- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

Principles for Climate-Related Financial Risk Management for Large Financial Institutions

Federal Reserve Board of Governors

Comment Period Opens: December 8, 2022

Comment Period Closes: February 6, 2023

Comment Submitted: February 3, 2023

Docket No. OP-1793

We appreciate the opportunity to comment on Principles for Climate-Related Financial Risk Management for Large Financial Institutions. Our comments reflect our concerns about recent efforts to indirectly influence climate change through regulation of the financial sector, rather than having Congress take initiatives to directly address climate change coming from the real sector. The request for comment suggests that financial institutions will likely be facing physical risks, because of weather-related events that may affect the financial institutions’ portfolios, and transition risks, because of policy or other changes that materially affect their provision of services.

On the one hand, the more complex the approach to dealing with banks is, the greater the transition risks are likely to be. We will show that the implementation of Basel capital requirements has introduced a significant (and growing) complexity to the existing regulatory framework over the past few decades. Adding a completely new climate regulatory framework may likewise further increase the complexity of bank regulation. On the other hand, the physical risks may be overstated. Although it may be too soon to tell, one of us has shown in a recent paper that the recent increase in the incidence and damage from natural disasters has not affected banks’ performance, as measured by return on assets or net interest margins.

Although we agree that climate change may pose extreme long-term risks, efforts to curtail physical and transition risks reflect a single-prong approach to address climate change that focuses on indirect mitigation through the financial sector rather than on direct mitigation through the real sector. Such efforts may have a limited impact. Instead, beyond mitigation of greenhouse gas emissions from the real sector, a three-prong approach that also reflects adaptation, which works to limit damage, and amelioration, which works to offset climate change from greenhouse gas emissions, may be necessary to manage problems from climate change. 2 Beyond having a deep and resilient financial system readily able to provide the debt and equity funding to finance adaptation and amelioration, it is not clear if adaptation and amelioration initiatives can be accomplished by targeting the financial system.

We believe other risks pose a more immediate risk to the financial sector. For instance, bank capital and liquidity may be insufficient to address the financial stability issues arising from cybersecurity risks.3 In addition, the systemic risk that arises from implementation of climate change stress tests could open the door to Federal Reserve policies becoming too sensitive to political issues, which may decrease the independence of Federal Reserve policies from congressional politics. Congress has already given the Federal Reserve the dual mandate of ensuring price stability and attaining full employment; the addition of financial stability, and now climate change, can potentially result in conflicting priorities for the Federal Reserve.

Stress tests should first address more immediate issues affecting the US economy. For example, one possibility would be to have an inflation stress test based on labor shortages in the supply chain. A stress test could conceptually incorporate the question, “If Congress had not introduced the Bracero program of the 1940s and 1950s, which introduced temporary visas to lessen the impact of inflation, what would the systemic impact to the financial sector have been?” This stress test would not only address a more pressing economic concern but also increase Federal Reserve independence by modeling the risks of political inaction to address labor supply shortages. The Federal Reserve could be the most credible government agency for raising concerns about supply-side shortages to Congress.

The request for comment on the Principles for Climate-Related Financial Risk Management for Large Financial Institutions asks those commenting to answer three questions. We will provide answers to the first two.

QUESTION 1: IN WHAT WAYS, IF ANY, COULD THE DRAFT PRINCIPLES BE REVISED TO BETTER ADDRESS CHALLENGES A FINANCIAL INSTITUTION MAY FACE IN MANAGING CLIMATE RELATED FINANCIAL RISKS?

One way the draft principles might be made more effective is by increasing capital requirements. A key objective of current federal bank regulation in the United States is to have banking entities maintain adequate levels of funding from equity or long-term debt, as short-term debt is more volatile. Banks in the United States have long operated within a holding company structure, and for this reason, the current regulatory framework holds that bank capital should be regulated at both the parent and the subsidiary levels. Furthermore, the “source of strength” doctrine (Regulation Y) suggests that parent corporations will come to the rescue of a failing subsidiary, even though, as Kupiec suggests, this may not be the case.

