- | Academic & Student Programs Academic & Student Programs

- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Is PAYGO a No-Go?

After a seven-year hiatus, the statutory "pay-as-you-go" (PAYGO) federal spending rule is once again the law of the land. Numerous policy makers have touted its benefits while emphasizing their

After a seven-year hiatus, the statutory "pay-as-you-go" (PAYGO) federal spending rule is once again the law of the land.1 Numerous policy makers have touted its benefits while emphasizing their renewed commitment to fiscal responsibility.2 President Obama recently described PAYGO as a very simple restraint: "Congress can only spend a dollar if it saves a dollar elsewhere."3

This oversimplification ignores the very limited scope of the rule. PAYGO is full of exceptions: It only applies to new or expanded entitlement programs that may increase the deficit. It does not apply to existing programs, such as Medicare, Medicaid, and Social Security. Nor does it apply to discretionary spending, which represents roughly 40 percent of the budget. Furthermore, by focusing on deficits rather than spending, PAYGO does not prevent simultaneous increases in spending and taxation that would hinder economic growth.

Finally, PAYGO has traditionally suffered from political manipulation that undermined its effectiveness. Achieving long-term fiscal stability will require a much broader approach to reform and a far more serious commitment from policy makers.

A BRIEF HISTORY OF PAYGO

Several years of large deficits in the early 1980s, combined with forecasts of continued and growing deficits in the future, spurred Congress to enact fiscal reform. The resulting Balanced Budget and Emergency Deficit Control Act of 1985 set into law a series of deficit targets that were supposed to achieve a balanced budget by 1991.4 If policy makers did not expect to meet deficit targets in a given year, a process known as sequestration, backed by executive order, would automatically cut spending in non-exempt programs.5 But even after passing a revision to the act, Congress did not meet annual deficit targets on several occasions. Not only was there no political agreement on how to achieve deficit reductions, but lower-than-expected economic growth made the task even more difficult. Though the president ultimately issued three sequesters, overriding legislative intervention negated much of the intended savings.6

The Budget Enforcement Act of 1990 (BEA) amended the 1985 law while offering a new strategy to control spending and deficits.7 The BEA divided the budget into two separate components that were subject to different restrictions and enforcement procedures. Discretionary spending (and budget authority) were subject to aggregate limits, while changes to mandatory spending and revenue laws were subject to the "deficit-neutral" requirement of PAYGO.8 Failure to comply with discretionary spending limits would result in cuts only to discretionary spending, and likewise for mandatory spending.9

In order to determine compliance with PAYGO, the director of the Office of Management and Budget (OMB), in consultation with the Congressional Budget Office (CBO), maintained a scorecard that tracked the budgetary effects of new mandatory spending and revenue laws. If the scorecard revealed an increase in the deficit or decrease in the surplus for a given fiscal year, the rule required the president to immediately issue a sequester that imposed across-the-board spending reductions for non-exempt mandatory spending programs.10 Due to the number of exemptions, the eligible pool of funds that could actually be cut was often fairly small.11

Congress extended the statutory PAYGO process in 1993 and 1997, but effectively terminated the rule by not renewing it in 2002. Both houses of Congress adopted procedural PAYGO rules in 2007, but these rules lack the enforcement mechanism provided by the sequester. As a result, policy makers relatively easily bypass or often ignore the rules.12 President Obama signed legislation in February 2010 that reinstated statutory PAYGO. Ironically, this reinstatement accompanied a $1.9 trillion increase in the federal debt ceiling.13

PAYGO SUCCESS STORIES?

The OMB issued a total of 12 PAYGO scorecard reports from FY 1992-2003. Each report indicated net savings or no increase in the deficit. Consequently, the president issued no sequesters under the PAYGO process. Also, starting in 1992, deficits began to shrink, and there were surpluses each year from 1998-2001. Policy makers use these facts as evidence of the effectiveness of PAYGO in controlling spending.

