- | Labor Markets Labor Markets

- | Policy Briefs Policy Briefs

- |

Flexible Benefits for a Flexible Workforce: Unleashing Portable Benefits Solutions for Independent Workers and the Gig Economy

Political leaders from left to right are grappling with how to approach the challenges caused by the rapid growth of an independent workforce. Today, 1-in-10 workers engage in independent work as their primary source of income, and as many as 1-in-3 use independent work as a supplementary source of income. Independent workers are diverse. They are found across a multitude of industries, skill levels, and educational attainment—for example, they can be freelance creatives or knowledge-work professionals, medium-skilled contractors, gig workers, high-skilled consultants, self-employed merchants or sellers, and entrepreneurs.

Even as more and more Americans are choosing these flexible forms of work, laws written almost one hundred years ago prohibit and discourage common workplace benefits from flowing to these workers. This is because our labor polices offer two primary paths of work. The first is through traditional employment, which comes with traditional benefits but often without the independence and flexibility that many workers desire or may require for personal reasons. The second is through independent work (legally classified as independent contracting), which provides flexibility and independence but without the common workplace benefits.

To address the challenges of independent work, there are two buckets of policy solutions:

-

Bucket 1: Reclassification. Policies that reclassify workers as employees instead of independent contractors.

-

Bucket 2: Access to Portable Benefits. Policies that allow independent workers to maintain their nontraditional work arrangements and improve their access to flexible benefits.

Currently, policymakers and regulators are only pursuing bucket 1 solutions. This is evident from the Department of Labor’s (DOL) back-and-forth changes in regulatory guidance on worker classification rules under the Fair Labor Standards Act. Most recently, on October 13, 2022, the DOL proposed a new rule that narrows the definition of “independent contractor.” Similarly, California passed Assembly Bill 5 (AB5) in 2019, creating a stricter test that significantly limited the circumstances for being an independent contractor. As intended, AB5 made it more difficult for workers to be classified as independent contractors.

By following bucket 1 solutions and narrowing the definition of what it means to be an independent contractor, policymakers and regulators, such as those at the DOL, are hoping that organizations will hire workers as employees instead of as independent contractors. But these restrictions, while they may defuse pressure from activists, will likely make independent workers worse off because companies cannot extend all contracting positions into employment positions, thereby leaving workers with fewer job opportunities altogether—as illustrated by the experience in California. Moreover, it should be noted that as many as 79 percent of primary-earning independent contractors have indicated that they prefer their arrangements over employment. Workers cite dependent care obligations, personal circumstances, or a strong preference for job flexibility (over job stability) as the primary reasons.

Reclassification efforts also do not address the central drawback for the millions of workers who still will remain as independent contractors and self-employed: access to workplace benefits. Instead of limiting work opportunities and flexibility for those who want them, policymakers should aim to provide access to more desirable portable benefits options. Portable benefits are increasingly becoming the best solution for workers to maintain their nontraditional work arrangements while also being able to access work-related benefits. However, current federal and state regulations restrict organizations, businesses, and individuals from providing independent contractors with benefits precisely because these benefits conventionally have been tied to employer-employee relationships.8 If an organization were to provide benefits to their independent contractors, those workers would likely have to be reclassified as employees.

There are other, secondary, aspects that make it difficult for portable benefits to emerge. Tax laws are unfavorable for independent contractors and effectively penalize them for health savings and retirement contributions. Moreover, federal laws prohibit independent contractors from joining together as an association to purchase health insurance.

This policy brief addresses three central points:

-

It examines why reclassification efforts are not desirable, and why portable benefits that allow workers to maintain the value of flexibility and independence while also having access to work-related benefits is the best solution. Given the diverse nature of the workforce and the complexity of work relationships, the preferences of the workers themselves, and the significant drawbacks to forcing workers into an employment relationship, reclassification policy does not seem like the best approach. Reclassification policy is a tool of the past attempting to solve the challenges of the future. Access to portable benefits is the only sustainable solution in the long run if the nature of work continues to change and flexible and diverse forms of work become the new norm. It is the best solution to help workers who choose to become entrepreneurs and self-employed small business owners.

-

It offers simple and politically feasible policy reforms to remove legal barriers across states and the federal government to allow businesses, organizations, and individuals to voluntarily provide benefits to workers. State policymakers or regulators and the Internal Revenue Service (IRS) can take the primary step of removing the presence of “benefits” from worker classification tests for independent contractors. Secondary steps include allowing Association Health Plans (AHPs) for independent contractors and allowing independent contractors to deduct healthcare and retirement contributions from the self-employment tax earnings calculations.

