- | Academic & Student Programs Academic & Student Programs

- | Housing Housing

- | Journal Articles Journal Articles

- |

The Appearance of Fiscal Prudence

Originally published in The Maryland Journal

Maryland should end the SAC and instead adopt a strict mathematical rule to limit spending based on the sum of the increase in population and inflation. Such a TEL must work with other institutional reforms in order to effectively meet the goal of limiting spending as intended by the designers of Maryland’s Spending and Affordability Committee.

In 2010, after grappling with a decade of structural deficits and two years of recession, Maryland’s Spending Affordability Committee (SAC) questioned its 30-year record on limiting state spending:

Recent years have sorely tested the budgetary concepts customarily employed to account for spending for spending affordability purposes. The combination of huge mid-year spending reductions, massive federal assistance and extensive reliance on one-time supports makes it impossible to clearly establish a basis for calculating a limit without arbitrary judgments about what should be in or out.

The new approach called for by the SAC charges the General Assembly and Governor with the task of reducing the state’s structural deficit.

The call for spending discipline by the SAC, a committee created to recommend prudent spending limits to Maryland’s Legislature and Governor, highlights the design flaws and erratic application of Maryland’s three decades-long SAC experiment. Maryland’s unsuccessful approach to limiting spending can be evaluated against the experience of other states with tax and expenditure limits. The SAC process is subjective, subject to gaming, and ties spending growth to anticipated revenue growth, functioning more as a spending target rather than a cap.

The SAC should be abolished and replaced with a clear, transparent, and easy to evaluate spending rule to guide the General Assembly’s and Governor’s budget deliberations.

The Spending Affordability Committee (SAC)

Creating a Tax and Expenditure Limit (TEL) became a campaign issue in Maryland during the 1978 gubernatorial elections with the passage of Proposition 13 in California. Proposition 13 amended California’s constitution and imposed a limit on property taxes while also requiring a two-thirds majority vote for all changes in the state’s statute that would result in a tax increase. Various states followed California’s move towards fiscal restraint and began to implement tax and expenditure limits of their own.

The same year California passed Proposition 13, Maryland Republican gubernatorial candidate Louise Gore proposed to limit spending to the yearly percentage increase in total personal income. Incumbent Governor Blair Lee III argued that increases in the State budget should be limited to 7 percent of total personal income. Neither campaign was successful. Harry Hughes was elected governor in 1978 and the discussion surrounding spending limits remained dormant for the following few years.

The discussion of creating a TEL for Maryland resurfaced in 1981 when Maryland’s Legislative Policy Committee created the Spending Affordability Committee (the “SAC” or “Committee”). The Committee was signed into law the following year and was given the role of limiting growth in state spending.

The SAC is composed of the Senate majority and minority leaders, the chairmen of the fiscal committees, a number of additional appointed members, and a citizen advisory committee. The Committee’s foremost responsibility is to draft an annual report that provides a recommended level of state spending that is reflective of the current economic and fiscal condition of the state. Based on the Committee’s analysis and briefings from the Department of Legislative Services, the Committee determines a rate of growth in state spending that is deemed affordable. This recommendation is presented to the Governor and the General Assembly each year. The recommendations are generally made in December, to give the Governor enough time to consider the limit before proposing the state budget in January.

To ensure that the spending limit is effective, the Committee notes that “consideration is given to constraining disproportionate growth in State-funded expenditures in any fiscal year which might necessitate or “build in” unsupportable levels of spending in future years.”

However, both the design and implementation of SAC has had the reverse effect. Maryland has experienced close to a decade of structural deficits, with the process of determining a spending limit itself subject to manipulation over the period. On average, spending has increased 5 percent a year in real terms since 1983. The Committee’s recommendations are formulated subjectively, and recommended spending levels are justified according to a shifting set of economic, fiscal, and policy criteria.

The SAC’s methodology is relatively straightforward. Last year’s appropriations are multiplied by a recommended rate of spending growth. The Committee defines base spending and selects a rate of growth for spending based on the results of subjective judgments, policy debate, and an inconsistent interpretation of economic and fiscal data. A review of the SAC’s reports indicates that determining a base level of spending and suggesting a rate of spending growth each point to the core design flaws in Maryland’s approach to limiting spending.

Building the Base

To recommend an absolute amount of spending for the operating budget, the Committee begins by “building the base.” Specifically, appropriations, deficiencies, or spending that occurred in the

previous year without an appropriation are added to last year’s appropriations. The spending limit only applies to general funds, special funds, and higher education funds. The Committee then deducts federal funds and certain higher education revenues from this total. Then, the committee subtracts “exclusions,” which are programmatic items that require a one-time outlay or are financed by fees, PAYGO, or debt such as capital expenditures. This total forms the base.

