- | Corporate Welfare Corporate Welfare

- | Federal Testimonies Federal Testimonies

- |

The Export-Import Bank: Winners and Losers of Government-Granted Privilege

Testimony before the Committee on Banking, Housing, and Urban Affairs of the US Senate

Contrary to what you will hear from its supporters and beneficiaries, the Ex-Im Bank plays a marginal role in export financing—backing a mere 2 percent of US exports each year. The vast majority of exporters secure financing from a wide variety of private banks and other financial institutions without government interference or assistance. With US exports hitting record high levels, it is obvious that such financing is abundant and government assistance is superfluous.

Good morning Chairman Shelby, Ranking Member Brown, and members of the Committee. Thank you for the opportunity to testify today on the important topic of the Export-Import Bank of the United States.

My name is Veronique de Rugy, and I am a senior research fellow at the Mercatus Center at George Mason University, where I study the US economy, the federal budget, homeland security, taxation, tax competition, and financial privacy.

We don’t agree on much in Washington. In view of the all of the economic and social problems facing our nation, we should agree that the federal government ought not direct our limited public resources to subsidies that benefit successful politically connected corporations at the expense of thousands of companies and millions of American workers who compete in the global marketplace without government favors. This is why Congress should not reauthorize the Ex-Im Bank.

The policy debate surrounding the Ex-Im Bank has focused on maintaining the privileges long enjoyed by Boeing and a few other similar large corporations. It is vitally important, however, to recognize the many unseen costs of political privilege, whether it takes the form of market distortions, resource misallocation, destroyed potential, higher prices, or the competitive disadvantages imposed upon Main Street businesses that lack connections in Washington or access to press offices and lobbyists. These Main Street businesses matter, too.

Contrary to what you will hear from its supporters and beneficiaries, the Ex-Im Bank plays a marginal role in export financing—backing a mere 2 percent of US exports each year. The vast majority of exporters secure financing from a wide variety of private banks and other financial institutions without government interference or assistance. With US exports hitting record high levels, it is obvious that such financing is abundant and government assistance is superfluous.

Furthermore, letting the Ex-Im Bank’s charter expire won’t disturb existing deals. Failure to reauthorize will prevent the Ex-Im Bank from extending new loans, which would be a win for taxpayers who are ultimately on the hook for a total of $140 billion if bank reserves fail to cover defaults.

In this testimony, I would like to address the following points:

1. The Ex-Im Bank distorts the market by creating privilege, undermining the legitimacy of both government and the market.

2. The Ex-Im Bank fails on its own grounds.

3. The Ex-Im Bank suffers from massive transparency issues.

1. THE EX-IM BANK: THE POSTER CHILD OF GOVERNMENT-CREATED PRIVILEGE

There is abundant research about the negative effects of cronyism. For example, in a book called The Pathology of Privilege: The Economic Consequences of Government Favoritism, my colleague Matt Mitchell explained that “Whatever its guise, government-granted privilege [to private businesses] is an extraordinarily destructive force. It misdirects resources, impedes genuine economic progress, breeds corruption, and undermines the legitimacy of both the government and the private sector.”

