- | Government Spending Government Spending

- | Working Papers Working Papers

- |

The Crisis in Public Sector Pension Plans

A Blueprint for Reform in New Jersey

In order to avert a fiscal crisis and ensure that future state employees have dependable retirement savings, New Jersey should follow the lead of the federal government and the private sector and

Pension plans operated by state governments on behalf of their employees are underfunded by an estimated $452 billion according to official reports,1 with total liabilities of $2.8 trillion and total assets of $2.3 trillion in 2008. However, many economists argue that even these daunting liabilities are understated. Current public sector accounting methods allow plans to assume they can earn high investment returns without any risk. Using methods that are required for private sector pensions, which value pension liabilities according to likelihood of payment rather than the return expected on pension assets, total liabilities amount to $5.2 trillion and the unfunded liability rises to $3 trillion.2 The ability of governments to pay for the retirement benefits promised to public sector workers runs up against the reality of limited resources.

In this study, we consider the case of New Jersey, which operates five defined benefit pension plans for state employees.3 The New Jersey Senate unanimously passed legislation in February 2010 that would put a question on the November ballot to constitutionally require the state to begin to make its full annual payment to the state's pension system.4 The bill requires the state to catch up to paying its full obligation by FY 2018.5 From that year forward the state will be constitutionally required to make the full payment to its pension systems each year as calculated by plan actuaries. The state reports that its pension systems are underfunded by $44.7 billion, when liabilities are discounted at the 8.25 percent annual return that New Jersey predicts it can achieve on funds' investment portfolios.

However, when plan liabilities are calculated in a manner consistent with private sector accounting requirements, methods that economists almost universally agree are more appropriate,6 New Jersey's unfunded benefit obligation rises to $173.9 billion.7 This amount is equivalent to 44 percent of the state's current GDP8 and 328 percent of its current explicit government debt. This calculation applies a discount rate of 3.5 percent (the yield on Treasury bonds with a maturity of 15 years) to reflect the nearly risk-free nature of accrued benefits for workers. It is estimated if state pension assets average a return of 8 percent, New Jersey will run out of funds to meet its pension obligations in 2019. If asset returns are lower than 8 percent, they will run out of funds sooner.9 State actuaries estimate that under certain assumptions, New Jersey's pension plans will run out of assets to make benefit payments beginning in 2013.10

Given the costs and risks inherent in the defined benefit plan to taxpayers, as well as the political incentives for legislators to overpromise benefits to public sector workers while shirking on the state's contributions, the state should close the current defined benefit plan to new workers and expand the existing defined contribution plans for all new state and local workers. Shifting employees to a defined contribution plan would ensure that New Jersey's pension system for its public sector workforce is sustainable in the long term and reward younger workers with a guaranteed employer contribution to their individual retirement.

New Jersey currently operates two defined contribution plans. The Alternative Benefit Plan (ABP) serves 17,000 faculty and administrative staff in the state's universities and colleges. In addition, in 2007 the state established the Defined Contribution Retirement Program (DCRP) with limited eligibility for elected and appointed officials and current participants in the Public Employees Retirement System (PERS) and Teachers' Pension Annuity Fund (TPAF). Either could serve as a model for a future defined contribution plan for all public sector employees.

To fund the debt owed to current DB participants, the state must take immediate action. This includes some or all of the following: capping salaries, increasing employee contributions, reducing the rate of the accumulation of future benefits, reducing annual cost of living adjustments (COLAs), and increasing the retirement age. These measures will reduce the size of the future benefits-funding burden and thus enable the state to better manage its pension obligations to employees vested in the system.

The alternative is to continue the DB gamble—promising benefits to public sector workers while concealing the size of that obligation to taxpayers. The current level of underfunding indicates that New Jersey will have a difficult-to-impossible task in keeping its commitments to current public sector workers. To continue adding workers and liabilities to the defined benefit plans is not tenable and represents a promise that the public cannot afford.

I. Public Sector Pensions: the Defined Benefit Plan

There are two general types of retirement plans: defined benefit plans and defined contribution plans. Most state and local governments in the United States offer defined benefit pension plans to their workers.

Under a defined benefit (DB) plan, the employer promises employees a regular pension payment (i.e., an annuity) over the worker's retirement years.11 The amount of the benefit payment depends on the worker's age, years on the job, and a measure of their final salary.12 More specifically, benefit formulas generally pay a given percentage of the employee's final salary multiplied by the number of years of employment. In a defined benefit plan, investment risk is borne by the employer since the employer's payment is independent of the investment return earned by the pension's fund.

In a defined contribution plan (DC), workers and employers make contributions to an investment account, such as a 401(k), 403(b), or the federal Thrift Savings Plan. Workers own and generally manage these accounts and bear the tradeoffs between risk and reward entailed by the investments they choose.

Because defined benefit retirement payments are guaranteed by state laws or constitutions but financed with a portfolio of risky investments subject to market risk, defined benefit plans present a distinct fiscal risk to taxpayers. Defined benefit plans obligate the employer to pay out benefits regardless of the financial status of the pension system when the employee retires. Current actuarial practice and accounting standards have contributed to a systematic underestimation of the size of the obligation owed to public sector employees, creating a moral hazard problem. Legislators are able to overpromise benefits, often negotiated by public sector unions, while passing the cost of these promises on to future taxpayers. Since most state constitutions treat public sector pensions as a form of debt, it is unlikely that states can default on pension obligations to employees without constitutional amendments.13

There are 222 defined benefit plans operated by the states covering 90 percent of public sector workers in the states. These plans cover 20 million employees and seven million retirees.14 In addition, there are 2,434 plans operated by local governments serving a smaller portion of public sector workers.15

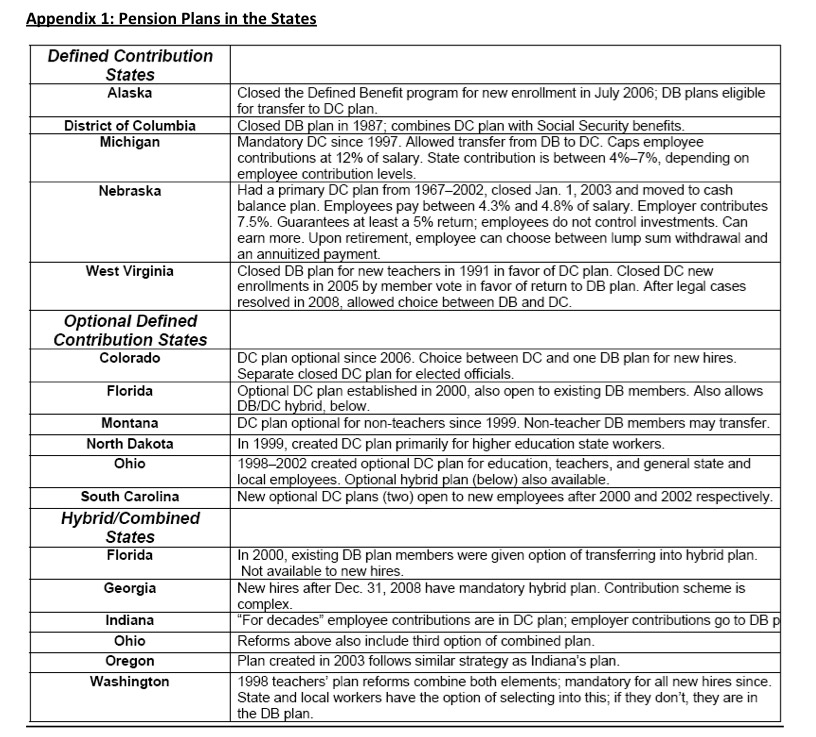

A few states have elected to move their employees to the defined contribution plan. Michigan closed its DB plan to new entrants in 1997. And Alaska moved to a DC plan in 2003. Florida, Nebraska, and Ohio offer hybrid plans. (See Appendix 1)

Why Are Plans Underfunded?

