- | Public Interest Comments Public Interest Comments

- |

The Interagency Working Group on the Social Cost of Greenhouse Gases Should Be Transparent About the Value Judgments Behind Its Estimates and Acknowledge Their Cost

Public Interest Comment Submitted to the Office of Management and Budget

The Office of Management and Budget (OMB) is seeking comments on behalf of the Interagency Working Group on the Social Cost of Greenhouse Gases (IWG) regarding a recent update made to estimates of the social cost of carbon, methane, and nitrous oxide in a technical support document (TSD) issued by the IWG. The IWG intends for federal regulatory agencies to use the values from the TSD in regulatory impact analyses to justify regulations targeting greenhouses gas emissions.

The Mercatus Center’s Fourth Branch project is dedicated to advancing knowledge about the effects of regulation on society. As part of its mission, scholars conduct careful and independent analyses that employ contemporary economic scholarship to assess regulations and their effects on economic opportunities and societal well-being. This comment provides guidance to OMB and to the IWG about ways to improve the social cost of greenhouse gases (SCGG) estimates in the TSD, in particular by providing transparency about the nature of value judgments embedded in the process of selecting SCGGs, as well as about the substantial cost that use of these estimates is likely to impose on the American public. Throughout this comment, recommendations will be written in bold, so it is clear what is being recommended to these federal agencies.

The IWG Report on the Social Cost of Greenhouse Gases Is an Economically Significant Regulatory Action

Under executive order 12866, an economically significant regulatory action, as defined in Section 3(f)(1) of the order, is “any regulatory action that is likely to result in a rule that may . . . have an annual effect on the economy of $100 million or more or adversely affect in a material way the economy, a sector of the economy, productivity, competition, jobs, the environment, public health or safety or State, local or tribal governments or communities.” Economically significant regulatory actions require a full regulatory impact analysis, which includes an assessment of benefits, costs, and alternatives.

The TSD on the SCGG meets the definition of an economically significant regulatory action under executive order 12866 because it “is likely to result in a rule that may . . . have an annual effect on the economy of $100 million or more.” As evidence, according to a 2017 law review article, the Obama administration used the social cost of carbon (SCC) or social cost of methane (SCM) metrics in economic analysis for at least 83 regulatory proceedings. The total cost of these 83 regulatory actions is estimated to be between $447 billion and $561 billion (in 2020 dollars), on the basis of regulatory agencies’ own impact analyses (see appendix A of this comment for these calculations). This estimate may be conservative because it is unclear whether the list of 83 regulatory proceedings is comprehensive, and because some regulatory analyses from these proceedings include only cost estimates for benchmark years (as opposed to calculating total cost across all years). The perpetuity value of $447 billion at a 7 percent interest rate is $31.3 billion, implying that if these costs were spread across an infinite time horizon, annual costs would still be 30 times higher than the threshold for economic significance, according to executive order 12866. Therefore, a regulatory impact analysis is required and should be made available for public scrutiny.

Recommendation 1: OMB should withdraw the TSD so that the TSD may be reintroduced, supplemented with a regulatory impact analysis, and made available for public comment.

The Social Welfare Function Used by the IWG to Calculate the SCGG Is Arbitrary and Lacks Justification

The SCGG values in the TSD are calculated using a social welfare function, the selection of which is normative in nature. The selection of the particular social welfare function used by the IWG is problematic for several reasons.

First, any number of alternative social welfare functions could be used to assign a value to the effects of greenhouse gas emissions on societal well-being, because the selection of the social welfare function is a value judgment made by analysts. Alternative social welfare functions are available in the academic literature. The IWG has not provided sufficient explanation for why it chose to use the particular social welfare function that it did.

Second, the social welfare function used (which is drawn from the Ramsey growth model) conflicts with a directive from President Biden regarding modernizing regulatory review. Biden has directed OMB to produce a set of recommendations that “promote . . . the interests of future generations,” which is clearly at odds with the social welfare function being used by the IWG, which treats the present generation as a dictator (more discussion of this issue comes later).

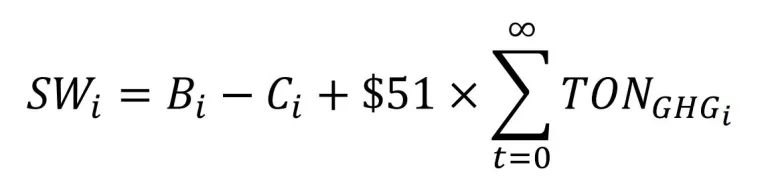

To demonstrate the arbitrariness of the IWG’s current approach, consider the following social welfare function:

I am not necessarily recommending that the IWG use the social welfare function in the equation (although greenhouse gas emissions may be correlated with things that people value); I present this equation only to point out the completely arbitrary nature of the social welfare function currently being used by the IWG. One could just as easily identify a social welfare function that reaches completely opposite policy conclusions—as I have just shown with equation (1). Without any explanation, how can one know which social welfare function is superior?