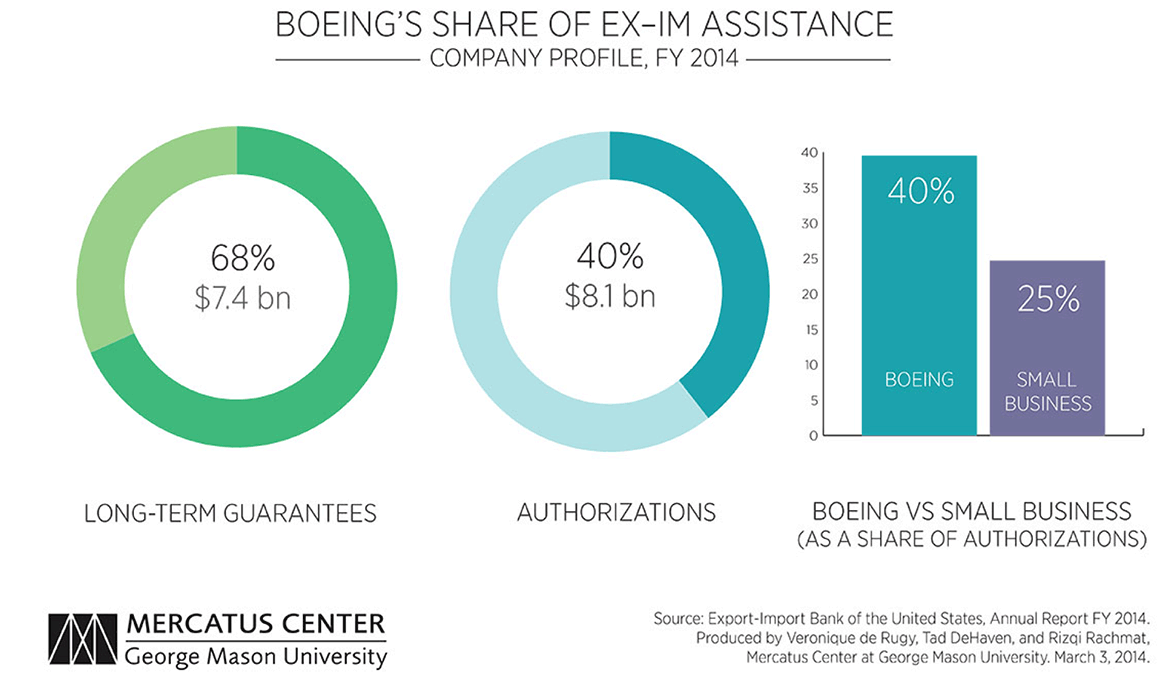

The Ex-Im Bank is one of those destructive government-granted privileges. This shows up in two forms, one strikingly visible, and the other invisible. Among the top ten domestic beneficiaries of the Ex-Im Bank is Boeing. At a 40 percent share of total Ex-Im Bank loan authorizations in 2014, Boeing dwarfs the 25 percent combined share of all small businesses. What we do not see are the higher costs borne by American exporters, due to the Ex-Im Bank being one of those destructive government-granted privileges.

A. Government Privilege and “Boeing’s Bank”

A look at the top 10 domestic beneficiaries for all Ex-Im Bank transactions between 2007 and 2014 shows that the Ex-Im Bank lives up to its nickname of “Boeing’s Bank.” The aviation giant, which has a market capitalization of $100 billion, is by far the biggest beneficiary of the Ex-Im Bank’s largesse, which provides $66.7 billion in subsidized financing to foreign purchasers of Boeing planes. General Electric, a company with a market cap of $279 billion, also ranks among the biggest beneficiaries, with $8.3 billion in export assistance. The $2.2 billion in Ex-Im Bank financing that benefits Caterpillar, a company with a market cap of $54 billion, is boosted by the $2.7 billion loan guarantee to its subsidiary, Solar Turbine Inc. (also on the Top 10 list).

B. Big Buyers Go With Big Exporters

On the foreign side, things aren’t much different—the subsidized financing largely benefits very large companies that either collect massive subsidies as state-controlled entities or could easily access private financing. The following table shows the top 10 foreign buyers, based on the total amount of financing authorized from FY 2007 through FY 2013.

The number one buyer was the Mexican state-owned petroleum company, Pemex, which has a market cap of $416 billion but has somehow needed more than $7 billion in US taxpayer–backed financing to facilitate deals with American exporters in recent years. Pemex, in fact, received some 30 percent of the more than $23 billion of Ex-Im Bank financing that flowed to foreign buyers in the oil and gas sector between 2007 and 2013. Overall, 21 percent of Ex-Im Bank financing went to this sector, a policy that seems at odds with the current administration’s less than favorable view of fossil fuels. In fact, the financing to foreign oil and gas firms exacerbates the regulatory burdens imposed by the Obama Administration, which favors Ex-Im Bank reauthorization, on the domestic oil and gas industry.

Other top buyers include foreign companies such as Emirates airline, which has benefitted from $3.4 billion in US-backed financing and proudly boasts on its website that it has “recorded an annual profit in every year since its third in operation.” Other foreign airlines also get cheap loans from the Ex-Im Bank, prompting charges of unfair competition. According to the lawsuit filed by Delta Airlines, along with the Airline Pilots Association, the unfair competition granted to Air India alone has resulted in the loss of some 7,500 US airline jobs.

These subsidies have prompted several American carriers and their employee unions to demand a rescission of the open-skies agreements with several airlines charging that the subsidies constitute unfair competition, including interest-free loans, discounted airport charges, government protection on fuel losses, and below-market labor costs.

The subsidies are largely captured by large producers, domestic and foreign, and the subsidies result in a policy mix that is contradictory in the goals it seeks to achieve. But there is more to the story.

