- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Hyperinflation and Seignorage in Venezuela

Venezuela’s socialist “Bolivarian Revolution” began unfolding about 20 years ago, in 1999 (see table 1). The expansion of state ownership of the means of production has translated into a move away from market-based production. With government controls on capital inflows and outflows, or capital controls for short, reports of extremely high rates of inflation, known as hyperinflation, have surfaced, even as the government has recently stopped reporting an official measurement of price inflation. The data used here suggest that the hyperinflation began in November 2016, and the Banco Central de Venezuela (BCV) began introducing new, larger-denomination notes shortly after that. The recent hyperinflation reflects the so-called fiscal dominance of monetary policy: the fact that in the face of high budget deficits, monetary policy adjusts to meet fiscal objectives, providing a way to pay for the gap between spending and revenue.

Ordinarily, a government may fund expenditures through current tax revenues, by issuing bonds that must be paid back with future tax revenues, or through central bank seignorage. In the United States, the Federal Reserve (Fed) reports seignorage as the interest savings offered to the government when it holds the Treasury’s debt on its balance sheet and returns the interest income earned from holding that debt after the Fed pays its expenses. For many countries, seignorage data is not publicly available, but by defining seignorage as the face value of new issuances of the currency (minus the cost of producing it, for which data are generally not publicly available), it can be estimated from central bank monetary statistics as the change in the stock of money deflated by a measure of the value of real goods and services.

Seignorage revenues reflect two forces that may work against each other during a period of hyperinflation (namely, the government’s desire to generate revenues to fund expenditures and also the public’s willingness to use the currency). During a hyperinflation, as the government relies more on seignorage, the public may be less willing to use the currency, which accordingly loses value.

The revenue-generating component of seignorage can be thought of as an “inflation tax.” In this case, the public’s holdings of the currency serve as the tax base, while the rate of inflation serves as the tax rate, since a higher rate of inflation implies that the government extracts more revenue, holding everything else constant. At the same time, the amount of revenue generated may be limited by the public’s willingness to hold those real money balances, since higher inflation rates result in the public holding fewer real money balances. This policy brief offers a summary of Venezuela's hyperinflationary experience viewed through the parallel foreign exchange market and a summary of the BCV’s seignorage-generating activities, before briefly discussing policy options.

The reason for focusing on the parallel market is that in hyperinflating economies, the constant downward pressure on the local currency’s purchasing power creates incentives for people to convert any local currency holdings into other assets (e.g., real estate, Bitcoin, US dollars, or other foreign currencies). That implies that increases in the volume of currency in circulation transmit first to exchange rates and then later to prices, as suggested by Jacob Frenkel’s monetary model of the exchange rate (MMER). Moreover, when governments institute capital controls, that tends to create incentives for currency to be traded in black or parallel markets, whereby the actual market exchange rate quotes differ from the official exchange rate quoted by the central bank. In a hyperinflationary environment, if the government maintains a rigid official exchange rate, demands for foreign currency in the black or parallel market will mean that the value of the local currency will continue to plunge, such that each unit of a particular foreign currency can be exchanged for an increasing number of units of domestic currency.

Data

In a period of hyperinflation, official price inflation estimates can become less reliable, and in Venezuela, the official consumer price index was last reported by the BCV in December 2015. Alternative inflation measures exist. To measure inflation in Venezuela, DolarToday offers a commonly used measure of the parallel market rate based on, among other things, local parallel market rates and even Bitcoin transactions. In 2017, Inflacion Verdadera began computing an alternative measure based on retail prices using a variant of the method applied by the Billion Prices Project; in this variant, individuals can use a cell phone app to send prices to Inflacion Verdadera, which then compiles a daily index of prices by product type. Finally, a third measure, the Café con Leche index, derives from the price of a cup of coffee in Caracas.

Data for the monetary series come from the monthly data series available from the BCV’s website. In the rest of this brief, I show the price index series, examine changes in note denominations, examine seignorage, and conclude.

