- | Government Spending Government Spending

- | Federal Testimonies Federal Testimonies

- |

Can Budget Process Reforms Produce Better Budget Outcomes?

Testimony before the Senate Committee on the Budget

Today I will comment on “wasteful and duplicative spending,” and discuss how better, more transparent budget processes are the first step, but not the solution, to controlling such spending. I would like to make three main points. First, changing the focus to the desired outcomes in the budget process is essential to controlling duplicative spending. Second, comparing the results of all activities that impact the same outcome is critical in allocating resources to the most effective activities and maximizing outcome achievement. And third, budget procedures matter when it comes to controlling spending, based on evidence from state governments and overseas.

Chairman Enzi and Ranking Member Sanders, I am honored to have been invited to testify before you on process and procedural options for reforming the budget process.

I am a vice president at the Mercatus Center at George Mason University. My work there over the last 15 years has focused on mechanisms that would improve the quality of governance in America. Prior to this, I served as an elected member of the New Zealand Parliament and a member of the Cabinet of New Zealand, and was then appointed New Zealand’s ambassador to Canada. The New Zealand government implemented a series of reforms to budget procedures when I served as a legislator. Canada made major changes to its budget processes during my tenure there. My comments today will draw on my research, as well as these experiences, and on research that we have done at the Mercatus Center on budget procedures throughout the United States.

Today I will comment on “wasteful and duplicative spending,” and discuss how better, more transparent budget processes are the first step, but not the solution, to controlling such spending. I would like to make three main points. First, changing the focus to the desired outcomes in the budget process is essential to controlling duplicative spending. Second, comparing the results of all activities that impact the same outcome is critical in allocating resources to the most effective activities and maximizing outcome achievement. And third, budget procedures matter when it comes to controlling spending, based on evidence from state governments and overseas.

US Efforts in Improving Performance Information to Inform Spending Levels

Over the last 25 years, many national, state, and provincial governments have experimented with changes to their budget processes and procedures—with varying levels of success. In nearly every case the objective of the reforms has been to develop a closer relationship between the outcomes of government spending and future appropriation decisions. While there are many instances where government agencies have significantly improved their ability to produce quality, outcome-oriented performance information, the initiatives have frequently stumbled at the spending decisions made by legislatures.

Not the least of these frustrations was the American experience with the Government Performance and Results Act (GPRA) and its later iterations. Mercatus conducted an annual evaluation of the Annual Reports of the 24 Chief Financial Officers Act agencies for the first 10 years of GPRA. In the initial years Annual Reports produced very poor quality performance information. But at the end of the 10 years, all agencies had dramatically improved the quality and the clarity of their reporting, with some agencies consistently producing excellent reports. The disappointing finding with the evaluation of 10 years of the Annual Reports was that this quality performance information was hardly ever used to inform the appropriations process. So changed procedures will not, on their own, improve budget decision-making if the legislature does not change its practices as well. However, better budget processes that more starkly demonstrate the options available to appropriators—and the consequences of each of the options—may well change the incentives for appropriators.

Controlling Duplicative Spending by Focusing on Outcomes

Successfully limiting duplicative and wasteful spending requires a change in the thought process behind budget decision-making. This means moving away from funding an activity or program and instead focusing on funding the outcome desired by policymakers. It is this concept that led the New Zealand Parliament to reorganize its committees and change the Financial Reporting Act so that parliamentary select committees had direct oversight of sectors of the economy instead of departments and programs. Under this new arrangement the Education and Science Committee examined all activity that was focused on education, regardless of which agency delivered the program. Under this arrangement the committee oversaw all education programs, could identify which were the most effective, which were the least effective, and how much each cost per unit of success. This enabled appropriators to strategically allocate resources to achieve the greatest public benefit. Parliament was able to eliminate outdated and redundant activity.

To shift the budget focus to outcome achievement, appropriations in New Zealand are now converted to purchase agreements that spell out precisely what the government expects in outcome results for this investment. For example; this investment of $XXX will buy an increase of 10 percent in ten-year-olds who are reading at their biological age. The purchase agreement is a binding contract between the CEO of the agency and the government. Failure to deliver the commitments in the contract could lead to the termination of the CEO’s employment.

Wasteful and duplicative expenditure is best controlled by ensuring that all activities addressing a common outcome have to compete for a common pool of money in the appropriations process. Reorganizing existing budget accounts by mission or objective could help policymakers and the public better relate costs to results.