C. The Unseen and the Unconnected Victims

It is difficult, but extremely important, that we consider the unseen costs of political privilege. Ex-Im Bank supporters tout subsidized firms’ successes, but they do not consider the unseen costs imposed on the other 98 percent of unsubsidized exports.

In these cases, it is firms’ own government—not a foreign government—that puts them at a competitive disadvantage. That is, foreign firms are receiving subsidized financing, which lowers their cost of business. But their American counterparts are paying market rates for financing, which means their cost of business is higher. The Ex-Im Bank also gives lenders an incentive to shift resources away from unsubsidized projects and towards subsidized ones—regardless of the merits of each project.

These capital market distortions have ripple effects. Subsidized projects attract more private capital while other worthy projects are overlooked. The subsidized get richer while the unsubsidized get poorer—or go out of business.

Unfortunately, we will never see the businesses that could have been. Perhaps they would have been better, more efficient, or more responsible than politically connected firms. But we will never know as long as the Ex-Im Bank exists and continues to distort the market through privilege.

Visible and invisible, this is how the Ex-Im Bank has come to exemplify “the extraordinarily destructive force” of government-granted privilege, in the words of my colleague Matt Mitchell.

2. THE EX-IM BANK: NOT WHAT IT IS MADE OUT TO BE

Some say that there are good reasons to continue the Ex-Im Bank’s subsidies and government privilege. They say that the Ex-Im Bank promotes US exports and supports small businesses while leveling the playing field and filling an important “financing gap.” They also claim that jobs would instantly disappear absent the Ex-Im Bank. But none of these arguments withstand scrutiny.

A. The Ex-Im Bank Can’t Affect The Trade Balance Overall

Economists tend to be extremely suspicious of export-subsidy schemes like those provided by the Ex-Im Bank and their ability to meaningfully boost exports. Sallie James, trade policy analyst at the Cato Institute, notes, “Export promotion programs for certain goods—marketing programs for certain commodities, say—may have beneficial effects for that industry but cannot affect the trade balance overall.” The Government Accountability Office (GAO) stated, “Export promotion programs cannot produce a substantial change in the US trade balance, because a country’s trade balance is largely determined by the underlying competitiveness of US industry and by the macroeconomic policies of the United States and its trading partners.”

The data confirms this point: the Ex-Im Bank backs less than 2 percent of US exports each year. Considering who a vast majority of the buyers and sellers are, it is unreasonable to assume that these exports will disappear if the Ex-Im Bank vanishes.

Also, while there is no doubt that the selected exporters benefiting from the subsidies enjoy them, the impact on the overall economy should not be overlooked. A review of the academic literature on the topic suggests that in most cases export subsidies reduce the total income of the country paying the subsidies. In other words, the GDP of the country issuing the subsidies is very likely to be negatively affected. In all cases, export subsidies reduce worldwide income by increasing the wealth of those, and only those, who are subsidized—at the expense of other exporters and taxpayers.

Reforming the broader macroeconomic policies that are more likely to harm the US trade position, such as the corporate income tax system, will help US exports far more than anything the Ex-Im Bank could do.

B. Jobs Will Not Vanish if the Ex-Im Bank Charter Expires

The Ex-Im Bank takes credit for supporting 164,000 jobs in 2014, but this number should be viewed with skepticism. In addition, economists have shown that in most cases schemes like the Ex-Im Bank redistribute jobs from nonsubsidized industries to subsidized ones.

Many in Congress, however, are still worried that letting the Ex-Im Bank charter expire will have an immediate impact on existing jobs supported by the Ex-Im Bank. They shouldn’t worry because even if the Ex-Im Bank is not reauthorized, it will have to honor the loans it already extended to companies. An orderly wind down means that the Ex-Im Bank won’t be able to extend new loans.

The biggest beneficiaries of the Ex-Im Bank know that their employees and their suppliers are perfectly safe in the event the charter is not reauthorized. That’s because Boeing, Caterpillar, General Electric, and the like all have billions of dollars of backorders that will keep their workers busy for years to come.

Diane Katz and I have released new research that shows the companies’ backlogs as reported in their latest annual reports. Boeing Co. posted a “record” backlog of $441 billion (in 2013); General Electric Co. recorded a backlog of $261 billion (in 2014); Caterpillar Inc.’s backlog is $16.5 million (in the first quarter of 2015); and Bechtel Corp. posted a “strong” backlog of $70.5 billion (in 2014).