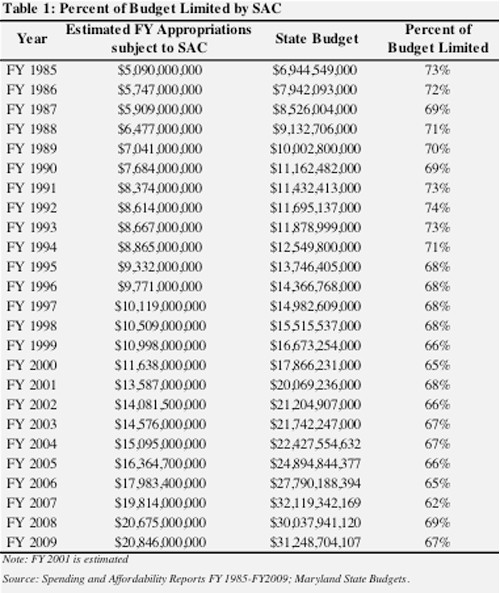

Two design flaws emerge at this point. The base is only a subset of Maryland’s budget. By excluding federal funds and spending on capital projects, the Committee’s charge is only to consider a portion of the budget when recommending a growth limit. As Table 1 shows, on average between FY 1985 and FY 2009, only 66 percent of Maryland’s budget has been subject to the SAC’s spending growth limit. The result is that Maryland’s budget began to experience very rapid growth in the areas outside SAC’s purview, such as the Transportation Trust Fund. In its 1990 report, the Committee notes, “For the third consecutive year, revenues have failed to meet expectations…and operating expenses are expected to rise.” To remedy this, the Committee recommended “revenue enhancements,” including increases in fuel and titling taxes and licensing and registration increases.

By 1995, the Committee, noting the rapid growth in PAYGO and in particular the Transportation Trust Fund, suggested it might “provide guidance to budget committees respecting DOT debt and capital spending levels,” and recommended the SAC’s guiding statute could be modified to include other areas of spending, including “matters relating to federal policy impacts and the long term budget outlook.”

A second flaw in “base building” is its subjective nature. Exclusions from the base largely consist of capital appropriations on the grounds that these projects do not involve ongoing spending. But what is considered an exclusion from the spending limit varies from year to year. Some examples of excluded items are: PAYGO appropriations to the Board of Public Works; transportation capital programs; natural resources and agricultural capital programs such as Program Open Space, waterway improvement, shore erosion prevention, agricultural heritage programs, and agricultural land preservation; capital projects at state universities and colleges; appropriations for housing programs and economic development programs; and the water quality program. The Committee admitted in its 1990 report that “determining what constitutes a capital project in some instances will involve a judgment decision.”

In FY 1992 the Committee modified its methodology for determining the base since the process was “difficult in good times, [but] complicated by the economic problems now facing Maryland.” These included deducting $119 million or the amount of spending withdrawn by the governor in FY 1991 to balance the budget. The Committee noted that the strategy of the SAC “customarily attempts to accommodate a level of spending which allows for a baseline budget and some level of budgetary enhancement.”

Since FY 1992 revenues could not support the “conventionally defined” base, the Committee chose “to be guided by the amount of revenue projected to be available from current sources,” and recommended a 5.1 percent increase in state spending.

Accommodating a spending increase by encouraging a search for “revenue enhancements” points to a final problem with defining base spending: it is subject to gaming. Over the years, the General Assembly has used the budget amendment process to manipulate base spending. Through budget amendments passed outside of the fiscal year budget bill, the General Assembly acts to reduce general spending while at the same time authorizing the use of special funds. The effect is to reduce the base amount of appropriations used to calculate a spending limit, while allowing the overall budget to grow. The Committee criticized this technique of increasing the budget outside of the SAC process in its 1991 report, yet the General Assembly did not begin to limit the practice until 2007.

The Rate of Growth in Spending – Spending Cap or Growth Target?

