- | Academic & Student Programs Academic & Student Programs

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

The Research and Development Tax Credit Suffers from Design and Implementation Problems

The research and development (R&D) tax credit—which is one of the largest corporate “tax expenditures,” with an annual cost of more than $9 billion—is one of about 50 “tax extenders” that Congress reauthorizes on a temporary basis. While the tax credit is intended to encourage economic growth by functioning as an incentive for investment in new and innovative technologies, it may not be the best policy to achieve growth.

The research and development (R&D) tax credit—which is one of the largest corporate “tax expenditures,” with an annual cost of more than $9 billion—is one of about 50 “tax extenders” that Congress reauthorizes on a temporary basis. While the tax credit is intended to encourage economic growth by functioning as an incentive for investment in new and innovative technologies, it may not be the best policy to achieve growth.

According to new research published by the Mercatus Center at George Mason University that surveys the current economic literature on the R&D tax credit, eliminating the credit and using the savings to lower the corporate tax rate for all businesses would be a more effective way to support innovation.

The tax credit is poorly targeted. Small, start-up firms conduct some of the most socially beneficial research, contributing to long-term economic growth—yet the credit is of limited or no use to them. The following charts show that the R&D tax credit is chiefly used by big businesses, providing them an advantage in the marketplace and disadvantaging small businesses.

