- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

Dodd-Frank’s Regulatory Surge: Quantifying Its Regulatory Restrictions and Improving Its Economic Analyses

We apply the methodology of RegData—which quantifies regulations using text analysis of the Code of Federal Regulations (CFR)—to objectively determine the number of new restrictions the Dodd-Frank Act has created and will create. We estimate that Dodd-Frank will increase financial industry regulatory restrictions by 32 percent once all of its rulemakings are finalized, yielding more new restrictions than were created between 1997 and 2010.

Most observers agree that the over-800-page Dodd-Frank Act will create numerous new regulatory restrictions, but no one knows just how many total restrictions Dodd-Frank will create. Further, it is difficult to know what benefits we will get in exchange for these regulations.

We apply the methodology of RegData—which quantifies regulations using text analysis of the Code of Federal Regulations (CFR)—to objectively determine the number of new restrictions the Dodd-Frank Act1 has created and will create. We estimate that Dodd-Frank will increase financial industry regulatory restrictions by 32 percent once all of its rulemakings are finalized, yielding more new restrictions than were created between 1997 and 2010.

Federal financial regulators’ economic analyses of their Dodd-Frank rulemakings have generally been of poor quality, making it nearly impossible to anticipate their potential costs and benefits with any confidence. This massive total increases the urgency of the need for improved economic analysis. To improve the quality of these analyses and the rules they accompany, federal financial regulators should be required to conduct economic analyses with at least the same rigor required of executive agencies.

Methodology and Findings

To quantify Dodd-Frank restrictions, we used the RegData methodology, which relies on the content of regulatory text as a data source.2 RegData parses the CFR to count the number of restrictions—words that indicate an obligation to comply, such as “shall” or “must”—published in it. We focused our analysis on Titles 12 (Banks and Banking) and 17 (Commodity and Securities Exchanges) of the CFR, where most financial regulations are published. Because the 2014 CFR, which will include most Dodd-Frank rulemakings finalized during 2013, has yet to be published, this analysis is limited to new Dodd-Frank rulemakings finalized by December 31, 2012. Consequently, we applied the RegData methodology to determine the change in restrictions within parts of the CFR affected by Dodd-Frank rulemakings between its passage and the end of 2012. Our methodology is further explained in the Appendix.

