- | Academic & Student Programs Academic & Student Programs

- | Regulation Regulation

- | Working Papers Working Papers

- |

In the Long Run, We’re All Crowded Out

Since the Great Recession began in December 2007, the United States federal government has spent over $1.2 trillion on direct stimulus measures. The positive effects of this spending have been

Introduction: Why Crowding Out Matters

Since the Great Recession began in December 2007, the United States federal government has spent over $1.2 trillion on direct stimulus measures.1 The positive effects of this spending have been obvious: cars have been purchased, teachers have remained employed, and infrastructure has been built. However, job creation and economic growth are affected not only by the easily observed results of policy, but also by the less-obvious results, many of which negatively impact the economy. What is more, these negative effects can last long after current policy makers have left office. To the extent that these less-conspicuous results are ignored or underestimated, policy is biased in favor of government spending. This paper examines one of the most important unseen effects of fiscal policy: crowding out.

The Keynesian Solution: Run a Deficit

The short-run stimulative impact of government spending is a topic of intense academic and political debate. Those who ascribe to a Keynesian view of the economy argue that government spending can provide a powerful boost to economic growth; others argue that government spending has a relatively weak stimulative effect.2

The resources that government spends must be obtained from the private sector through borrowing or taxation.3 If the private sector would have otherwise employed these resources, then government spending creates a cost that must be weighed against whatever benefit comes from spending.

Typically, Keynesians acknowledge the economic costs of taxation and therefore do not think stimulus spending should be financed with taxes.4 Instead, the Keynesian prescription is for government to borrow money and to run deficits during an economic downturn. Then, once the economy begins to grow again, Keynesians counsel surpluses to pay for the debt that was accumulated during the recession. The Keynesian economist Brad DeLong puts it this way:

We want to run a budget that is in surplus during boom, in deficit during recession, that borrows in order to fund investments that benefit the future, and that runs surpluses and pays down debt in order to fund future expenditures that benefit today's taxpayers.5

Indeed, deficit-financed spending has been policy makers’ tool of choice during the most recent recession.6

What is Crowding Out?

Though the costs of borrowing may be less-conspicuous than the costs of taxing, they are no less real. Economists use the term “crowding out” to refer to the contraction in economic activity associated with deficit-financed spending.7 As a result of crowding out, government spending yields less economic growth and this must be weighed against whatever positive impact results from government spending.8

In his General Theory, Keynes himself discussed the potential for crowding out to dominate the growth spurred by government spending.9 He points out:

If, for example, a Government employs 100,000 additional men on public works, and if the multiplier... is 4, it is not safe to assume that aggregate employment will increase by 400,000. For the new policy may have adverse reactions on investment in other directions The method of financing the policy and the increased working cash, required by the increased employment and the associated rise of prices, may have the effect of increasing the rate of interest and so retarding investment in other directions.10

How Does Crowding Out Happen?

Government borrowing can crowd out private spending and investment in a number of ways. Consider first the most-extreme case in which government borrowing has the exact same effect on the economy as government taxation.

Borrowed money must eventually be paid back. And because of this, some taxpayers may view government borrowing as delayed taxation. If so, these taxpayers will spend less today to save in anticipation of paying higher taxes in the future. Accordingly, deficit-financed spending is equivalent totax-financed spending: it induces people to spend less and save more.11 In the extreme version of this theory, there is 100 percent crowding out: households and firms reduce their current consumption and investment by the full amount of the borrowed money. In this sense, government cannot stimulate the economy by borrowing and spending.