The magnitude of underfunding stems from how pension obligations have been actuarially valued and how governments have chosen to manage pension funding and benefit levels. The dramatic downturn in market performance in the last few years, while harmful, is not the primary cause of underfunded public sector pension plans.

Pension plans have been systematically weakened by interactions between actuarial practice the tendency for governments to make unrealistic promises to employees, and the choice of governments to contribute less than what plan actuaries recommended to fund plans over a period of years.

Public pension actuarial practices assume that plan assets can earn high rates of return, leading actuaries to calculate employer contributions at a lower level than needed to fund plan liabilities. In addition to understating required employer contribution amounts, because GASB funding rules for public pensions are a recommendation and not a requirement, many state governments have routinely put aside less than what was recommended by plan actuaries to meet future obligations.16 In other words, pension accounting lowers the standard for plan funding, and even then, many state governments have failed to meet it.

How Defined Benefit Public Pension Plans Are Funded and Valued

Public sector-defined benefit plans are financed by current employer and employee contributions and the returns on the investment of those assets.17 Typically, these contributions are invested in a mix of stocks, bonds, and other financial instruments. In recent years, plans have increasingly turned to more exotic investments, including hedge funds and private equity.18 Pension plan investments are managed by financial managers selected by the pension board.

The amount contributed by the employer and the employee to fund the pension system is calculated by actuaries who determine the size of the obligation promised to employees. Actuaries value a pension plan based on demographic and economic assumptions, such as estimated age of retirement, mortality rates, salary growth, and inflation, to arrive at an "Annual Required Contribution" (ARC). If the actuarial assumptions are reasonable, the ARC approximates the amount that needs to be contributed annually (by employers and employees) to ensure the payment of future obligations.

These actuarial assumptions and practices play a large role in determining how much governments must contribute to ensure a well-funded plan. Inaccurate assumptions or unsound practice can result in an underfunded plan. If the actuarial assumptions closely reflect actual outcomes, then paying the ARC in full should result in a well-funded pension system.

To determine the funding status of pension plans, actuaries perform annual actuarial valuations measuring the plan's accrued liabilities and compare liabilities to the value of the plan's assets. Comparing plan liabilities and assets allows actuaries to determine the degree to which the plan is funded and able to pay out promised benefits. Actuaries calculate two basic measures of pension plan performance. These are the funding ratio—the plan's assets divided by the plan's liabilities—and the unfunded liability—the plan's assets minus the plan's liabilities. Plans that are 100 percent funded and have no unfunded liabilities are considered "fully funded."19

How Reliable Is the ARC? The Role of Actuarial Methods

According to the Government Accounting Standards Board (GASB), the ARC is to be calculated so that it covers annual benefit accruals and spreads any unfunded liability over a 30-year amortization period.20 One practice that has contributed to the pension funding gap is the selection of an improper discount rate when valuing pension plan liabilities. Discounting allows one to value a future benefit in today's dollars. It asks, "How much is needed to put into the pension system today in order to pay out a promised benefit in the future?" According to the Government Accounting Standards Board (GASB) ruling 25 and Actuarial Standards of Practice (ASOP) item 27, public pension liabilities are to be discounted by the expected rate of return on pension assets. Typically public pension funds assume they will earn nominal returns of around 8 percent annually, using this interest rate to discount future benefit liabilities back to the present.

However, most economists believe this approach to be fundamentally flawed, running contrary to both financial theory and the practice of financial markets, which hold that the means by which a liability is financed is irrelevant to the value of that liability. For instance, Donald Kohn, the Vice Chairman of the Federal Reserve Board, recently stated that

While economists are famous for disagreeing with each other on virtually every other conceivable issue, when it comes to this one there is no professional disagreement: The only appropriate way to calculate the present value of a very-low-risk liability is to use a very-low-risk discount rate."21

Discounting public sector pension liabilities at the expected rate of return on pension assets violates a number of economic precepts, including:

- The Modigliani-Miller theorem, which holds that the value of an investment project is independent of how it is financed

- The Black-Scholes options pricing formula, which shows that guarantees against market risk grow more expensive over long periods and when the underlying asset is more volatile (public pension accounting holds that long-time horizons justify ignoring market risk and that holding riskier, higher-returning assets improves a pension's funding level)

- The Arrow-Lind theorem, which holds that governments can ignore the risk of investments only when the investments are small relative to and uncorrelated with the size of the tax base and

- The general "law of one price," which holds that two investments producing similar income streams should carry similar prices (public pension accounting implies that governments can produce the same level of pension benefits at roughly half the cost of a private firm).

For consistency with economic theory, the practice of financial markets, and rules applied to private sector firms, liabilities should instead be valued according to the risk inherent in those liabilities. To do otherwise implies limitless possibilities for riskless arbitrage, producing potentially absurd results.22

From the perspective of workers, defined benefit pensions in the public sector are risk-free; they are guaranteed benefits by the state, which has the power to tax. This means, of course, that from the perspective of the taxpayer, the liability is a near-certainty. The discount rate chosen to value future liabilities in the plan, therefore, should reflect the low-risk character of the benefits promised to workers.23

From the government's perspective, it is appealing to use a higher discount rate to estimate plan liabilities because it produces a lower annual contribution. By contrast, a low discount rate will result in a higher annual contribution required by the employer (in this case, the government) to fund pension obligations.

Over the past decade, state pension liabilities have been valued using an average discount rate of 7.97 percent.24 This may seem reasonable, since the median investment return for pension assets over the past 20 years has been around 8 percent. However, returns on market investments are not guaranteed, as the market downturn of 2001-2002 and the crash of 2008 demonstrate.25 Even if plans accurately predicted average market returns over a very long period, the majority of plans' obligations are payable over the next 15 years, in which average market returns would be more uncertain. There is a significant possibility—and in some cases, a probability—that a "fully funded" plan would be unable to meet its obligations even if the plan accurately projected average market returns.26

In addition to understating funding requirements, using a high discount rate to value public pension liabilities encourages plan managers to invest in higher risk portfolios in order to target the expected rate of return, producing bad incentives in the management of pension assets.27 Instead, financial theory suggests pensions should be discounted according to the lower risk (and lower return) Treasury bond rating of 3.5%.28

When applying a much lower discount rate, based on the return on Treasury bonds, the size of pension obligations is far larger than state estimates,29 rising from $2.8 trillion nationwide to $5.2 trillion.30 In other words, the size of the obligation owed to public sector workers will require a far larger contribution than current actuarial reports would suggest.