-

It provides a framework for the implementation of benefits for independent workers. The three design principles for the program are that (a) participation is voluntary, (b) contributions come from multiple sources, and (c) benefits accounts are tied to the worker rather than to a specific organization.

The policy reforms and design principles herein do not outline what an ideal portable-benefits world would look like, where benefits are entirely decoupled from work for both employees and independent workers. Instead, they offer simple, low-hanging-fruit solutions that are politically feasible today. Independent workers need more than just swings in worker classification rules and partisan battles between labor and business. A system of fair and flexible benefits for this flexible workforce is long overdue.

THE FUTURE OF WORK IS FLEXIBLE BENEFITS FOR A FLEXIBLE WORKFORCE

The world of work is changing. Technology, globalization, cultural attitudes, and preferences are creating both a more diverse and innovative workforce—but also challenging and transforming labor markets, the concept of work itself, and the safety net programs often associated with it. Technological innovations are reducing the transaction costs of contracting in the market and creating greater exchanges between consumers and labor suppliers, leading to more work opportunities for contractors and freelancers. At the same time, sociologist Richard Florida identified 20 years ago an emerging demographic group he called the “creative class,” who value more independent, entrepreneurial, and creative forms of work. After the COVID-19 pandemic, demands for flexible jobs are on the rise, which has led to workers seeking out more entrepreneurial endeavors and independent forms of work.

Who Are Independent Workers?

Independent work can be found across a diverse set of roles—for example, musicians, tutors, writers, online marketplace sellers, delivery drivers, electricians, software developers, translators, yoga instructors, nannies, financial advisors, graphic designers, photographers, nutritionists, Instagram “influencers,” and more than 120 other professions.

According to an IRS and Treasury Department study using tax data, between 2001–2016, the share of workers with independent contracting income has grown by 22 percent while the share of workers who were employees decreased by 1.5 percent. The largest share of independent contractors make most of their income through W-2 employment and supplement their income with independent work opportunities. They are in the top quartile of the income distribution. However, about 60 percent of contractors in the bottom half of the income distribution, where contractor growth has been the fastest, receive the majority of their earnings through contracting.

The tax data also indicate that the industries with the greatest share of independent contractors (whether primary or supplementary earners) are “professional, scientific, and technical services,” followed by “other services” (e.g., repairing, grant-making, personal and pet care services, civic and religious service, etc.) and “health care.” All three industries have seen the greatest growth in the number of independent contractors since 2001. In the latest version of the “Contingent and Alternative Employment Arrangements—May 2017,” the Bureau of Labor Statistics reports that the industries with the greatest number of independent contractors engaging in this work as their primary form of income are in the “professional and business services” industry, followed by “construction,” and “other services.”

It’s worth noting that while Uber, Lyft, and DoorDash are ubiquitous in our everyday lives, workers at those type of online labor platform companies amount to only 8.6 percent of the overall independent contractor workforce. Furthermore, one of the IRS and Treasury reports concludes that this workforce’s exponential growth is “driven by individuals whose primary annual income derives from traditional jobs and who supplement that income with platform-mediated work.” For example, 96 percent of Lyft drivers are either students or those who work elsewhere, and 95 percent of them drive fewer than 20 hours per week.

Independent workers are therefore a wholly diverse set of people—spanning across different income brackets, industries, and roles as well as those who work as either primary or supplementary earners. This is partially why one-size-fits-all reclassification will be problematic—those efforts ignore the diversity of the independent workforce.

Why Reclassification Efforts Are Not the Right Approach

Worker reclassification policy efforts have sprung up in recent years with the emergence of platform-economy companies and concerns over misclassified “gig workers.” These policy efforts are often justified on the grounds that going after these large platform companies ensures gig workers receive proper benefits and protections. Regrettably, policy efforts that are aimed at gig workers specifically also impact the entire independent workforce more broadly, since all independent workers are legally classified as independent contractors.

As noted above, the gig economy workforce is less than 10 percent of the independent workforce and comprise almost entirely of workers who are supplemental earners on the platforms. Policymakers and regulators hope that by narrowing the definition of independent contractor, organizations will hire workers as employees instead of as independent contractors. At first glance, this change portends significant gains for workers who are reclassified as employees and receive proper benefits and protections. But there are reasons to doubt that independent workers will benefit from the restrictions.