This means that absent subsidies from the Ex-Im Bank, these corporations have production backlogs that will take years to fulfill—some with Ex-Im Bank financing in place and others without. Shutting down the Ex-Im Bank will not result in job losses—except, perhaps, among the ranks of lobbyists who are trying to scare members of Congress into maintaining this fount of corporate welfare.

C. The Ex-Im Bank Does Not Mostly Support Small Businesses

In recent years, the Ex-Im Bank has tried to recast its role away from export subsidies towards other priorities. For instance, Ex-Im Bank defenders argue that 90 percent of its deals benefit small firms. Of course, this shouldn’t be a reason for renewing the Ex-Im Bank’s charter, since its main function (export subsidies) is harmful to the US economy.

In addition, the Ex-Im Bank’s small business claim is dubious. By dollar value, in 2014, some 25 percent of the Ex-Im Bank’s activities benefited small businesses (defined as a company with 1,500 employees or less than $21 million in annual revenues).

Also, even using the Ex-Im Bank’s definition, the vast majority of US small businesses—over 99.9 percent—receive no benefits from the Ex-Im Bank and are placed at a competitive disadvantage against large, subsidized competitors.

Finally, it is worth noting that the Ex-Im Bank has been caught mislabeling its data to make it look as if more lending has gone to benefit small businesses, and it has been touting small business successes of companies that were large or already successful before any involvement with the Ex-Im Bank.

D. The Ex-Im Bank Is Not Really Leveling the Playing Field for US Exporters or Filling a Financing Gap

A common argument about the Ex-Im Bank is that without the export subsidies, foreign companies would not purchase US goods and would instead buy goods from companies whose countries offer such subsidies. For instance, without Ex-Im Bank, Emirates airline wouldn’t buy any Boeing planes but would instead buy Airbus planes to benefit from European subsidies. Defenders of the Ex-Im Bank also claim that private lenders are unwilling to risk lending to foreign companies. In our example, it implies that lenders would only extend loans to Emirates to buy a plane if the US government or one of the three EU governments offering export credits backs the deal.

This fear is reflected in the Ex-Im Bank charter. It spells out three criteria for Ex-Im Bank financing: 1) “to assume political or commercial risk that exporter and/or financial institutions are unwilling or unable to undertake”; 2) “to overcome maturity or other limitations in private-sector export financing”; or 3) “to meet competition from a foreign, officially sponsored export-credit agency.”

