- | International Freedom and Trade International Freedom and Trade

- | Policy Briefs Policy Briefs

- |

A Trivial Legal Issue with Nontrivial Economic Consequences

Why Raising De Minimis Thresholds Is Important for International Trade

Traditionally, imports of small-value items have been too trivial to merit customs consideration. These are considered de minimis, an important legal and economic term with Latin roots meaning “about minimal things.” In international trade, the de minimis threshold (DMT) is a valuation ceiling. For goods valued below the DMT, no duties are charged, and clearance procedures and data requirements are minimal. Shipments valued above the threshold are subject to duties, taxes, and time-consuming clearance procedures, which are costly and burdensome regulations that impose delays on consumers and businesses.

The cost of compliance and clearance procedures for minimal-value parcels can easily outweigh the tax and duty revenues these shipments generate. If set too low, de minimis thresholds can impose nontrivial costs on governments, consumers, and businesses.

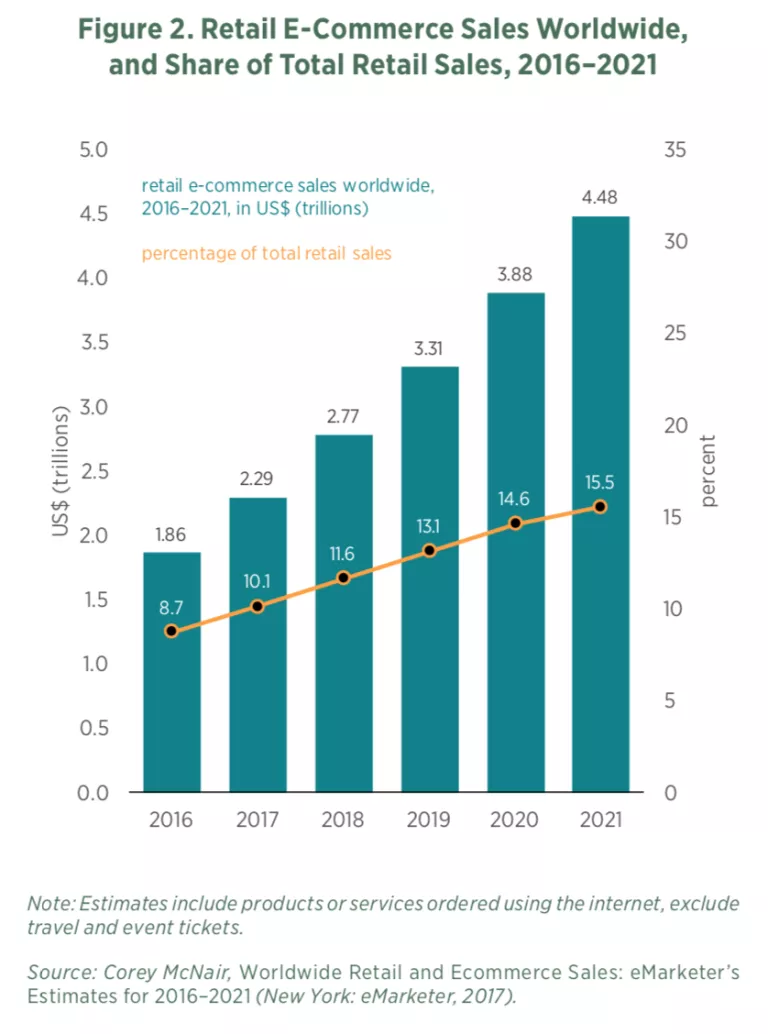

Today’s modern global economy brings new meaning and relevance to de minimis thresholds. International e-commerce is growing, and largely consists of direct business-to-consumer (B2C) sales and relatively low-value parcels. The estimated value of international e-commerce was $2.3 trillion in 2017, up from $1.3 trillion in 2014, and is expected to reach nearly $4.5 trillion by 2021.

The DMT in the United States is one of the highest in the world, at $800, but the DMTs for many US trading partners are still quite low, such as $20 in Canada and $50 in Mexico.

