- | Regulation Regulation

- | Public Interest Comments Public Interest Comments

- |

Comment on the Proposed Rulemaking on "Regulatory Capital Rule: Large Banking Organizations and Banking Organizations with Significant Trading Activity"

I appreciate the opportunity to comment on the notice of proposed rulemaking for “Regulatory Capital Rule: Large Banking Organizations and Banking Organizations with Significant Trading Activity.” I am a Senior Research Fellow at the Mercatus Center, a university-based research center at George Mason University. My comments do not reflect the views of any affected party but do reflect my general concerns about the effectiveness and unintended consequences of regulation. My comments address question 3 and also deeper problems with the proposal’s methods and assumptions.

Question 3 asks about the advantages and disadvantages of harmonizing the calculation of regulatory capital across large banking organizations and using different approaches (for example, the expanded risk-based approach and the US standardized approach) for the calculation of risk-weighted assets. It is also about the proposal’s unintended consequences.

I see only advantages of harmonizing the calculation of regulatory capital across all banking organizations, and not just large ones, since using nominal dollar thresholds does not provide an effective cutoff in an inflationary environment where more banks will gradually be captured through regulatory creep. However, I argue that harmonizing can be effectively accomplished using the leverage ratio alone, measured as equity relative to debt (or the sum of equity and debt), not in combination with risk-based capital (RBC). Concerns about market risk can be addressed by using market values of equity, or by comparing market and book values; risk-based capital requirements attempt to introduce what market equity already does.

Many comments already submitted suggest that higher bank capital will make it more difficult for banks to lend. That is true of RBC but not the leverage ratio, which has minimal effects on bank asset allocations. The leverage ratio implicitly assumes equal risk-weights for all assets and is best designed for unexpected losses, as risk-weighting cannot anticipate where unexpected losses will arise, and problems only become apparent after subsequent bank distress. If the agencies want to protect depositors or prevent bank failures without deterring lending, they should abandon efforts to turn all losses—including unexpected losses—into actual expected losses through risk-weighting and instead just have banks meet a funding prerequisite of higher equity, say 15 percent or more relative to debt (or the sum of equity and debt); it’s the “unknown unknowns,” rather than the “known unknowns,” that harm depositors and cause banks to fail.

This was apparent in the lead up to the 2007–2009 Financial Crisis for assets that turned out to be riskier than the risk-weights suggested. It was also true with the Silicon Valley Bank (SVB) and Silvergate failures in March 2023. These banks held large positions in agency mortgage-backed securities (MBS) and Treasuries, which have low risk-weights and risk-weights equal to zero, respectively, reflecting their low default risk. Low risk-weights meant those banks had little capital to back such asset holdings, and the problem was compounded by those banks not hedging against interest-rate risk, which could have offset such losses. [1]

I elaborate on these issues in the next four sections, in support of the thesis that the leverage ratio—and not risk-based capital—is the more effective regulatory capital regime:

Changes to risk-weights after the 2001 Recourse Rule had unintended consequences that contributed to the 2007–2009 Financial Crisis.

Post-crisis revisions adopted by US regulators from the Basel III capital guidelines resulted in riskweights that distorted bank balance sheets.

Risk-weighting did not prevent the March 2023 bank failures.

Regulatory verbosity on risk-weighting has led to regulatory complexity, creating distortions and added costs of compliance.

1. The Unintended Consequences of RBC and Its Role in the 2007–2009 Financial Crisis

The notice of proposed rulemaking highlights the role of the 1996 market risk rule as a factor in the 2007–2009 Financial Crisis (p. 64091) and the motivation behind current regulatory proposals to end bank use of internal modeling, when calculating RBC. Internal modeling certainly has flaws; however, the notice of proposed rulemaking ignores the role of the changes to risk-weights after the 2001 Recourse Rule. [2] The Recourse Rule adopted early Basel II proposals by the Basel Committee on Banking Supervision, which also contributed to the 2007–2009 Financial Crisis, as pointed out in the Financial Crisis Inquiry Commission Report. [3]

