- | Corporate Welfare Corporate Welfare

- | Data Visualizations Data Visualizations

- |

The Export-Import Bank’s Small Business Program Supports Big Companies

Among its four principal financial products, the Export-Import Bank has provided “working capital” loans and loan guarantees that assure repayment to private lenders in the event a borrower defaults. According to bank officials, this form of subsidized financing “primarily” benefits small business. In a July 16 letter to Sen. Marco Rubio and others, Ex-Im president Fred Hochberg characterized the bank’s working capital financing as “issued to mostly small businesses.”

Among its four principal financial products, the Export-Import Bank has provided “working capital” loans and loan guarantees that assure repayment to private lenders in the event a borrower defaults. According to bank officials, this form of subsidized financing “primarily” benefits small business. In a July 16 letter to Sen. Marco Rubio and others, Ex-Im president Fred Hochberg characterized the bank’s working capital financing as “issued to mostly small businesses.”

But as is the case with a great many claims from Ex-Im officials, the data tell a different story.

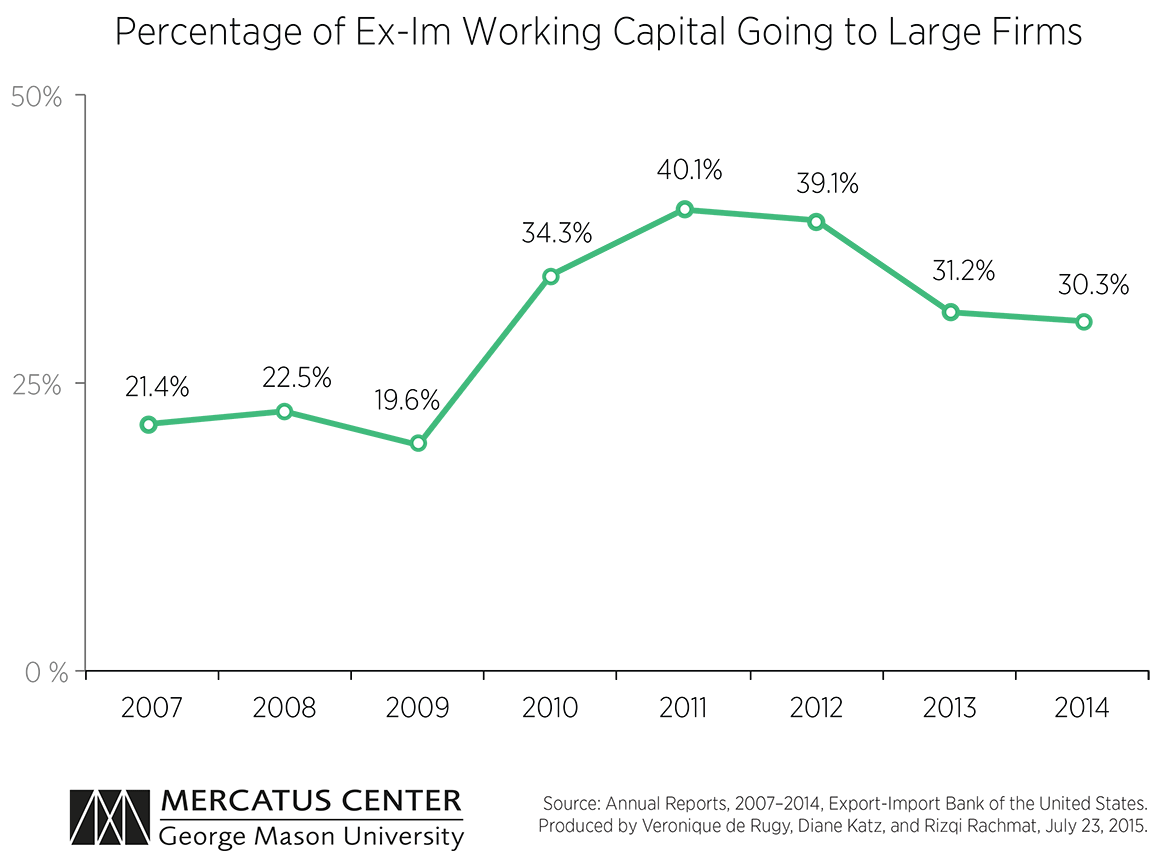

According to the Ex-Im Bank’s definition, a small businesses can have as many as 1,500 employees and up to $21.5 million in revenue. However, the data show that as much as 40 percent of the bank’s working capital loans and loan guarantees in a single year has benefitted large corporations with impressive market capitalization, as the chart above illustrates. (The data were derived from the Ex-Im Bank’s annual reports, and do not include the “supply chain finance program.”) This finding documents yet again that bank officials vastly overstate Ex-Im assistance to small business.

Between 2007 and 2014, large corporations—rather than small businesses—collected between 19.6 and 40.1 percent of the Ex-Im Bank’s working capital loans and guarantees. These included two transactions totaling $711.5 million for Boeing Co. (the Bank’s No. 1 beneficiary, with a market cap of $108.8 billion) and three transactions totaling $850 million for Ford Motor Co. (with a market cap of $58.5 billion). So it’s a real stretch to claim a program “primarily” benefits small business when major companies consistently collect a third or more of the benefits.

Lenders offer lower rates when loans and loan guarantees are backed by US taxpayers—up to 90 percent of principal and interest are backed by taxpayers in the case of working capital guarantees. That gives beneficiaries of the Ex-Im program a significant competitive advantage over firms that don’t have access to these cheaper loans. Other Ex-Im programs primarily finance foreign companies and countries. But the working capital program largely finances US firms, which means their domestic counterparts are put at an increased disadvantage.

The lapse of the Ex-Im charter on June 30 means that the bank is prohibited from awarding any new loans or loan guarantees. But the bank’s proponents—principally big corporate interests—remain committed to winning reauthorization. In hopes of doing so, they will continue to claim that small business is the bank’s “core mission.” Don’t believe it. The truth is that a substantial share of the Ex-Im Bank’s benefits go to large, politically favored corporations.