- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

What Happens When Governments Pay for Spending with Money Creation? Lessons from the Early Riksbank

In recent years, Modern Monetary Theory (MMT) has received greater attention in both the popular press and in the public debate over deficit spending and the level of government debt. The basic idea at the core of MMT is as follows:

The monetarily sovereign government is the monopoly supplier of its currency and can issue currency of any denomination in physical or non-physical forms. As such the government has unlimited capacity to pay for the things it wishes to purchase and to fulfill promised future payments, and has an unlimited ability to provide funds to other sectors. Thus, insolvency and bankruptcy of this government is not possible. It can always pay.

Although this statement is true by definition, it does not necessarily provide a useful guide for thinking about paying for government spending. Before a government makes plans to pay for its expenditures or repay what it has borrowed with money creation, it should carefully consider the consequences of doing so.

It is largely uncontroversial to assert that a government with its own currency never has to default on its debt and can always spend. However, from this observation, MMT draws the implication that the government has no actual budget constraint. To the extent that one can write down a government’s budget constraint, the equation is simply an accounting identity of how government spending was financed. In other words, since money can be printed in unlimited quantities, this should not be considered a constraint.

Advocates of MMT seem to view the absence of a government budget constraint as a logical extension of the fact that states with their own currency can always simply print new currency to meet the government’s obligations. For example, ignoring government borrowing, the government budget constraint can be written as

where G is government spending, T is tax revenue, and delta C is the change in the supply of currency. The claim made by MMT advocates is that since the government can make Change in C whatever it likes, this is not a constraint in any meaningful sense. Any budget deficit, G - T > 0, can simply be financed by increasing the supply of currency. Any budget surplus, G - T < 0, simply results in a reduction in the supply of currency.

Whereas the logic is straightforward, this claim is based on writing the government’s budget constraint in nominal terms. Typically, economists care about real allocations, which depend on the purchasing power of the money spent. In other words, it is fine to say that the government can always buy $1 million worth of tanks for the military because it can, if need be, print $1 million to pay for the tanks. But the important question is how many tanks that $1 million can buy and whether printing 1 million new dollars instead of collecting it in taxes affects the number of tanks (and other goods) the government can purchase.

The fact that a government has the ability to pay for what it wants by printing the currency necessary to pay for it is both uncontroversial and uninteresting. The fact that the government can print currency to pay for things does not reveal anything about the macroeconomic effects of printing currency to pay for things or whether the government should print currency to pay for things.

To ignore this point is to ignore a vast literature within macroeconomics. Advocates of the Quantity Theory of Money, for example, argue that increasing the supply of currency without any change in the demand to hold currency would, at least in the long run, cause an increase in the price level. Advocates of the fiscal theory of the price level argue that, in the absence of any change in the expected discounted value of future primary surpluses, an increase in the supply of currency would similarly lead to a higher price level.

What each of these theories suggest is that there can be macroeconomic consequences to paying for expenditures with newly issued currency. In fact, there is a large literature in economics on optimal seigniorage revenue. The purpose of this literature is to determine the maximum amount of real revenue that the government can receive from money creation and at what rate of inflation this maximum amount of revenue is achieved. This literature explicitly recognizes that the government can pay for things by printing the money. However, it also recognizes that the extent to which money creation can generate more real revenue depends on the macroeconomic effects of money creation.

Others, going back at least to the work of Earl Thompson and Robert Barro in the modern literature, have raised questions about whether there is any difference between financing government spending with taxes and financing government spending with borrowing. Again, this literature examines the overall effect of government debt issuance in comparison with taxes. One can think of this literature as examining whether it matters how the government pays for its spending.

It is not entirely clear where MMT fits within the context of this literature. Advocates of MMT are dismissive of Quantity Theory–type arguments, saying that printing money “supposedly causes inflation.” At the same time, MMT suggests that inflation is caused by real constraints:

Inflation is a real constraint not a financial constraint, so inflation does not prevent the government from funding itself—as such the capacity of the government to fund itself is independent of the state of the economy. Indeed, as the currency-issuer, government can always outbid the private sector, which certainly is a concern of MMT. At full employment, increasing government spending will certainly be inflationary; before full employment government can cause bottlenecks and inflation of prices of key inputs.

