- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

What Would Milton Friedman Say about Financial Stability?

This policy brief is part of a Mercatus Symposium titled “What Would Milton Friedman Say?” The symposium explores what the late Nobel laureate, economist Milton Friedman, might say about monetary policy today, as the Federal Reserve grapples with increasing inflation in the wake of the COVID-19 pandemic.

Since the passing of Milton Friedman in 2006, there have been two significant financial crises that hit the US economy: the Great Financial Crisis of 2007–2009 and the pandemic-caused financial crisis of 2020. If Friedman had been alive and experienced these events, what lessons might he have drawn about financial stability?

This question is an interesting one, but it requires some speculation. Fortunately, Friedman had a lot to say about previous financial crises and their implications for policy. So we have some basis from which to make reasonable conjectures about the lessons Friedman would have drawn from these two recent financial crises and what they mean for future financial stability concerns.

Two broad principles, in particular, emerge from Friedman’s work that speak to financial stability concerns. First, he believed a stable monetary policy regime would lead to stable nominal income growth and, in turn, support financial stability. Second, he wanted banks and other moneycreating institutions to be robust to economic shocks so that they do not cause fluctuations in the money stock and, in turn, nominal income.

This paper will use these two principles to consider how Friedman would have seen and interpreted the recent financial crises. Specifically, the case will be made that Friedman probably would have viewed the 2007–2009 crisis as a time when his principles were not closely followed, whereas in the 2020 crisis they were followed but to an excess. The paper also will argue that Friedman most likely would have promoted a general application of his principles as the best way to deal with the potential financial stability challenges that lay ahead.

Before these arguments can be made, though, a closer look of Friedman’s two principles of financial stability is covered next.

THE FIRST PRINCIPLE OF FINANCIAL STABILITY

Friedman’s first principle is that a stable monetary policy regime will lead to stable nominal income growth and, in turn, support financial stability. To see why, recall that Friedman for most of his career believed stable growth in the money supply was necessary for a stable monetary regime. Friedman also believed that if the Fed kept money growth stable, the rate of use or “velocity” of money would be stable too. For example, in testimony before Congress, he said, “If you keep the money supply fairly steady, the historical records suggest that the changes in velocity are rather moderate. . . . On the average, velocity tends to move in the same direction as the quantity of money.” This understanding meant that nominal income—the product of the money supply and velocity—would be stable if the Fed kept money on a stable growth path.

Friedman, therefore, viewed stable nominal income growth as a sign of a stable monetary regime and came to see “the broadest framework . . . of the work that I and others have done in analyzing monetary experience” as a “theory of nominal income.” This framework is why Friedman advocated a money-supply target rather than an inflation target for most of his career. He believed that the “relation between changes in the nominal quantity of money and changes in nominal income is almost always closer and more dependable than the relation between . . . changes in the quantity of money per unit of output and changes in prices.” The Fed, he believed, could more easily control nominal income than inflation.

Nominal income, in turn, mattered for financial stability for three reasons. First, because of sticky output prices, “real income tends to vary over the cycle in the same direction as money income.” Swings in nominal income, therefore, lead to similar movements in real economic activity that directly affect the health of the financial system.

Second, most debt contracts, like mortgages and leases, are denominated in fixed nominal terms. As a result, borrowers must make forecasts of their nominal income when entering such sticky nominal debt contracts. Financial stability, consequently, requires those expectations to be realized through stable nominal income growth.

Third, stable nominal income growth creates better risk sharing between debtors and creditors. The basic idea here is that a stable nominal income growth path means any unexpected changes in inflation will come from supply shocks and be countercyclical. This will cause real debt burdens to move in a procyclical manner and benefit debtors during recessions and creditors during booms. Fixed nominal debt contracts will act more like equity than debt and therefore promote financial stability.

