The whole Bayer-Monsanto case is a classic example of how a vociferous public debate can disguise or even reverse the true issues at stake.

Bayer’s proposed purchase of Monsanto, the biggest deal of the year so far, has led to a heated public debate over economic concentration. Unfortunately, both sides are failing to identify the key issues behind the potential transaction.

The good news is that the deal announced on Sept. 14 would not increase market concentration by much. Bayer is primarily a pharmaceutical and health care company whereas Monsanto deals in crop chemicals and seeds.

Since Bayer does make biotech products and agricultural chemicals, there is overlap in the markets for cottonseed and canola seeds. But what’s the actual problem from possibly limiting competition in those markets? There are many substitutes for cotton fabrics and canola oil (how many of us could pass a blind taste test for canola versus vegetable oil?).

Critics who dislike Monsanto for its leading role in developing genetically modified organisms and agricultural chemicals shouldn’t also be citing monopoly concerns as a reason to oppose the merger -- that combination of views doesn’t make sense. Let’s say for instance that the deal raised the price of GMOs due to monopoly power. Farmers would respond by using those seeds less, and presumably that should be welcome news to GMO opponents.

It appears that some of the opposition to the deal can be traced to a dislike of the companies involved, especially Monsanto. If that becomes a consideration for U.S. and European Union regulators, it will amount to a worrisome politicization of antitrust policy. Keep in mind that the proposed acquisition needs approval in about 30 different political jurisdictions, hardly a recipe for flexible adjustment to changing marketplace conditions. The shares of Monsanto have been trading well below the offer price, a sign that investors don’t expect the proposal to survive.

Social media has given many companies popular reputations that make it harder to evaluate antitrust deals on an appropriately technocratic basis. That makes it more likely that popular companies will receive favorable treatment from governments while unpopular ones face higher hurdles. Especially in Europe, which has far more anti-GMO sentiment than the U.S., Monsanto is often vilified. Yet running antitrust law by democratic opinion is hardly a good idea, given the complexity of the economic issues involved and the paucity of information before most voters. A significant portion of the electorate, for instance, fails to accept that GMOs have been adjudicated as safe by a wide variety of established experts.

There is a silver lining to this whole mess, however, namely that it may not matter much if the deal falls apart.

What does Bayer hope to get for its $66 billion, $128-a-share offer? The company has argued that it will be able to eliminate some duplicated jobs and expenses, negotiate better deals with suppliers and invest more funds in research and development. Maybe, but the broader reality is less cheery. There is a well-known academic literature, dating to the early 1990s, showing that acquiring firms usually decline in value after tender offers, especially after the biggest deals. Mergers do not seem to make companies more valuable or efficient.

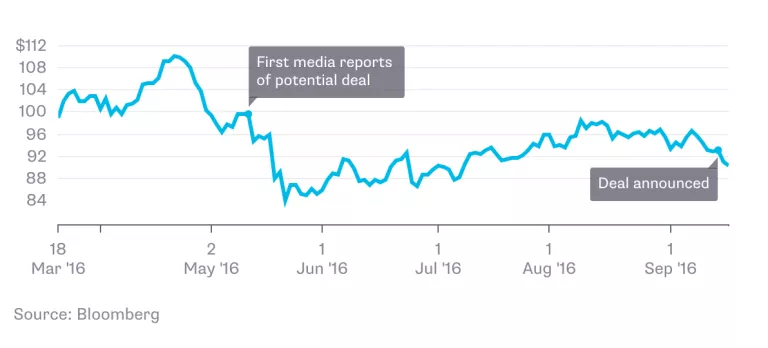

Why then do so many mergers and acquisitions happen? Well, some of them do pay off (Google buying YouTube), but also many managers engage in empire-building by increasing the size of their companies, even at the expense of the shareholders. Another possibility is what economists call “winner’s curse,” namely that the winner of an auction or contest or bidding war tends to be the person or institution most optimistic, and in fact overly optimistic, about the value at stake. Consistent with this view, Bayer’s shares are down since the merger became a media rumor on May 11.

Not Exactly Merger Mania

Bayer's daily closing stock price

The whole Bayer-Monsanto case is a classic example of how a vociferous public debate can disguise or even reverse the true issues at stake. If Bayer fails to close the deal for Monsanto, Bayer shareholders may be the biggest winners. The biggest losers from a failed deal may be its opponents, who will spend the rest of their lives in a world where misguided judgments of corporate popularity have increasing sway over laws and regulations.

That wouldn’t be good for anybody. However the deal turns out, it’s hard to see in the process of considering it a society that is making decisions rationally.