Alternative Price Index Proxies

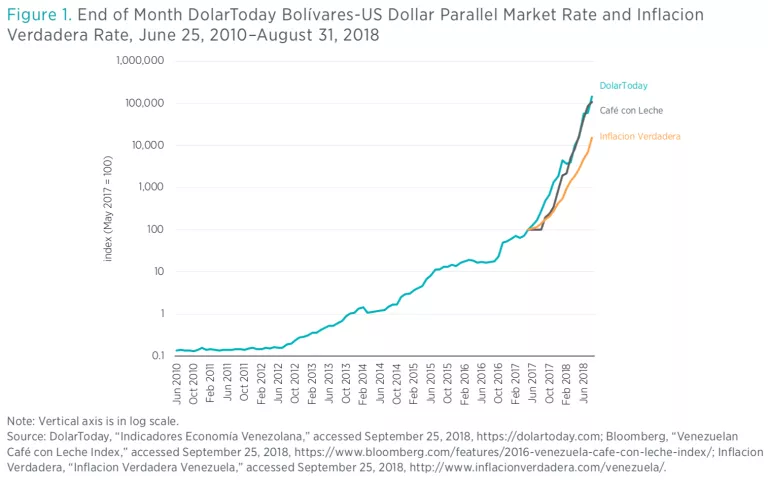

In terms of the dollar rates, figure 1 depicts the monthly DolarToday rate from June 2010 through August 2018. The base value, equal to 100, occurs in May 2017. On August 16, 2018, the BCV reissued the currency while dropping three zeroes from notes. However, I add the zeroes back after that date to preserve the trend, given that removing zeroes does not alter the currency’s purchasing power. The figure also includes the Café con Leche rate and the Inflacion Verdadera rate from May 2017 through August 2018 and suggests that the DolarToday and Café con Leche rates are similar and have outpaced the Inflacion Verdadera rate. In this sense, the DolarToday rate offers an “upper bound” estimate, while the Inflacion Verdadera rate offers a “lower bound” estimate.

Monthly Note Supply by Denomination

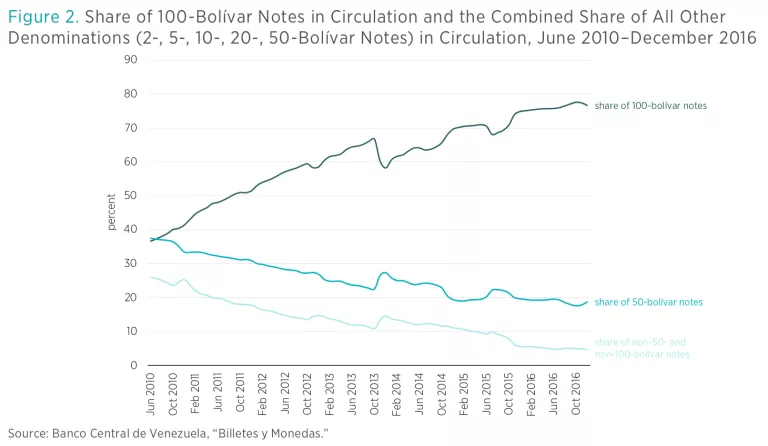

One aspect of the note-printing history in Venezuela that deserves attention is that the note denominations were fixed through late 2016. At the same time, the share of 100-bolívar notes grew to prominence starting in December 2009, when it surpassed 30 percent of the stock of currency in circulation. Figure 2 depicts the share of the stock of currency in circulation comprised of 100-bolívar notes, 50-bolívar notes, and the combined share of 2-, 5-, 10-, and 20-bolívar notes from June 2010 through December 2016. By December 2016, 100-bolívar notes exceeded 75 percent of the stock outstanding.

In January 2017, the BCV began reporting newly introduced denominations including 500-, 5,000-, 10,000-, and 20,000-bolívar notes, just as the hyperinflation began unfolding. By March 2017, the BCV began reporting 1,000- and 2,000-bolívar notes, and in November 2017, the BCV began reporting 100,000-bolívar notes. In February 2018, the government announced it would introduce a petrol-based cryptocurrency as an alternative to bolívares. In August 2018, the old currency was reissued with five zeroes removed, while issuances of new higher-denomination notes expanded that stock of currency nearly tenfold. With this brief summary of price index and currency-in-circulation trends, I now turn to seignorage revenue generation.