Let us first understand how the Recourse Rule came about. Banks complained about the unequal regulatory capital treatment between agency mortgage-backed securities (MBS) tranches and similar private-label MBS tranches originated by banks under Basel I standards. The Federal Deposit Insurance Corporation (FDIC), the Federal Reserve System, and the Office of the Comptroller of the Currency (OCC) addressed the unequal treatment through the Recourse Rule. The final rulemaking linked risk-weights to securities ratings, lowering risk-weights (which lowered capital requirements) on the highest-rated, private-label securitization tranches while increasing risk-weights (which increased capital requirements) on the lower rated tranches. That sounds good in principle, but the rule change did not take into account how asset-securitizing banks could game the risk-weights or produce tranches that turned out riskier than their ratings suggested.

Figure 1 below depicts what happened before and after the final rulemaking. On average, the share of highly rated, private-label securitization tranches—held by the largest bank holding companies (BHCs) that were active in securitizing assets and submitting comments to influence the proposed Recourse Rule—increased, while the share of lower rated tranches decreased. [4] For BHCs that did not comment directly on the proposed Recourse Rule, the share of highly rated tranches remained low and constant, while the share of lower rated tranches decreased. So while the intent of the Recourse Rule was to encourage securitization without added risk-taking, it enabled asset-securitizing BHCs to create and also hold more highly rated tranches, some of which later were completely wiped out during the crisis. [5] BHCs that held more of the highly rated, private-label tranches had greater increases in equity-return volatility and risk of default during the crisis.

Studies following the 2007–2009 Financial Crisis showed that all banks facing distress during the crisis had satisfied the regulatory capital requirements. [6] One study also points out that Citigroup had about 6 percent equity in 2006, and a loss of 60 percent on the highly rated tranches would be enough to wipe out their equity. [7] If banks had been required to have just a higher leverage ratio of 15 percent or more, they likely would have had the loss-absorbing capacity to handle the unexpected losses from securitization exposures. [8] RBC ratios, which exceed the simpler regulatory leverage ratios, give the appearance that banks are highly capitalized when they are not. They appear highly capitalized due to the way the capital requirements are specified (e.g., equity capital relative to risk-weighted assets) and due to banks wanting to minimize equity capital funding to increase debt funding. As such, the apparent high ratios arise because banks, especially the larger ones, tend to shift toward assets with lower risk-weights (and hence lower capital requirements) and away from assets with higher risk-weights (and hence higher capital requirements).

In the aftermath of the 2007-2009 Financial Crisis, reform initiatives failed to recognize the role of RBC as a cause of that crisis. First, Congress made no references to the Recourse Rule when Section 939 of the Wall Street Reform and Consumer Protection Act, or Dodd-Frank Act, called for eliminating regulatory references to ratings, which for securitizations originated with the Recourse Rule. [9] Instead, rating agencies bore the brunt of congressional blame, even though in a comment letter dated February 2, 1998, obtained from an electronic Freedom of Information Act (eFOIA) request, former Moody’s Managing Director Donald Selzer stated this in response to an earlier proposed Recourse Rule: [10]

Moody's comments address only those aspects of the Proposal that propose the use of credit ratings to measure the level of risk for recourse obligations and direct credit substitutes or other securitized tranches of asset securitizations. It notes that the Proposal attempts to address some adverse consequences of the use of credit ratings for these purposes, but Moody's believes that those adverse consequences will ultimately undermine both the validity of the risk-based capital standards and the credibility of credit ratings. Specifically:

• Rating scales vary substantially between rating agencies. Ratings that appear equivalent due to similarities of their alphanumeric symbols may not be equivalent from a credit risk perspective. A regulatory scheme that uses ratings of different rating agencies interchangeably inherently contains systematic errors.

• The proposed regulation gives regulated financial institutions, as investors in ABS, an incentive to demand higher credit ratings from rating agencies than a security's risk would warrant. It weakens the tension between the interests of the investors who rely on ratings and the interests of the issuers who pay rating agencies to generate ratings. This proposal will compound the adverse effects on rating agencies already resulting from the use of ratings by regulators in other financial sectors, and will over time exert further negative pressure on the quality and consistency of rating opinions.