A de minimis threshold that is too low can be a barrier for international trade, particularly global e-commerce, which is an important growth avenue for small and remote businesses. The following analysis demonstrates that a higher threshold would improve efficiency in customs procedures, lower costs for consumers and businesses, and remove a barrier for US small businesses in the global marketplace. Higher thresholds should remain a priority when modernizing the North American Free Trade Agreement (NAFTA), receive full consideration in the World Trade Organization’s recently announced work program on electronic commerce, and be included in all free trade agreements moving forward.

A DMT That Is Too Low Is Costly and Impedes Trade

The geographic distance between economic agents (buyers and sellers) increases a number of transaction costs: the transport costs of shipping goods, the time cost of shipping, the costs of contracting at a distance, and search costs (i.e., acquiring information about remote economies, buyers, and sellers). The economic effects of distance have been quantified since at least the mid-20th century.

Digital platforms, however, may be able to reduce distance, or at least the economic effects of distance, in international trade. Using a unique dataset on cross-border transactions conducted over eBay, the world’s largest online marketplace, Lendle and his coauthors examine the effect of distance on international online trade. The authors find that the effect of distance on trade is 65 percent smaller on eBay than through traditional marketplaces. They argue that technology, namely, online markets and digital platforms, can reduce the economic distance between the buyers and sellers by reducing search costs.

A de minimis threshold that is too low, however, threatens to limit the progress that technology and digital platforms can offer.

To understand the cost of low thresholds, consider a typical parcel that is valued above the de minimis threshold. Customs officials expend resources to assess the parcel’s value (for duties and taxes), to ensure the paperwork is complete, and to ensure the taxes and duties are paid (or to send out a notice to the recipient with the corresponding invoice). The consumer incurs brokerage fees, the time costs of delay, and the actual tax and duty. The business, as the importer, incurs the brokerage fee, the time costs of delay, the cost of administrative tasks such as claiming a tax credit if one applies (e.g., if the import was an intermediate input), and the actual tax and duty.

In principle, the costs of a tax borne by all affected economic agents almost always exceed revenues received for any tax. This principle holds regardless of the size of the transaction because of collection and enforcement costs added to the tax paid. In the case of the de minimis threshold, the costs are excessive and nearly everyone is worse off with the tax (even the government), especially when the value of an item is relatively low.

These costs tend to fall more heavily on small businesses. Smaller firms are more likely to import in small batches, and they have fewer resources than large firms to expend on administrative tasks. They therefore face a disproportionately high cost of compliance with import procedures and low-value parcels.

Studies on the economic effects of raising the de minimis threshold generally find that higher thresholds offer net economic benefits. For instance, Hufbauer and Wong studied the US de minimis threshold in 2011—before the 2016 increase—and found that the loss of tariff revenues and fees was more than offset by the savings to stakeholders in the delivery chain.

A study by International Trade Strategies estimated the effects of raising the de minimis threshold for 12 Asia-Pacific Economic Corporation countries and found net economic benefits from raising the threshold. The European Union has a $170 threshold for the customs duty and a much lower threshold ($17–$25, depending on the country) for the federal value-added tax (VAT). Hinsta and coauthors found that the VAT threshold for imports should be raised because collection costs incurred by customs officials and the private sector exceeded the revenues collected.