The Real Seignorage Breakdown

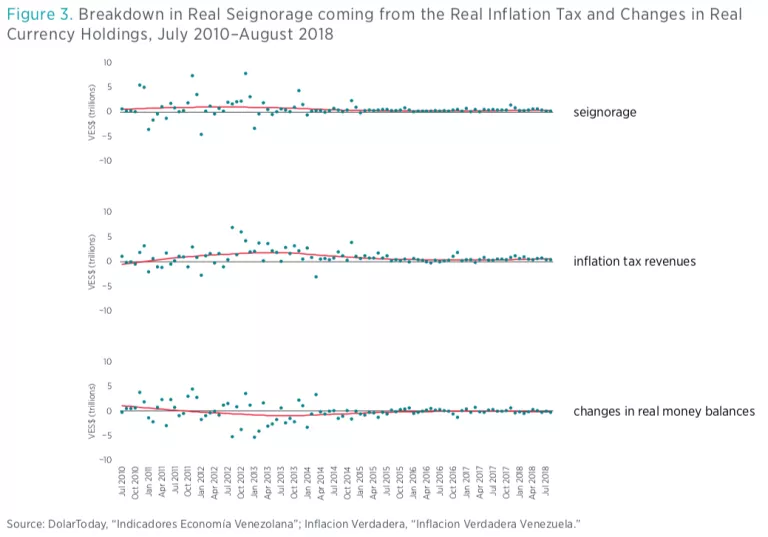

Real seignorage reflects inflation tax revenues and changes in real currency in circulation. The underlying intuition here suggests that while higher rates of inflation may increase inflation tax revenues, they can also result in declining holdings of currency valued in terms of goods and services, reflecting the declining tax base from printing currency. Ideally, the central bank should operate at no more than the seignorage-maximizing rate; beyond the maximizing rate, a central bank could generate more revenue at a lower inflation rate.

Figure 3 makes use of the DolarToday price index before May 26, 2017, and the Inflacion Verdadera index starting on May 26, 2017 (teal data points). Figure 3 also depicts a nonlinear trend in each panel (red line). The peak volume of inflation tax revenues was 6.76 trillion bolívares in August 2012, while the trend for inflation tax revenues reached a peak in June 2013, not long after President Maduro’s succession to power in April of that year. Since that time, seignorage and inflation tax revenues have been declining.

Policy Options: Official Dollarization, Currency Boards, and Fiscal and Currency Reform

Several policy options exist to address hyperinflation, including the following: (1) official dollarization, (2) instituting a currency board, and (3) fiscal and currency reform. While each option may offer similar solutions in terms of outcomes and therefore benefits, the key differences arise with their implementation and therefore the costs.

While dollarization can occur unofficially, as when individuals substitute more stable foreign currencies for the domestic one, an official dollarization arises when the government in power allows households to use foreign currency instead of the domestic currency. The latter can result from a policy decision, such as in Zimbabwe, in that the government may publicly announce that it will allow payments, including taxes, to be settled in foreign currency. The obvious benefits from dollarization are that it can restore price stability, while the costs include the government abandoning independent monetary policy, as well as seignorage.

A currency board option offers a more involved solution for the longer term to restore price stability. While in some ways similar to a central bank, a currency board does not act as a lender of last resort for the banking system. Upon creating the currency board, a country can issue a stock of notes, which are fully backed by interest-earning foreign assets and convertible into the foreign currency (e.g., US dollars). The currency board can thus earn seignorage revenues equal to the difference between that interest on foreign assets and the cost of printing the domestic currency. Such an option has the benefit of restoring price stability, while also offering the possibility of generating seignorage revenues. The cost includes giving up independent monetary policy.

Lastly, given the fiscal dominance of monetary policy mentioned earlier in this brief, in the longer term, a key component of efforts to end a period of hyperinflation lies with reining in government budget deficits and introducing central bank independence. As Thomas Sargent discusses, efforts to institute these changes following the four classic periods of hyperinflation in post–World War I Europe brought a quick end to those periods of hyperinflation. This does require a broad political consensus, however. Presuming that the current government does not come to an end in Venezuela, and given that figure 3 shows that real seignorage and inflation tax revenues appear to be dwindling (while the government does still earn revenues from petroleum exports), the government may find itself with no options but to abandon the currency and dollarize officially. This would not be without precedent for a hyperinflating economy; for instance, after exhausting all revenues, the government in Zimbabwe officially dollarized and introduced tax reform as a way to generate revenues.

Conclusion

Venezuelan seignorage revenues appear to be dwindling as the government has operated on the wrong side of the inflation tax Laffer curve since 2013. As the government exhausts seignorage, the regime will likely have to rely on alternative sources of revenue, including greater petroleum exports, tax reform, or both.