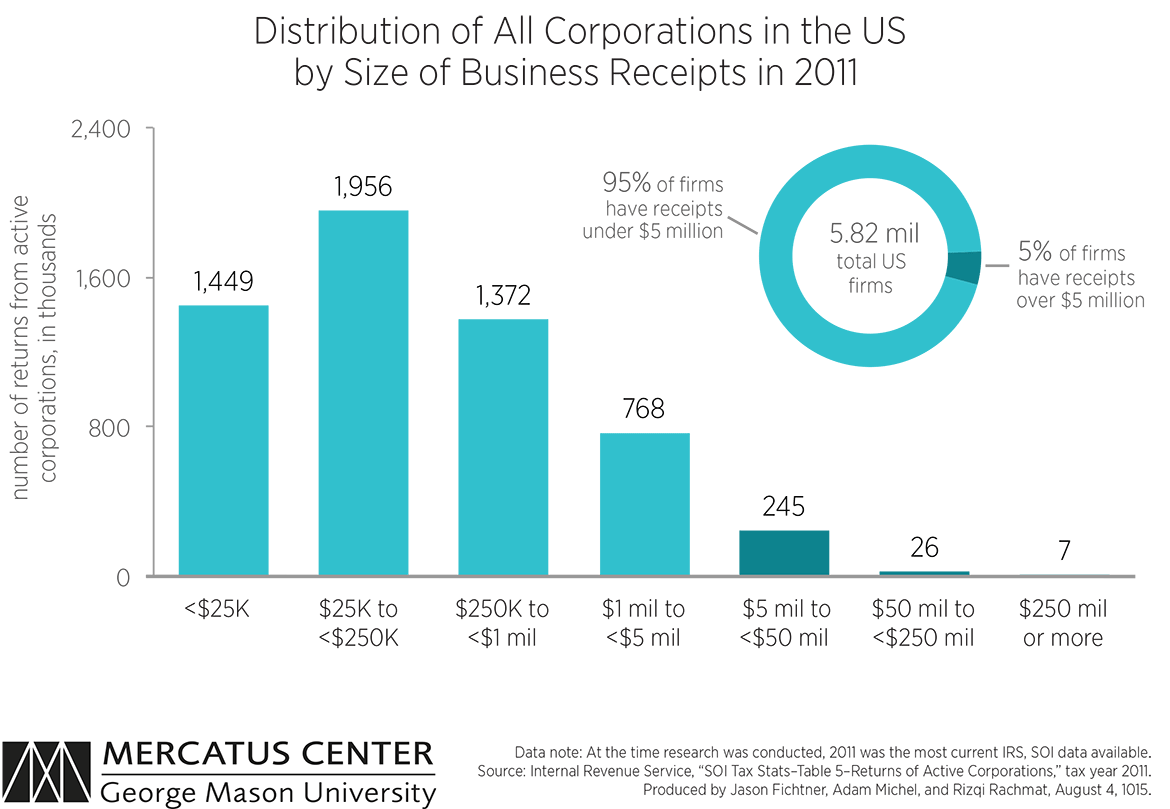

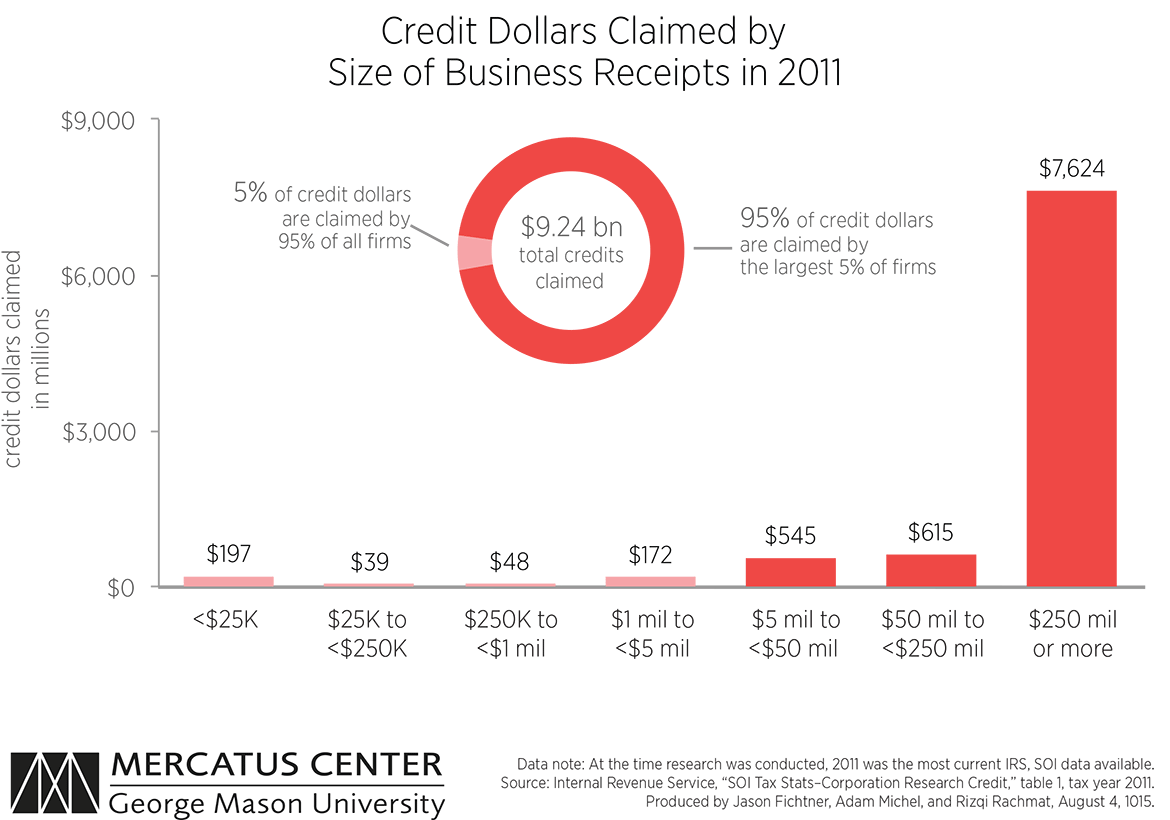

The first chart shows that most firms in the US economy are small—only a small fraction of firms take in over $5 million in receipts. The second chart shows a striking disparity in credit dollars distributed to the largest firms and the combined four smallest firm categories. The largest 5 percent of firms claim 95 percent of all research tax credit dollars, while the four smallest firm categories (receipts less than $5 million), which make up 95 percent of all firms, claim just 5 percent of credit dollars. Twenty-eight percent of the largest firms (i.e., those firms with business receipts over $250 million) receive a credit—compared to 1 percent of the four smallest firm classes.