As noted above, though, Friedman believed the Fed targeting the money supply was the best way to create stable nominal income growth. Modern central banks, however, no longer look at money supply targets but at interest rate targets and, when at the zero lower bound, large-scale asset purchases (LSAPs). A practical reframing of Friedman’s first principle, then, would be a monetary regime that successfully promotes stable nominal income growth through the appropriate use of its interest rate target and LSAPs. Friedman saw the natural interest rate as the appropriate value for setting the interest rate target and believed that over the long run, it was shaped by nonmonetary forces. He also endorsed the use of LSAPs in Japan in 2000 as a way to get off the zero lower bound and restore macroeconomic stability. Friedman, ultimately, would want both tools used to promote nominal income growth stability, his first principle for financial stability.

THE SECOND PRINCIPLE OF FINANCIAL STABILITY

Friedman’s second principle for financial stability is that banks and other money-creating institutions should be robust to economic shocks so that they do not cause fluctuations in the money stock. Friedman believed his first principle, outlined above, should be sufficient in most cases for maintaining money stability, but he also recognized that credit markets are susceptible to nonmonetary shocks. Consequently, he thought it appropriate to have policies that keep such shocks from spilling over into the money supply and nominal income.

Friedman favored 100 percent reserve banking for most of his career as the ideal policy to ensure this outcome. However, he understood this idea was radical and unlikely to be adopted, so he took a more pragmatic approach that included the championing of deposit insurance, bank capital, and bailouts in certain circumstances.

Friedman especially liked deposit insurance and saw it as “contributing so greatly to monetary stability . . . far more than the establishment of the Federal Reserve System.” He held this favorable view of deposit insurance over his entire career. On bank capital, he noted that “a substantial equity cushion” not only gives banks a shock absorber but also provides “ample incentives to avoid excessive risk.” Finally, Friedman believed that official recapitalization of banks was okay if the entire banking system was in distress or if there would be a systemic run on the financial system in the absence of the bailout. That is why he supported the work of the Reconstruction Finance Corporation in the 1930s, the rescue of the large commercial bank, Continental Illinois, in 1984, and backstopping banks during the 1987 stock market crash. In general, Friedman thought bailouts were warranted when “the benefits of increased financial stability outweighed concerns about moral hazard.”

Friedman viewed these policies, some of which required increased government intervention, as a means to guarantee a stable money supply and, in turn, stable nominal income growth that supported financial stability.

THE FINANCIAL STABILITY PRINCIPLES APPLIED TO THE RECENT FINANCIAL CRISES

Based on these financial stability principles, how would Friedman have viewed the Great Financial Crisis of 2007–2009 and the pandemic-caused financial crisis of 2020? In both crises, the Federal Reserve pushed its interest rate target to zero percent as the natural interest rate fell and aggressively used large-scale asset purchases. Various forms of backstops to the banking and shadow banking systems were also used in both crises, including the Fed’s emergency liquidity facilities and the temporary facilities created by Congress like the Troubled Asset Relief Program (TARP) and the Paycheck Protection Program (PPP). Financial policy also began requiring more capital funding for banks. On the surface, then, it might appear the government’s response to both crises followed Friedman principles for financial stability. A closer look, however, reveals a different conclusion. Friedman probably would have seen his principles as not being closely followed in the 2007–2009 crisis. Conversely, he would have seen them as being followed more closely in the 2020 crisis.

