- | Financial Markets Financial Markets

- | Policy Briefs Policy Briefs

- |

Did Basel III Regulations Dampen Lending at Large Banks?

In Q1 2013, when US regulators began implementing guidelines proposed by the Basel Committee on Bank Supervision (BCBS) at the Bank of International Settlements in response to the 2007–2009 financial crisis, large bank holding companies (BHCs) began readjusting their holdings of various asset classes. They may have done so because the BCBS’s revised guidelines (known as Basel III), among other things, called for increasing risk-based capital requirements to further reduce the risk of bank insolvency and introduced new liquidity rules to encourage greater liquid asset holdings.

Risk-based capital requirements vary across asset classes. Commercial loans have the highest capital requirements, loans such as mortgages have lower capital requirements, and reserves and US Treasury securities (US Treasuries) have no capital requirements. One traditional problem with risk weighting arises because the simplest risk weights require all assets with the same classification, such as commercial loans or mortgages, to have the same capital, thereby implying that they are equally risky, when the underlying risks may differ. And the more complex risk weights used by the largest advanced approaches BHCs (which tend to have at least $250 billion in total assets) may still be inaccurate despite their complexity.

It remains to be seen whether the US Basel III guidelines have improved the practice of risk weighting. But after the US implementation of the capital and liquidity guidelines, advanced approaches BHCs increased their loan shares but by a much smaller amount than did other large BHCs in the United States with at least $10 billion in total assets. One implication of these findings is that the risk weighting of loans could have discouraged advanced approaches BHCs in the United States from expanding their lending further.

How Basel Capital Regulations Disfavor Loans

In a recent policy brief, I discuss how the implementation of the Basel III capital and liquidity rules in the United States could have encouraged holdings of assets with no capital requirements that were also favored by liquidity rules, such as excess reserves and US Treasuries. In that policy brief, table 1 and the discussion of its contents illustrate how a bank might substitute between commercial loans, which have the highest risk weights, and reserves and US Treasuries, which have risk weights equal to zero, if the minimum risk-based capital requirement increases as happened beginning in Q1 2013. Because loans tend to have the highest risk weights and their illiquid nature means holdings cannot be used to satisfy liquidity regulations, the US implementation of Basel III meant loans were disfavored by these regulatory changes.

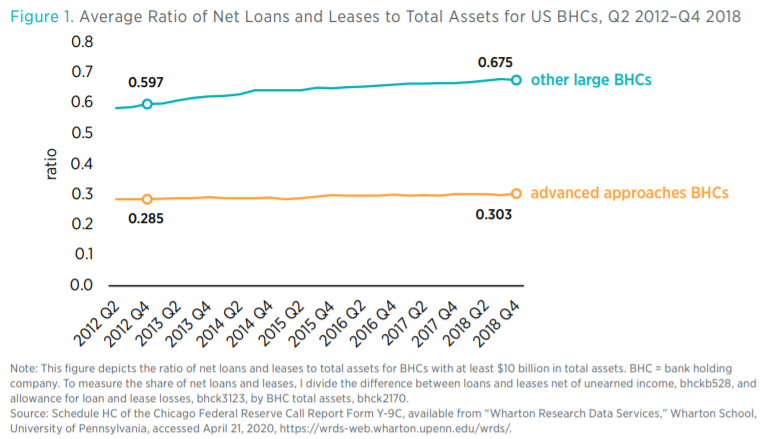

Empirically, figure 1 depicts the ratio of loans and leases, net of allowances for loan and lease losses, to total assets for (a) the largest advanced approaches BHCs, which were subjected to the most stringent capital and liquidity standards, and (b) other large BHCs that were subjected to less stringent standards. During the period sampled in the figure, the share of net loans and leases for the largest advanced approaches BHCs rises from about 28.5 percent in Q4 2012—just before the proposed US Basel III capital rules were unveiled—to 30.3 percent by the end of the period. For other large BHCs, the share rises from 59.7 percent in Q4 2012 to more than 67.5 percent by the end of the period. A simple calculation of the differences between the Q4 2012 and the end-of-period average share for each bank group suggests that Basel III capital and liquidity regulations could have resulted in advanced approaches BHCs having about a 6 percentage point (i.e., 30.3 − 28.5 − (67.5 − 59.7)) smaller share of loans.

One explanation for this finding is that risk-based capital requirements, when they bind, cause banks to substitute away from higher-risk-weight assets, such as loans, and toward lower-risk-weight assets, such as reserves and US Treasuries. Also, this result could reflect the combined effects of the new risk-based capital and liquidity requirements, each of which favor holding reserves and US Treasuries and disfavor holding loans. That said, the role of risk-based capital is evident from the fact that most of the relatively smaller share of loans for the advanced approaches banks comes from the highest-risk-weight loan category.