Getting Spending Under Control: Experience in the States

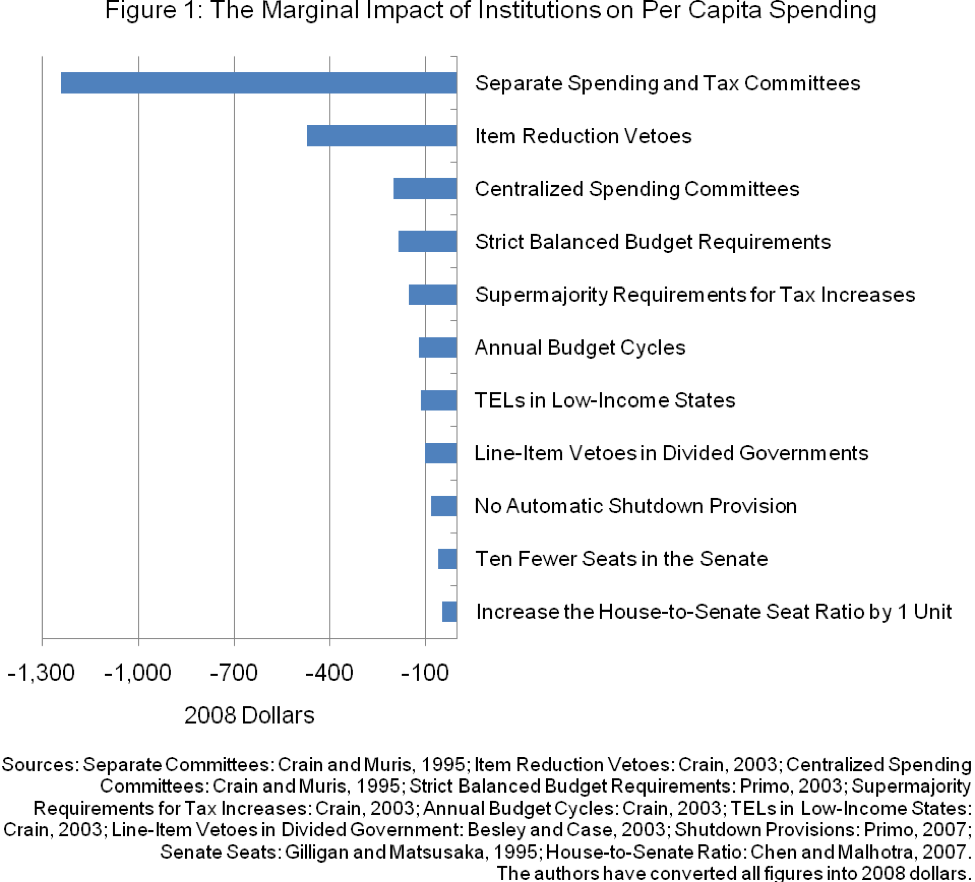

Research conducted by Matt Mitchell and Nick Tuszynski and published by the Mercatus Center examined differing budget procedures across the 50 states. (The study is attached to this testimony as an appendix.) They found that different budget procedures had a significant effect on per capita spending in the state concerned, as demonstrated in the example below and in figure 1.

Merely having different committees that consider taxing and expenditure separately reduces per capita spending by $1,241. And having a line item reduction authority reduces spending by $471 per capita. To put these figures in perspective, 2008 state and local per capita expenditures averaged approximately $5,708.

Thus, the studies we review suggest that these institutions can decrease per capita spending up to 22 percent. It is clear that Justice Brandeis’s “experiment” has yielded economically significant results.

Overseas Trends

Governments in other countries, driven by dissatisfaction with outcomes from existing practices, have been debating and legislating different budget procedures.

Many are starting the budget process early by separating budget policy and economic strategy from spending by publishing a budget policy and strategy document as many as six months before the budget. The goal is to allow extensive debate on these issues prior to the appropriation process.

Some have shortened the time for the appropriation process (New Zealand’s is only 12 weeks) since many of the contentious issues have already been debated. As each of these countries has a parliamentary system, the consequence for not passing the budget is an immediate new election.

There is a trend to much greater transparency throughout these new procedures, and they have developed statutes that make it more difficult for governments to depart from established procedures and requirements. Some, like Ireland, have set up independent bodies to comment on how well the government is meeting fiscal and budget requirements.

The following are summaries of laws from different countries that give a picture of some initiatives. (Appendix I gives more detail on each of the laws referenced.)

Australia: the Charter of Budget Honesty Act 1998. This was the Australian response to the frustration felt by incoming governments that the country’s fiscal position after an election was often much worse than had been portrayed during the election.

Ireland: the Fiscal Responsibility Act. This was a response to the perceived fiscal nonaccountability of successive governments. This law did something extraordinary—it set up the statutorily independent Irish Fiscal Advisory Council. The council’s job, as laid out in the statute, is to comment quite specifically on whether the government is acting in a fiscally responsible manner.

New Zealand: the Fiscal Responsibility Act and the Financial Reporting Act. These laws, and a number of others, were responses to decades of highly inept fiscal management that led the country to the verge of bankruptcy in the early 1980’s. “Having cleaned up the mess, don’t let it happen again” probably best describes the rationale driving the compendium of fiscal and operational laws passed in New Zealand.

Conclusion

There exists a huge volume of research and real world experience, both in the United States and overseas, on the subject of budget processes and procedures. My testimony has touched very lightly on a number of the initiatives currently in practice to identify options that might be attractive to the Senate. What can be said with certainty is that more transparent procedures, a linkage between agency performance and future budget allocations, and a focus on measuring progress against outcome achievements all appear to be goals of these initiatives. It could also be said that there appears to be a cultural shift within these nations to a greater appreciation of the importance of keeping spending and debt within predetermined parameters that define fiscally responsible behavior.