Boom and Bust: Pension Asset Investments

By assuming a higher rate of return on pension assets investments, states pursued investment strategies that favored higher-risk, higher-volatility investments.31 Before the 1980s most systems held their assets mainly in fixed-income securities. Investment choices were restricted by legal lists. In the 1980s legal lists were replaced with the "prudent person" rule.32 Moving to this standard allowed pension systems, as long as standards of diversification and prudence were met, to hold larger percentages of equities and capture the higher returns being generated in a booming market.33

During boom years the effect of high returns on pension assets may have induced other behavioral changes in the management of pension assets and encouraged more risk taking with pension assets. Because the I.R.S. code states that "no part of plan assets may be used for purposes other than the exclusive benefit of employees and beneficiaries" the guaranteed benefit coupled with the workers' claim on surpluses compound the moral hazard problem in the management of public pensions. Where accounting methods base pension asset valuations on a high-risk expected rate of return, political pressure may result in excess surpluses of pension assets being distributed to public employees as enhanced benefits. This magnifies the incentive to take risks in pension asset investments in order to apply surpluses as expanded benefits, particularly in plans that have heavy employee representation.34

This is borne out in the changing makeup of public pension assets investments. Following the advent of the "prudent person" rule, these investments have increasingly been invested in higher-return and higher-risk vehicles.

In 1990, 40 percent of public sector pension assets were held in equities, rising to 70 percent in 2006, roughly 10 percent higher than the allocation of pension assets to equities in private pension systems.35

The Employer: How Public Pension Plans are Over-promised and Under-delivered

In the case of many state pension plans, governments may choose to pay less or more than the ARC.36 The ARC is a recommendation, not a requirement. As we outlined above, ARCs calculated under current pension accounting rules are inadequate to guarantee that plans can meet their obligations. And many state governments fail to pay even the ARCs that are calculated, leaving plan funding well short of what is truly needed. The result is greater costs and greater risk shifted onto future taxpayers.

The amount contributed to the pension system by the government is the employer contribution, sometimes referred to as the statutory contribution. In many states, the annual contribution made to pension systems has been below the ARC. These choices made by many state governments include putting off payments into the pension system—pension deferrals or "pension holidays"—contributing less than the ARC in order to expand spending in other areas or to avoid tax increases, and awarding increases in retirement benefits for public sector employees in lieu of salary increases. All of these result from the incentives facing the employer—the state—as pension plan steward.

In the private sector the employer may also pass on the risk of an underfunded pension plan. Private sector pensions are guaranteed by the Pension Benefit Guaranty Corporation (PBGC). This guarantee creates the potential for moral hazard in how private sector pensions are invested. Since benefits are partially guaranteed, private sector pension managers for troubled firms may be incentivized to embrace a higher-risk investment strategy.37 From the point of view of the worker covered under a private sector DB plan, a high risk investment strategy may not be as appealing. If a private employer defaults on their pension obligation to employees, the amount paid out by the PBGB may be less than the amount the employer promised.38

In the case of public sector plans, the states pass on the cost associated with the guarantee of full benefits to the taxpayer. Since the state has the power to tax, from the worker's perspective this is the equivalent of a 100 percent guaranteed benefit, regardless of the financial condition of the pension plan when they retire. Taxpayers are responsible for pension deficits, but workers often have a claim on pension surpluses. How plan surpluses are treated may influence investment and funding choices of governments. For example, plan surpluses may be shared between taxpayers (in the form of a reduced state contribution) and employees (as enhanced benefits).39 During a bull-market, pensions may experience surpluses even when contributions are zero, creating an incentive for public sector employees to favor heavier investment of pension assets in high-risk assets.40

The magnitude of the pension crisis in the states points to the inadequacy, and fiscal dangers, of offering defined benefit plans to public sector workers. Actuarial methods informed by the Government Accounting Standards Board are flawed and reflect inadequate understanding of the proper treatment of pension liabilities. Governments as employers and pension stewards face very different incentives than employers in the private sector, since liabilities are guaranteed by taxpayers at 100 percent of their value. States have effectively misused pension funds—underfunding obligations to balance budgets or expand spending—while overpromising benefits to workers.

The Alternative: The Defined Contribution Plan

In a defined contribution plan the employer and employee generally each contribute a certain percentage of the employee's pay to an individual pension account. These contributions are invested in a combination of stocks, bonds, and other instruments, and grow over time. The key difference between the DC plan and the DB plan is the assignment of risk. In a DC plan, the risk or reward of varying investment performance is borne by the employee, who receives a higher or lower pension based upon the returns generated by investments held in his account. The employer's obligations are to manage the plan and to make annual contributions as promised; the employer bears no contingent liability regarding the performance of plan assets. The risk is transferred from the employer (or in the case of the public sector, the taxpayer) to the employee. In a DC plan, the employer's financial obligation ceases when the required contribution is made to the individual employee's retirement plan.

The risks borne by the employer in a defined benefit pension are one reason why, beginning in the 1970s, the private sector began to switch to offering its employees defined contribution plans. Between 1979 and 1998, the share of employees covered by DB plans fell by 17 percent and the share of those covered by DC plans rose by 12 percent.41

A second reason that the private sector switched to the DC system is that it offers employees greater mobility. Benefits are less "portable" in a DB system. In most DB systems, an employee's accrued benefits depend on their final salary at the time they terminate employment. If an employee moves jobs multiple times to different pension systems and has multiple DB accrued benefits, the total of all vested benefits is less than what the benefits would be if the employee stayed in one system.42 Once vested in a particular defined benefit pension plan, the employee risks losing a significant amount of benefit income by terminating too early or moving around too often.43 This makes DB pensions less attractive to younger, more mobile workers that employers might wish to attract.

Can a State "Catch Up"?

If state pension plans were frozen today with no new employees eligible for benefits, would states be able to catch up to their obligations to current beneficiaries? With lower asset values than in prior years and rising numbers of retirees, states now face difficult policy options as they attempt to catch up on pension funding contributions during a period of prolonged decreases in revenues, even as employees continue to accrue rights to future benefits. Since states are either constitutionally or statutorily obligated to pay out benefits, the size of that underfunding means that either benefit amounts and salaries must be reduced, taxation must be significantly increased, or states may be faced with a default-scenario.

