- | F. A. Hayek Program F. A. Hayek Program

- | Financial Markets Financial Markets

- | Policy Briefs Policy Briefs

- |

Loans are not Toasters: The Problems with a Consumer Financial Protection Agency

In an effort to correct problems that led to the current housing and mortgage crisis, policy makers have proposed a new Consumer Financial Protection Agency (CFPA) that would have the authority to

In an effort to correct problems that led to the current housing and mortgage crisis, policy makers have proposed a new Consumer Financial Protection Agency (CFPA) that would have the authority to regulate the terms of credit products offered to consumers. The agency's premise is based on the assumption that subprime mortgages are faulty products in need of a recall, similar to faulty consumer products like toasters. This foundation is a simplistic, one-sided view of a dynamic situation. Subprime mortgages are complicated loans that provide variety, choice, and opportunity to homeowners and investors. This Mercatus on Policy will analyze the causes of the foreclosure crisis and counter the prevailing arguments being used to support the creation of the new agency.1

THE FINANCIAL CRISIS IS NOT A CONSUMER PROTECTION ISSUE

The default and foreclosure crisis was caused by misaligned incentives, anti-deficiency laws, and erratic monetary policy. These causes are all safety and soundness issues and not consumer protection issues. Essentially, safety and soundness relates to banks engaging in risky or responsible lending, while consumer protection deals with fraud, deception, and unfair practices in the marketplace.

Unfortunately, policy makers have not made this distinction and have proposed legislation that will create the CFPA.2 As the argument goes, while consumers cannot buy a toaster that has a 20 percent chance of exploding, current federal law permits the existence of subprime mortgages that have a 20 percent likelihood of resulting in foreclosure.3 This over-simplified analogy misses the point. While an unsafe toaster is not suitable for any consumer, an "unsafe" loan might actually be both safe and suitable for a consumer depending on the situation.4

Virtually every credit product—whether credit cards, mortgages, or payday loans—is suitable for some consumers in some situations but not for all consumers in all situations. Borrowers have substantial influence over whether their loans "explode" by responding to incentives and changes in the market. There are appropriate reasons for why a borrower may choose a risky, low-documentation (or even no-documentation) loan. For instance, a borrower who has a high credit score and is seeking to refinance will use a low-documentation loan because it will save her the substantial cost, delay, and inconvenience incurred from using a full-blown refinancing process. Of course, this kind of loan wouldn't make sense for a new borrower seeking a nothing-down, purchase-money loan. Federal regulators cannot successfully hair-split "safe" and "dangerous" loans at these individual levels. Additionally, federal regulators cannot successfully create a one-size-fits-all regulation that encompasses all the components of the mortgage industry and still promotes competition and choice for consumers.

THE FORECLOSURE CRISIS: A CONSEQUENCE OF RATIONAL DECISION MAKING

At the height of the housing bubble, speculative investors throughout the country were encouraged to purchase property and flip it for profit. Such incentives were formed by the combination of zero-down payment, interest-only, adjustable-rate subprime mortgages made available by banks and default-friendly state laws (such as anti-deficiency statutes which limit a bank's recourse to foreclosure with no right to sue the homeowner for any deficiency between the value of the home and the amount owed on the mortgage). As the housing market crashed, the same speculators chose to walk away from the now-underwater homes, further exacerbating the situation. Replicate this scenario several hundred thousand times and a housing and mortgage crisis is born.

Although foreclosures have risen throughout the country, an epidemic exists only in a handful of areas.5 In Las Vegas, Phoenix, Miami, and the Inland Empire region of California, foreclosure rates are five to ten times higher than the national average. These areas saw rampant speculation, which produced price bubbles that have since popped.