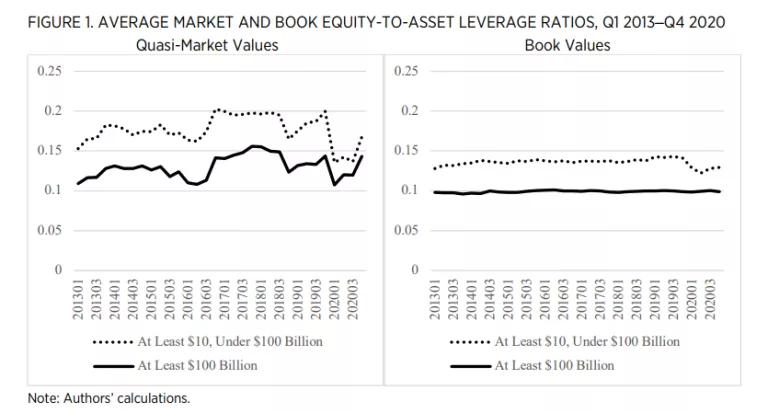

The word “risk” appears 194 times in the guidelines, while the word “uncertainty” appears twice. The distinction between these terms is important in the context of the draft principles because much remains unknown about whether and how banks will be affected by climate change. Given growing uncertainty about the physical or transition risks that may arise from climate change, bank capital is especially relevant because it, and especially equity capital, is an ideally suited funding source in the face of unexpected losses. In figure 1, we depict the average quasi-market equity-to-asset ratio, measured as the market value of equity relative to the quantity of book value of assets minus book value of equity plus market value of equity. This figure also depicts the average book equity-to-asset ratios for banks with at least $10 billion but under $100 billion and for banks with at least $100 billion. The graphs in figure 1 show that the largest banking entities, on average, have the lowest equity-to-asset ratios, whereas smaller banking entities have higher average ratios.

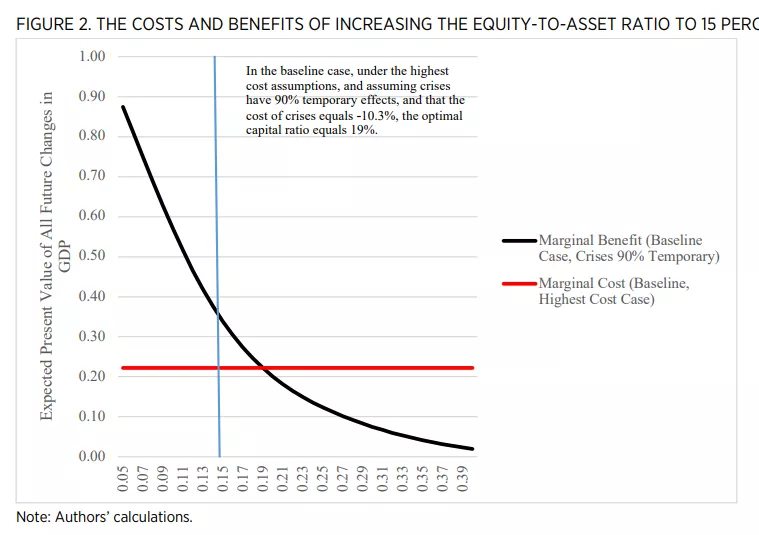

How high could bank capital be? Following the 2007–2009 financial crisis, a 15 percent threshold had been suggested as an option. Previously published research indicates that the benefits of increasing the equity capital-to-asset ratio to at least 15 percent (a higher threshold than that in current regulatory guidelines) might well outweigh the costs without incorporating climate change into the analysis. The benefits in this analysis come from having banks experience a lower probability of default, which in turn lowers the probability of a banking crisis and the associated reduction in GDP. The assumed costs in the analysis relate to the assumption that equity funding is more expensive than debt, so that having banks funding with more equity could increase the borrowing costs that are passed on to customers, resulting in fewer loans and a reduction in GDP. In figure 2, showing a baseline case from Barth and Miller (2018), the intersection between the marginal benefits and costs suggests an optimal ratio of 19 percent. Barth and Miller examined 287 other assumption-based cases; in 163 of the 288 cases, the optimal ratio equaled or exceeded 20 percent. In 221 cases, the optimal ratio equaled or exceeded 15 percent. In 258 cases, the optimal ratio equaled or exceeded 10 percent.

In a recent blog post, one of us shows that as a bank’s assets are exposed to more systematic climate risk, the bank has a greater capacity to take on asset risk if it has a higher equity-to-asset leverage ratio (20 percent in the example) than if it has a low equity-to-asset leverage ratio (5 percent in the example). That means that if a bank operates with 95 percent debt and 5 percent equity, it must keep ultra-safe assets on its books, which would tend to exclude typical bank assets such as loans that may be exposed to transition risks and perhaps physical risks. Otherwise, it will be at greater risk of default. However, if the bank operates with 80 percent debt and 20 percent equity, it can hold on to riskier assets that may be exposed to transition risks and perhaps physical risks; this means the banks can continue lending.