• The proposal's attempt to reduce rating shopping by having special requirements for "non-traded positions within a securitization" is inadequate, as it fails to address the underlying problem of the change in investor interests (and therefor rating agency motivations) created by this rule.

• The small incremental benefit that the use of ratings might bring to the risk-based capital adequacy system does not justify its adverse impact on the rating process.

• Alternatives exist that would more consistently capture the specific credit risks of individual exposures and their portfolio credit risk implications and the interaction of those securities with all other securities and risk exposures on a financial entity's balance sheet.

The lesson following the 2007–2009 Financial Crisis was that risk-weighting creates more scope for regulatory failure, but the Recourse Rule escaped scrutiny.

Second, Section 941 of the Dodd-Frank Act called for risk-retention regulation to get BHCs to retain more of deal credit risk, even though Federal Reserve research showed that with some securitization deals, originating banks could signal confidence in deals by holding the highest-rated rather than the unrated equity tranche. [11] In my view, this does not speak to the fault of the research but does speak to the fault of regulatory efforts to encourage certain activity, securitization in this case, by lowering risk-weights on parts of deals that regulators deem safe. With only a leverage ratio in place, this would not have happened.

2. How Risk-Weights Distort Bank Balance Sheets

In the previous section, I empirically showed how risk-weights created distortions and affected securitizing BHC holdings of highly rated and lower rated tranches leading up to the 2007–2009 Financial Crisis. But post-crisis revisions have resulted in additional distortions. After the 2007–2009 Financial Crisis, in addition to the regulatory changes pursuant to the Dodd-Frank Act, the Basel Committee issued the Basel III capital guidelines that US regulators largely adopted. In this section I show why RBC ratios, such as the Tier 1 capital ratio, for the most part distort bank asset holdings with relatively little changes in the bank funding mix, while the simpler leverage ratios primarily change the bank funding mix with little distortions to bank asset holdings. So when parties submit comments attacking the Basel III Endgame proposal, they are correct specifically regarding changes in risk-weights, but incorrect regarding increasing equity funding.