-

Substantial Job Losses for Independent Workers. Many independent workers would not receive the additional benefits associated with becoming employees, because many of them would neither become employees nor be able to maintain their jobs as independent workers. This is because companies will not extend all contracting positions into employment positions, thereby leaving workers with fewer job opportunities altogether. For example, a recent report in Massachusetts finds that reclassifying app-based drivers “would result in a loss of at least 49,270 app-based [ridesharing] and [delivery] jobs in Massachusetts, which is equivalent to losing 58% of these earning opportunities in the state.” As we saw in the immediate aftermath of California’s AB5, businesses such as theaters, music venues, and small media organizations cut contracting jobs. It’s also worth noting again that because most independent workers, especially gig workers, are supplemental earners, reclassification efforts will not likely benefit them. They already have employment, and reclassification policies risks eliminating their “side” contracting jobs.

-

Fewer Options for Individuals Facing Income Loss. Independent work is an important source of income for those who face income loss and unemployment.26 Therefore, the loss of independent work opportunities would cause particular harm to these more vulnerable individuals.

-

Fewer Options for Majority of Workers Who Prefer Independent Work. According to the Bureau of Labor Statistics, a majority of independent workers (79 percent) prefer their nontraditional job arrangements over a traditional employment arrangement. Independent work provides far more flexibility in terms of work schedule, which gives workers more freedom to choose what time and how often to work. By contrast, traditional employment often means a specified schedule (e.g., nine-to-five) and a specified quantity of work (e.g., 48 weeks a year).

-

Disadvantage Women’s Employment Opportunities. Restricting independent work opportunities and reclassifying independent work as traditional employment would disadvantage women, many of whom tend to be the primary caregivers in their families and turn to independent work for the flexibility they need in their work schedules. Survey research reveals that 96 percent of women preferred to participate in independent work precisely because they need the flexibility in working hours.

-

Hamper Workers Who Had Contact with the Criminal Justice System. Restricting independent work would disproportionately harm the criminal justice population, because recent evidence shows that the gig economy provides an important avenue to work for those who previously had a criminal record.

-

Unduly Constraint Small, Innovation-Driven Technology Startups. Restricting independent work would harm small technology startups that rely on independent workers. In a survey of technology startup CEOs, 57 percent indicated that the use of contract labor is an indispensable or essential part of their business model, and 39 percent indicated that its highly valuable to their business models. Executives said that they required contract labor because they needed individuals with specialized talent or for one-off projects (69 percent) or because they needed flexibility, given the risk associated with early stage development (60 percent).

While reclassification efforts may benefit the smaller fraction of workers who prefer to be full-time employees and will be extended an employment opportunity, it would harm the majority of the independent workforce, especially women and individuals who previously had a criminal record.

A Better Way Forward: Flexible Benefits for a Flexible Workforce

To welcome the workers in a diversity of roles, who may value or require job flexibility and who are leading the way toward more creative and entrepreneurial ways of working, policy reforms are needed to pave the way for portable benefits. Indeed, 80 percent of self-employed workers would like flexible, shared, or portable benefits. These are benefits tied to the worker, rather than attached to an employer.

The fundamental problem is that by its very design, all workplace benefits are tied to only one form of work: the employment relationship. Current laws in the United States restrict organizations, businesses, and individuals from providing independent contractors with benefits precisely because these benefits—healthcare, retirement, vacation days, paid or sick leave, or parental benefits—have conventionally been tied to employer-employee relationships. If an organization were to provide benefits to their independent contractors, those workers would likely have to be reclassified as employees and thus lose their independence and flexibility.

Portable benefits, therefore, are becoming the best solution that allow workers to maintain the value of flexibility and independence while also having access to work-related benefits.

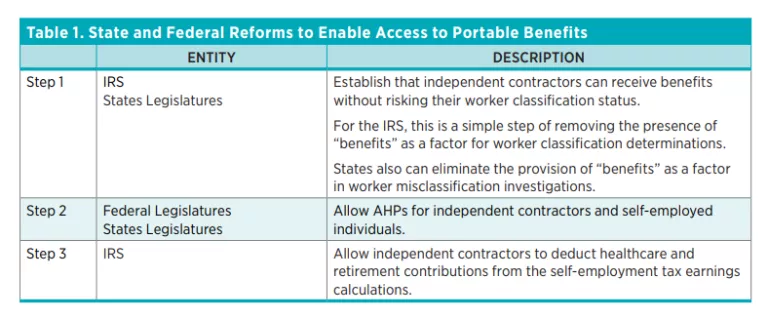

STATE AND FEDERAL REFORMS TO ENABLE ACCESS TO PORTABLE BENEFITS FOR INDEPENDENT WORKERS

To enable portable benefits solutions for independent workers, current regulatory and legal barriers need to be removed. Table 1 provides a summary of the simple steps that federal and state governments can take to eliminate these barriers.