Recommendation 2: The IWG should be explicit about which social welfare function it is using, and it should explain why it selected that particular social welfare function.

Additionally, the social welfare function utilized by the IWG is not consistent with producing “an assessment of the potential costs and benefits” of a regulatory action, as is required under executive order 12866. Thus, the values in the TSD should not be used in any benefit-cost analysis. This is the case because, rather than assessing the dollar value of impacts, the TSD filters greenhouse gas impacts through a social planner’s welfare function before final headline numbers are reported. The values reported in the TSD are estimates of a social planner’s well-being, not estimates of benefits or costs (which are measured in dollars). This issue leads to confusion throughout OMB and IWG documentation. For example, the Federal Register notice from OMB announcing the opening of the comment period on the IWG report states “the Executive Branch has developed a set of estimates that represent the monetized impact to society associated with an incremental change in greenhouse gas emissions.” This statement is incorrect as written, as what is being reported is not a money value. In fact, calculations of the SCC, SCM, and social cost of nitrous oxide are incorrectly labelled throughout the TSD as well, including in tables ES-1, ES-2, and ES-3, where the primary values are reported. The numbers in these tables are reported in dollar terms, but what are actually being measured are estimates of well-being. Values represent units of the well-being of a social planner (or someone similar), and they should be reported as such.

Recommendation 3: The IWG should report units accurately when reporting the SCGG values. The IWG should make clear that the units the SCGG values are measured in which are units of the well-being of a social planner or of society. Alternatively, the term “well-being dollars” would be appropriate.

Recommendation 4: The IWG should make clear that the SCGG values are inappropriate for use in any benefit-cost analysis, where the relevant impacts are measured in US dollars.

The IWG should acknowledge the normative nature of the SCGG metrics, given that they are statements of what policy should aim to do according to analyst preferences, not a statement of what greenhouse gas emissions actually do to the environment or the economy. As such, I also recommend the following:

Recommendation 5: The IWG should acknowledge that the SCGG values are normative statements of analysts’ political priorities, divorced from objective science.

The Social Discount Rates Used by the IWG to Calculate the SCGG Are Arbitrary and Lack Justification

Like the social welfare function, the social discount rate is a normative input in benefit-cost analysis. To its credit, the IWG acknowledges that certain ethical values go into the selection of this rate, but it falls short of acknowledging the full truth, which is that selection of this rate is entirely dependent on value judgments. There is no objective scientific way to arrive at the rates currently being used by the IWG.

The TSD identifies several ways in which the selection of the social discount rate could occur. One approach is to follow OMB’s guidance in Circular A-4, which is to base the social discount rate on market interest rates. There are at least two problems with this approach. First, there is no compelling reason why one should rely on market interest rates to select the social discount rate, as opposed to any other method. This is especially true of policies (like those related to greenhouse gases) with intergenerational consequences. Future generations cannot participate in present markets, so present markets will not reflect their preferences. Second, OMB’s discount rate guidelines in Circular A-4 are flawed and should not be replicated. For example, Circular A-4 discounting guidance leads regulatory agencies to fail to account for the opportunity cost of capital properly, because Circular A-4 conflates two concepts: the social discount rate and the opportunity cost of capital. If anything, aspects of the discounting guidelines in Circular A-4 should be abandoned, not given more legitimacy by being cited in the TSD.

Recommendation 6: The IWG should not double down on the most problematic aspects of OMB Circular A-4, such as its social discounting guidance.

Recommendation 7: The IWG should make clear that the consumption rate of interest used to discount the SCGG and the opportunity cost of capital are two different concepts.

Recommendation 8: The IWG should make clear that there is no objective reason why market interest rates should be the basis for selecting the social discount rate.

In addition to discussing basing the social discount rate on market interest rates, the TSD discusses using the Ramsey equation to select a social discount rate. Following this approach, the social discount rate is “approached from the perspective of a social planner who wishes to maximize the social welfare of society.” The discount rate in this method is the planner’s rate of time preference, and it serves as a device to convert benefits and costs from dollar values into units of the planner’s well-being.