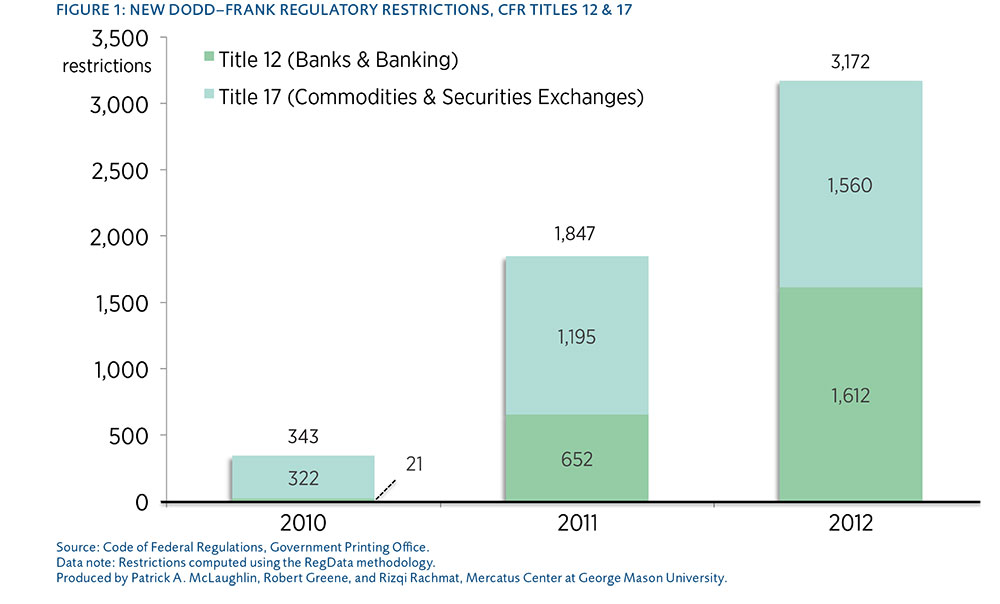

We find that between its passage in July 2010 and the end of 2012, Dodd-Frank created 5,362 new restrictions in CFR Titles 12 and 17.3 The growth of restrictions has accelerated in recent years (see figure 1). We estimate that in 2010, 343 new regulatory restrictions were created; in 2011, 1,847 were created; and in 2012, 3,172 were created because of Dodd-Frank. In total, Dodd-Frank’s 5,362 new restrictions represent a 10.5 percent increase from the 51,116 restrictions that existed in Titles 12 and 17 before Dodd-Frank amended them.

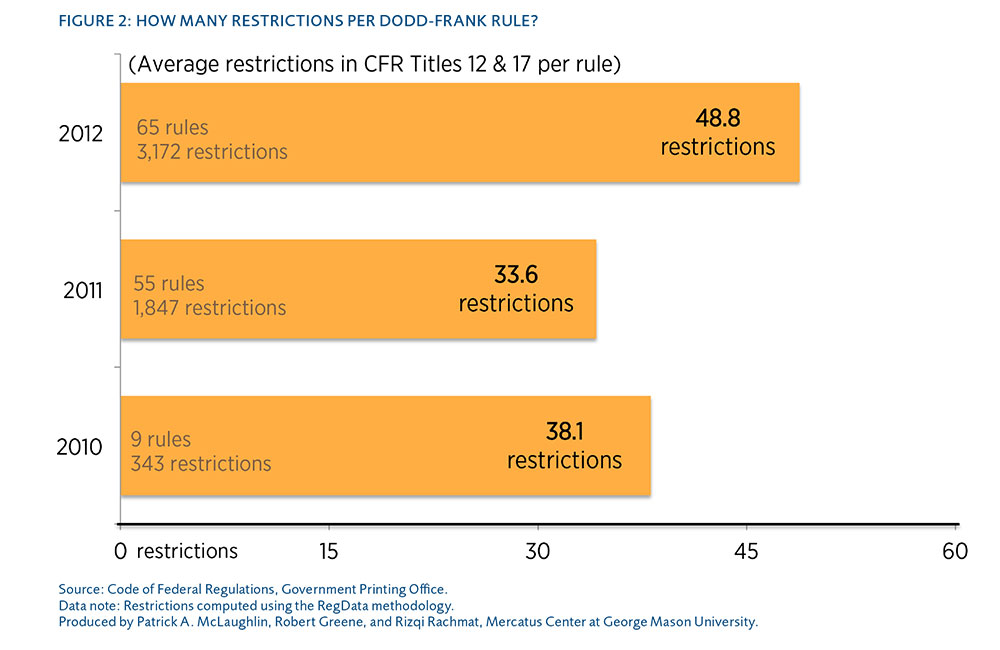

It is important to bear in mind, however, that most Dodd-Frank rulemakings have yet to be finalized.4 New rules could be more or less restrictive than the rules adopted through the end of 2011. We estimate that average rule restrictiveness has increased to 48.8 restrictions per rule in 2012 from 38.1 in 2010 (figure 2). Overall, however, each new Dodd-Frank rule creates about 41.6 restrictions. Dodd-Frank requires the creation of—by one count—a total of 398 rulemakings.5 Assuming the remaining regulations are proportionately restrictive, Dodd-Frank would create 16,543 new restrictions in total.6