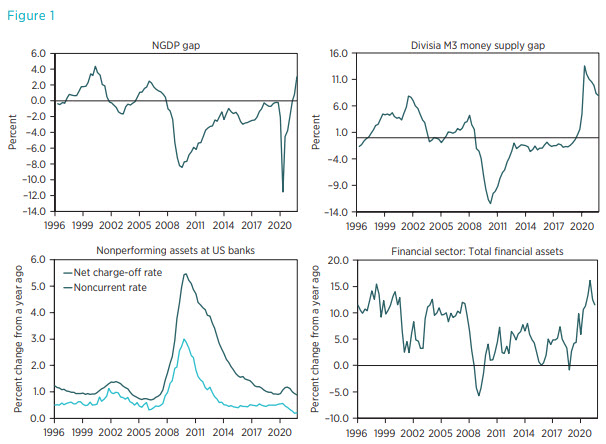

This interpretation finds support in the actual growth path of nominal income, Friedman’s defining measure for thinking about financial stability. Since nominal income equals nominal GDP, the top-left chart of figure 1 shows one way to see this outcome, the nominal GDP gap. This measure shows the percent deviation of nominal income from its expected growth path and reveals that it collapsed relative to expectations in the 2007–2009 crisis and only slowly recovered. During the 2020 crisis, it also fell sharply relative to expectations but then quickly recovered and overshot expectations. The slow recovery of the nominal GDP gap after of 2007–2009 crisis versus the quick recovery after the 2020 crisis indicates the latter period more closely followed, though to an excess, the Friedman principles for financial stability.

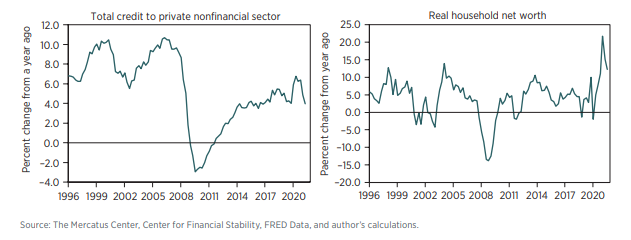

This interpretation is corroborated by the other charts in figure 1. The top-right chart in the figure shows the Divisia M3 money supply gap. This chart shows the percent deviation of this broad measure of the money supply from the path needed to keep nominal income on a stable growth path given trend velocity. It provides a useful cross-check on the stance of money policy. This measure also collapses in the 2007–2009 crisis but vastly overshoots in the 2020 crisis. Similar patterns are seen in the growth of nonperforming bank assets, the growth of financial assets issued by the financial sector, the growth in credit to the private nonfinancial sector, and the growth of real household net worth. They all indicate that financial conditions were very tight in the 2007–2009 crisis but much easier during and after the 2020 crisis. These outcomes are consistent with the quicker recovery in nominal income in the latter crisis.

The difference in nominal income stability and therefore financial stability for these two periods can be traced to three developments. First, the Federal Reserve eased monetary policy much slower in 2007–2009 than in 2020. The Fed cut interest rates from 4.5 to 2.0 percent between September 2007 and April 2008, but then it sat on 2.0 percent through October 2008 and signaled it may raise rates because of inflation concerns. It did not start LSAPs until November 2008 and finally got to a zero percent interest rate target in December 2008. This waiting period was deadly to the economy and crushed nominal income. It all but guaranteed that what probably would have been a garden-variety recession got turned into the Great Recession. By contrast, the Federal Reserve in 2020 got to a zero percent interest target in a month and quickly started LSAPs. Unlike 2008, there was no hesitancy in 2020 that could have harmed nominal income.

The second development behind the robust recovery of nominal income was that the Fed adopted a new framework in 2020 called flexible average inflation targeting. This new framework allows the Fed to do “makeup” policy, which in terms of nominal income means the Fed was empowered to return nominal income to its pre-pandemic expected growth path. The Fed did not have the flexibility during the Great Recession.

The final development was that the Federal Reserve got to implement its new framework with a strong tailwind coming from fiscal policy. Multiple rounds of stimulus checks, enhanced unemployment benefits, and the PPP all amounted to a large “helicopter drop” of money to the public over the 2020–2021 period. This fiscal policy tailwind supported nominal incomes and, in particular, personal incomes.

These three developments are why nominal income was quickly restored in 2020 and financial stability better preserved than in the prior crisis. They are also why, however, nominal income overshot its expected growth path in late 2021 and is likely to do so in the first half of 2022. In hindsight, there was too much nominal income support in 2021.