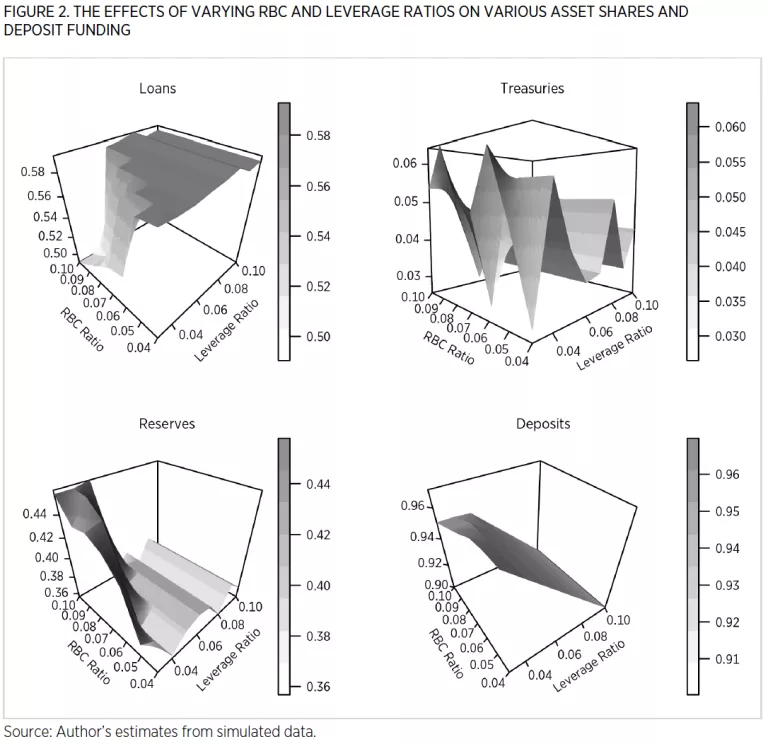

To illustrate this, figure 2 below shows what happens to a bank’s holdings of loans, reserves, and Treasuries, as well as deposit funding, as you increase the RBC ratio from 4 to 10 percent and the leverage ratio from 3 to 10 percent. The graph below is generated from solutions to a profit-maximizing bank’s optimal asset shares and the share of deposits that vary with the minimum RBC ratio from 4 to 10 percent and the leverage ratio from 3 to 10 percent. [12]

The figure shows that loans and reserves respond mostly to increases in RBC but not the leverage ratio, such that as the RBC requirement rises from 4 to 10 percent, the bank maximizes profits subject to its constraints by shifting from loans to reserves; Treasuries vary less because of the assumption that they earn a slightly lower return and have slightly higher administrative costs than reserves, as discussed in footnote 12. On the funding side, deposits respond mostly to increasing the leverage ratio but not much to increasing the RBC ratio. Overall, these results suggest that the leverage ratio for the most part affects the funding aspect of a bank, while the RBC ratios affect the asset allocation aspect of a bank.

3. RBC Was Not Effective in Preventing the March 2023 Bank Failures

Whether the goal of RBC requirements is to protect depositors or prevent bank failures, the distressed banks satisfied RBC-based regulatory capital requirements, in spite of their complexity, in March 2023 just as they did in 2007–2009.13 While risk-weighting did not cause these banks to fail, it also did not prevent the recent bank failures in the spring of 2023. Figure 3 below shows that the RBC Tier 1 capital ratios of Silicon Valley Bank, Signature, and First Republic were all above 10 percent and changed little even as the banks became increasingly distressed. In the case of Silvergate, its Tier 1 capital ratio was over 50 percent before it eventually voluntarily liquidated!

While the complex RBC ratios do not signal when a bank faces distress, simpler measures do. For instance, the quasi-market leverage ratio—the ratio of the market value of equity to the quantity of book assets minus book equity plus market value of equity—does indicate when a bank’s performance deteriorates. Figure 4 below shows the ratios for the three failed banks and Silvergate were declining throughout 2022, indicating that they faced deteriorating balance sheet conditions.

In addition, the associated book equity to book asset ratios show that these banks were all highly leveraged. Even though the market leverage ratios were higher than the book ratios for most quarters, as shown in Figure 5, by the end of 2022, the market ratios had fallen to, or even below, the book ratio values, which suggests that they were underperforming.

4. On the Verbosity (and Complexity) of Basel-Type Capital Regulation

Given the length of the proposed rulemaking, it would be useful to have additional insights about the extent to which regulatory verbosity and the associated complexity contributes to or undermines the effectiveness of capital regulation. After all, Basel capital rules have contributed to a steady increase in the complexity of existing regulation leading up to the 2007–2009 Financial Crisis, and that regulation roughly doubled after the crisis. The complexity creates distortions with potentially undesireable effects that prove difficult to predict.

To visualize the growing verbosity associated with the complexity of regulation, figure 6 depicts the share of words in the Code of Federal Regulations on OCC capital regulation (Part 3, Title 12, Parts 1–199) and FDIC capital regulation (Parts 324 and 325, Title 12, Parts 300–399. The figure shows that capital regulation verbiage makes up an increasing fraction of words concerning banking.

The figure shows that prior to the 1988 Basel Accords, words on capital requirements made up under 5 percent of regulatory word counts for banking. After US regulators adopted the Basel Accord guidelines in the years leading up to the 2007–2009 Financial Crisis, that number increased to over 10 percent. Since the crisis, with the implementation of Basel III the number doubled again to about 20 percent—and that’s even though the words involving bank capital itself comprise only a small fraction of just one side of a typical bank’s balance sheet.