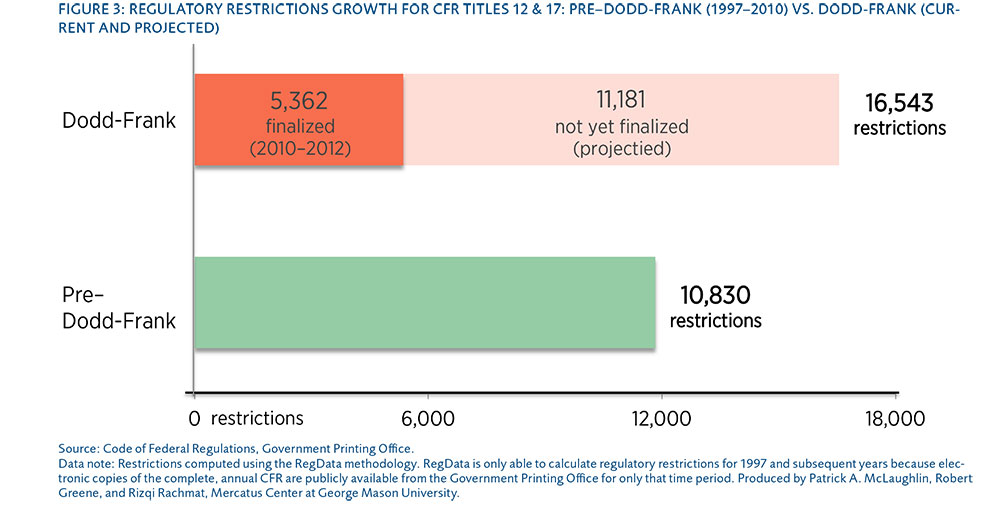

To give this figure—16,543—additional perspective, we compared it to the total number of restrictions—51,116—in effect in 2010 in CFR Titles 12 and 17. If Dodd-Frank adds 16,543 restrictions to those CFR titles, it will have caused a 32 percent increase in restrictions in those titles. Therefore, we project Dodd-Frank will create more regulatory restrictions in CFR Titles 12 and 17 than were created between 1997 and 2010 (see figure 3).7

The Need for Thorough Economic Analysis by Federal Financial Regulators

What are we getting in exchange for all these new regulations? It is difficult to know. Executive agencies are required by Executive Orders 12,866 and 13,563 to conduct thorough economic analysis of proposed rulemakings to help ensure that desired outcomes are achieved at minimum cost.8 These economic analyses may be reviewed by the Office of Information and Regulatory Affairs (OIRA), which is directed by Executive Order 12,866 to ensure that analyses meet the standards set by this Executive Order and OMB Circular A-4 for economic analyses.9 However, because according to current statute most federal financial regulatory agencies are “independent regulatory agencies,” the economic analyses of most federal financial regulators do not have to comply with Executive Order requirements and are exempt from OIRA review.10

While some federal financial regulators—including the Securities and Exchange Commission, Commodity Futures Trading Commission, and Bureau of Consumer Financial Protection—are required by statute to conduct a certain degree of economic analysis for some proposed rulemakings, others—such as the Federal Reserve Board, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation—have no statutory requirement to conduct economic analyses of proposed rulemakings. Instead, internal guidelines encourage these agencies to produce economic analyses for proposed rules.11

Regardless of internal or statutory requirements, a 2012 review of 192 proposed and final Dodd-Frank rules revealed that 57 contained no cost-benefit analysis,

while another 85 contained cost-benefit analyses that were entirely non-quantitative.12 Research suggests that independent agencies generally produce economic analyses of poorer quality than executive agencies.13 The Government Accountability Office has found federal financial regulators’ efforts to conduct economic analysis for Dodd-Frank rulemakings “fall short of what could be done to determine the potential costs and benefits of the new rules.”14 Similarly, a recent Mercatus Center study found that “federal financial regulators generally have shied away from conducting thorough regulatory analysis.”15

There are several different ways policymakers could improve the quality of financial regulators’ economic analysis. Congress could create statutory requirements that subject all federal financial agencies to rigorous economic analysis standards. Alternatively, Congress could make federal financial regulators subject to Executive Order 12,866, thereby necessitating that they conduct economic analyses with the same degree of thoroughness required of executive agencies. This would require that federal financial regulators’ economic analyses be reviewed by OIRA, which, studies show, improves the quality of analysis.16 Some argue that the president could unilaterally require federal financial regulators to comply with Executive Order 12,866.17

Any of these reforms would help ensure that the projected 16,543 regulatory restrictions created by Dodd-Frank have a better chance of achieving desired outcomes at lower economic costs.18 Granted, executive branch agencies’ actual analysis of proposed rules often falls short of expectations.19 However, executive branch analysis is certainly superior to the level performed by financial regulators for most Dodd-Frank rulemakings.

