- | Healthcare Healthcare

- | Research Papers Research Papers

- |

Downgrading the Affordable Care Act: Unattractive Health Insurance and Lower Enrollment

The sicker-than-expected risk pool, together with the phase-out of a large back-end subsidy program to offset insurers’ costs for the most expensive enrollees, is already translating into plans with higher premiums, higher deductibles, and narrower networks. These changes will make ACA plans look even less attractive to the relatively healthy uninsured, creating conditions for an adverse-selection “death spiral” in the individual market.

The goal of the Patient Protection and Affordable Care Act (ACA) was to expand comprehensive health insurance coverage, a goal that many forecasting organizations predicted it would meet. Recent data show, however, that forecasters overestimated total exchange enrollment, the share of higher-income individuals enrolling, and the general health of those who did enroll. The plans offered on ACA exchanges are not attractive to a large number of uninsured, especially the relatively young and healthy individuals needed to make the ACA’s complicated regulatory structure work.

A new study for the Mercatus Center at George Mason University examines the reasons behind the ACA exchanges’ failure to meet widespread expectations. The study explains the likely impact of this failure on health insurance prices and risk pool stability, bringing into question the law’s future prospects of survival without significant revisions.

KEY FINDINGS

- Enrollment figures fell short of projections. Initial Congressional Budget Office (CBO) projections overestimated the number of 2014 enrollees by 2.5 million and 2015 enrollees by 3.5 million, and other forecasting organizations overestimated by even more.

- Enrollment of all but the near-poor is far below projections. Individuals and families earning more than 200 percent of the federal poverty line, who do not qualify for subsidies that significantly reduce high exchange plan deductibles, are largely shunning exchange plans.

- The individual mandate failed to motivate as many uninsured to enroll as predicted. Projections assumed that a large noneconomic motivation to conform to a social norm of having insurance would motivate people to comply with the mandate, but financial incentives to remain uninsured appear to be dominating insurance decision-making for the middle class.

- The pool of enrollees is sicker and more costly than projected. Despite an $8 billion subsidy to cover most of the cost of their expensive enrollees, in 2014 insurers suffered losses equivalent to about 12 percent of the premiums of ACA plans (plans satisfying the law’s new rules and requirements). Insurers are increasing premiums, raising deductibles, and narrowing provider networks in response to unexpectedly large losses on ACA plans.

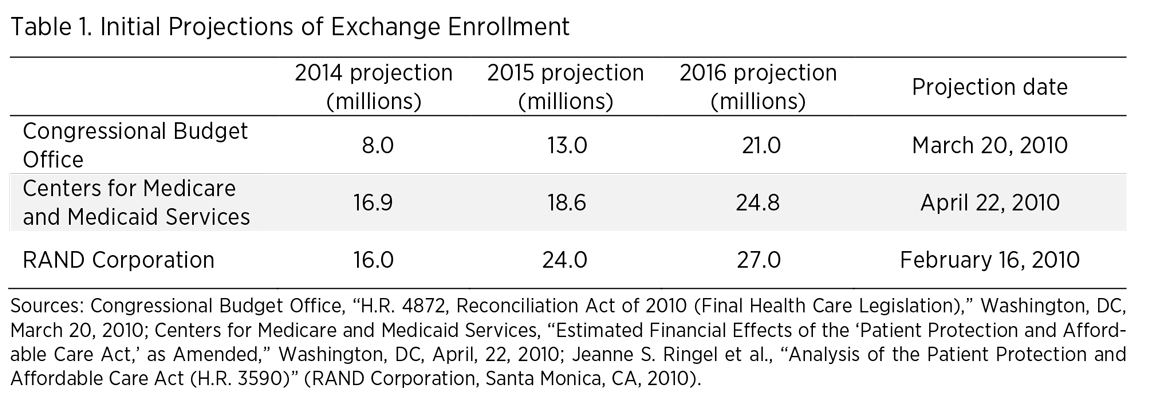

ENROLLMENT SHORTFALL

As Congress was debating the ACA in March 2010, CBO released initial projections of ACA exchange enrollment. They were followed by more optimistic projections by the Centers for Medicare and Medicaid Services and RAND Corporation later that year. The three-year projections are displayed in table 1.

