- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

A Flawed Regulatory Concept

The Community Reinvestment Act

In "A Flawed Regulatory Concept," Lawrence J. White examines the underlying concept of the Community Reinvestment Act (CRA) and whether the CRA contributed to the financial crisis of 2007 -

The 2007-2008 financial debacle has raised many questions as to whether the Community Reinvestment Act (CRA) played a facilitating role. Congress enacted the CRA in 1977 in response to the belief that low and moderate-income (LMI) communities needed expanded access to credit. This legislation is a regulatory effort to "lean on" banks and savings institutions1 in vague and subjective ways to make loans and investments that (CRA proponents believe) those depository institutions would otherwise not make. Although the goals for promulgating the CRA were well intended and the CRA was not instrumental in the current subprime mortgage-driven debacle, the CRA is not good public policy.

THE CONCEPTUAL FRAMEWORK

The basic concept of the CRA is that banks are somehow neglecting loan opportunities in the communities in which they have establishments—primarily, in LMI communities—and thus regulation must force them to lend in those communities.2

This concept rests on the notion either that (a) banks are lazy (or ill-intentioned) and are inefficiently passing up profitable opportunities to lend to creditworthy customers in LMI communities, hence they need regulations to force them to lend more; or (b) since banks have market power and excess profits, regulation can force them to use the excess profits to cross-subsidize the unprofitable loans in LMI communities. Either version has the flavor of the pre-1970s world of banks and banking, where competition was not especially vigorous and state and national regulations often impeded entry and prevented banks from branching outside their home communities, which often created pockets of local market power.

THE DRAWBACKS OF THE CRA

Let us instead consider lending in the context of the first decade of the 21st century. In that context, there are some key reasons for questioning the wisdom of the CRA.

1. If loans are profitable, profit-seeking banks should already be making them.

In this case, CRA is redundant at best (yet still costly due to the costs of compliance and of regulatory monitoring). Of course, banks make mistakes and may not be the perfect maximizers so often described in introductory economics textbooks. But the CRA is based on the notion that banks systematically overlook profitable opportunities in LMI communities, which seems unlikely in today's environment.

If there were spillover effects that rendered single loans unprofitable but would cause a group of loans to be profitable, we would see banks forming joint ventures to "internalize" the externality and make these loans profitable.

However, if the loans are not profitable, then (a) they require a cross-subsidy from the excess profits from other (super-profitable) activities of the bank, but in the increasingly competitive environment of financial services there will be little or no excess profits; (b) they will involve losses for the bank; or (c) banks will avoid these loans that are not profitable. Neither of these last two prospects should be the basis for good public policy.

2. Today, there is nothing special about local geographic areas or about the specific placement of physical bank locations.

Banks should not be obliged to lend to a specific local geographic area. Likewise, banks should have no obligation to hire only employees who live in that same geographic area or to purchase their desks from local merchants. The broad sweep of public policy in the financial services area, which has been to erase protectionist measures (such as restrictions on intrastate and interstate branching and the forced compartmentalization of financial services) and to place more trust in competition, differs from the orientation of the CRA.

Further, the idea that a bank might be "draining deposits" from a local area ignores the substantial value to an LMI community of a bank that offers primarily deposit services and a few related services (such as check-cashing, cash transfers, and perhaps some personal loans). Even if banks provide a limited menu of services, they can compete with other higher-cost alternatives, such as check-cashing offices and payday lenders to lower the costs of banking services. Ironically, the lending obligations of CRA may well discourage the establishment of branches in LMI areas in the first place.

3. Banks are not unique in their lending ability and thus regulations should not place special obligations on them.

There are many other categories of lenders for most of the types of loans that banks make. However, banks are special in at least two important ways: (a) They (along with credit unions) provide federally insured deposits, which is an important benefit for financially unsophisticated customers who seek a safe place for their transactions accounts; deposit insurance also provides stability for the overall banking system by forestalling the kinds of depositor runs on banks that plagued American banking before 1933 (and that Britain revisited in September 2007 with their Northern Rock debacle);3 and (b) Commercial banks especially are important sources of credit for small and medium-size enterprises (SMEs). Both special features are good arguments for vigorous antitrust enforcement to ensure that bank mergers do not create anticompetitive environments in local markets for deposits and SME lending. Neither, however, provides an argument for imposing CRA requirements to make loans that they would not be inclined otherwise to make.