Step 1: Reform Federal and State Laws to Establish that Independent Contractors Can Receive Benefits without Risking Their Worker Classification Status

The IRS uses a 20-factor common-law test as their basis for determining whether a worker is an employee or a contractor. One factor, the “type of relationship,” looks in depth at the employer-employee or employer-contractor relationship. The IRS points to the presence of “benefits” as one indicator of an employer-employee relationship rather than an employer-contractor one.The IRS says specifically:

"Employee benefits include things like insurance, pension plans, paid vacation, sick days, and disability insurance. Businesses generally do not grant these benefits to independent contractors."

This prevents and discourages organizations or clients from giving benefits to independent contractors with whom they work. Indeed, several companies have already indicated that they want and are ready to give benefits to independent contractors, conditional on the law allowing them to do so. Lawyers also advise companies not to provide benefits to their independent contractors for this reason. Therefore, the first step to improve access to portable benefits is for the IRS to establish that benefits for independent contractors should not be used to determine a worker’s classification status. In other words, organization should be free to provide benefits to their independent contractors without the risk of them being reclassified as employees. This would be a simple fix: merely remove the presence of “benefits” from the factors in the employee and independent contractor classification tests. In that case, companies, organizations, and clients of independent contractors could contribute funds or provide benefits without additional tax consequences.

Each state law also has its own determinations for whether a worker should be considered an employee or independent contractor. States can pass similar reforms to establish that, under state law, independent contractors are free to receive benefits from companies or clients without risk to their independent contractor status. This is the primary step that states could take to enable a flow of benefits to independent contractors.

Step 2: Reform State and Federal Laws to Allow Association Health Plans for Independent Contractors and Self-Employed Individuals

Under federal law, small-business employers and self-employed workers cannot join together to purchase health insurance as a large group, though there is one limited exception for small businesses commonly known as “Pathway 1 AHPs.” This exception means that an AHP that covers small-business employers could be considered a large group health plan if “the employers were bound together by a common interest beyond health coverage and effectively operated as a one employer controlling the association.” Employers in this group are required to share a common trade, business, or profession—shared geographic location is not enough.

It is important to emphasize that this exception only applies to small businesses. It does not apply to individual self-employed workers or independent contractors, because an association of individuals cannot be considered as a “single employer.” Therefore, under federal law, there is no real pathway for independent workers to join together as an association for the purposes of buying health insurance. Reforms commonly referred to as “Pathway 2 AHPs” would enable small businesses and self-employed workers (without their own employees) to join together under a “commonality of interest,” including any broadly defined common geography.

In 2018, the DOL issued a rule that expanded the definition of “employer” for the purposes of AHPs to include self-employed individuals, independent contractors, freelancers, and gig workers. The DOL stated that “Association Health Plans work by allowing small businesses, including self-employed workers, to band together by geography or industry to obtain healthcare coverage as if they were a single large employer.” However, a federal court voided this rule after years of legal challenges. Therefore, reform in this area would likely need to come from federal legislatures, rather than as a regulatory rule change from agencies.

Similarly, states can also provide reform by enabling Pathway 2 AHPs under state laws. There are currently at least seven states that have enabled some aspects of Pathway 2 AHPs. In North Carolina and Florida, for example, the laws allow small businesses (even those that do not have their own employees) to offer health plans based on shared geography and industry. While there is some uncertainty regarding how federal enforcement will impact state laws, states could move forward nonetheless by allowing AHPs under their own state laws.

Step 3: The IRS Could Allow Independent Contractors to Deduct Healthcare and Retirement Contributions from the Self-Employment Tax Earnings Calculations

Under current tax laws, an employer’s contributions to an employee’s retirement plan or health insurance are deductible from the employer’s business income and are not subject to federal payroll taxes for either the employee or the employer. But workers who are independent contractors face unequal tax treatment. If an independent contractor deposits the earnings they receive from a company into a tax-deferred retirement account, they will still have to pay federal payroll taxes on that contribution (although they can deduct the contribution from their federal income tax).