A recent study based on a survey of homeowners provides evidence of speculation, finding that one in four mortgage defaults are strategic, rational decisions made by people with the ability to make their payments but choose not to.6 Additionally, moral and social considerations were found to be important variables in choosing to default, for "the social pressure not to default is weakened when homeowners live in areas with high frequency of foreclosures or know other people who defaulted strategically."7 These findings run contrary to the publicized notion that mortgage brokers and financial institutions duped consumers into taking risky mortgages. Treating all consumers as hapless victims rather than recognizing that many consumers do in fact rationally respond to incentives is a recipe for unintended consequences.

THE CASE AGAINST A CONSUMER FINANCIAL PROTECTION AGENCY

A CFPA would not prevent another financial crisis because its goals and objectives do not align with the reality of the financial market. Loans are risky, complex products that cannot be simplified and standardized without hindering consumer well-being. Consumers demand variety, not simplicity. It would be unwise for the hypothetical CFPA to try to elevate simplicity above all else without considering the impact of its actions on competition, innovation, and consumer choice.

Proponents of the CFPA have called for standardized products in order to eliminate loans that appear to be volatile or risky. However, the recent foreclosures occurred because of drastic fluctuations in the actual interest rate. Specifically, the Federal Reserve forced down short-term interest rates during 2001-2004, which encouraged consumers to purchase new homes or refinance with adjustable-rate mortgages, then quickly increased short-term interest rates, causing interest on those mortgages—both prime and subprime—to increase rapidly, thereby increasing monthly payment obligations. It was the Federal Reserve's erratic monetary policy that made adjustable-rate mortgages "explode," not the loans themselves. This may also explain the findings of Stan Liebowitz, a professor of economics at the University of Texas at Dallas: "51 percent of all foreclosed homes had prime loans, not subprime, and that the foreclosure rate for prime loans grew by 488 percent compared to a growth rate of 200 percent for subprime foreclosures."8

Consumer advocates criticize the existence of certain lending terms and practices because of consumer protection issues. Yet, terms like prepayment penalties (fees incurred with paying off a loan early through refinancing at a lower interest rate) attempt to reduce risk and ensure financial soundness. On average, a borrower pays a premium of at least 50 basis points (or 0.5 percent of the amount borrowed) to have the right to prepay her mortgage. Prepayment penalties are more common and even higher for subprime borrowers,9 yet, despite consumer advocate concern, empirical studies have found no link between the presence of prepayment penalty terms and increased foreclosures. However, banning prepayment penalties would result in higher interest rates for riskier borrowers, increasing their risks of default. Moreover, the absence of prepayment penalties in prime mortgages has exacerbated the foreclosure problem by enabling millions of homeowners to engage in cash-out refinances that stripped their equity, resulting in negative equity positions when home prices fell.10

Traditional, fixed-rate mortgages have their own risks, namely higher interest rates and the substantial costs associated with refinancing when interest rates fall. Yet, the proponents of the CFPA apparently insist that the old-style American mortgage should be the gold standard against which all other mortgages would be considered "exotic" or "risky" even though non-traditional loans provide the flexibility and variety demanded by today's consumers, particularly those consumers who would not have access to capital otherwise

This obsession with simplicity above all else threatens innovation as well as competition.11 Innovation is a boon for consumers even if it increases complexity. For example, 30 years ago credit cards were exceedingly simple products: high annual fees just to own the card (often $40-$50), high fixed interest rates (approaching 20 percent), and no benefits (like frequent flyer miles or cash rebates). Today, credit cards are more complex products, reflecting consumer demand for more risk-based pricing and greater benefits. Annual fees have been eliminated for no-frills cards, interest rates are flexible, and behavior-based fees are more prevalent. Competition is fierce, and consumers have a wide selection of cards with different features. The evolution of risk-based pricing in the credit card industry probably would not have succeeded if new innovations had required Uncle Sam's approval.