Placed in this context, it is hard to determine what makes MMT unique. As I state earlier, few would deny that a government with its own currency can always print money necessary to pay for its expenditures. The relevant questions are about what happens when it prints money to pay for things and whether it is a good idea.

Furthermore, this articulated view of the relationship between government spending, money printing, and inflation is fairly conventional. Even the crudest version of the Quantity Theory of Money states that in the long run (at full employment), real economic output is determined by real factors. As such, an increase in the growth rate of the money supply (for any reason, including to pay for government spending) results in inflation. In addition, quantity theorists argue that to the extent that there is an excess demand for money and money-like assets during a recession (when employment is below full employment), an increase in the money supply is not inflationary and is actually stabilizing for economic output.

Similarly, this description of inflation sounds perfectly consistent with Keynesian arguments, both old and new. The centerpiece of Keynesian analysis of inflation is the Phillips Curve. According to this view, the inflation rate declines when employment falls below full employment, and the inflation rate rises when employment rises above full employment. Thus, full employment and real constraints are central to this theory of inflation as well.

Nonetheless, regardless of whether MMT has anything unique to say about the government budget constraint or inflation, it does raise an interesting question: What would happen if the government were to decide to finance its spending by printing money? Rather than trying to answer this by comparing and contrasting different theories and engaging in arguments over semantics, it might be useful to try to answer this question by appealing to actual experience and evaluating the evidence. History provides a unique example. In the mid-1700s, the Swedish parliament controlled both the budget and the Riksbank (Sweden’s central bank). This effectively consolidated monetary and fiscal policy into one decision-making process. It is therefore of some value to consider what happened when Sweden tried to finance government expenditures with money creation.

The Swedish Experiment

Following the death of King Karl XII in 1718 and Sweden’s loss in the Great Northern War, there was uncertainty about who would take over the throne. The king had left no heirs. The king’s sister, Ulrika, negotiated her own ascension to the throne with the Swedish Riksdag (parliament). However, this negotiation resulted in a new constitution that concentrated power within the Riksdag rather than with the crown.

The Riksdag consisted of four estates: nobles, burghers, clergy, and peasants. The only taxes that were allowed to be permanent were those that existed before the new constitution. However, the Riksdag could implement temporary taxes. Tax policy was determined by a tax committee that had representatives from each estate. Issues related to government expenditures, as well as monetary policy and foreign policy, “were considered secret state matters.” These policies were determined by the Secret Committee that consisted of 100 members of nobles, burghers, and the clergy in the Riksdag. These changes effectively consolidated monetary and fiscal policy within the Riksdag.

The period from 1719 until 1772 is referred to as the “Age of Freedom.” The first two decades of this period witnessed relative stability and peace. However, the period from 1739 to 1772 saw a considerable conflict of visions between two political parties known as the Hats and the Caps.

The Hats took over control of the government in 1739. In 1741, the Hats tried to capitalize on the uncertainty in Russia over who would ascend to the throne following the death of the Russian empress. Their objective was to regain land lost during the Great Northern War. Ultimately, however, the Hats’ Russian War was a failure. In 1745, in large part because of the money creation during the war, the government suspended the convertibility of bank notes indefinitely.

What made the period after 1745 particularly interesting was the Hats’ use of monetary and fiscal policy under this consolidated regime with inconvertible paper money. The Hats sought to increase economic activity through a variety of policies. These included direct subsidies to manufacturers, export subsidies, and the construction of roads and canals. The Hats used the Riksbank to give loans directly to firms. The Riksbank also lent directly to the government to finance spending. The increased lending on the central bank’s balance sheet resulted in a corresponding increase in note issuance. Given the consolidated nature of the government’s balance sheet, this meant that government spending was effectively paid for with money creation.

There is some evidence that the Hats believed that using money creation would be expansionary, although there are differing views on exactly what their precise ideas were. Nonetheless, one thing is clear: the Hats thought that financing expenditures with money creation would be expansionary for the economy, and they denied that doing so would result in inflation. The Caps, conversely, argued that the increase in the supply of bank notes would cause inflation.