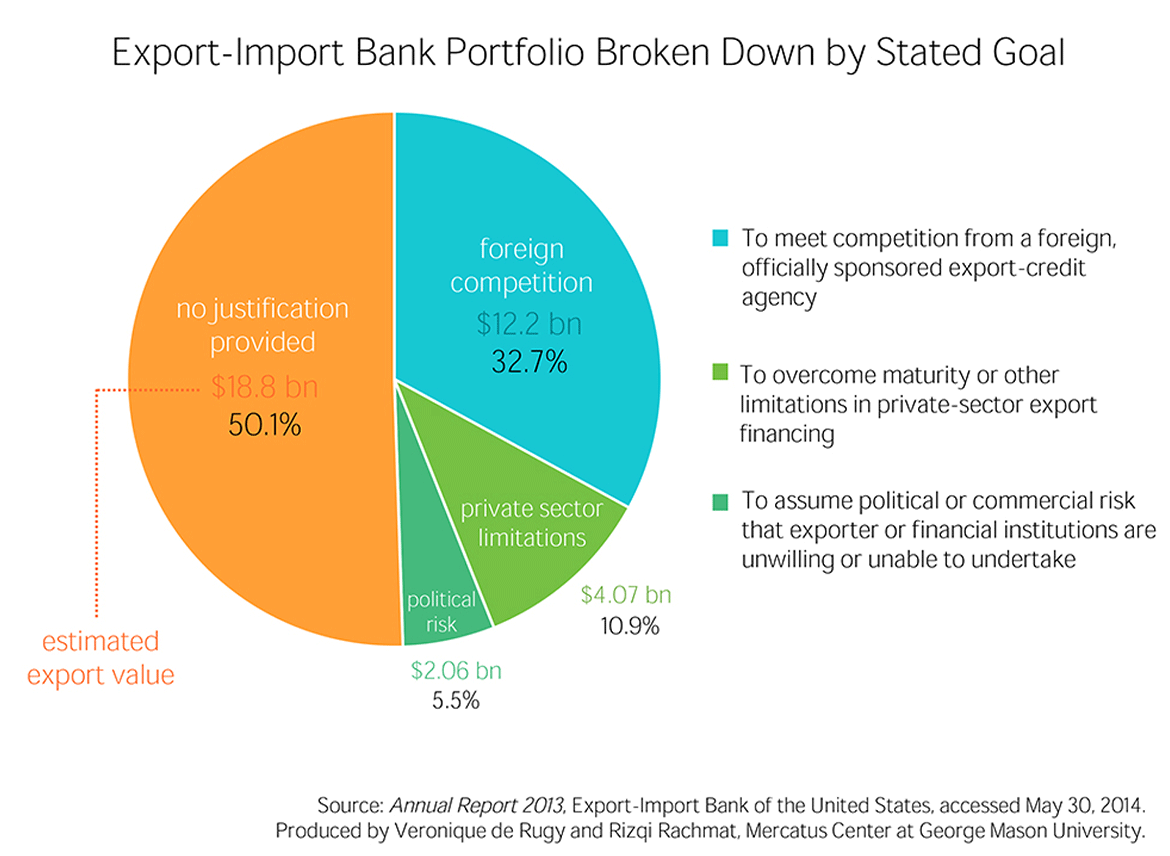

However, the data demonstrate that there is a gap between what the Ex-Im Bank claims it should be doing and what it actually does. As a condition of its most recent reauthorization in 2012, Congress required the Ex-Im Bank to designate the purpose served for certain financing deals. While the bank still does not provide justifications for all transactions in its portfolio, its current charter compels it to provide at least some explanation by category for all loans and long-term loan guarantees in its annual report.

The data show that less than one-third of the estimated export value of the Ex-Im Bank’s portfolio is intended to counteract competitive disadvantages created by foreign governments’ own export subsidies. Moreover, more than 98 percent of US exports occur without government financing through the Ex-Im Bank, demonstrating that the Ex-Im Bank is not critical for helping US exports thrive globally.

As for the claim that the Ex-Im Bank fills an important “financing gap” by supporting US exports, it is not supported by data. The Ex-Im Bank designates only 16.4 percent of its financing as necessary to address a lack of private capital. That means that most of what the Ex-Im Bank does has nothing to do with “filling a financing gap.”

What about the claim that foreign carriers will not purchase Boeing planes without subsidized financing from the United States and would instead buy Airbus planes with export credits from foreign governments?

The reality is that there is no shortage of private capital to finance aircraft purchases, and airlines would continue to purchase Boeing products in the absence of Ex-Im Bank subsidies. In my recent paper with Diane Katz, we look at the example of Emirates airline. The UAE state-owned company is the second biggest recipient of Ex-Im Bank financing. We write:

"In June 2012, Emirates bought two Boeing 777s using Ex-Im Bank financing, and four Airbus A380s using private financing. Obviously, the state-controlled airline could afford to buy planes without subsidies, and subsidies are not the only factor in the carrier’s choice of aircraft."

This is consistent with the results of a study by the GAO that found 85 percent of Boeing and Airbus large-aircraft deliveries were not subsidized by export-credit agencies.

3. The Ex-Im Bank is Suffering from Massive Transparency Issues

Scholars have been critiquing the poor quality of the Ex-Im Bank data for years. A 2014 report by the American Action Forum notes: “There continues to be areas needing additional transparency. For instance, publicly available data on program authorizations can often be incomplete and inadequate.”