Additionally, a new stand-alone agency for consumer credit problems would create bureaucratic problems. Governmental agencies tend to expand their jurisdictions.12 The new agency's enforcement authority, which includes the ability to impose massive fines, would have potentially imperiling effects on the safety and soundness of financial institutions by imposing "appropriate" consumer terms. Such actions would inevitably lead to a conflict between the new agency and the safety and soundness oversight authority of the Federal Reserve and the Federal Trade Commission, raising the potential for turf battles and inconsistent policies, which other elements of the financial regulatory overhaul are intended to eliminate.

A BETTER APPROACH GOING FORWARD

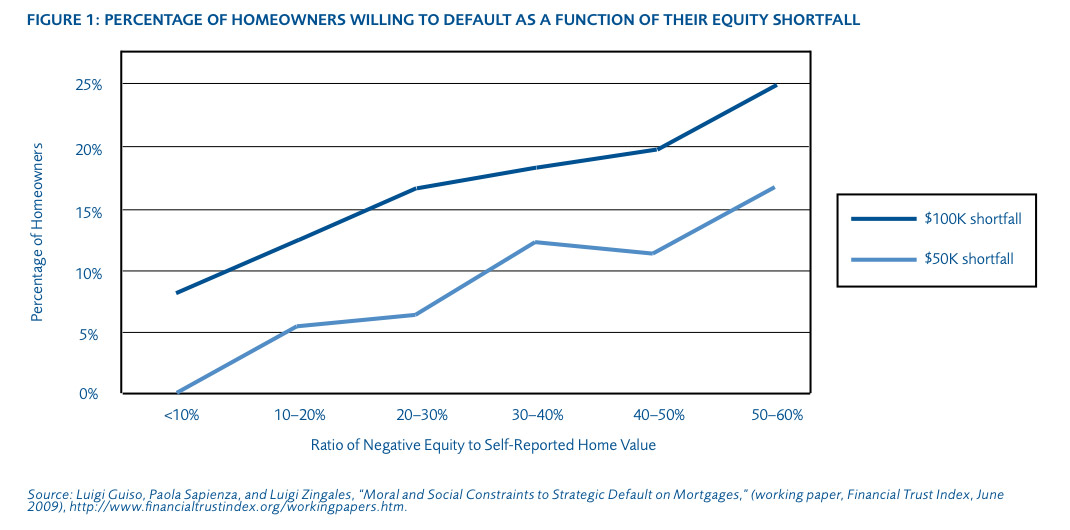

Policy actions relying on the assumption that many households faced an "excessive burden" of mortgage payments, due to ignorance, deception, or misfortune, neither explain nor resolve the common problem of negative equity. Figure 1 illustrates the relationship between negative equity and homeowners' willingness to default. When 22 percent of U.S. households have mortgages greater than the values of their homes, they might be tempted to walk away from their mortgages even if they can afford to pay them.13 Thus, policy makers must focus on the rational decisions made by homeowners, speculators, and lenders in order to reform the incentives and prevent further meltdown of the financial sector.

Instead of a new Consumer Financial Protection Agency, Washington should first look to revise and simplify its current policies and the incentives formed by such policies. Some areas in need of reform include disclosure mandates, the tax structure and other incentives that encourage overinvestment in housing, and the incentives for homeowners to walk away from foreclosure. Government policies in these areas are complex, confusing, and can result in unintended consequences. The Federal Trade Commission (FTC) would be well-suited for this undertaking, as it has a longstanding expertise in the financial market and the ability to account for the effects reforms have on competition and innovation.

CONCLUSION

Despite current rhetoric, the housing and mortgage crisis is one of misaligned incentives and the rational response of consumers and lenders to those incentives, not a crisis of consumer protection. A new agency premised on the erroneous belief to the contrary is likely to do more harm than good. Instead of creating a new ineffective, or possibly even damaging, bureaucracy, policy makers should review and modify the prevailing regulations that prompted this crisis.