An example from researchers Michael Mandel and Alec Stapp can be illustrative here. If an independent contractor is paid $1,000 from a company and their marginal federal income tax rate is 22 percent, they end up paying about 13 percent tax on the $1,000 used toward benefits, rather than 0 percent as salaried employee. This means that an independent contractor is effectively penalized for their retirement savings. Similarly, if an independent contractor uses their earnings to pay for health insurance, they must still pay federal payroll taxes on those earnings (although they can deduct the cost of the health insurance from their federal income taxes). As is the case for the retirement contributions, an independent contractor pays about 13 percent on the $1,000 payment from a company used to purchase health insurance coverage. In contrast, if an employer contributes to a health insurance plan for the employee, that amount is exempt from federal payroll taxes (within limits).

To put independent contractors and employees on a more equal footing, the IRS should allow independent contractors to deduct healthcare and retirement contributions from the self-employment tax earnings calculations.

HOW PORTABLE BENEFITS CAN BE IMPLEMENTED

There are a multitude of ways to design and implement a portable benefits program. The Aspen Institute’s Future of Work Initiative has been at the forefront of research on designing portable benefits solutions. In one of their reports, they provide a summary of the different types of portable benefits plans that already exist either in the United States or elsewhere in the world. For example, the Black Car Fund in New York established a fund for livery and for-hire vehicle drivers (all of whom are independent contractors) to receive workers’ compensation. The statute requires that 2.5 percent of every taxi and for-hire vehicle ride be allocated to this fund.

In another report by the Aspen Institute, the authors build a framework for thinking through different types of portable benefits plans. The framework introduces four components that matter for portable benefits plans:

- Who administers it?

- Who pays for it?

- Is it mandatory?

- Who is eligible?

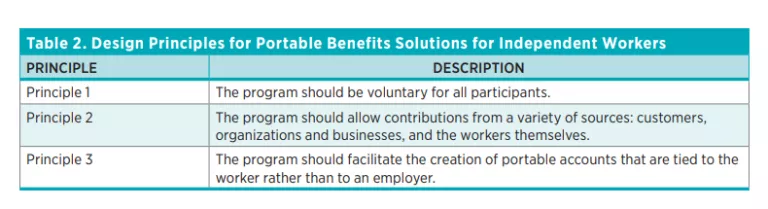

Overall, the comprehensive guide provided by the Aspen Institute casts a wide net of possibilities for what various types of portable benefits could look like. This policy brief uses their broad framework and goes beyond it to provide the specific design principles that would maximize potential benefits for independent workers while also minimizing the costs on society, especially on small-business owners, and avoiding any unintended consequences that may emerge from making a portable benefits system mandatory. Table 2 presents an outline of the three design principles that can guide policymakers and industry leaders in their approach when implementing portable benefits program.

Principle 1: The Program Should Be Voluntary for All Participants

Over 99 percent of businesses in the United States are considered “small businesses” (with under 500 employees), and 88 percent of these small businesses have fewer than 20 employees while more than half (56 percent) have one to four employees. Many of these small businesses are not highly profitable, and nearly 40 percent make less than $100,000 in revenue. Many small business owners come from immigrant or low-income backgrounds, and most of them, since they are self-employed, do not have access to common-workplace benefits that are tied to employment. A requirement that businesses must provide benefits for freelancers and independent contractors may thus unduly burden these small businesses and other resource-constrained organizations such as small nonprofits. Even a temporary exemption for small businesses may not address the challenges, because the vast majority of them remain small for most of their existence. Furthermore, it’s important to note that individuals also work with independent contractors—for example, an ordinary American household may hire a contractor electrician or plumber.

Moreover, requiring businesses to provide mandatory benefits privileges larger companies that have the resources to do so and harms potential entrants into the market. Quasi-portable benefit programs that require transportation and delivery companies to provide mandatory benefits to independent contractors may result in fewer competitors for these larger companies because the requirement raises the costs of entry.

The program should be voluntary for the workers as well because the majority of independent contractors are supplementary earners and may already have access to workplace benefits from their full-time employment. For example, as noted above, 55 percent of Lyft drivers have a traditional job and 95 percent of them drive fewer than 20 hours per week. This is the case for most other gig-economy platforms, including Uber and DoorDash.