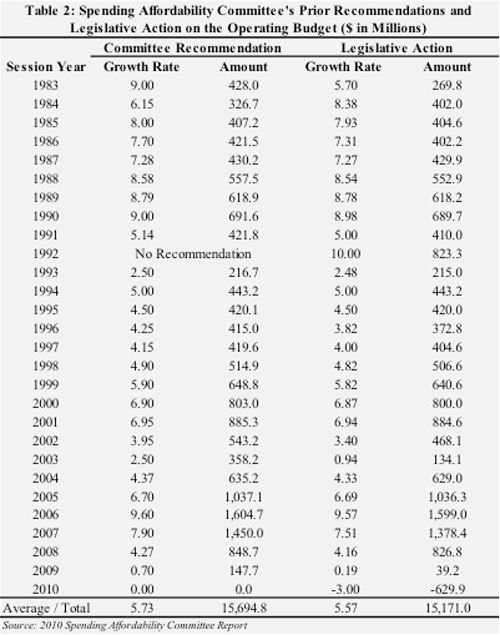

The second element of calculating an annual spending limit is the recommended growth rate, which is multiplied by the spending base. As Table 2 shows, over its history, Maryland’s SAC has recommended a positive rate of growth in the state’s operating budget. In no year has the Committee recommended negative growth (a cut in spending). On the surface, determining a growth rate for state spending appears to be a matter of careful deliberation in the SAC’s annual reports, with the Committee considering economic and fiscal data. However, the reports themselves contain many examples of the Committee ignoring its own rules and analysis.

In its first decade, the Committee’s reports indicated spending growth was tied directly to growth in state personal income. However, the Committee did not follow such a rule. For FY 1986, the Committee justified a recommended 8 percent growth rate in appropriations, a full 20 percent higher than personal income because “It is rate of growth less than the 3-year average growth in personal income (8.11 percent) and 10 percent less than a 4-year average or business cycle approach.”

Thus, while 8 percent growth in appropriations is far higher than growth in personal income – the Committee’s stated guideline – 8 percent is smaller than other measures the Committee could have used.

In addition to ignoring the guidelines used to select a spending growth rate, the Committee seems to interpret economic and fiscal data with a view towards reaching a spending target rather than curtailing spending growth, or reducing spending. In its 1998 report, the Committee stated that while in earlier reports it was guided by a “two-stage process” to establish a spending growth rate: the reported growth in personal income for the preceding year modified by anticipated growth. That year it would recognize an additional factor: economic uncertainty amid a revenue boom.

Plenty is the word which best captures the budget situation. Going into the 1999 session there is plenty of cash in the balances of the general fund and the reserve fund. For the future there is plenty of uncertainty as the forecast of an economic slowdown spawned by the Asian financial crisis and stock market instability contrasts with the current prosperity.

While worried over the effect of tax reductions, the Committee wrote, “Capital gains [not included in personal income statistics] have experienced significant growth in recent years, far outstripping growth in wages and salaries.” This boom in capital gains led the Committee to portray as conservative a recommended 5.9 percent spending growth limit since this,

…recognizes that the personal income measure has understated real growth in the economy due to the exclusion of income from capital gains. The ceiling also recognizes that recent spending limit recommendations were based on personal income projections lower than that actually experienced for the year.

After 28 years of proposing annual increases in spending averaging 5 percent, on the heels of the Great Recession, for FY 2010 and FY 2011 the Committee scaled back the recommended growth rate in spending to 0.7 percent and 0 percent, respectively. While this approach sounds draconian, it simply means spending remains flat in one portion of Maryland’s budget. It is not a negative growth rate and thus does not imply budget cuts.

The SAC’s Inconsistent Recommendations

Over time, the Committee has portrayed its actions as consistent with the principles of fiscal prudence and guided by rigorous deliberations. Yet its reports contain a very inconsistent narrative. Each year, the Committee has defended its decision to recommend increases in spending while simultaneously warning the General Assembly and Governor about the emergence and persistence of structural deficits. The 2002 report, for example, noted that due to lower than anticipated revenue “the Committee is projecting a $549 general fund shortfall in fiscal 2003… if no actions are taken to decrease expenditures or generate additional revenue, fiscal 2004 operating expenditures could exceed revenues by $1.2 billion…the outlook for subsequent years is no better.” In 2004, the committee recommended a 2.5 percent increase in spending.

The following year, while acknowledging the budget was balanced with one-time transfers and one-time revenues, the Committee recommended a 4.37 percent rate of growth in spending while encouraging the legislature to find revenue enhancements, noting that “budget reductions cannot comprise the whole solution to the State’s structural problem…even as we limit spending growth to ‘affordable’ levels in economic terms, the committee notes that the existing revenue base of the State is insufficient to support the remaining programs.” In addition to tasking the Governor and General Assembly with finding more revenue to fund spending increases, the committee simultaneously asked that “future sustainability be a primary consideration…with the imbalance between revenues and expenditures erased by FY 2006,” calling into the question the very purpose of the SAC.