II. Case Study - New Jersey

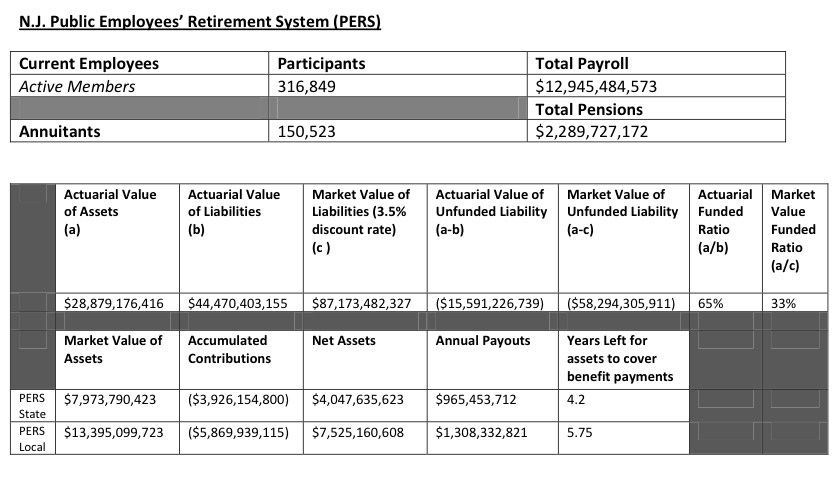

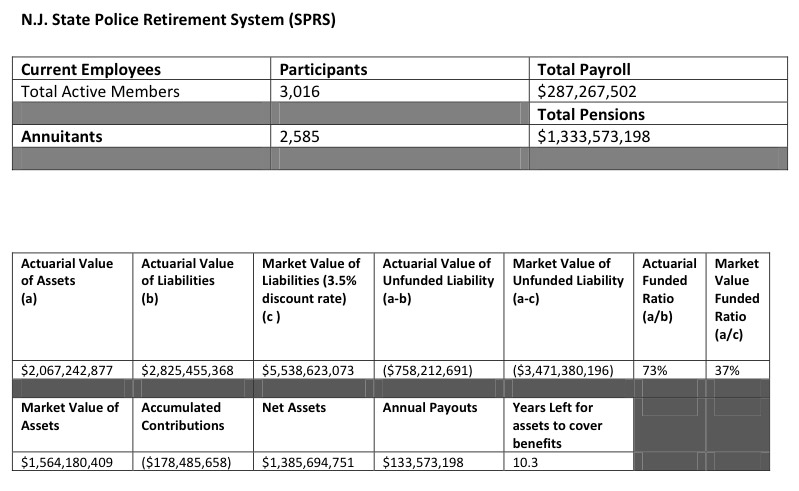

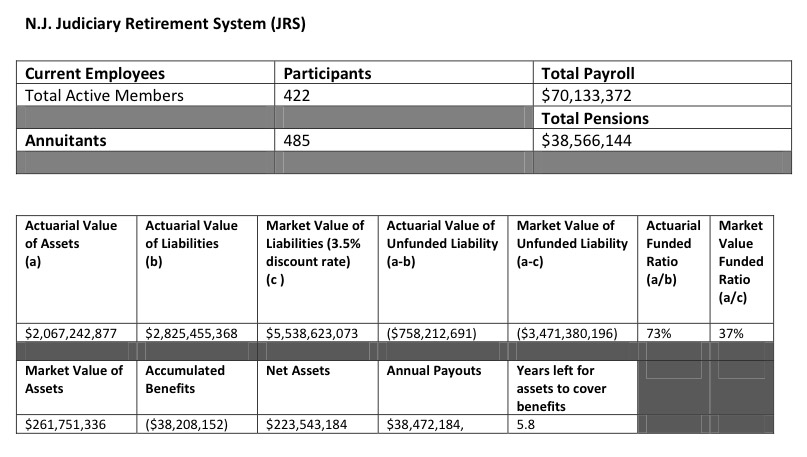

The State of New Jersey operates five defined benefit pension plans.44 These include the Teachers Pension Annuity Fund (TPAF), the Police and Firemen Retirement System (PFRS), Public Employees Retirement System (PERS), State Police Retirement System (SPRS), and the Judicial Retirement System (JRS).45

In total, New Jersey's five active defined benefit plans cover 770,869 workers. In FY 2010 the plans paid out $5.85 billion to 265,296 retirees and beneficiaries.

The actuarial assumptions used to value New Jersey's pensions include an assumed rate of return on pension assets of 8.25%. The assumed rate of return is established by the State Treasurer, not by plan managers or actuaries. Applying this rate of return, New Jersey pensions face an unfunded liability of $45.8 billion as of June 30, 2009. When applying the rate of return on investments that reflects the risk- free character of pension obligations, such as the current Treasury bond rate of 3.5%, the unfunded liability in New Jersey's state pensions increases to $173 billion.46

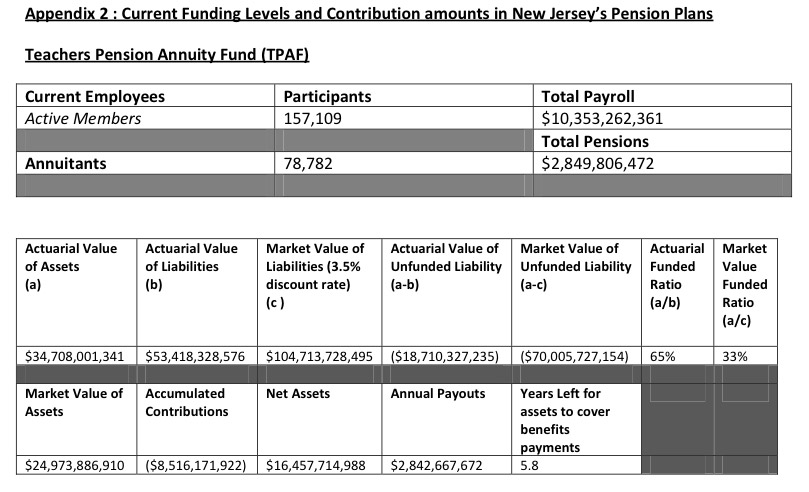

Given the current market value of assets and the previous year's benefit payments, state actuaries calculate that New Jersey's pension plans will start to run out of money in 2013.47 This projection is based on a specific scenario, one that excludes gains from investment income, state and employee contributions, and changes to the size of benefit payments. (See Appendix 2 for the unfunded liability and years until benefits are exhausted in each plan.)

How Pensions Have Been Managed and Promised in NJ

The implicit debt facing New Jersey in its underfunded pension plans, as with most states, was encouraged by the actuarial methods used to value the plans and the choices of legislators over a period of years to extend generous benefits while deferring payments to the pension funds. More stringent accounting rules would have encouraged greater funding and more restrained benefit growth over time.

Several changes undertaken in the 1990s changed how the New Jersey pension system was valued, allowing the state to lower its annual contribution. In 1992 under Governor Jim Florio, the Pension Revaluation Act (PRA), (L. 1992, C.41) changed the interest rate assumption used to calculate plan liabilities, replacing the book value interest rate assumption of 7 percent with the market value interest rate assumption of 8.75 percent.48 A higher assumed rate of return on funds allowed localities to reduce their pension contributions in FY 1992 and FY 1993 by $1.5 billion. The legislation was intended to help balance the FY 1993 budget and pay for unfunded cost of living adjustments adopted in the 1970s.49

In 1994, the Pension Reform Act (L. 1994, C.62) required the state to switch the method it used to value the fund from the Entry Age Normal method (EAN) to the less-demanding Projected Unit Credit Method (PUC) and reset the amortization period for the unfunded accrued liability from 30 to 40 years. Additional changes, including a downward revision in the COLA assumption and a reduction in the average salary scale, led the state to reduce state and local employer contributions to the pension plans by $547.4 million in FY 1994, and by $946.8 million in FY 1995, allowing Governor Christie Whitman to reduce taxes and present a balanced budget.50

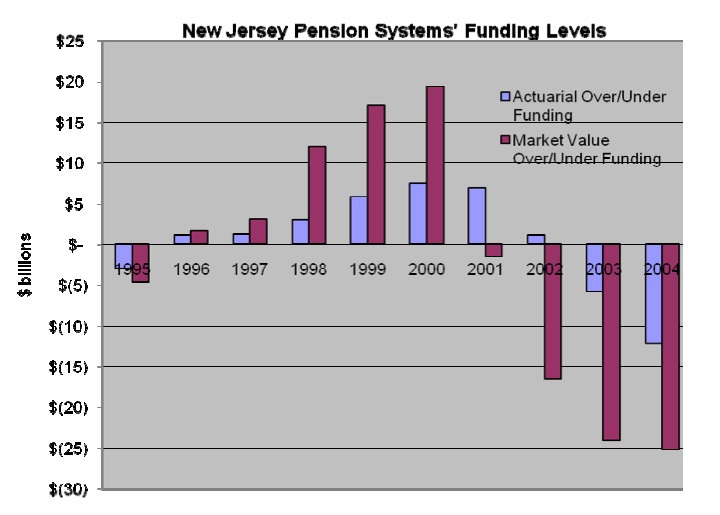

These gains were temporary, the results of assumption changes rather than reality. The switch in methodology and changed assumptions led to an underestimation of contribution amounts, producing a funding gap. To close the gap, in 1997 The Pension Security Plan permitted the state to issue $2.8 billion in pension obligation bonds which were used to partially eliminate a $4.25 billion unfunded liability that had surfaced.51 The proceeds of the bond sale were deposited into the pension system.