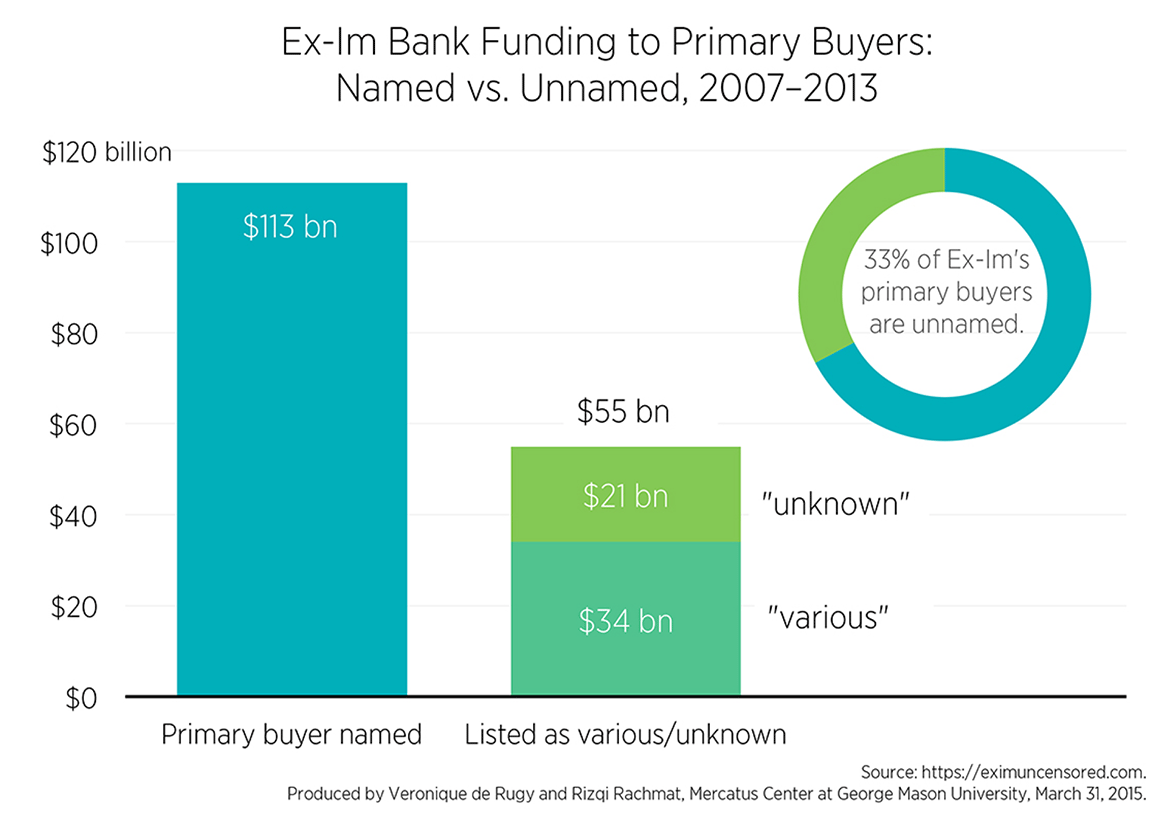

My own research has documented in detail that the dataset stored at Data.gov, a federal website launched in 2009, was spotty and incomplete—the GAO and the Ex-Im Bank’s own inspector general have repeatedly found that the agency’s recordkeeping is subpar and needs improvement. The dataset available at Data.gov is missing a great deal of information, and it is common to find beneficiaries marked as “unknown” or “various US companies”. It is also common to find the names of companies misspelled or identified differently on different forms, which makes working with the numbers even harder.

Let me illustrate how that should present a major problem for Congress. The Ex-Im Bank isn’t allowed to lend money to customers in certain countries, such as North Korea, Libya, and Iran. Russia was added to the list last year. But in order to know whether the Ex-Im Bank is actually complying with these restrictions and limitations, we need to be able to check its data. Unfortunately, as I have mentioned before, the Ex-Im Bank’s data, when available, are a mess. So much of the data are labeled “unknown” and “various countries” that it is hard for Congress to utilize the Ex-Im Bank’s data for proper oversight.

The following chart displays the top foreign buyers of exports financed by the Ex-Im Bank from 2007 to 2013. (We had to use the old dataset that used to be on Data.gov but was one day mysteriously removed and later replaced with an abridged dataset that did not list critical fields such as “Primary Buyer.”) This chart shows the total dollar amount of deals financed by the Ex-Im Bank in which the Primary Buyer is marked as “unknown” or “various” in data made available to the public—33 percent of buyers by dollar value are not named.

How do we know that some Ex-Im Bank loans didn’t go to companies in restricted countries if we don’t know which companies are getting loans? In some cases, the dataset shows the name of a country associated with the unknown deal. But how can we be sure that it is actually accurate without the name of the company?

I would like to trust the Ex-Im Bank, but it is hard to in light of how it has intentionally mislabeled its data to make it look as if more lending was going to benefit small businesses than actually was; how it has employees being investigated for taking bribes in exchange for loans; and how it indulged in collusion with top corporate executives at Boeing by asking for input on bank policies that could benefit their firm. Even without the Ex-Im Bank’s past missteps, it’s hard to see why we should trust it when it does not even release accurate data.

CONCLUSION

Beyond its operational lapses and its economic inefficiency, the problem with the Ex-Im Bank is that the many groups who its activities affect are people who don’t have connections, lobbyists, and press offices in Washington. These unseen victims matter, too.