4. The vagueness of the CRA's language—that banks should meet "the credit needs of its entire community, including low and moderate-income neighborhoods . . ."4 —has led to vagueness and subjectivity of enforcement.

Initially, enforcement focused on a bank's efforts toward serving its community and the documentation of those efforts; after 1995, enforcement focused more on documenting lending outcomes. The inherent vagueness of "needs" inevitably leads to the vagueness and subjectivity of enforcement. This cannot be the basis of good public policy.

In sum, the CRA emphasizes protectionism and localism and distrusts competition in an era when the sweep of policy is to reduce and eliminate local barriers and to rely more on competition than on forced lending. And, by discouraging entry in LMI areas, the CRA may well be contrary to the long-run interests of the communities that it is intended to help.

THE CRA AND THE SUBPRIME MORTGAGE-RELATED SECURITIES CRISIS

Recently, broader critiques of the CRA have emerged: that the CRA encouraged banks to make subprime mortgage loans (which were then securitized) and thus the CRA bears major responsibility for the housing bubble of 1999-2006 and the mortgage-related securities crisis of 2007-2008.

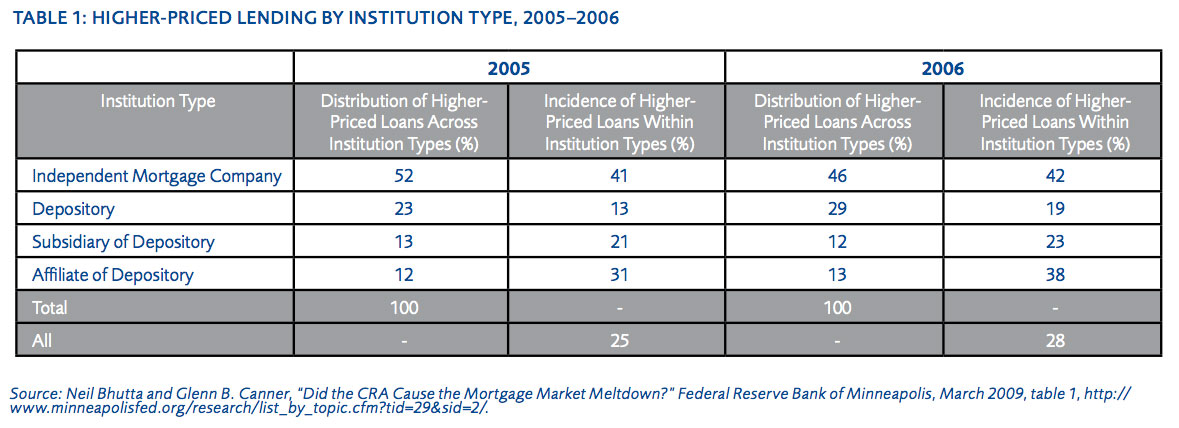

These broader critiques are poorly aimed. It appears that non-bank lenders—i.e. mortgage institutions that either securitized the mortgages themselves or quickly sold the mortgages to securitizers—made the bulk of the subprime lending of the earlier years of this decade. The CRA requirements did not cover these non-bank lenders [see table 1 for a breakdown of mortgage originations at the height of the subprime mortgage bubble]5. Further, although investment banks (such as Bear Stearns, Lehman, Morgan Stanley, and Merrill Lynch) and a large insurance conglomerate (AIG) experienced major financial difficulties that were related to investments in these mortgage securities, the CRA requirements did not apply to these financial services entities either. Where banks did experience difficulties that were related to subprime mortgages—such as Citibank, WaMu, Wachovia (having absorbed Golden West in 2006), IndyMac, and Countrywide—it appears that they were heavily involved in subprime lending because of its perceived profitability (and their under-appreciation of the risks) and not because of CRA pressures.

Essentially, the CRA has multiple flaws, but responsibility for the subprime mortgage lending and securities debacle does not appear to be one of them.

BETTER PUBLIC POLICIES

These criticisms of the CRA should not be interpreted as a statement that no governmental action is warranted. As stated earlier, there are better ways to achieve the goals of the CRA's advocates.