Though there is little empirical evidence for the extreme version of this theory in which deficit-financed spending is 100 percent crowded out by private reductions in consumption, few economists endorse the opposite extreme that there is zero crowding out.12

When government borrows to finance its spending, it competes with private entrepreneurs who are borrowing to finance their own activities. Capital used by the government is capital that cannot be used by private businesses. Moreover, when government borrows, competition in the market for loanable funds increases, raising the price of borrowing, or the interest rate, for private investors. For firms, this means an increase in the cost of doing business. Companies and projects that would have otherwise been profitable are no longer able to be so at the higher interest rate.13

Lastly, borrowing may have longer-term effects on the nation’s capital stock, and through that, on its future national income. This can happen when increased borrowing is financed in part or in whole by international capital inflows (foreign lending). In this case, domestic production may not decline in the short run and interest rates may not increase in the short run. But because the nation must eventually repay its foreign debts, future national income is less than it otherwise would be.14

Weighing the Good with the Bad

Whether the stimuluative or crowding-out effect of government spending dominates is a source of debate amongst economists. Monetarists, for example, argue that crowding out negates the growth effects of government spending. Keynesians, however, retort that the multiplier-effects of increased government spending dominate.15 However, on one point there is consensus: fiscal stimulus is most likely to be effective as a short-term fix. In the long run, government cannot get something for nothing and not even the most-ardent Keynesian believes that government should run large, persistent budget deficits.16

Is Government Spending Temporary?

As an empirical matter, however, policy makers do not follow the Keynesian recommendation: Intentions aside, emergency government programs often become permanent.17 For example, a 1973 U.S. Senate investigation examined the impact of Great Depression-era policies that still lingered four decades later:

Since March 9, 1933, the United States has been in a declared state of national emergency... These proclamations give force to 470 provisions of Federal law... Under the powers delegated by these statutes, the President may: seize property; organize and control the means of production; seize commodities; assign military forces abroad; institute martial law; seize and control all transportation and communication; regulate the operation of private enterprise; restrict travel; and, in a plethora of particular ways, control the lives of all American citizens.18

The tendency for temporary and emergency measures to become permanent is alive and well today. In the president’s 2011 budget proposal, 19 once-temporary programs were slated for extension and another 5 were expanded at a net cost of more than $200 billion over the next ten years.19 This, however, only includes federal spending. Since 2009, the federal government has channeled some $250 billion in aid to state and local governments. If the past is any indication, this aid is likely to induce local governments to permanently increase their own expenditures by about $0.40 for every $1.00 of aid.20

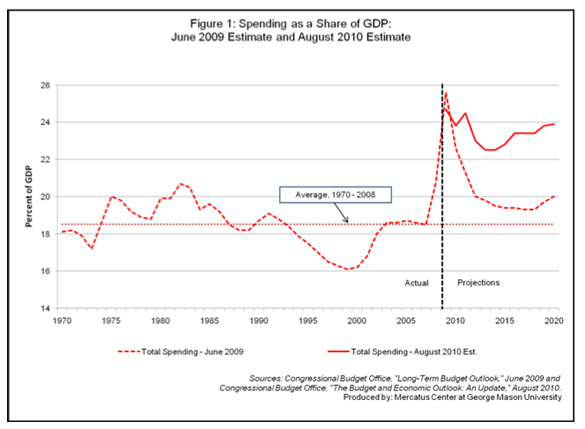

Looking forward, the current government response to the crisis seems likely to lead to a permanently higher level of government spending. Consider figure 1, reproduced from Congressional Budget Office (CBO) reports issued in June 2009 and August 2010. As is the Keynesian prescription, federal spending as a share of Gross Domestic Product (GDP) increased markedly in response to the Great Recession; it rose from less than 19 percent in 2007 to about 25 percent in 2009. In keeping with Keynesian policy recommendations, the spending was initially projected to be temporary. In its 2009 estimate, the CBO projected that spending as a share of GDP would fall back down to near pre-recession levels (though not down to the 1970–2008 average). One year later, however, the CBO is now projecting that spending as a share of GDP will remain significantly above its pre-recessionary level for the foreseeable future.

The tendency for ostensibly temporary spending to become permanent spending helps explain why policy makers fail to take the Keynesians’ advice when it comes to surpluses. Though governments invariable go into deficit during recessionary periods, they rarely run surpluses during expansionary periods. Keynesian recommendations notwithstanding, over the same 74 years since Keynes’s General Theory, the economy has been in expansion 83 percent of the time. Over the same 74 years, the federal government ran a deficit 85 percent of the time.21 Observing this phenomenon a quarter-century ago, Richard Wagner and Nobel Laureate James Buchanan concluded:

Keynesian economics has turned the politicians loose; it has destroyed the effective constraint on politicians' ordinary appetites. Armed with the Keynesian message, politicians can spend and spend without the apparent necessity to tax.22

Given the tendency for temporary stimulus spending to become permanent stimulus spending, what can we say about the net effects of stimulus?