Removing the legal barriers should be the priority. It’s the most simple, low-hanging-fruit solution that would at least open up the pathway for organizations, individuals, and businesses to provide a “menu of benefits”—for example, some organizations may provide one or two sets of benefits whereas others, especially larger companies, may provide a more complete set of benefits. It is true that this type of voluntary programs means that not all organizations will provide benefits to all their independent contractors. However, because independent contractors often receive income from a variety of different clients and organizations, the voluntary nature of the program may mitigate this problem.

Principle 2: The Program Should Allow Contributions from a Variety of Sources: Customers, Organizations and Businesses, and the Workers Themselves

Allowing contributions from different sources can maximize the amount that each individual independent worker receives without placing excessive burden on one party to provide everything. Platform companies, small businesses, and organizations can each implement this in different ways.

For example, Upwork, a freelancer platform, can facilitate contributions from three parties in the following way: It can set up a 5 percent “fee” that will go into a benefits fund (a specific or general fund) for the independent worker. Of that fee, 2.5 percent will be paid by the platform, and 2.5 percent will be paid by the client or customer who is hiring the independent worker. It is not uncommon to have a fee for the payer. Airbnb charges each customer a standard service and cleaning fee. The Black Car Fund in New York charges a 2.5 percent mandatory tax to customers for each taxi or ridesharing transaction (the fund is only for drivers and only for workers’ compensation insurance). The third payer could be the independent workers themselves, and larger companies can set up various “matching contributions” plans to encourage greater savings. Tax incentives, as described above, also could help to encourage independent contractors to contribute to these funds.

Another example is that a third-party company could work with independent workers to set-up either a general account or a specific account (e.g., retirement, health savings). The independent worker could then provide that account to any client or organization with whom they work. A client or organization could make contributions to that account on behalf of the independent worker—whether as a flat fee or a transaction rate. Moreover, the independent worker could request and specify their own fee or rate for any client or organization.

However the program is implemented, the importance here is to allow for a variety of shared ways to pay for the benefits. Independent workers will have different relationships with their clients and organizations. Some will contract with only large companies and have access to a more desirable and wider set of benefits, perhaps partially paid for by the companies themselves, whereas others may contract with only households or small-business owners and therefore have fewer benefits.

Principle 3: The Program Should Facilitate the Creation of Portable Accounts That Are Tied to the Worker Rather than to an Employer

Benefits programs for independent workers should be portable, which means the benefits should be tied to the worker and not to the organization or employer. The benefits should travel with the worker—whether they go from one client to another or from one platform company to another. For example, these accounts could look like an individual retirement account (IRA) or a health savings account (HSA), where the accounts are tied to the worker regardless of where they work and different companies are allowed to contribute to these funds.

The reason it is foundational to have accounts tied to the worker is because most self-employed workers change work often and contract with many different businesses and clients at one time. It would be counterproductive to have benefits tied to a specific organization, like health insurance is for employees. Precisely because an employment relationship is often long-term and a contractual relationship is often short-term, it would impose significantly greater costs on independent workers to have to change their benefits every time they change a client or an organization.

Many different types of benefits could be made portable for independent workers. For example, maternity leave or sick paid leave benefits could be tied to an individual worker—like an IRA or an HSA account—rather than to one particular employer. This would mean that different companies, organizations, and clients could contribute to one maternity leave account for one independent worker, administered by a third party, and that the worker could access that account whenever they need to take maternity leave. This would be especially beneficial to women who self-select into independent work and out of employment because of childcare or other obligations, because they would still have access to maternity leave benefits.

CONCLUSION

Flexible forms of work are beneficial and are desirable opportunities for a large set of working Americans. We should embrace and welcome the reality that many Americans choose and prefer these types of nontraditional work arrangements. At the same time, we need to fix the shortcomings that exist in these flexible work arrangements—for example, workers do not have access to benefits afforded to traditional employees. These limitations have led to policy battles across states and on the federal level. These tensions are arising because our system prioritizes the immobility of benefits (e.g., healthcare being tied to one employer) in a world where worker preferences have shifted and more value is placed on choice and portability. Indeed, a survey found that 80 percent of self-employed respondents would like access to flexible or portable benefits—benefits that are not tied to a particular job or employer.

To better meet the needs of the growing independent workforce, federal and state governments could take the simple and small steps outlined here to reform laws that would enable independent workers to have access to benefits. Embracing innovative policy reforms will create a fairer system for all workers—both employees and self-employed workers.