ENDNOTES

1. For more information on this topic, see Todd J. Zywicki, "Let's Treat Borrowers Like Adults: The problems with a financial products safety panel," The Wall Street Journal, July 8, 2009, http://online.wsj.com/article/SB124701284222009065.html; Todd J. Zywicki, "Testimony on the Consumer Financial Protection Agency: Banking Industry Perspectives on the Obama Administration's Financial Regulatory Reform Proposals," Congressional Testimony, United States House of Representatives Committee on Financial Services, July 15, 2009, http://www.mercatus.org/uploadedFiles/Mercatus/Publications/CFPA%20Todd….

2. Find out more about the Consumer Financial Protection Agency Act of 2009 at http://www.financialstability.gov/latest/tg189.html. The idea is the brainchild of Elizabeth Warren, a Harvard law professor and Chair of the Congressional Oversight Panel for the Troubled Assets Relief Program, and has also been supported by leading policymakers. Also an overview of the agency and who supports it can be found in Kenneth R. Harney, "Consumer Financial Protection Agency: An Overview," The Los Angeles Times, August 2, 2009, http://www.latimes.com/classified/realestate/news/la-fi-harney2-2009aug….

3. Elizabeth Warren, "Unsafe at Any Rate: If it's good enough for microwaves, it's good enough for mortgages. Why we need a Financial Product Safety Commission," Democracy: A Journal of Ideas, Issue #5 (Summer 2007), http://www.democracyjournal.org/article.php?ID=6528.

4. The federal agency that regulates items such as toasters—the Consumer Product Safety Commission (CPSC)—relies primarily on the use of voluntary standards to promote product safety. The proposed framework of the CFPA would take a much greater "command and control" approach to regulation than the CPSC. Notably, in instances where the CPSC has exercised its regulatory authority, it has often created significant unintended consequences. See: W. Kip Viscusi, "Consumer Behavior and the Safety Effects of Product Safety Regulation," Journal of Law and Economics 28.3 (1985): 527-553, http://www.jstor.org/stable/725345.

5. See the interactive database on housing prices and foreclosures at http://www.zillow.com/local-info/#metric=mt%3D5%26dt%3D1%26tp%3D5%26rt%…. Also see a report on foreclosures at http://www.realtytrac.com/ContentManagement/PressRelease.aspx?channelid….

6. Luigi Guiso, Paola Sapienza, and Luigi Zingales, "Moral and Social Constraints to Strategic Default on Mortgages," (working paper, Financial Trust Index, June 2009), http://www.financialtrustindex.org/workingpapers.htm.

7. Ibid, 22.

8. Stan Liebowitz, "New Evidence on the Foreclosure Crisis: Zero money down, not subprime loans, led to the mortgage meltdown," The Wall Street Journal, July 3, 2009, http://online.wsj.com/article/SB124657539489189043.html.

9. Prepayment premiums are higher for subprime mortgages because of the risk of refinancing due to the improved credit scores of borrowers in addition to refinancing due to fluctuations in the market interest rate.

10. Kelly D. Edmiston and Roger Zalneraitis, "Rising Foreclosures in the United States: A Perfect Storm," Economic Review, 4Q: 2007, Federal Reserve Bank of Kansas City, http://www.kc.frb.org/PUBLICAT/ECON-REV/PDF/4q07Edmiston.pdf, 130-131.

11. A supporting idea is found in Peter Boettke, "What Happened to 'Efficient Markets'?" (working paper 09-22, Mercatus Center at George Mason University, June 2009), http://www.mercatus.org/uploadedFiles/Mercatus/Publications/WP0922_What…

12. Gordon Tullock uses the term "bureaucratic imperialism" to refer to the tendencies for government departments, agencies, and entire bureaucracies to expand through increasing their workforce or "raiding the trains of other rival politicians." Gordon Tullock, "Bureaucracy: The Selected Works of Gordon Tullock, Volume 6," The Politics of Bureaucracy (Indianapolis: Liberty Fund, 2005), 145-147.

13. Guiso, Sapienza, and Zingales, 21.

To speak with a scholar or learn more on this topic, visit our contact page.