The reports show great contradiction between the stated goal of fiscal prudence and the justification of higher levels of spending in each fiscal year. Over the last decade in a period of declining revenues and economic and budgetary stress, the Committee appeared to struggle with presenting a justification for its recommended spending increases, leading to the most recent report’s call for reform of the process. Ultimately, Maryland’s approach to limiting state spending has been ineffective in both its design and implementation.

How to Design a Binding Spending Rule

Twenty-eight states currently operate under tax and expenditure limits (TELs). The effectiveness of TELs, however, has been widely debated. Some research suggests that TELs are generally ineffective means of limiting growth in state spending whereas other research suggests that TELs can be an effective restraint. A TEL’s effectiveness is a function of its design, where “no two TELs are exactly alike.” There are a range of characteristics in which TELs can differ, including, among others, their adoption method (referendum, initiative, constitutional convention), their codification (statute or state constitution), the way in which they can be overridden (supermajority or simple majority), they way in which they handle surpluses, and the type of formula that they use.

The most common type of TEL in the U.S. limits state budget growth to growth in state income. This type of TEL, however, is associated both with smaller budgets in low-income states and larger budgets in high-income states. A more effective TEL limits budget growth to the sum of inflation plus population. This type of TEL has the greatest effect on spending and is effective in both low-income and high-income states.

TELs are only limiting if they bind the legislature to spend less than it intended. If the TEL suggests a limit greater than what legislators intended to spend, the TEL may instead function as an excuse to spend more. Where TEL formulas tie the limit to growth in overall spending to state income, then high-income or high-growth states may end up with higher growth rates and justifications for greater spending. A TEL cannot work alone to limit spending. In addition, other characteristics that make a TEL more effective include its codification in the state’s constitution, its basis on spending rather than revenues, the requirement of a supermajority or public vote for an override, and a provision that automatically refunds surpluses in excess of the limit.

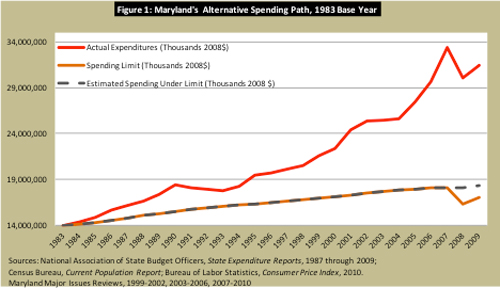

If instead of establishing the SAC, Maryland had instituted a spending rule that limited annual increases in spending to the sum of inflation plus population growth during the same time the SAC was created, total expenditures in 2009 would have been $18.3 million rather than $31.5 million.

The 2010 SAC report stated: “The spending affordability process was put in place in 1982 with the goal of calibrating the growth in State spending to growth in the State’s economy. In implementing that objective, a unique method of classifying and accounting for State spending was developed and has been periodically revised as circumstance has required.” The Actual Expenditures line in the above graph shows that the Committee’s “unique method” has clearly not been able to effectively limit state spending. Moreover, if the state would have adopted the strict formula of limiting annual increases in spending to the sum of inflation plus population growth, it could have avoided the issues that stem from the subjective nature of its calculations and periodic revisions.

Conclusion

In its 2010 report, the Spending Affordability Committee called for a reassessment of the process the Committee has used since 1983 to determine a recommended spending growth limit for the state. For several reasons, the SAC has failed to effectively constrain state spending growth over a three-decade period in Maryland. First, the Committee is only charged with limiting a subset of state spending: general funds, special funds, and higher education funds. The result is that only 66 percent of Maryland’s budget is subject to the SAC’s recommendations. Second, in constraining only one portion of the budget, SAC’s methodology is subjective. Both the definition of base spending and how the Committee generates a recommended rate of spending growth are subjectively determined and prone to gaming.

From its annual reports, the Committee appears to justify a desired level of spending by inconsistently interpreting economic and fiscal data. In both good and bad economic times, the Committee has recommended that spending levels increase for an average annual increase of 5 percent growth in the operating budget. By tying spending growth to personal income growth, the Committee has built in generous spending increases, and during economic downturns only slowed the rate of spending growth, rather than recommend a spending cut. Furthermore, the General Assembly, through the use of budget amendments, has successfully shifted spending outside of the SAC process contributing to an even greater increase in spending.

For these reasons, Maryland should end the SAC and instead adopt a strict mathematical rule to limit spending based on the sum of the increase in population and inflation. Such a TEL must work with other institutional reforms in order to effectively meet the goal of limiting spending as intended by the designers of Maryland’s Spending and Affordability Committee.

To speak with a scholar or learn more on this topic, visit our contact page.