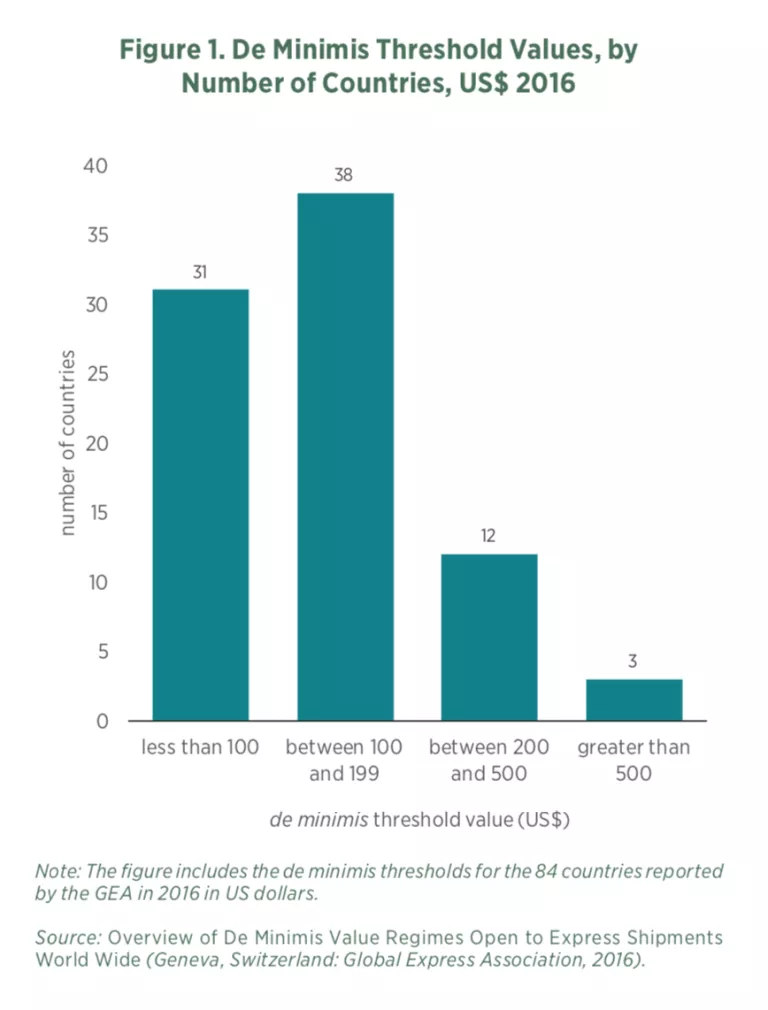

Few Countries Meet the ICC Recommendation of a De Minimis Value of at Least $200

The International Chamber of Commerce (ICC) recommends establishing a global baseline de minimis value of at least $200—and ideally $1,000—in order to “generate economic benefits by refocusing public revenue collection on more efficient revenue sources.” The ICC states that setting a meaningful de minimis level will have a positive impact on small and medium-sized enterprises and offer opportunities for increased e-commerce. These guidelines are only a suggestion, however, and countries are free to set their own thresholds.

The US de minimis threshold increased from $200 to $800 in 2016 with the US Trade Facilitation and Trade Enforcement Act of 2015 (which included an amendment to the Tariff Act of 1930). This change took effect in March 2016. The US DMT of $800 is one of the highest in the world (only Qatar has one higher, with a DMT of $822).

Empirical Evidence from Canada

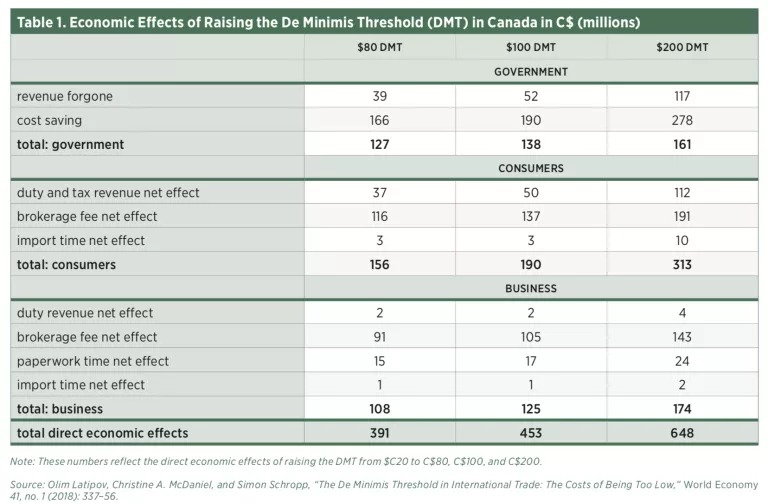

Canada has one of the world’s lowest de minimis thresholds, at C$20 (US$ 16). Customs and shipping experts estimate that the customs administration cost of the assessment process is US$38.74 for air and land cargo per parcel and US$48.19 for sea cargo per parcel for Canada. With duties averaging 2.4 percent for Canada, on average C$1.20 is collected for duties; and, with a Goods and Services Tax (GST) of 5 percent, C$2.50 is collected in taxes. In other words, on a per-parcel basis, the government is spending US$38–US$48 (C$47–C$60) to collect C$3.70.