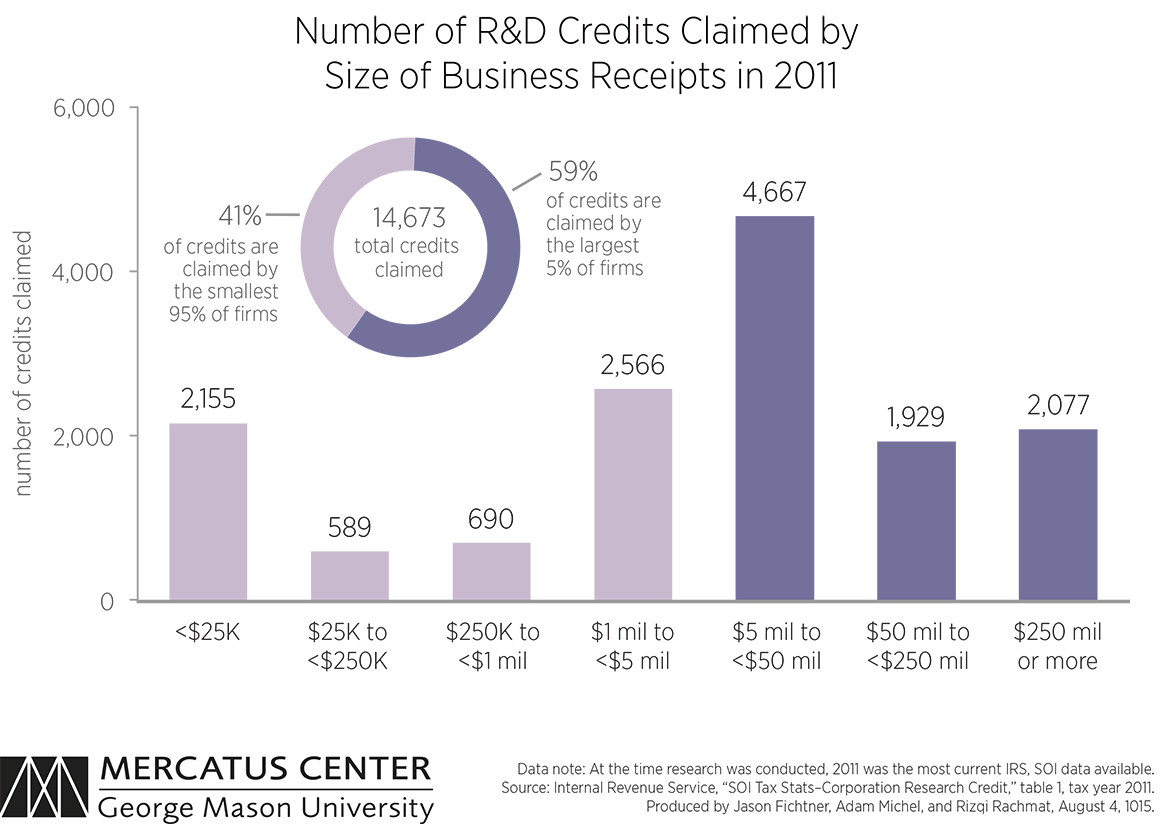

The third chart shows the spread of R&D credits claimed by firms ordered by the size of business receipts. Firms with more than $5 million in receipts compose less than 5 percent of all firms but claim 59 percent of the total credits. The largest 0.13 percent of all firms in the US claim 14 percent of the credits, while the smallest firms claim only 15 percent of credits, but make up 24.88 percent of all firms.