Estimating the Costs of Crowding Out in the Long Run:

John Maynard Keynes famously remarked that, “in the long run, we are all dead.” More than a pithy comment on human mortality, this is an accurate description of Keynesian sentiment. Even if deficit- spending will eventually catch-up to us, the thinking goes, we shouldn’t worry about it today. But one generation’s long-run is the next-generation’s present. And the long-run effects of deficit spending are costly. In a review of the literature on deficit spending, William Gale concluded:

The direct effect of the increase in government borrowing is to reduce national saving and raise long-term interest rates, often by empirically sizable amounts... the results suggest that the sustained deficits facing the nation will impose significant economic costs.23

Andrew Mountford and Harold Uhlig provide a quantitative estimate of these costs. They calculate that a 2 percent increase in government spending will—under the best scenario—lead to a less than 2 percent increase in GDP in the short-run. Eventually, however, the tax increases needed to finance this spending will result in a more than 7 percent contraction in GDP.24

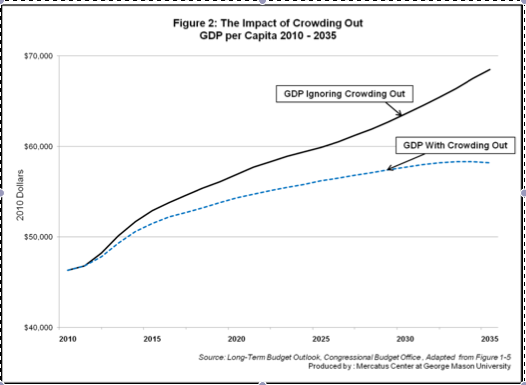

The CBO has also estimated the cost of crowding out over the long run (see figure 2). By their estimate, crowding out will reduce inflation-adjusted gross domestic product per person by 6 percent in 2025 and by 15 percent in 2035.25 For the economy at large, this means an economic cost of $1.2 trillion in real lost economic activity in the year 2025, more than the cost of the wars in Iraq and Afghanistan combined. For individuals, this will mean lower incomes and less opportunity.

Accounting for Crowding Out and the Near-Permanence of Policy:

Over a century and a half ago, the French economist Frédéric Bastiat wrote:

There is only one difference between a bad economist and a good one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those effects that must be foreseen.26

The same may be said of policy makers. Good policy makers should account for both the obvious, beneficial effects of spending as well as for the less-obvious, deleterious effects of spending. Moreover, policy makers should appreciate the fact that government spending programs—even those that are ostensibly temporary—tend to lead to permanently higher spending levels that persist well after the economic troubles subside.27

This principle should also be applied to estimates performed by Congress’s economic forecasting organizations: the Congressional Budget Office and the Joint Committee on Taxation (JCT). Under certain circumstances—as when they have received a specific request from Congress—these organizations account for crowding out in their estimates. (CBO’s estimate, cited in figure 1 above, is a case in point.) In estimates of typical legislation, however, they ignore the crowding effects of spending. Moreover, these organizations are required by law to estimate the cost of a piece of legislation, as it is written.28 This means that if a program is designed to be temporary, it must be scored as such, even though many temporary programs tend to become permanent. In this way, the true cost of legislation is systematically underestimated, biasing lawmakers to favor more spending.

To provide a more complete perspective of the impact of spending, CBO and JCT should account for crowding out in their typical analyses. Ideally, these analyses would also include an additional estimate accounting for the possibility that temporary projects might become permanent. This will encourage lawmakers to account for both the seen and the unseen effects of their actions.

ENDNOTES

1. Bailout Tracker, August 2010.

2. The Obama administration claims that each additional dollar of federal stimulus spending can yield up to $1.57 in economic activity. See Romer and Bernstein (2009), p. 12. Harvard economists Robert Barro and Charles Redlick (2010, p. 1), on the other hand, find that one dollar in spending yields only $0.4 to $0.7 in economic activity. UCSD’s Valerie Ramey (2009) estimates the effect is somewhere between these two estimates: $0.6 to $1.1.