As shown in table 1, Latipov and coauthors find that by keeping the DMT at C$20 instead of, say, C$80, the government of Canada is spending C$166 million to collect C$39 million (first column, top two rows). Similarly, by keeping the DMT at C$20 instead of raising it to C$200, the Canadian government is spending C$278 million to collect C$117 million (last column, top two rows).

The authors examine the direct effects of raising Canada’s DMT from C$20 to a higher level (C$80, C$100, and C$200). They use a unique dataset, including transaction-level data from eBay Canada and data from the GEA. These data allow them to identify the distribution of parcels across various consignment values, and the split between inbound parcels handled by Canada Post and express couriers. The ability to accurately identify the distribution of parcels across consignment values, as well as the split between the postal service and express couriers, is a key component to empirical work in this area.

Their results indicate that increasing the DMT in Canada would have clear benefits for consumers and businesses, particularly small and medium-sized businesses, because the cost savings for smaller entities are disproportionately large. The effects on the government would be fiscally neutral or positive depending on how the government utilized or redirected the freed-up resources.

For instance, in one scenario, the government realizes the cost savings internally, such as through a redeployment of government priorities or a more efficient allocation of resources (the assessment rate of higher-value parcels does not change). These results are shown in table 1. In another scenario, the freed-up resources are used to increase assessments of the higher-value parcels. Overall, there are net cost savings in each scenario.

The authors consider a range of alternative higher thresholds (summarized in table 1). They find that raising Canada’s DMT to just C$80 would yield C$391 million in government savings, consumer savings, and business savings.

The results reflect the relative inefficiency of de minimis assessments. Raising the DMT can alleviate these inefficiencies and yield benefits such as cost savings from a reduction in brokerage fees, costly import delays, and administrative costs for government.

Cross-Border E-Commerce Growth Puts Spotlight on De Minimis

The de minimis threshold is not a new international trade policy issue. Nearly two decades ago, the 1999 Revised Kyoto Convention acknowledged the e-commerce trend of increasing numbers of small consignments, and included a provision on de minimis values.

Recent growth in e-commerce, however, has returned de minimis to the spotlight. In the United States, according to Census data, the e-commerce share of retail sales has grown from 4 percent in 2010 to 8.4 percent in 2017. If cars, gasoline, restaurant meals, and other items that people generally do not buy online are excluded, those figures become 9.5 percent for 2010 and 21 percent for 2017. Retail e-commerce sales have grown worldwide and are expected to continue to grow in absolute and relative terms (figure 2).

The growth in e-commerce has also increased the issuance of federal and state taxes on sales from remote sellers. The treatment of de minimis imports in terms of sales taxes is discussed in Box 1.

E-commerce can be an important market access tool. PayPal reports that over 65 percent of its US-based merchants engage in international trade, whereas Census data show that, in general, less than 5 percent of US firms export. This striking difference reflects the potential of digital platforms and cross-border e-commerce, particularly for small businesses that may not otherwise reach foreign markets and would be otherwise confined to the ups and downs of their local economies.