Moreover, under Basel III, as Richard Herring notes, there are at least five different numerators and denominators to produce 39 different regulatory capital requirements. [14] The added constraints dramatically increase the complexity of the requirements bank staff must follow, which adds to the costs of complying with that regulation. The added costs diminish the resources banks could use to address other crucial problems (e.g., cybersecurity) and can adversely affect provision of financial services (e.g., spending on compliance rather than actual credit).

Herring also suggests that just by keeping only about one quarter of the total number of capital ratios, the complexity could be reduced without detrimental effects on safety and soundness. For instance, given the stated importance of Common Equity Tier 1 (CET1), it no longer makes sense to also record Tier 1 or Total capital: A more effective approach would do away with risk-weighting altogether.

Conclusions

I agree with a key objective of the notice of proposed rulemaking: to enable banks to fund with more capital. However, in complying with the regulation, banks subjected to the Basel III Endgame rule will likely not increase capital but instead just reallocate their assets to lower the risk-weighted asset denominator rather than the numerator of the RBC ratio. A more effective regulatory capital regime—the leverage ratio—would change the debt-equity funding mix toward more equity funding. The bank failures in March 2023, as the bank distress in 2007–2009, show the dangers of allowing banks to operate with little equity while being subjected to and complying with seemingly high RBC requirements. Higher equity capital requirements that reduce bank debt funding provide a less distortionary, yet effective way of protecting depositors or reducing banks failures.

Notes

For a discussion of Silicon Valley Bank’s and Silvergate’s low risk-weight securities exposures see Stephen “Steph” Miller, “On SVB’s Failure and Other Bank Distress: What’s Going On?,” FinRegRag, March 15, 2023, https://www.finregrag.com/p/on-svbsfailure-and-other-bank-distress.

Risk-Based Capital Guidelines; Capital Adequacy Guidelines; Capital Maintenance: Capital Treatment of Recourse, Direct Credit Substitutes and Residual Interests in Asset Securitizations, 66 Fed. Reg. 59614 (November 29, 2001).

See “The Financial Crisis Inquiry Report: Final Report of the National Commission on the Causes of the Financial and Economic Crisis in the United States,” (Washington, DC: US Government Printing Office, January 2011), 99–100. See also Stephen Matteo Miller, “The Recourse Rule, Regulatory Arbitrage, and the Financial Crisis,” Journal of Regulatory Economics 54, no. 2 (October 2018): 195–217, for a discussion of the effects of the Recourse Rule, which, by adopting Basel II guideline risk-weights for securitization tranches that lowered the risk-weights for the highest rate tranches, spurred demand for those tranches. For a discussion of the effects of the Recourse Rule on Commercial Mortgage Backed Securities pricing, see Richard Stanton and Nancy Wallace, “CMBS Subordination, Ratings Inflation, and Regulatory-Capital Arbitrage,” Financial Management 47 (Spring 2018): 175–201. For a related discussion of the effects of Basel II risk-weights on German banks, see Matthias Efing, “Reaching for Yield in the ABS Market: Evidence from German Bank Investments,” Review of Finance 24, no. 4 (July 2020): 929–59.

See Miller, “The Recourse Rule, Regulatory Arbitrage, and the Financial Crisis.”

For a discussion of the worst-performing assets during the 2007–2009 Financial Crisis, see Larry Cordell, Yilin Huang, and Meredith Williams, “Collateral Damage: Sizing and Assessing the Subprime CDO Crisis,” (Federal Reserve Bank of Philadelphia Working Paper 11-30, Philadelphia, PA, 2012) and Greg Feldberg, Larry Cordell, and Danielle Sass, “The Role of ABS CDOs in the Financial Crisis,” Journal of Structured Finance 25, no. 2 (Summer 2019): 10–27.

For a discussion of this problem for US banks, see Mark J. Flannery, “Maintaining Adequate Bank Capital,” Journal of Money Credit and Banking 46, no. s1 (February 2014): 157–80 and James R. Barth and Stephen Matteo Miller, “On the Rising Complexity of Bank Regulatory Capital Requirements: From Global Guidelines to Their US Implementation,” Journal of Risk and Financial Management 11 (October 2018): Article 77. For a related discussion of the same problem with European banks see Mark J. Flannery and Emanuela Giacomini, “Maintaining Adequate Bank Capital: An Empirical Analysis of the Supervision of European Banks,” Journal of Banking and Finance 59 (2015): 236–49.