3.In practice, monetary policy offers another way to obtain revenue: if government can print money or somehow increase the velocity of money, it can finance its expenditures that way. We ignore these possibilities in the current paper.

4. For a Keynesian-oriented treatment of taxation, see Romer and Romer (2010).

5. Brad deLong, 2008.

6. International Monetary Fund, 2010.

7. Here we focus of the crowding-out effects of deficit-financed government spending. This is the most common conception of the term. Increasingly, however, economists have come to use the term to refer to various effects of government intervention in the private economy. One example is the crowding-out of private employment by public employment. See Feldman (2006) or Malley and Moutos (1996 and 1998). Another example is the crowding out of private charitable giving by government spending on social programs. See Payne (1998). For a recent account of crowding out as it affects employment, R&D, and sales, see Cohen, Coval, and Malloy (2010).

8. Cowen and Tabarrok, 2010.

9. Spencer and Yohe, 1970.

10. Keynes, [1936] 1963, emphasis original.

11. The idea can be traced back to the classical economist, David Ricardo. Because it implies that deficit-financed spending is equivalent to tax-financed spending, the theory is known as the Ricardian equivalence theorem. In its modern incarnation, it is generally associated with Robert Barro. See Barro (1974).

12. Romer, 2001.

13. Mankiw, 2008, pp. 589-91.

14. Gale, 2008.

15. Snowdon and Vane, 2005.

16. See DeLong’s comments above. More generally, see Center for American Progress, 2009.

17. Nobel Laureate Milton Friedman famously stated: “Nothing is so permanent as a temporary government program.” For an empirical examination of the growth of government spending after crises in the United States, see Holcombe (1993).

18. Church and Mathias, 1973.

19. These figures are drawn from the Office of Management and Budget, 2010. In her farewell address, the Chair of the Council of Economic Advisors, Chrstina Romer, asserted that “$266 billion of additional temporary recovery measures were in the 2011 budget.” See Romer (2010).

20. Sobel and Crowley, 2010.

21. Budget data are calculated from the White House Office of Management and Budget (2010). Economic data are from the U.S. Bureau of Economic Analysis (2010).

22. Buchanan and Wagner, [1977] 1999.

23. Gale, op cit.

24. Mountford and Uhlig, 2008.

25. Congressional Budget Office, the “The Long-Term Budget Outlook,” 2010.

26. Bastiat, [1848] 1995.

27. For a discussion of the path dependent nature of government growth, see Holcombe (2005).

28. For an examination of CBO’s current cost scoring methodology, see Congressional Budget Office. Background on Cost Estimates. (2010). For a discussion of the JCT methodology, see Joint Committee on Taxation, Joint Committee Revenue Estimation Process (2010).

BIBLIOGRAPHY

Barro, Robert. "Are Government Bonds Net Worth?" Journal of Political Economy, 1974: 1095-1117.

Barro, Robert, and Charles Redlick. "Macroeconomic Effects from Government Purchases and Taxes." Mercatus Center at George Mason University Working Paper, July 2010.

Bastiat, Frédéric. Selected Essays on Political Economy. Translated by Seymour Cain. Library of Economics and Liberty, [1848] 1995.

Buchanan, James, and Richard Wagner. Democracy in Deficit. New York: Academic Press, 1977.

Center for American Progress. Progressives and the National Debt: Consequences and Solutions. September 30, 2009. http://www.americanprogress.org/events/2009/09/deficit_event.html (accessed September 1, 2010).

Church, Frank, and Charles McC Mathias Jr. Emergency Powers Statutes. Senate Report, Washington, D.C.: U.S. Government Printing Office, 1973.

CNNMoney.com. "Bailout Tracker." August 2010. http://money.cnn.com/news/storysupplement/economy/bailouttracker/ . Cohen, Lauren, Joshua Coval, and Christopher Malloy. "Do Powerful Politicians Cause Corporate Downsizing?" National Bureau of Economic Research Working Paper, no. 15839 (2010).