First, the Equal Credit Opportunity Act of 1974, the Fair Housing Act of 1968, and other such statutes have the appropriate provisions to address discrimination by lenders of any kind with respect to racial or ethnic or other prohibited categories.

Second, maintaining the competitiveness of banking markets is important. The entry of new players, especially those that have a business model of providing value to LMI households, should be encouraged—or, at least, not discouraged.6 It is indeed ironic that the same community groups who advocate more banking services for LMI households were also those who lobbied the FDIC and the Congress from 2005 to 2007 (in alliance with the banking lobbyists, with whom the community groups are at odds with respect to efforts to expand the CRA's burdens on banks) to thwart Wal-Mart's efforts to enter the banking business by obtaining an industrial loan company charter from the state of Utah. Current regulatory tools are robust enough to handle potential safety and soundness issues that may emerge from such companies' ownership of banks. The potential problems are no more serious than the problems resulting from current ownership structures.7

Third, to the extent that there is a good social case for local lending and investment that local lenders somehow do not satisfy, policymakers should provide such lending and investments via the public fisc. Such a program, including the Community Development Financial Institutions Fund, should replace whatever socially worthwhile projects would be eliminated if CRA were repealed.

Finally, if the CRA remains in force, policymakers should replace its vague and subjective regulatory enforcement with a set of specific annual lending obligations that would encompass both originations and portfolio holdings. These obligations would then be tradable among banks. Those banks that were less efficient at originating and holding these types of loans could pay other banks that were more efficient at the activities to take over these obligations.8

CONCLUSION

The CRA is an anachronistic and protectionist effort to force artificially a local focus for finance in an increasingly competitive, increasingly electronic, and ever-widening realm of financial services. Further, ironically, the burdens of the CRA may well discourage banks from setting up new locations in low-income neighborhoods and thus providing local residents with better-priced alternatives to high-cost check-cashing and payday lending establishments. The CRA is not a good public policy tool for achieving the goals that it advocates.

ENDNOTES

1. For the remainder of this piece, the word "banks" will include both commercial banks and savings institutions, unless otherwise indicated.

2. Community Reinvestment Act of 1977, U.S. Code 12 (1977), chap. 30, http://www.fdic.gov/regulations/community/community/12c30.html/.

3. Apparently, there was a modest-sized run on Washington Mutual Bank (WaMu) in September 2008 by insured and uninsured depositors before the Federal Deposit Insurance Corporation (FDIC) declared a receivership and arranged for JPMorgan Chase to absorb WaMu's deposits and assets. In March 2008, Bear Stearns experienced a "run" by short-term creditors that had similar characteristics to that of a bank run. And in September 2008, in the wake of Lehman Brothers' bankruptcy, a prominent money-market mutual fund (the Reserve Fund) experienced significant losses on the Lehman commercial paper that it held and declared that the value of its nominal one-dollar shares would be only $0.97 (it "broke the buck"), which then caused shareholder runs on money market mutual funds more broadly (which caused the Federal Reserve then to offer guarantees on existing shares).

4. Community Reinvestment Act of 1977, sec. 2903 (a) (1).

5. See also Elizabeth Laderman and Caroline Reid, "CRA Lending during the Subprime Meltdown," in Revisiting the CRA: Perspectives on the Future of the Community Reinvestment Act, Prabal Chakrabarti, David Erickson, Ren S. Essene, Ian Galloway, and John Olson, eds. (Boston and San Francisco: The Federal Reserve Banks of Boston and San Francisco, 2009), 115-133.

6. Lawrence J. White, "Statement before the Financial Services Committee of the U.S. House of Representatives," February 13, 2008.

7. It is anomalous that the local car dealer is permitted to own a bank, but AutoNation, Inc. (a publicly traded company that operates a large number of car dealerships) is not.

8. See Michael Klausner, "A Tradable Obligation Approach to the Community Reinvestment Act," in Revisiting the CRA: Perspectives on the Future of the Community Reinvestment Act, Prabal Chakrabarti, David Erickson, Ren S. Essene, Ian Galloway, and John Olson, eds. (Boston and San Francisco: The Federal Reserve Banks of Boston and San Francisco, 2009), 75-83.