See p. 421 in Isil Erel, Taylor Nadauld, and Rene Stulz, “Why Did Holdings of Highly Rated Securitization Tranches Differ So Much Across Banks?” Review of Financial Studies 27, no. 2 (February 2014): 404–53.

See James R. Barth and Stephen Matteo Miller, “Benefits and Costs of a Higher Bank ‘Leverage Ratio’,” Journal of Financial Stability 38 (October 2018): 37–52.

Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. Law 111-203; 124 Stat. 1376 (2010).

See Miller, “The Recourse Rule, Regulatory Arbitrage, and the Financial Crisis” for more details about the eFOIA requestion.

See Michael S. Gibson, “Understanding the Risk of Synthetic CDOs,” (Working Paper, Federal Reserve Board, 2004) and Erel, Nadauld, and Stulz, “Why Did Holdings of Highly Rated Securitization Tranches Differ So Much Across Banks?”

The model used here is a variant of one used by Stephen Matteo Miller and Blake Hoarty, “On Regulation and Excess Reserves: The Case of Basel III,” Journal of Financial Research 44, no. 2 (Summer 2021):, 215-247. The problem calls for choosing the optimal weights, 𝑤!, to maximize profits from loans (L), Treasuries (T), reserves (R), deposits (D) and equity capital in the following problem

max𝛱 = 𝑤"𝑟" + 𝑤#𝑟# + 𝑤$𝑟$ − 𝑤%𝑟% − 𝑤&𝑟& − 1,2 (𝛼𝑤"' + 𝜏𝑤#' + 𝜙𝑤$' + 𝛿𝑤%' + 𝜀𝑤&'). 𝑠. 𝑡. 𝑤" + 𝑤# + 𝑤$ ≤ 1, 𝑤% + 𝑤& = 1, 𝜅"&( ≤ 𝑤&, 𝜅$)*(𝜔"𝑤" + 𝜔#𝑤# + 𝜔$𝑤$) ≤ 𝑤&

subject to a funding constraint, 𝑤% + 𝑤& = 1 that indicates banks fund from deposits and equity funding, a risk-based capital constraint, 𝜅$)*(𝜔"𝑤" + 𝜔#𝑤# + 𝜔$𝑤$) ≤ 𝑤& that indicates that the bank must fund with at least 𝜅$)* of its risk-weighted assets with equity, a leverage ratio, 𝜅"&( ≤ 𝑤& that indicates that the bank must fund with at least 𝜅"&( of total assets with equity. The return on loans (𝑟") equals 0.0829, the return on Treasuries (𝑟#) equals 0.0537, the return on reserves (𝑟$) equals 0.0540, the return on deposits (𝑟%) equals 0.0024 and the return on equity (𝑟&) equals 0.09. I assume that loan holdings are more costly to administer than Treasuries or reserves, as such I assume 𝛼 = 0.005, 𝜏 = 0.004 and 𝜙 = 0.001. I assume that the equity funding cost parameter equals that for deposits, or 𝜀 = 𝛿 = 0.01. I assume that the return on equity 𝑟& = 0.06. In terms of remaining parameters, I vary the leverage ratio 𝜅"&(, defined as equity to total assets, from 0.03 to 0.1 and the risk-based Tier 1 capital ratio from 0.04 to 0.1. I solve for the weights numerically using the Alabama package in R.

See footnote 5 for references.

See Richard Herring, “Less Really Can Be More: Why Simplicity and Comparability Should Be Regulatory Objectives,” Atlantic Economic Journal 44, no. 1 (March 2016): 33–50 and Richard Herring, “The Evolving Complexity of Capital Regulation,” Journal of Financial Services Research 53, no. 2 (June 2018): 183–205.