Congressional Budget Office. Background on Cost Estimates. http://cbo.gov/costestimates/CEBackground.cfm (accessed August 8, 2010).

Congressional Budget Office. "Long-Term Budget Outlook." Washington, D.C. , 2010.

Cowen, Tyler, and Alex Tabarrok. Modern Principles of Economics. New York: Worth Publishers, 2010.

DeLong, Brad. "The Bush Budget Clown Show." Grasping Reality With Both Hands. February 4, 2008. http://delong.typepad.com/sdj/2008/02/the-bush-budget.html (accessed August 13, 2010).

Feldman, Horst. "Government Size and Unemployment: Evidence From Industrial Countries." Public Choice 127 (2006): 451–467.

Gale, William. "Budget Deficits." In The New Palgrave Dictionary of Economics, by Steven Durlauf and Lawrence Blume. Palgrave Macmillan, 2008.

Holcombe, Randal. "Government Growth in the Twenty-First Century." Policy Challenges and Political Responses: PublicChoice Perspectives on the Post-9/11 World 124, no. 1/2 (2005): 95-114.

Holcombe, Randall G. "Are There Ratchets in the Growth of Federal Government Spending." Public Finance Review, 1993.

International Monetary Fund. Navigating the Fiscal Challenges Ahead. Fiscal Monitor Series, Washington, D.C. : IMF, 2010.

Joint Committee on Taxation. Joint Committee Revenue Estimation Process. http://www.jct.gov/about- us/revenue-estimating.html (accessed 8 18, 2010).

Keynes, John Maynard. The General Theory of Employment, Interest, and Money. New York: Hartcourt, Brace and Company, [1936] 1963.

Malley, Jim, and Thomas Moutos. "Does Government Employment 'Crowd Out' Private Employment? Evidence from Sweden." Scandenavian Journal of Economics, 1996: 289-302.

—. "Government Employment and Unemployment: With One Hand Giveth, The Other Taketh, mimeo." Department of Economics University of Strathclyde ICMM Discussion Paper. no. 47. 1998.

Mankiw, Gregory. Principles of Economics. Mason, OH: South-Western Cengage Learning, 2008.

Marron, Donald. "Understanding CBO Health Cost Estimates." Backgrounder: Published by the Heritage Foundation, July 2009.

Mountford, Andrew, and Harald Uhlig. "What Are the Effects of Fiscal Policy Shocks?" NBER Working Paper, no. 14551 (2008).

Office of Management and Budget. Budget of the United States Government, Fiscal Year 2011. Washington, D.C.: U.S. Government Printing Office, 2010.

Payne, Abigail. "Does the Government Crowd-Out Private Donations? Evidence from a Sample of Non- Profit Firms." Journal of Public Economics 69 (1998): 323-345.

Ramey, Valerie. "Identifying Government Spending Shocks: It's All in the Timing." National Bureau of Economic Research Working Paper No. 15464, October 2009.

Romer, Christina. Not My Father's Recession: The Extraordinary Challenges and Policy Respones of the First Twenty Months of the Obama Administration. Washington, D.C.: National Press Club, 2010.

Romer, Christina, and David Romer. "The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks." American Economic Review 100 (June 2010): 763–801.

Romer, Christina, and Jared Bernstein. The Job Impact of the American Recovery and Reinvestment Act. Washington, D.C. : Council of Economic Advisors, 2009.

Romer, David. Advanced Macroeconomics. Boston, MA: McGraw-Hill, 2001.

Snowdon, Brian, and Howard Vane. Modern Macroeconomics: Its Origins, Development, and Current Statei>. Cheltenham, UK: Edwar Elgar Publishing, 2005.

Sobel, Russel, and George Crowley. "Do Intergovernmental Grants Create Ratchets in State and Local Taxes?: Testing the Friedman-Sanford Hypothesis." Mercatus Working Paper, 2010.

Spencer, Roger, and William Yohe. "The 'Crowding Out' of Private Expenditures by Fiscal Policy Actions." Federal Reserve Bank of St. Louis, October 1970.

To speak with a scholar or learn more on this topic, visit our contact page.