a 2 percent inflation target. Fed officials worry that a 0 percent average inflation rate would occasionally lead to deflation, which can result in high unemployment (violating the other part of the Fed’s dual mandate). They also worry that with 0 percent inflation, the nominal interest rate would also frequently fall to zero, making it harder to conduct monetary policy. Thus, the 2 percent inflation target is a compromise—higher than true price stability, but much lower than the inflation of the 1960s, 1970s, and 1980s. To summarize, 2 percent inflation and roughly 4 percent unemployment is how the Fed currently interprets its dual mandate.

When inflation is above 2 percent, the Fed may conduct a contractionary monetary policy. This might consist of open market sales to reduce the monetary base or an increase in IOR to encourage banks to hold onto reserves and not move the money out into the economy where it would be spent. By reducing the supply of money or boosting the demand for money, or both, the Fed raises the value of money, which holds down inflation.

When inflation is less than 2 percent, the Fed may conduct an expansionary monetary policy. This might consist of open market purchases to boost the monetary base or a decrease in IOR to discourage banks from holding onto reserves. In both cases, the goal is to reduce the value of money, by either increasing the money supply or reducing money demand. If successful, the fall in the value of money will lead to higher prices, moving inflation up toward the 2 percent target.

Notice that the Fed may adopt an expansionary or contractionary policy to move toward the 2 percent inflation target. In the real world, things are more complicated owing to the dual mandate. Inflation may be currently off target but expected to return to 2 percent in the near future. And in some cases, it’s not possible to simultaneously achieve both sides of the dual mandate, and the Fed must strike a balance between the effects of monetary policy on inflation and its effects on employment.

Recall that nominal GDP growth is the sum of inflation and real GDP growth. Because real GDP is closely linked to the employment part of the dual mandate, some economists favor a nominal GDP target growth rate of roughly 4 percent or 5 percent, suggesting that this would provide for roughly 2 percent inflation in the long run, plus enough money to support 2 percent or 3 percent real GDP growth.

Summary

The Fed influences macroeconomic variables such as inflation, unemployment, GDP, and interest rates by adjusting the supply and demand for base money. Because the Fed has a monopoly in the production of base money, it has almost unlimited ability to influence its value, which is why Congress gave the Fed the duty of stabilizing the price level. After all, the price level is merely the inverse of the value of money. Controlling inflation means stabilizing the value of money.

Because the Fed sets a short-term interest rate target, changes in that target are often a headline story in the financial press. However, there are actually many different forces that impact market interest rates, and low interest rates do not necessarily imply that an easy money policy is in effect. Some economists believe that the underlying movement in nominal GDP growth may provide a better indication of whether policy is easy or tight, relative to the underlying goals of Fed policy.