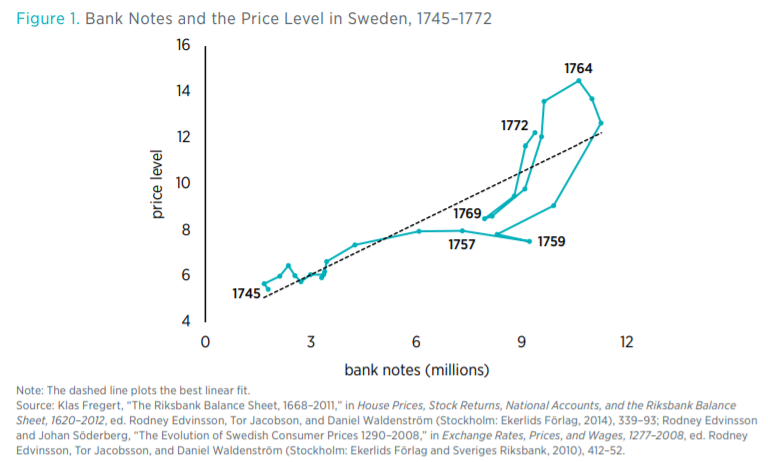

Given this background, this historical example seems useful for addressing the macroeconomic effects of financing government expenditures with money creation. Figure 1 plots the supply of bank notes and the price level. As shown in the figure there is a clear positive relationship between the supply of bank notes and the price level over this period. The one exception appears to be during the years 1757 to 1759, when Sweden entered the Pomeranian War. The fact that real money balances rose substantially at the beginning of the war might have been the result of an expectation that the money creation used to pay for the war was only temporary and that the money supply would return to its previous trend at the end of the war. Regardless, the evidence from figure 1 suggests that the increase in bank notes issued by the Riksbank was associated with higher prices. Thus, though the government was able to continue to pay for its spending, the evidence suggests that the result was higher prices.

Critics might argue that I am extrapolating too much from a scatterplot. Economists are concerned with counterfactuals, after all. I have two responses to this critique. The first concerns the scatterplot itself. The Hats remained in power until 1765 when the Caps took over. The Caps were elected in large part because of the backlash against the Hats caused by inflation. When the Caps took power, they immediately reversed course and started contracting the money supply. The resulting costly deflation was enough to bring the Hats back to power in 1769. A coup d’état restored the monarchy in 1772.

Given this understanding of events, the scatterplot does a remarkable job illustrating the changes in policy regimes. As figure 1 shows, the reversal of policy is coincides perfectly with the change in the party in power. When the Hats are in charge, the supply of bank notes and the price level rise together. When the Caps take power in 1765, the line graph immediately begins retracing its steps as the supply of bank notes and the price level each decline. Then, when the Hats retake power in 1769, the line graph begins retracing its steps yet again, with money and prices moving higher once more. In other words, money and prices not only move together, they do so in a way that is consistent with changes in the policy regime and marked turning points.

My second response is that more sophisticated statistical analysis of this period largely tells the same story as the scatterplot. Nils Herger, for example, finds that monetary factors explain the rising inflation. Furthermore, in my own work, I have found no evidence that the increase in the supply of bank notes had any effect on real economic activity.

Overall, the evidence suggests that the primary effect of using money to finance government expenditures appears to be higher prices.

Conclusion

Recently, MMT has gained some degree of popularity, as evident by its inclusion in public discussions about government budget deficits and debt. Unfortunately, much of the discussion about MMT often ends up mired in disputes about what MMT really says or debates over semantics.

Nevertheless, MMT does raise an interesting question: Given that a government with its own currency could pay for its expenditures through money creation, what would happen if the government were to do so? Rather than debate theoretical and semantic points, I have pointed to a historical example in which the decision makers chose to finance some amount of government expenditures through money creation. Like advocates of MMT, those decision makers also denied that doing so would be inflationary. The historical record suggests otherwise. Financing these expenditures through money creation was inflationary.

Just because the government can pay for its expenditures with money creation does not necessarily mean that it should. Like all decisions, the decision to pay for expenditures with money creation requires that policymakers navigate a tradeoff, one that is well-known in the literature on optimal seigniorage. Perhaps there is nothing new under the sun, after all.