Still, the fact remains that over the 2020–2021 period, a policy-generated growth in nominal income kept the US financial system from experiencing a large systemic crisis. The causality in this case clearly runs from robust nominal income growth to financial stability. One can make a similar case, but in the other direction, for the 2008 period. Then, monetary policy caused nominal income to fall amid an already weakened economy and helped spawn the Great Financial Crisis. A recent study provides evidence on this latter view by looking at 11 advanced economies over the 2008–2013 period and finds causality running from nominal income to financial stability. Figure 2 replicates some scatterplots from this study that show reduced form evidence linking nominal income (NGDP) forecast errors to financial indicators.

Friedman, in addition to distinguishing between the 2007–2009 and 2020 financial crises, probably would have reiterated the more general point that macroeconomic policy that strives to keep nominal incomes on a stable growth path and is complemented by financial policies of appropriate backstops for money-creating institutions and ample bank capital will make it far less likely that a major financial crisis will emerge. These policy recommendations are considered next in light of future potential financial crises.

THE FINANCIAL STABILITY PRINCIPLES APPLIED TO FUTURE POTENTIAL CRISES

So how would Friedman think about dealing with potential financial crises given his principles for financial stability? He probably would make two points. First, he would argue for simplicity. He was a longtime advocate of simple monetary policy rules, and it seems reasonable to assume he would similarly suggest simple rules for financial stability that could easily be applied across different financial firms. Second, Friedman would care about maintaining the political legitimacy of rules and regulations for financial stability. In particular, he would probably subscribe to Paul Tucker’s legitimacy argument that any major financial stability policies coming from the Fed or other regulators should have the support of a majority of the population. Otherwise, the Fed and other agencies risk being politicized and losing their legitimacy among the body politic.

To see how these points might look in practice, consider the growing financial stability concerns over climate change. The Friedman principles and points outlined above would lead him to be leery of the current approach being taken by the Federal Reserve on this issue. The Fed has been considering moving in the direction of policies specifically designed for climate change risk, such as climate stress tests and the greening of credit, collateral, and asset purchases in monetary policy. The Fed has already set up two committees on climate changes—the Supervision Climate Committee and the Financial Stability Climate Committee—and has joined the Network for the Greening of the Financial System.

Friedman would question all the attention being given to climate change by the Fed when there are other risks that could be seen as equally or more problematic for financial stability. For example, why not worry about other slow-moving changes that will adversely affect asset values such as the US population growth decline or the long-term productivity slowdown? Also, why not focus on other existential threats like a nuclear war, asteroids, solar flares, or pandemics that have a bearing on financial stability? The COVID-19 pandemic and the RussiaUkraine war are stark reminders that there is a plethora of potentially large shocks that could harm financial stability.

So why not use a more general financial stability approach that can be applied to these different potential challenges? Specifically, Friedman would probably call for more capital funding for banks overall rather than focus on specific risk like climate change. Also, as noted above, he would probably recommend a monetary policy regime that promotes nominal income stability and therefore provides financial stability support against all these potential challenges. This is keeping it simple.

On political legitimacy, Friedman would be worried that the Fed’s focus on climate change and the greening of monetary policy would be seen by half the body politic as the politicization of the Fed and undermine its independence. Whereas the Fed addressing climate change is not a consensus view among Americans, the Fed addressing financial stability concerns more generally is one. The latter, therefore, would have legitimacy and could be implemented by the simpler policies such as increased capital funding for banks and stable nominal income growth.

CONCLUSION

Milton Friedman viewed financial stability issues primarily through the lens of nominal income and the money stock. He believed that if both were kept on a stable growth path, then financial stability would follow in most cases. As a result, he likely would have viewed the Great Financial Crisis of 2007–2009 when nominal income and the money supply crashed as a policy failure. Conversely, he would have seen the rapid recovery in nominal income and the money supply after the pandemic-caused financial crisis of 2020 as a success but also seen its extension into 2021 as excessive. Finally, Friedman would have advocated for the Fed to take a simple but general approach, such as increased capital funding and stable nominal income growth, to the many potential future financial risks.

Citations and endnotes are not included in the web version of this product. For complete citations and endnotes, please refer to the downloadable PDF at the top of the webpage.