Conclusion

In this study, we use the RegData methodology to quantify the regulatory restrictions created by Dodd-Frank between its passage and the end of 2012. In just 30 months, we estimate that Dodd-Frank created 5,362 new restrictions in Titles 12 and 17 of the CFR. If subsequent Dodd-Frank rules are proportionately restrictive, we estimate that Dodd-Frank will add a total of 16,543 new restrictions to CFR Titles 12 and 17. By this estimate, Dodd-Frank would cause a 32 percent increase to the amount of restrictions in CFR Titles 12 and 17 when compared to restrictions in those titles in 2010. So far, the Dodd-Frank rulemakings’ economic analyses—which are intended to ensure the achievement of regulatory objectives, maximize benefits, and reduce costs—have generally been of poor quality. To help reduce unnecessary economic costs of Dodd-Frank rulemakings, federal financial regulators should be required to conduct economic analyses with the same degree of thoroughness that is currently required of executive agencies. To further improve the quality of Dodd-Frank rulemakings, OIRA should be enabled to review the economic analyses of federal financial regulators.

Appendix: Regdata Methodology

To identify CFR Title 12 and 17 rules finalized pursuant to Dodd-Frank authority between the date Dodd-Frank became law and December 31, 2012, we used a list of final Dodd-Frank rules and notices compiled by the Federal Reserve Bank of St. Louis.20 According to this list, 129 of Dodd-Frank’s required or permitted rulemakings were published in the Federal Register as final rules by December 31, 2012. Because the restrictions of interim final rules created in one part of the CFR can later be duplicated by final rules in separate CFR parts, we exclude them from our analysis to avoid overestimating the number of restrictions Dodd-Frank has created.21 We also exclude guidance documents and other similar agency documents.22 Additionally, certain Dodd-Frank rules were not included in the Federal Reserve Bank of St. Louis list.23 Consequently, our analysis likely understates the number of new restrictions Dodd-Frank has generated.

To quantify Dodd-Frank’s restrictions through 2012, we first identified Title 12 and 17 parts of the 2011, 2012, and 2013 CFRs created, altered, or amended by each of the 129 Dodd-Frank rules finalized before the end of 2012.24 We used the RegData method to calculate the number of restrictions within each affected CFR part before and after the rule amending or adding that part was published in the Federal Register. If an entirely new part to the CFR was added, we calculated the number of restrictions in that new part. If one part of the CFR was modified by several rulemakings during a given CFR year, new restrictions added between CFR years for each impacted part were only counted once, regardless of how many rules impacted a particular part, in order to avoid double-counting of restrictions.

Title 12 of the CFR is revised as of January 1 of a given year. Thus for Dodd-Frank rulemakings affecting Title 12, those published in the Federal Register 2010, 2011,

and 2012 created new restrictions in the 2011, 2012, and 2013 CFRs, which we attributed to calendar years 2010, 2011, and 2012, respectively. Due to the publication lag for Title 17 rules, the methodology differed. Title 17 of the CFR is revised as of April 1. If a Title 17 rule was published in the Federal Register before April 1 of a given year, we subtracted restrictions contained within the rule’s impacted parts in the CFR of the year before the rule was published from restrictions of the rule’s impacted parts in the CFR of the year during which the rule is published. If a rule was published on or after April 1 of a given year, we subtracted restrictions contained within the rule’s impacted parts in the CFR of the year during which the rule was published from restrictions of the rule’s impacted parts in the CFR of the year after which the rule was published.25 As mentioned above, we only counted new restrictions created within a part between CFR years once when calculating total annual restrictions to avoid double-counting.

Six Title 17 parts were impacted by rules that spanned two calendar years, but only impacted one CFR year.26 To estimate the impact on annual restrictions of these rules, we distributed restrictions generated within the span of two calendar years proportionally based on the number of rules affecting that part in each calendar year.27

Related Content

- | Regulation Regulation

- | Data Visualizations Data Visualizations

Did Deregulation Cause the Financial Crisis? Examining a Common Justification for Dodd-Frank

- | Financial Markets Financial Markets

- | Books Books

Dodd-Frank: What It Does and Why It's Flawed