Loans with the Highest Capital Requirements Were Affected Most

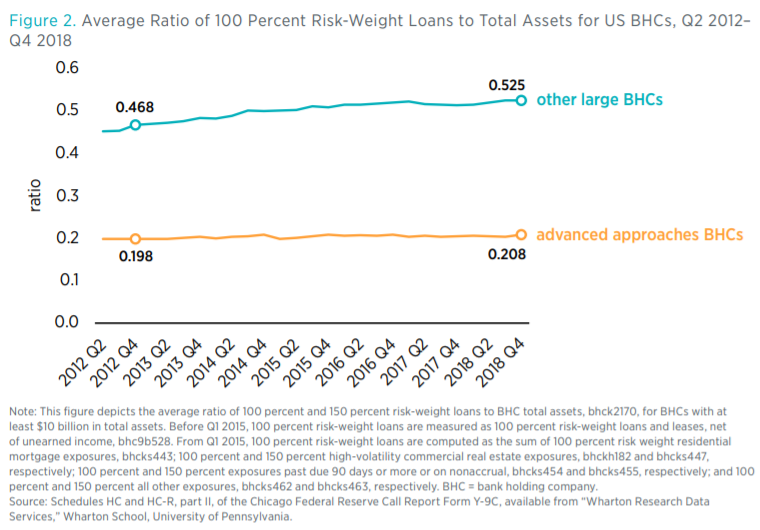

To show that loans with the highest capital requirements were affected most, figure 2 depicts the ratio of 100 percent risk-weight loans, meaning those that require at least the full 8 percent minimum Tier 1 and Tier 2 capital to risk-weighted assets or more for every dollar of the asset held. Commercial and industrial loans are included in this category. During the sample period, the share of net loans and leases for the largest advanced approaches BHCs rises from about 19.8 percent in Q4 2012, just before the proposed US Basel III capital rules were unveiled, to 20.8 percent by the end of the period. For other large BHCs, the share rises from 46.8 percent in Q4 2012 to about 52.5 percent by the end of the period. A simple calculation of the differences between the Q4 2012 and the end-of-period average share for 100 percent risk-weight loans implies that advanced-approaches BHCs had about a 4.7 percentage point (i.e., 20.8 − 19.8 − (52.5 − 46.8)) smaller share of loans with the 100 percent or higher risk weight. The 50 percent risk-weight category was affected to a lesser extent.

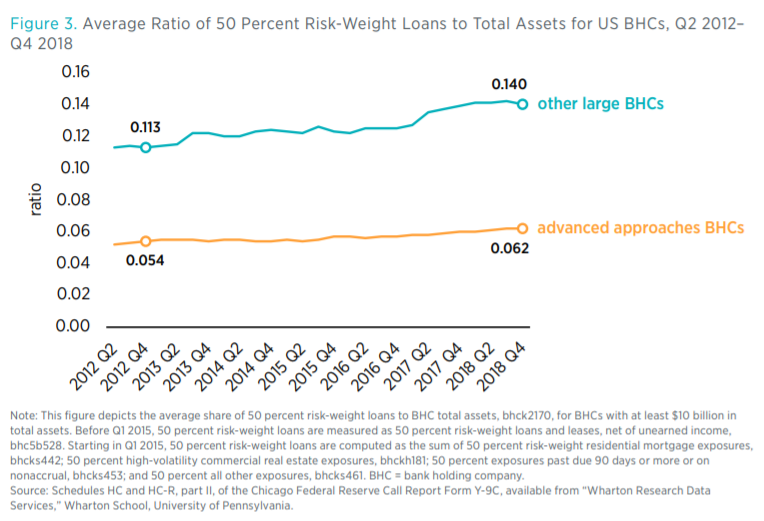

To show this lesser effect, figure 3 depicts the ratio of 50 percent risk-weight loans, meaning those that require at least 4 percent minimum Tier 1 and Tier 2 capital to risk-weighted assets for every dollar of the asset held. Mortgages are a predominant source of such loans. During the sample period, the share of 50 percent risk-weight loans for the largest advanced approaches BHCs rises from about 5.4 percent in Q4 2012, just before the proposed US Basel III capital rules were unveiled, to 6.2 percent by the end of the period. For other large BHCs, the share rises from 11.3 percent in Q4 2012 to about 14 percent by the end of the period. A simple calculation of the differences between the Q4 2012 and the end-of-period average share for 50 percent risk-weight loans implies that advanced approaches BHCs had about a 1.9 percentage point (i.e, 6.2 − 5.4 − (14.0 − 11.3)) smaller share of loans with the 50 percent risk weight.

Conclusion

Bank capital regulation, if done properly, can address the too-big-to-fail problem by making it less likely that a bank will become insolvent. It took 25 years to get from the US Basel I standards, which were unveiled in 1988, to US Basel III standards, which were unveiled in 2013. The process has involved considerable trial and error that has greatly complicated regulatory capital guidelines and created distortions on bank balance sheets. A simpler, alternative approach would increase the equity-to-asset leverage ratio. Doing so would eliminate the distortions to the assets’ portfolio created by risk-based capital requirements while addressing concerns about bank insolvency.