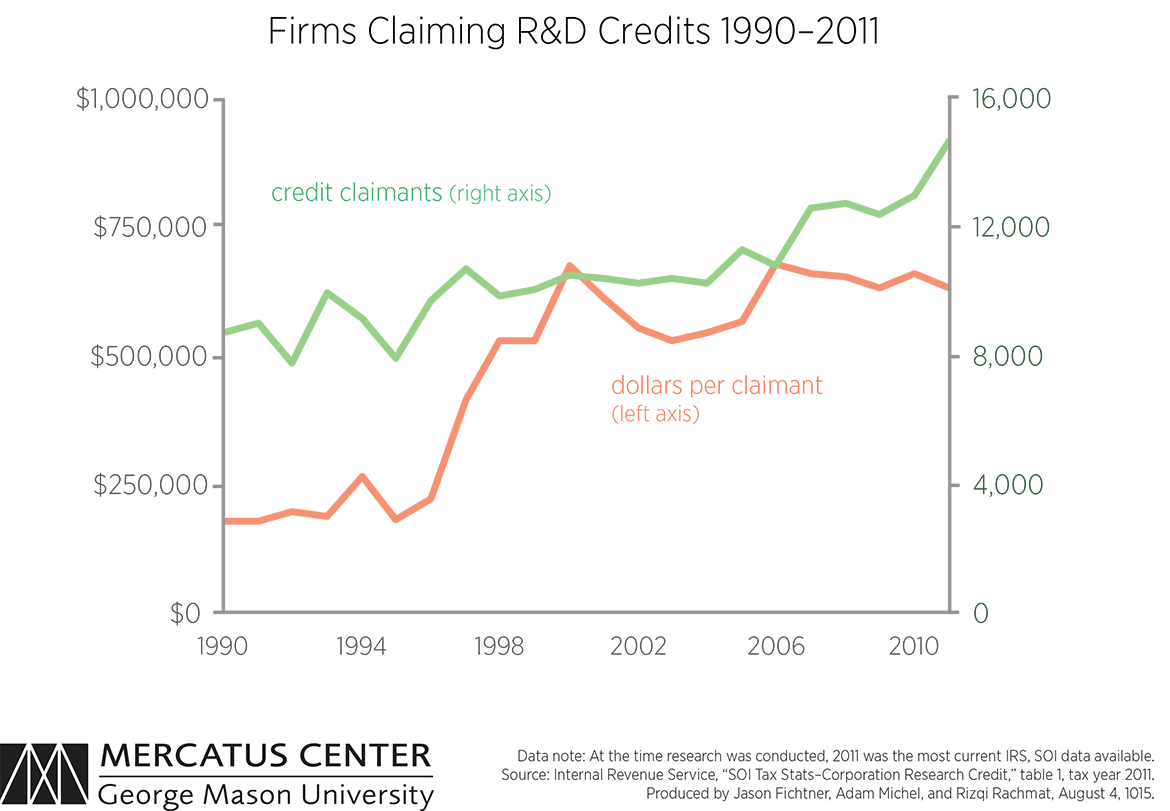

The fourth chart shows trends in R&D credits between 1990 and 2011. The total number of firms claiming the credit has increased by almost 6,000 since 1990, an almost 41 percent increase. There has been a more dramatic rise in the size of dollar claims over the same period, increasing from under $200,000 in 1990 to over $600,000 in 2011. Over that same period, total dollars expended increased by $7.7 billion or 83 percent.

The R&D tax credit is a prime example of policymakers’ inability to target government programs to reap the promised benefits. The R&D credit also suffers from a poor definition of R&D, inducing wasted resources on lobbying and recurring policy uncertainty.

The inability to target businesses that carry out the most innovative and economically beneficial research is just one reason the R&D tax credit should be eliminated and the savings used to lower the corporate tax rate. Lowering the tax rate has been shown to encourage R&D investment and will help all businesses while increasing US global competitiveness.

To speak with a scholar or learn more on this topic, visit our contact page.