Indeed, one explanation could be that the threat of a sequester acted as a significant deterrent and forced members of Congress to work together to minimize new spending.14 In fact, shortly after PAYGO expired, Congress enacted two programs that led to significant increases in the deficit: the Jobs and Growth Tax Relief Reconciliation Act of 2003 and the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. The government could not have passed these pieces of legislation, or at least not as easily, had the PAYGO system still been in place.15

Another explanation for the lack of sequesters and the shrinking deficit could be that there were significant improvements in the fiscal situation during that time. For instance, mid-decade spending reductions, especially in the defense budget, a revenue boom due to the dot-com bubble, and a reduction of the capital gains tax led to surpluses. The Congressional Budget Office acknowledges that the surpluses of the 1990s were only partially related to the BEA and PAYGO.16

Ironically, the fiscal fortunes of the 1990s eventually led policy makers to break the rules and effectively undermine the BEA and PAYGO. The former CBO director, Douglas Holtz-Eakin, noted, "In that new fiscal landscape, with projections showing mounting surpluses for the coming decade, the BEA could not restrain the pressures to spend more."17

LIMITATIONS OF PAYGO

The 12-year reign of statutory PAYGO might have played some role in limiting further increases in mandatory spending. Nonetheless, several factors limit the extent to which PAYGO can reign in long-term fiscal stability.

1. PAYGO only covers changes to mandatory spending and revenue laws, and it is full of exceptions. Therefore, PAYGO does not address the nation's long-term fiscal imbalance.

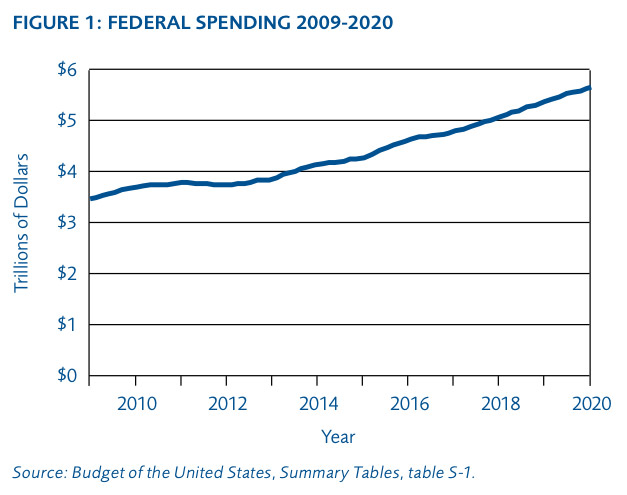

About $1.2 trillion, or one-third of federal spending in 2009, went toward discretionary programs.18 Certainly, devising an effective rule to constrain the growth of discretionary spending would help reduce future deficits. Yet this alone would not solve the nation's fiscal challenges. Even more problematic is the growth in mandatory spending. Figure 1 projects that overall spending will grow by more than 63 percent from 2009-2020, with mandatory spending growing by 52 percent.

Estimates by the Government Accountability Office show that Medicare, Medicaid, and Social Security alone could consume about 25 percent of the U.S. economy by 2080.19

As the current director of the Office of Management and Budget and former director of the Congressional Budget Office, Peter Orszag, explained in 2007, "Although PAYGO may help to prevent a deterioration in the fiscal picture, it only applies to new policy changes rather than the effects of existing policy."20 Therefore, PAYGO will do nothing to remedy the nation's pre-existing fiscal imbalance, which is driven largely by rising expenditures on Social Security, Medicare, and Medicaid.

The PAYGO legislation recently signed by the president also contains a list of over 100 mandatory-spending programs that are exempt from PAYGO requirements.21 CBO analysis of a previous but similar PAYGO bill showed that various exceptions and nuances in the law would allow Congress to increase the deficit by several trillion dollars without triggering a sequestration.22

2. Budget rules such as PAYGO are prone to political manipulation that undermines their credibility and effectiveness.

The credibility and effectiveness of PAYGO rests on the successful enforcement of rules to constrain policy makers. However, the members of Congress who are, in theory, bound by these rules are also the same people who create the rules. Consequently, policy makers frequently create loopholes, rewrite the rules, or simply ignore the rules through various legislative directives.23

Former Chairman of the Joint Economic Committee Jim Saxton explains the process:

There are many ways to sidestep the potential bite that sequestration might impose on the budgetary flesh. One approach is called "directed scorekeeping." With directed scorekeeping, provisions are enacted into law that instruct the director of the OMB not to count certain direct spending increases or revenue reductions on the PAYGO scorecard. Another option is simply to pass a law that mandates no sequestrations occur for a given fiscal year. Yet another technique is to instruct the OMB director to "reset" the balances on the PAYGO scorecard ". . . to avoid having to deal in the future with the long-term effects of its legislative actions." It is also possible to avoid sequestrations by designating various spending or revenue provisions as "emergency requirements," which effectively remove them from the PAYGO scorecard.24

Members of Congress have used most of these procedures to circumvent the rules. Over the course of several years, the OMB director removed more than $700 billion that would have otherwise triggered a number of sequesters under the BEA from PAYGO scorecards.25

3. PAYGO addresses deficits, but it does not place limits on the growth of underlying spending and taxation. Simultaneous increases in spending and taxes could seriously hinder economic growth.

While deficits matter, balanced budgets are not the only important component of fiscal responsibility. The underlying levels of spending and taxation also have significant impacts on the economy. Studies consistently show that high levels of government spending and taxation leads to lower growth and lower income.26 Over the long run, even small changes in economic growth can have a dramatic impact on living standards. PAYGO does nothing to prevent the possibility that Congress will have to raise taxes in order to fund expanded entitlement program, for if past experience is any indicator, policy makers will underestimate the cost of expanding programs, leaving successive generations to deal with the problem.27

POLICY RECOMMENDATIONS

Previous experience indicates that PAYGO may help limit the deterioration of the nation's fiscal imbalance. On the other hand, the latest version of PAYGO does nothing to address the policy's previous shortcomings. It remains vulnerable to the political meddling that undermines its effectiveness. Its emphasis on deficits distracts from underlying spending and taxation that could stunt economic growth. It is full of exceptions and fails to address the nation's pre-existing long-term fiscal challenges.

For PAYGO to be effective, it must apply to the entire federal budget, not just to a small portion of it: there could be no new spending without offsetting cuts. Alternatively, Congress should consider dropping PAYGO altogether, for PAYGO would make many major reforms, like Social Security privatization, non-starters.28 Ultimately, achieving a long-term fiscal balance requires a much more comprehensive reform strategy and many real spending cuts.

ENDNOTES

1. Statutory Pay-As-You-Go Act of 2010, HJ Res 45, 111th Cong., Public Law 111-139, (2010), http://www.govtrack.us/congress/bill.xpd?bill=hj111-45.

2. Nancy Pelosi, "Pelosi: 'PAYGO is a Critical Step on the Path Toward Deficit Reduction and Fiscal Discipline," press release, February 12, 2010, http://www.speaker.gov/newsroom/pressreleases?id=1541/.

3. Barack Obama, "Remarks by the President on 'Pay as you go,'" The White House, Office of the Press Secretary, June 9, 2009, http://www.whitehouse.gov/the-press-office/Remarks-by-the-President-on-….

4. Public Law 99-177, title II, (December 12, 1985), U.S. Statutes at Large 99: 1038, codified at U.S. Code 2 § 900.

5. Congressional Budget Office (CBO), The Budget and Economic Outlook: Fiscal Years 2004-2013, Appendix A—The Expiration of Budget Enforcement Procedures: Issues and Options, January 2003, http://www.cbo.gov/doc.dfm?index=4032&type=0&sequence=7; Robert Keith, The Statutory PAYGO Process for Budget Enforcement: 1991-2002, Congressional Research Service, December 30, 2009; Peter Orszag, Issues in Reinstating a Statutory Pay-As-You-Go Requirement, testimony before the Committee on the Budget, U.S. House of Representatives, July 25, 2007, http://www.cbo.gov/ftpdocs/83xx/ doc8385/07-24-PAYGO_Testimony.pdf.

6. Ibid.

7. Public Law 101-508, title XIII, U.S. Statutes at Large 104: 1388-573, codified at U.S. Code 2 and U.S. Code 15 § 1022.

8. Mandatory spending is also referred to as direct spending. It includes programs such as Social Security, Medicare, Medicaid, federal retirement programs, and unemployment compensation. Discretionary spending is set by annual appropriations acts and is dispersed to government departments and agencies.