Full annual contributions were made to New Jersey's pensions until 1997, but states may defer payments to pension systems when they contain excess assets. During this period the pension system invested heavily in technology stocks.52 In 2000, technology stocks comprised 32 percent of the pension plans' common stock allocations.53 The boom in high-tech stocks during the late 1990s coupled with the pension bond gave the temporary appearance of a fully funded plan.

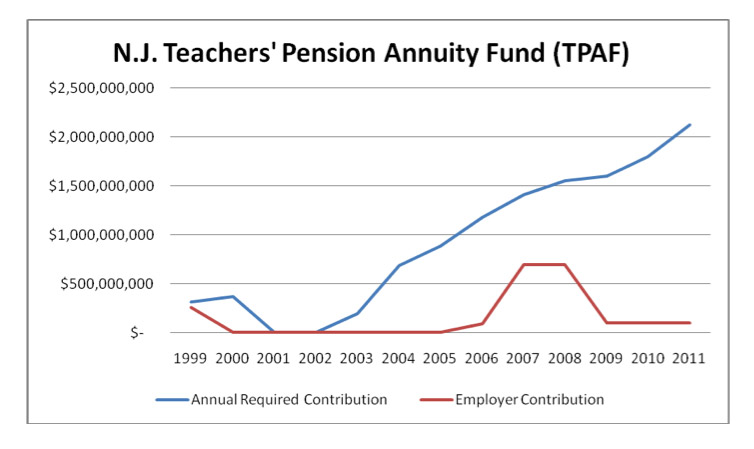

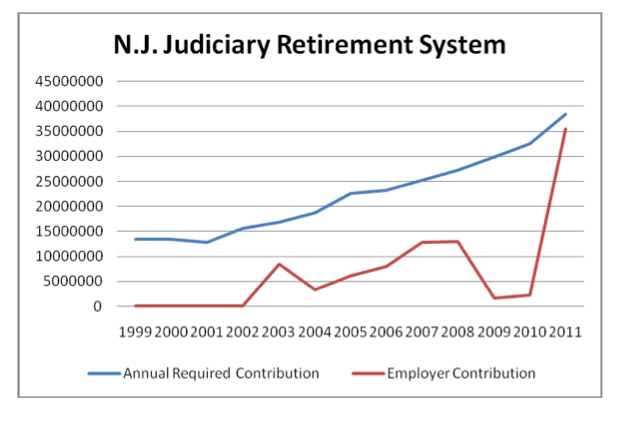

Once excess assets were exhausted, the pension quickly returned to its underfunded status. Pension deferrals also weakened the system. While deferring payments provides short-term budgetary relief to state and local governments, it also creates a fiscal illusion. In the short-term, governments adjust their behavior, dedicating revenues meant for the pension system to other areas. When scheduled contributions resume, governments find they are unable to pay the full amount because they have adjusted their spending behavior by treating temporary payment reductions as permanent. This necessitates a gradual "phase-in" of full contributions.

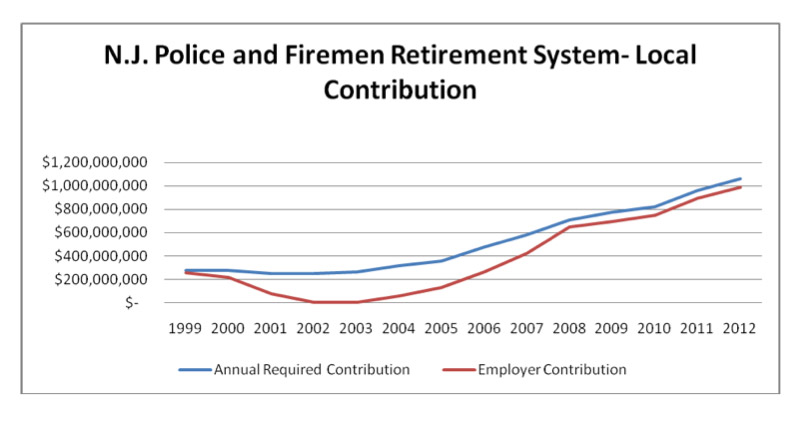

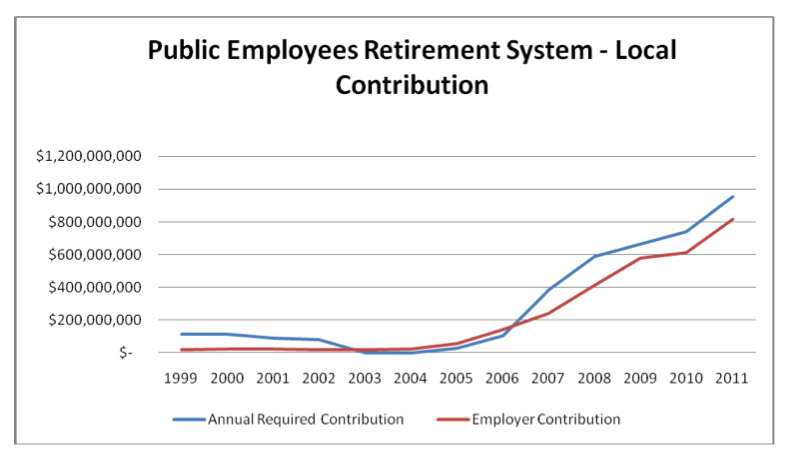

In 2003, local governments gradually began to increase their contributions at increments of 20 percent a year until they reached 100 percent of the calculated local contribution for the ARC in 2008. Phase-ins, by continuing to delay full contributions to the system, increase the amount needed to fully fund the pension system.

In addition to deferring the employer's payment, the state reduced the amount required for employees to contribute to their retirement. In January 1998, the State Treasurer reduced the employee contribution rate in the TPAF plan from 5% to 4.5% through 2001. The rate was further reduced to 3% until December 31, 2003. In January 2004, the TPAF employee contribution rate returned to 5%.

In the PERS plan the employee contribution rate was reduced to 3% from January 1, 2000 through June 30, 2004, at which time it reverted back to the 5% contribution for state PERS employees. The 3% employee contribution rate remained in effect for local PERS employees until January 2005.

Deferred contributions and accounting changes were coupled with a series of pension enhancements. In 1999 benefits were extended to surviving spouses, increasing liabilities by $500 million. In 2001 several bills were passed that increased benefits for current and retired employees by 9.12 percent by changing the percentage used to calculate benefits, effectively raising the percentage of average salary being replaced in the annual benefit.54 This act coincided with the bust of the dot-com bubble leading to a significant increase in the size of the plans' unfunded liabilities.

In 2007, Governor Jon Corzine promised "serious restructuring" of the pension system. A few minor changes were made. The Public Employee Pension and Benefits Reform Act of 2008 increased the retirement age from 60 to 62,55 and income eligibility requirements for a teacher's pension were increased to $7,500. In March 2009, the legislature approved the governor's proposal to allow municipalities to defer, for the next year, half of their payments into the pension system to prevent an increase in property taxes.