The Ramsey equation provides a useful way to explain the role of the social discount rate in a benefit-cost analysis. The social planner abstraction is used as a proxy to represent the current generation’s well-being. However, the parameters of the Ramsey equation still require ethical judgments for their selection, and there is no reason to believe that the analysts who work on the IWG have any particular expertise in this area.

Given these facts, I recommend the following.

Recommendation 9: The IWG should acknowledge the normative nature of the social discount rate and be upfront that ethical judgments, which likely fall outside the expertise of analysts, are required to identify a social discount rate.

Recommendation 10: The IWG should acknowledge that the social discount rate is often interpreted as the rate of time preference of a social planner.

Recommendation 11: The IWG should acknowledge that what is being measured after social discounting is the well-being of a social planner or of society, either one being an abstraction meant to capture the welfare of the current generation of citizens.

Conclusion

There is a very real danger that the values reported in the TSD will be perceived as objective scientific inputs in regulatory analysis, as opposed to what they are: statements reflecting the political priorities of analysts. No doubt some serious scholars have been involved in the calculation of these values, but when they work in this context, they are stepping outside of the domain of scholarship and entering into the domain of political advocacy. There is nothing wrong with political advocacy, per se, but political advocacy should not masquerade as objective science, and there is a danger of this occurring with the SCGG values in the TSD.

The IWG should be explicit and transparent about the value-laden nature of the metrics it is producing, or it should cease to use these metrics altogether and focus on scientifically based measures of the impacts of greenhouse gases instead, measures that should be consistent with objective assessments of benefits and costs.

Attachments (2)

“The Social Discount Rate: A Primer for Policymakers” (Mercatus Policy Brief, Mercatus Center at George Mason University, Arlington, VA, June 2020)

“What Is vs. What Should Be in Climate Policy: The Hidden Value Judgments Underlying the Social Cost of Carbon” (Mercatus Policy Brief, Mercatus Center at George Mason University, Arlington, VA, April 2021)

Appendix A: Cost Estimates for Obama-Era Regulatory Proceedings Utilizing the Social Cost of Carbon or Social Cost of Methane

It is estimated that the Obama administration employed the SCC or SCM metrics to justify regulatory proceedings with an estimated total cost of between $447 billion and $561 billion (in 2020 dollars). This analysis uses a list of 83 rulemaking actions found in a 2017 paper by Peter Howard and Jason Schwartz that is presented in table A-1. The authors note that at that time, “at least eighty-three separate regulatory or planning proceedings conducted by six different federal agencies have used the SCC or SCM in their analyses.”

Using this list of 83 regulatory proceedings as a starting point, I employ the following methodology to calculate the cost of these rules. I collect the Federal Register notices for each of the 83 items (or, if the item is not a regulation, I collect the relevant primary document). Next, I identify cost estimates in the regulatory agencies’ regulatory impact analyses. These numbers are found either in the preamble of the rulemaking notice or in a separate regulatory impact analysis document. The usual practice of regulatory agencies is to calculate costs using 3 percent and 7 percent discount rates, so I collect both sets of cost estimates. In cases where the agency calculates a range of costs, I take the average of the range calculated at each discount rate.

Some costs are reported by the agency as a present value, whereas others are reported in annualized form. Meanwhile, still other estimates are calculated for specific benchmark years only. For annualized costs, I identify the time horizon of the analysis and convert costs from annualized to present value using the relevant discount rate. For those rules with cost estimates in specific benchmark years, I assume costs occurred in only those years (which clearly underestimates the costs of these rules). However, for one rule, a series of benchmark years are presented over a 10-year time frame, so I interpolate costs for the missing years using the benchmark year values. Finally, I adjust all values for inflation to 2020 dollars and then aggregate the estimates. The range of estimates, $447 billion to $561 billion, reflects estimates calculated at the 7 percent and 3 percent discount rates, respectively.

There are a number of issues relating to uncertainty surrounding these cost estimates that should be noted. First, these are ex ante cost estimates, meaning that these are forecasts made by the regulating agency prior to a rule going into effect. Forecasts of the future can turn out to be incorrect. Moreover, numerous analytical assumptions go into these agency calculations, any number of which could turn out to be wrong or biased in some manner. Some regulations on the list are duplicates. Cost estimates from duplicate regulations are dropped from the total cost estimate. Some items are not regulations. For example, there are several environmental impact studies on the list. I assume that these items have zero cost. Some regulations are insignificant, or they otherwise do not have a cost estimate associated with them. I assume these have zero cost. Finally, some regulations are proposals, meaning that they were either later finalized or may not have been finalized. I include cost estimates for these regulations because they are regulatory actions that are supported using the SCC or SCM metrics.