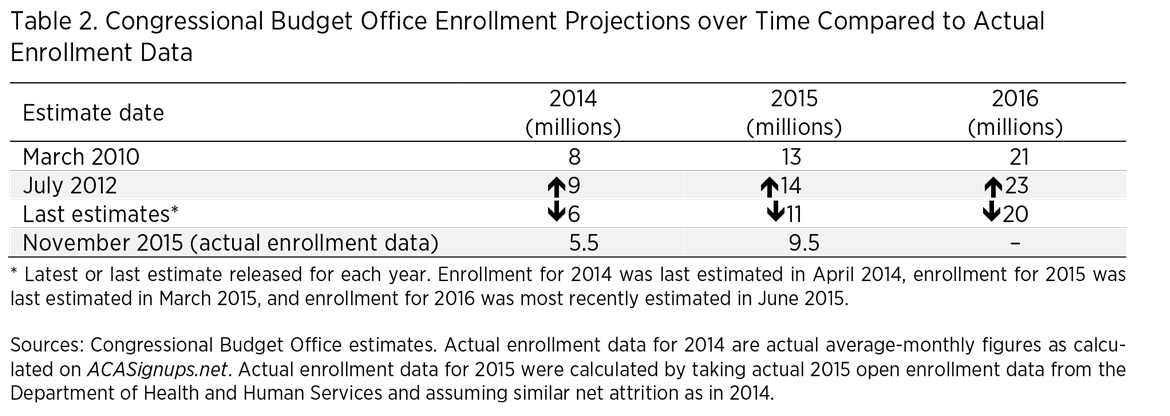

In July 2012, CBO revised its estimates slightly upward following the Supreme Court’s ruling that Medicaid expansion would be at the option of the states, which meant more people just above the poverty line gained eligibility for subsidized exchange plans. Following the initial failures of HealthCare.gov, CBO revised its projections downward, and has repeatedly downgraded its estimates over the past three years. However, data from the Department of Health and Human Services show that even the downgraded estimates are overly optimistic. Table 2 shows CBO projections over time and compares them with actual enrollment data.

Low enrollment figures have been driven, in large part, by the exchange plans’ failure to attract middle-class uninsured people. Most recently, CBO projected 3 million unsubsidized enrollees in 2015, when in fact there were only 1.6 million. In early 2015, the Urban Institute estimated that 25 percent of enrollees in 2016 would be earning more than 400 percent of the federal poverty line; at the end of the 2015 open enrollment period, only 2 percent of enrollees fell into that income class. Most strikingly, only 2 percent of eligible individuals earning more than 400 percent of the federal poverty line chose to purchase exchange plans.

A contributing factor to these forecasting errors was the assumption that the individual mandate would be a more effective tool than it has been thus far. Several forecasting organizations assumed a large noneconomic motivation to conform to laws and to a new social norm for having health insurance. However, a recent study found that most households above 200 percent of the poverty line would be financially better off forgoing ACA insurance for economic reasons, an effect that appears to be dominating decision-making more than any noneconomic desire to conform to the mandate. Moreover, numerous exemptions to the mandate allow people with a broad range of financial difficulties to remain uninsured and not pay the penalty.

HIGH-COST RISK POOL

Early results from the risk corridor program, an ACA-created profit- and loss-sharing program between insurers, show significant losses for insurance companies selling ACA plans. Specifically, profitable insurers owed $360 million, while unprofitable insurers filed claims for $2.9 billion, a shortfall of $2.5 billion. The risk corridor data indicate that insurers’ 2014 losses on ACA plans equaled about 12 percent of the premiums collected.

The performance of the risk corridor program falls short of CBO projections and reflects a significantly sicker (and thus more expensive) pool of enrollees than originally expected. The sicker-than-expected risk pool, together with the phase-out of a large back-end subsidy program to offset insurers’ costs for the most expensive enrollees, is already translating into plans with higher premiums, higher deductibles, and narrower networks. These changes will make ACA plans look even less attractive to the relatively healthy uninsured, creating conditions for an adverse-selection “death spiral” in the individual market.