9. CBO, Budget and Economic Outlook; Keith, Statutory PAYGO Process; Orszag, Statutory Pay-As-You-Go Requirement.

10. According to OMB, if the balance was positive—that is, it caused an increase in the deficit or decrease in the surplus for that fiscal year—a PAYGO sequestration (an automatic reduction in mandatory spending) was required to offset the increase in the deficit or decrease in the surplus.

11. "Spending for the Social Security program, except for administrative expenses, was exempt from sequestration, as were many other direct spending programs. Any reductions in Medicare spending were limited to 4% and other special sequestration rules applied to selected programs." Keith, Statutory PAYGO Process.

12. CBO, Budget and Economic Outlook; Keith, Statutory PAYGO Process; Orszag, Statutory Pay-As-You-Go Requirement.

13. Statutory Pay-As-You-Go Act of 2010.

14.CBO, Budget and Economic Outlook; Keith, Statutory PAYGO Process; Orszag, Statutory Pay-As-You-Go Requirement.

15. Peter Orszag, testimony before the Committee on the Budget, U.S. House of Representatives, June 25, 2009, http://www.whitehouse.gov/omb/assets/testimony/director_062509_paygo.pdf.

16. CBO, Budget and Economic Outlook; Keith, Statutory PAYGO Process; Orszag, Statutory Pay-As-You-Go Requirement.

17. Douglas Holtz-Eakin, Reforming the Federal Budget Process, testimony before the Subcommittee on Legislative and Budget Process, Committee on Rules, U.S. House of Representatives, March 23, 2004, http://www.cbo.gov/doc.cfm?index=5220&type=0/.

18. U.S. House of Representatives, Committee on the Budget, Frequently Asked Questions About the Federal Budget, July 31, 2009, http://budget.house.gov/faq_budget.shtml/.

19. David Walker, Long-Term Budget Outlook: Saving Our Future Requires Tough Choices Today, testimony before the Committee on the Budget, U.S. Senate, GAO-07-342T, January 11, 2007, http://www.gao.gov/products/GAO-07-342T/.

20. Orszag, Statutory Pay-As-You-Go Requirement.

21. Statutory Pay-As-You-Go Act of 2010.

22. Douglas W. Elmendorf, An Analysis of H.R. 2920, the Statutory Pay-As-You-Go Act of 2009, July 14, 2009, http://www.cbo.gov/ftpdocs/104xx/doc10434/07-14-PAYGO.pdf.

23. David Primo, Rules and Restraint: Government Spending and the Design of Institutions (Chicago: University of Chicago Press, 2007). Also see Cheryl Block, "Budget Gimmicks," in Garrett, Graddy, Jackson, eds., Fiscal Challenges: An Interdisciplinary Approach to Budget Policy (Cambridge: Cambridge University Press, 2008); Edward Davis, "The Evolution of Federal Spending Controls: A Brief Overview," Public Budgeting & Finance 17 (September 1997): 10-24, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=465701; Elizabeth Garrett, "Harnessing Politics: The Dynamics of Offset Requirements In The Tax Legislative Process," University of Chicago Law Review 65 (1998), http://papers.ssrn.com/sol3/papers.cfm?abstract_id=43580/.

24. Jim Saxton, Extending the Budget Enforcement Act: Revision of PAYGO Rules Necessary for Better Tax Policy, United States Congress, May 2002, http://www.house.gov/jecpaygo.pdf.

25. CBO, Budget and Economic Outlook; Orszag, Statutory Pay-As-You-Go Requirement.

26. Daniel Mitchell, "Fiscal Policy Lessons from Europe," Backgrounder #1979, The Heritage Foundation, October 25, 2006, http://www.heritage.org/research/budget/bg1979.cfm/.

27. For example, see Ceci Connoly and Mike Allen, "Medicare Drug Benefit May Cost $1.2 Trillion," Washington Post, February 9, 2005, A01, http://www.washingtonpost.com/wp-dyn/articles/A93282005Feb8.html/.

28. In the case of Social Security privatization, if Americans could opt out of Social Security, the federal government would likely face an instant and severe decline in revenue. If that were to happen, Social Security would spend less in later years (as fewer people would be in the program), but under PAYGO rules the lag would make it hard to implement this change. Other major reforms would face similar difficulties.

To speak with a scholar or learn more on this topic, visit our contact page.