- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Obama Corporate Tax Reform Will Harm U.S. Firms

Obama's plan doesn't constitute reform. Indeed, it introduces as many problems as it hopes to solve.

This article was originally published in the Washington Examiner

President Obama has introduced his corporate tax reform plan to cut the rate to 28 percent from its current 35 percent, while eliminating some tax deductions and expanding others.

Obama would also impose a minimum tax on foreign income of U.S. companies, and create a special rate for manufacturers.

Beyond the fact that the president continues the Washington tradition of picking winners and losers, the plan won't do much to fix our horribly inefficient system.

First, the reduction in the corporate tax rate is a first good step, but it's not enough to put the United States on par with countries with competitive tax rates. Among nations in the Organisation for Economic Co-operation and Development in 2011, the top national statutory corporate tax rates ranged from 8.5 percent in Switzerland to 35 percent in the U.S.

The picture changes only slightly once we add subnational corporate tax rates to the top national rate. Reducing the rate to 28 percent would move the U.S. from the second-highest rate to the fourth-highest rate.

It's unfortunate. A 2002 study by American Enterprise Institute economists Kevin Hassett and Eric Engen made the case effectively that the most efficient corporate tax rate is zero.

The mobility of capital income means that even a small amount of tax introduces large distortions into an economy as capital flies away to a lower tax environment.

More interesting, if counterintuitive, is the fact that because of capital mobility, the people who stand to benefit most from a corporate tax cut are workers.

In a 2006 study, economist William C. Randolph of the Congressional Budget Office concluded that "domestic labor bears slightly more than 70 percent of the burden" imposed by corporate taxes.

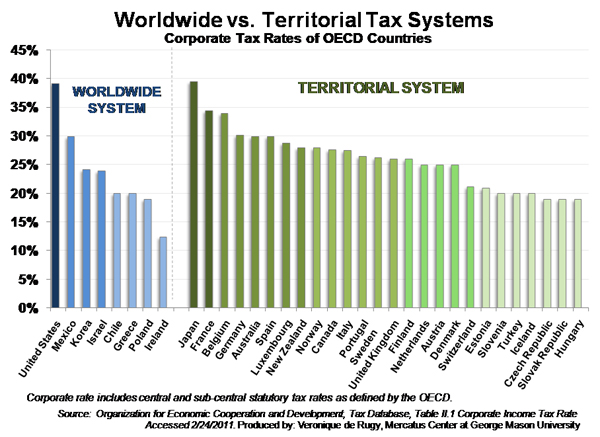

Second, Obama's proposal does nothing to move away from the worldwide income tax. Under the current system, profits made by an American-owned computer plant are subject to U.S. tax whether the plant is located in Texas or Ireland.

Most other major countries do not tax foreign business income as aggressively. In fact, most OECD nations have "territorial" systems that tax firms only on their domestic income.

The combination of high rates and a competitive global marketplace makes the U.S. corporate tax system extremely punishing. Imagine a French firm competing with a U.S. firm for business in Ireland.

The Irish government taxes each subsidiary on its Irish income at the (low) national rate of 12.5 percent. Fair enough. But unlike the French competitor, the U.S. parent company must also register its Irish affiliate's dividends back home as income, which is then taxed.

If the company can meet certain requirements, it can receive a credit for taxes paid to the Irish treasury. But the firm would still have to pay American taxes at the American rate on the Irish income, minus the tax credit. The result is double taxation, costly paperwork and less competitiveness with the French.

These differences have important implications for American companies competing in foreign markets. Because of higher tax costs, U.S.-based firms are losing foreign market share, generating lower returns for American shareholders, and hiring fewer skilled workers back home in the U.S.

Under these conditions, it's no surprise that American multinational companies that want to sell their goods abroad try to keep as much cash out of the U.S. legally as they can. It's a matter of survival.

Other countries understand this. Several nations, most recently including Japan and Britain, are moving to a territorial system, taxing only corporate profits earned within their borders.

By contrast, Obama is proposing to implement a tax on U.S. companies' foreign earnings, making them even more uncompetitive. The tax reform should have lowered the rate much more than it did and moved to a territorial tax system.

Better yet, it should have abolished the corporate tax altogether. Obama's plan doesn't constitute reform. Indeed, it introduces as many problems as it hopes to solve.