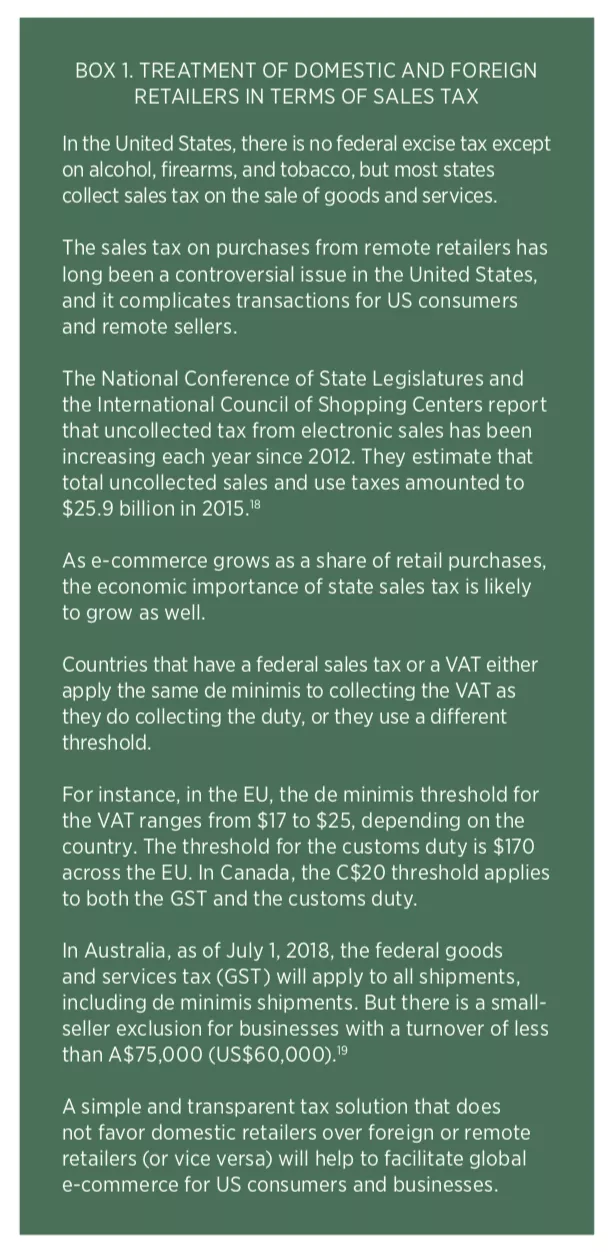

In the United States, there is no federal excise tax except on alcohol, firearms, and tobacco, but most states collect sales tax on the sale of goods and services.

The sales tax on purchases from remote retailers has long been a controversial issue in the United States, and it complicates transactions for US consumers and remote sellers.

The National Conference of State Legislatures and the International Council of Shopping Centers report that uncollected tax from electronic sales has been increasing each year since 2012. They estimate that total uncollected sales and use taxes amounted to $25.9 billion in 2015.

As e-commerce grows as a share of retail purchases, the economic importance of state sales tax is likely to grow as well.

Countries that have a federal sales tax or a VAT either apply the same de minimis to collecting the VAT as they do the duty, or they use a different threshold.

For instance, in the EU, the de minimis threshold for the VAT ranges from $17 to $25, depending on the country. The threshold for the customs duty is $170 across the EU. In Canada, the C$20 threshold applies to both the GST and the customs duty.

In Australia, as of July 1, 2018, the federal goods and services tax (GST) will apply to all shipments, including de minimis shipments. But there is a small-seller exclusion for businesses with a turnover of less than A$75,000 (US$60,000).

A simple and transparent tax solution that does not favor domestic retailers over foreign or remote retailers (or vice versa) will help to facilitate global e-commerce for US consumers and businesses.

Conclusion

A too-low de minimis threshold can be a barrier for international trade, particularly global e-commerce, which is an important growth avenue for small and remote businesses. Research suggests that, based on assessment costs alone, many of America’s largest trading partners have thresholds that are too low.

Higher thresholds would improve efficiency in customs procedures, lower costs for consumers and businesses, and remove a barrier for US businesses, especially small or remote US businesses, in the global marketplace.

One of America’s largest trading partners, Canada, has one of the lowest thresholds in the world, and studies on Canada show that a higher threshold would yield economic benefits for Canadian consumers, businesses, and even the government.

Locking in higher thresholds should remain a priority for trade negotiators as they seek to modernize NAFTA, and should be included in all free trade agreements moving forward.