QUESTION 2: ARE THERE AREAS WHERE THE DRAFT PRINCIPLES SHOULD BE MORE OR LESS SPECIFIC GIVEN THE CURRENT DATA AVAILABILITY AND UNDERSTANDING OF CLIMATERELATED FINANCIAL RISKS? WHAT OTHER ASPECTS OF CLIMATE-RELATED FINANCIAL RISK MANAGEMENT, IF ANY, SHOULD THE BOARD CONSIDER?

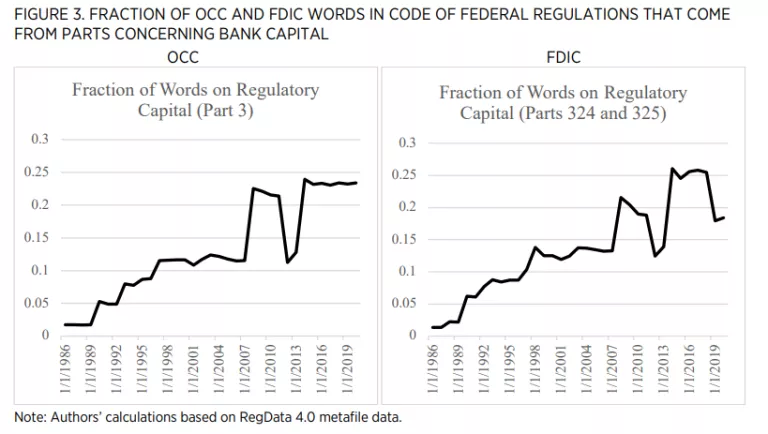

Simpler approaches may be more effective than complex ones, given the uncertainties associated with climate change and the policies being discussed to address it. As a counter-example (reflecting a more complex approach to regulation), take the risk-based capital framework that US banks must comply with. As figure 3 shows, the proportion of words in the Code of Federal Regulations that relate to the capital regulations of the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC) has grown from well under 5 percent in the early 1980s to roughly 20 percent in recent years. That is in spite of the fact that capital, as shown in figure 1, often makes up only 10–15 percent of one side of a bank’s balance sheet.

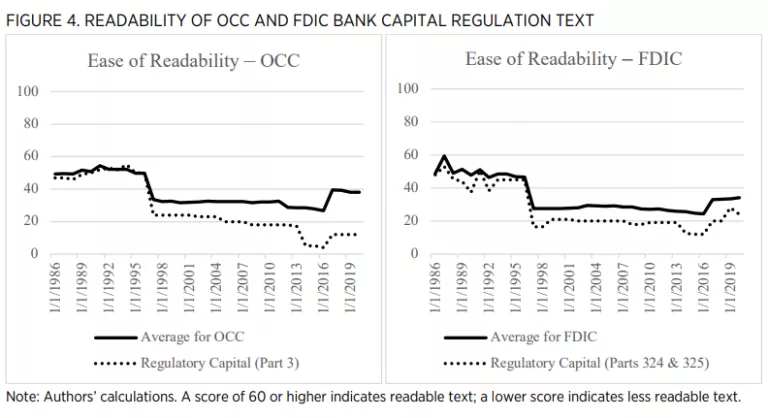

Moreover, as figure 4 shows, OCC and FDIC text concerning bank capital regulation is less readable than other parts of the OCC’s and the FDIC’s regulatory code, as measured by the Flesch test of reading ease. In addition to the low readability score for bank capital regulation text overall, the OCC’s regulatory capital text had a lower score than the FDIC’s, which may indicate how much more complex the text is for the largest banks. This verbosity and lack of readability opens the way to even more costly banking because bank staff may have to hire more lawyers, accountants, and now climate change experts to navigate newly added regulatory text.

CONCLUSION

As regulators, banks, and, most important, bank customers face a world of new regulatory initiatives to address climate change, we underscore the effectiveness of a relatively simple approach to ensuring that banks remain resilient—that is to increase equity capital.

Citations and endnotes are not included in the web version of this product. For complete citations and endnotes, please refer to the downloadable PDF at the top of the webpage.