Governor Chris Christie signed legislation on March 22, 2010 to reduce the size of the unfunded liability. These measures include capping payments for unused sick days, banning part-time workers from receiving pensions, and requiring government workers to contribute 1.5 percent of their salaries toward health care. Legislation also adjusted the formula used to calculate benefits, returning to the pre-2001 formula where benefits equalled 1.7 percent of final salary times number of years of service, versus 1.8 percent of final salary in the TPAF and PERS plans. Also, members of these plans would have their retirement allowance calculated based on the final five years of service, instead of the final three. However, these changes to benefits would apply only to newly-hired public employees. Current workers, even those who recently entered the job rolls, would be able to continue under the current benefit formula for the rest of their careers.56

These measures will help at the margins but do little or nothing to address the size of the liability that has already been accrued. The rate of accrual of benefits will have to be reduced further, and employees will have to contribute more to their plans. The state must recognize that adding more workers to a system that is underfunded by $173 billion by market standards, representing over 40 percent of New Jersey's GDP, is not a tenable option.

Recommendations

1) Extend the Defined Contribution Plan.

The State of New Jersey made a decision to offer a DC option to state employees in 1965 when it created the Alternative Benefit Plan (ABP) for university faculty and administrative staff. The ABP is a tax-deferred, defined contribution system in which university employees contribute 5% of their base salary to a tax-deferred investment account. This is matched by an 8% employer contribution.57 In this plan, participants are vested after one year of participation in the system. As a defined contribution plan, it offers workforce mobility to employees since retirement funds can be carried to a future employer or rolled into an IRA.

The state moved further toward this model in 2007 when it created the Defined Contribution Retirement Program (DCRP).58 The DCRP provides members with a supplemental retirement to the existing DB plans. The DCRP is a tax-sheltered defined contribution retirement benefit. Eligibility was at first restricted to state and local officials and employees of the PERS or TPAF systems who earn in excess of the established maximum contribution limits. In FY 2009/2010 this maximum wage was established at $106,800. Employees earning above the maximum are automatically enrolled (unless they waive participation.) In 2008, eligibility was expanded to those TPAF and PERS employees hired after November 2, 2008 who do not earn the minimum annual salary of $7,700.59

Employees contribute 5.5% of their salary and the state contributes 3%. The funds are invested in an account established with Prudential Financial, which administers the DCRP.

2) Reduce the liability.

The state should move to reduce the rate of accumulation of benefits for workers going forward. This includes adjusting the salary replacement factors used to calculate the final benefit. Chapter 1, P.L. 2010 changed the formula to calculate benefits in two important ways. First, pension benefits are now equal to 1/60th of final salary for each year of employment (from a prior value of 1/55th); second, final salary was increased from the highest three to the highest five years of services, for new hires. The State should consider going further than this; these standards should be applied to current participants, and not simply applied to new hires.

To reduce the size of the unfunded liability, the state should consider reducing or freezing cost of living adjustments (COLAs). For instance, a 1-percentage point reduction in annual COLAs would reduce the plan's accrued liability by approximately 10 percent.60

Alternately, COLA payments could be limited to the currently projected rate of 1.8 percent per year, based on the formula where COLAs are equal to 60 percent of the change in the Consumer Price Index. This would limit plan payouts in the case inflation were to exceed projected rates.

3) Transition non-vested workers to the DC plan.

Currently, there are 274,380 workers who are not yet vested in their benefits. These workers should be shifted to the defined contribution plan. The switch will accomplish two objectives. It will guarantee new workers with a current contribution to their retirement. And in the long run, it will replace the DB system with one that is sustainable while shifting risk away from the taxpayer and removing the moral hazard associated with the state's management and stewardship of public worker investments.

According to state actuarial reports, between 5 and 18 percent of accrued benefits are not yet vested.61 Shifting non-vested employees to a DC plan could reduce these liabilities, even if employee contributions to the DB plan were partially or fully refunded. Younger employees often prefer DC plans over DB pensions for reasons of portability, so it may be possible to come to an agreement with current non-vested employees. Such a change could significantly reduce plan liabilities while more quickly moving to a sustainable pension financing model.

These steps would not significantly reduce current pension liabilities. Accrued pension benefits, be they in the private sector or the public sector, are rarely reduced to any significant extent. However, shifting employees to a defined contribution system and/or reducing benefit accrual rates for employees who remain in the defined benefit programs would better insure that unfunded liabilities do not continue to grow over time. When the programs' unfunded liabilities are capped, the state can better plan how to pay off these debts over time. Without reforms, though, it is likely that unfunded pension obligations will continue to grow, eventually to an unsustainable level.

Conclusion

Public sector pension plans around the country face significant funding shortfalls, facilitated by accounting practices that understate true liabilities and state and local governments that often failed to meet their financial obligations even under these more permissive accounting standards. When measured on a market valuation basis, which is required of private sector plans and which economists universally believe to be the appropriate standard, public sector pensions nationwide are underfunded by more than $3 trillion. State and local governments around the country face massive fiscal consolidations as these bills come due.

New Jersey's public pensions are emblematic of pension funding problems across the country. Over the past two decades, New Jersey's plans loosened accounting standards and increased investment risk while the government often failed to meet its required contributions. As a result, New Jersey plans are underfunded by more than $100 billion on a market valuation basis. New Jersey has recently passed reforms that would increase funding and reduce benefits for newly-hired public employees. These steps are useful but must go much further if a potential fiscal crisis is to be averted.

We outline several steps New Jersey policymakers may consider. First, all newly hired employees should be shifted to a defined contribution pension model based upon the plan already offered to New Jersey's university employees. A defined contribution model is more attractive to the young, mobile employees state governments seek to attract and provides a clear measure of the state's funding obligations.

Second, current reforms lowering pension replacement rates should be continued and, if possible, extended to current employees. All vested benefits should be honored, but the rate at which future benefits are earned should be reduced. Such a change is commonplace in the private sector and there is no reason public employees should be exempted from such changes. Third, New Jersey pensions should consider reductions or freezes in COLA payments, which could reduce future benefit liabilities and spread the burdens of reform more evenly between taxpayers, newly hired employees and current employees, and retirees.

Finally, current employees who are not yet vested in their benefits might be shifted along with newly hired employees to a defined contribution plan. This step could produce savings to existing DB plans while moving more quickly to a sustainable pension model for public employees.

Additionally, New Jersey's pension reports contain useful and detailed information on plan liabilities and the distribution of benefits by age, experience, and earnings. However, these reports can be improved, in particular by making publicly available a more detailed analysis of the assumptions involved in projecting investment returns in the pension assets portfolio. Most public pension financial and actuarial reports make only a cursory effort to justify their investment return assumptions. This is particularly important given the crucial role the discount rate plays in public pension accounting.

ENDNOTES

1. "The Trillion Dollar Gap: underfunded state retirement systems and the roads to reform," The Pew Center on the States, February 2010, 2-3. We calculate the size of the unfunded liability applying a discount rate of 3.5%, the yield on Treasury bonds with a maturity of 15 years as of May 27, 2010.

2. Novy-Marx, Robert and Joshua Rauh, 2009. "The Liabilities and Risks of State-Sponsored Pension Plans," Journal of Economics Perspectives 23(4), 191-210, p. 42. This result is based on the premise, derived from Modigliani and Miller (1958), that a future obligation should be discounted at the interest rate on a portfolio that matches the timing and risk of its payments. Modigliani, Franco and Merton H. Miller, 1958, "The Cost of Capital, Corporation Finance, and the Theory of Investment," American Economic Review 48: 261-297.

3. These are the Teacher's Pension Annuity Fund (TPAF), the Public Employees Retirement Fund (PERS), the Police and Firemen's Retirement System (PFRS), the State Police Retirement System (SPRS), and the Judicial Retirement System (JRS). In addition, the state operates two defined contributed plans, the Alternative Benefit Plan (ABP), and the Defined Contribution Retirement Plan (DCRP). There are two existing defined benefit plans closed to current workers, the Consolidated Police and Firemen's Pension Fund (CPFPF), and the Prison Officer's Pension Fund (POPF). See, the State of New Jersey, Department of the Treasury, Division of Pensions and Benefits, http://www.state.nj.us/treasury/pensions/.

4. The proposal requires the state to contribute at least 1/7th of the Annual Required Contribution (ARC) in 2011 and increase the state's annual payment by at least 1/7th for each of the following six years to permit the state to gradually adjust to appropriating the full amount needed to contribute the total ARC. For text of Senate Concurrent Resolution 1, see http://www.njleg.state.nj.us/2010/Bills/SCR/1_I1.HTM

5. http://www.newjerseynewsroom.com/state/nj-pension-reform-bills-approved…

6. Current public sector pension accounting rules effectively violate well-accepted economic precepts such as the Modigliani-Miller results in corporate finance, the Black-Scholes formula for options pricing, and the general "law of one price."

7. Authors' calculations. Waring (2008) finds that the mid-point of a public pension's stream of future benefit payments is around 15 years in the future. Thus, a lump sum payment 15 years hence can be treated as an approximation of the annual benefit liabilities owed by a plan. Following Rauh and Novy-Marx, we compound the reported present value liability forward for 15 years at the expected rate of return, then discount back to the present at the Treasury interest rate. Waring, M. Barton, "Liability-relative investing," Journal of Portfolio Management 30(4).

8. In 2008 New Jersey's Gross Domestic Product was $390.35 billion and state debt was $52.785 billion.

9. Joshua D. Rauh, "Are State Public Pensions Sustainable? Why the Federal Government Should Worry About Pension Liabilities," National Bureau of Economic Research, May 15, 2010 p. 3.

10. According to New Jersey's actuarial reports, the state PERS plan will run out of assets to make its benefit payments in 2013. The plans for teachers (TPAF), judges (JRS), and local PERS employees will run out of assets between 2014 and 2015. The Police and Firemen's plans and the State Police Plan run out of funds between 2018 and 2019. This calculation is based on the assumptions that the plans experience no gains from investment income, no state and employee contributions, and no changes to the size of benefit payments.

11. Edwin S. Hustead and Olivia S. Mitchell, "Public Sector Pension Plans: Lessons and Challenges for the 21st Century," p. 6, in Pensions in the Public Sector, ed. Olivia S. Mitchell and Edwin C. Hustead, Pension Research Council The Wharton School of the University of Pennsylvania, University of Pennsylvania Press, Philadelphia, 2001.

12. Olivia S. Mitchell, David McCarthy, Stanley C. Wisniewski and Paul Zorn, p. 11 "Developments in State and Local Pension Plans" in Pensions in the Public Sector, eds. Mitchell and Hustead, 2001.

13. It is estimated that New Jersey's annual payout to retirees will reach $15 billion, half of the state's current budget, in 2017. In this case, the state may be forced to reexamine the constitutional protections that prevent the reduction in accrued benefits to retirees. See "Yes, a Public Pension Can be Forfeited," John Bury, NJ.com, June 28, 2008. (http://blog.nj.com/njv_johnbury/2008/06/yes_public_pension_can_be_forf…)

14. U.S. Government Accountability Office, "State and Local Government Retiree Benefits: Current Funded Status of Pension and Health Benefits," GAO-08-223, January 2008, p. 1, http://www.gao.gov/new.items/d08223.pdf.

15. Government Accountability Office, "State and Local Retiree Benefits," GAO-07-1156, p. 18, http://www.gao.gov/new.items/d071156.pdf.

16. According to The Pew Center on the States the collective liability for pension obligations in the states is $2.77 trillion, and states have contributed $2.31 trillion towards this obligation, leaving a $452 billion gap. However, when adjusting these numbers to reflect the riskless characteristics of these liabilities, the total liability rises to $5.2 trillion and the unfunded liability rises to $3 trillion. See "The Trillion Dollar Gap: Underfunded State Retirement Systems and the Roads to Reform," The Pew Center on the States, February 2010, p. 15.

17. Typically state and local governments operate separate funds for different occupations (e.g., teachers, public employees, police, and firemen).

18. As of April 30, 2010, New Jersey had invested $10.6 billion of $68.9 billion in assets in "alternative investments." See New Jersey Department of the Treasury, Division of Investment, http://www.state.nj.us/treasury/doinvest/, and also, "New Jersey Tops Another List," John Bury, Nj.com, June 13, 2010.

19.Ibid, Andrew G. Biggs, "The Market Value of Public-Sector Pension Deficits," April 2010, p. 2.

20. Amortization is the process of paying off a loan, spreading the cost of paying the principle and interest over time.

21. Kohn, Donald L., "Statement at the National Conference on Public Employee Retirement Systems Annual Conference." New Orleans, Louisiana, May 20, 2008, http://www.federalreserve.gov/newsevents/speech/kohn20080520a.htm

22. For instance, if governments can guarantee high investment returns without risk or cost due to their long time horizons, there would be enormous welfare gains by having all investments held and guaranteed by the government. Likewise, taxes could be eliminated if the government borrowed sufficient amounts and invested these sums in high-returning assets.

23. Jeffrey R. Brown and David W. Wilcox, "Discounting State and Local Pension Liabilities," American Economic Review: Papers & Proceedings 2009, 99:2, p. 538.

24. See Novy-Marx and Rauh (2008). The median (and modal) discount rate for 108 of the 112 state pension plans with assets greater than $1 billion in 2005 was 8 percent.

25. According to the Pew Center Study, the Financial Accounting Standards Board (FASB) which governs rules for pensions in the private sector recommends that investment returns be discounted more conservatively and suggests using the rate of return on corporate bonds. As of 2008, the top 10 private pensions had an assumed rate of return of 6.36%.

26. It is unclear whether investment returns from public plans are presented as simple averages (the arithmetic mean) or as the projected compound return (the geometric mean). The compound return is lower than the simple average return to the degree that annual returns vary from year to year. A plan that was fully funded assuming a given projected rate of return would need to achieve a compound return at that level to be able to pay its liabilities in practice. If a plan projected its future return as a compound return, then given market volatility one could expect a fully funded plan to have a 50 percent probability of being able to pay its liabilities in practice. However, if the plan's return was projected as a simple average—as seems to be the case for some plans—then one could expect a below 50 percent probability of a fully funded plan being able to meet its obligations. Public pension accounting rules, which consider the average return to plan assets but not the risk of such returns, do not illustrate the range of outcomes that are possible.

27. Wilcox notes that the link between discount rates and investment returns is "remarkable...because it suggests that plan sponsors can reduce their funding obligations by investing in riskier securities, whereas conventional finance theory would suggest that a given level of benefit security can be maintained despite a shift to riskier investment portfolio by increasing, rather than reducing, contributions to the plan." See, Brown and Wilcox, "Discounting State and Local Pension Liabilities," 2009, p. 538.

28. According to Brown and Wilcox, "The ideal set of discount rates would be derived from securities that deliver fully taxable cash flows; that deliver those cash flows with a high degree of assurance; that trade in markets without extraordinary liquidity characteristics; and that are free of flight-to-quality effects." p. 541.

29. Ibid. Novy-Marx and Rauh, "Public Pension Promises," 2010, p. 2.

30. Ibid. Novy-Marx and Rauh, "Public Pension Promises," 2010, p. 42. We arrive at a total liability of $5.2 trillion, by discounting the total liability for state pensions systems of $2.8 trillion in 2008 reported by the Pew Center using the 3.5% yield on 15 year Treasury bonds as of May 27, 2010. This is subtracted from the total reported assets in 2008 of $2.31 trillion to arrive at a total unfunded obligation of $3 trillion.

31. J. Fred Giertz, "The Impact of Pension Funding on State Government Funds," State Tax Notes, August 18, 2003, p. 511.

32. The prudent person rule was codified with the Employment Retirement Income Security Act of 1974 (ERISA), which established standards for private sector pensions.

33. Olivia S. Mitchell, David McCarthy, Stanley C. Wisniewksi, and Paul Zorn, "Developments in State and Local Pension Plans," Chapter 2 in Pensions in the Public Sector, eds. Olivia S. Mitchell and Edwin C. Hustead, University of Pennsylvania Press, Philadelphia 2001, p. 14.

34. J. Richard Aronson, James A. Dearden and Vicent C. Munley, "Public Employee Defined Benefit Pension Systems: the Impact of Explicit Surplus Sharing Contracts and Stakeholder Influence on Investment Strategies," February 2007 (Lehigh University) p. 3.

35. Andrew G. Biggs, "The Market Value of Public-Sector Pension Deficits," Retirement Policy Outlook No. 1, American Enterprise Institute for Public Policy Research, April 2010, p.2.

36. Government Accountability Office, "State and Local Retiree Benefits," GAO-08-223, p. 9.

37. See Jeffrey R. Brown, "Guaranteed Trouble: The Economic Effects of the Pension Benefit Guaranty Corporation," Journal of Economic Perspectives, Volume 22, No. 1, Winter 2008, pp. 177-198. Brown finds the financial deterioration of the PBGC to a government organization with a deficit in 2006 of $18.9 billion is due to design flaws leading the PBGC to a) fail to properly price insurance and thus encourage excessive risk taking by plan sponsors, b) fail to promote adequate funding of pension obligations, and c) fail to promote sufficient information disclosure to market participants.

38. Jeffrey Brown, "Guaranteed Trouble," Winter 2008 and also, Andrew Biggs and Jeffrey Brown, "Reforming the Pension Benefit Guaranty Corporation," forthcoming chapter in Public Insurance and Private Markets, Jeffrey R. Brown, ed., AEI Press, 2010.

39. Ibid, J. Richard Aronson, James A. Dearden, and Vincent G. Munley, "Public Employee Defined Benefit Pension Systems," p. 4.

40. Ibid, J. Richard Aronson, James A. Dearden, and Vincent G. Munley, "Public Employees Defined Benefit Pension Systems," pp. 7-8.

41. Stephanie Aaronson and Julia Coronado, Are Firms or Workers Behind the Shift Away from DB Pension Plans?, Finance and Economics Discussion Series, Divisions of Research & Statistics and Monetary Affairs, Federal Reserve Board, Washington, D.C., February 2005, p. 1.

42. Karen Steffen, "State Employee Pension Plans," in Pensions in the Public Sector, eds. Olivia S. Mitchell and Edwin C. Hustead, Pennsylvania University Press, Philadelphia 2002, p. 52.

43. Firm preferences and the enactment of ERISA (The Employee Retirement Income Security Act) in 1974 are often cited as reasons for the growing shift away from DB plans and towards DC plans in the private sector. Another factor is increased worker demand for DC plans. Aaronson and Coronado find that changing workforce characteristics including the influx of women in the workforce and concomitant increase in dual-income earner households may have increased the demand for flexibility by workers. Women as caregivers may have less attachment to specific employers and the labor market. Dual-income households must engage in joint-decision making—adjusting their employment in response to a change in employment of a spouse. See, Aaronson and Coronado, Are Firms or Workers Behind the Shift Away from DB Pension Plans?, Federal Reserve Board, February 2005, pp 6-7.

44. In addition, the state operates two plans that are closed to new members. These are the Consolidated Police and Firemen's Pension Fund (CPFPF): L. 1952, c. 266 and Prison Officers Pension Fund (POPF): L. 1941, c. 220.

45. New Jersey's state pension systems date to the creation of the Teacher's Retirement Fund in 1896, a statewide contributory annuity plan. The plan made no provisions for the funding of pension liabilities, leading to its near collapse. In 1919 the New Jersey legislature instituted the Teachers' Pension and Annuity Fund (TPAF) to ensure that the system be "established on a scientific (actuarial) basis." Between 1941 and 1973, the remaining six retirement systems were established. The PERS, PFRS and CPFPF plans, "allowed local governments to move from their unfunded pensions to State-administered plans that allowed centralized administration of these benefits and funding on an actuarial reserve basis. Today the process of consolidating public retirement benefits in a State- administered plan is nearly completed. A few locally-administered systems remain, including the Employees Retirement System of New Jersey and a small number of special funds for lifeguards in a few beachfront cities." See, "The New Jersey Pension System," Tom Bryan, in Pensions in the Public Sector, eds. Olivia S. Mitchell and Edwin Hustead, University of Pennsylvania Press, 2001.

46. Authors' calculations.

47. Public Employees' Retirement System of New Jersey, 55th Annual Report of the Actuary, July 1, 2009, p. 21, http://www.state.nj.us/treasury/pensions/pdf/financial/2009-actuary-rep…. See also, "Actuaries Going Ballistic," John Bury, nj.com, February 28, 2010.

48. See, The Hall Institute of Public Policy, "History and Future of New Jersey Pensions," p. 3. Additional actuarial assumptions were changed. The average salary increase assumption went up from 4.75 percent and 5 percent to 6.25 percent. The COLA inflation assumption increased from 2.25 percent and 2.5 percent to 3 percent. See Tom Bryan, "The New Jersey Pension System," in Mitchell and Hustead, pp. 337-338.

49. The Hall Institute of Public Policy, "History and Future of New Jersey Pensions," p. 3 and Tom Bryan, "The New Jersey Pension System," p. 337. Annual COLA benefits had been provided to retirees and beneficiaries beginning in 1969 on a pay-as-you-go basis. The state had been paying the full cost of health benefits coverage and Part B Medicare premiums for its qualified retirees and their eligible dependents since 1972. In 1987, the NJEA successfully lobbied for legislation requiring the state to pay for teacher health benefits.

50. See Tom Bryan, "The New Jersey Pension System," in Hustead and Mitchell, p. 343 for a detailed description of the effects of each alteration to the pension system and to contributions for the period between FY 1994 and FY 1998.

51. Eileen Norcross and Frederic Sautet, "Institutions Matter: Can New Jersey Reverse Course?" Mercatus Center Working Paper No. 09-30, July 2009, p. 22.

52. In 2000 New Jersey's five largest international common stock investments were concentrated in information technology: Nokia (AB) Oy, Ericsson (LM) Tel., Alcatel, Vodafone Group, Nortel Networks Corp. See "History and Future of New Jersey Pensions," The Hall Institute of Public Policy, p. 5.

53. The Hall Institute of Public Policy, "History and Future of New Jersey Pensions," September 2009, 5, http://www.hallnj.org/index.php/component/content/article/90-public-pen…- changes-in-nj-pension-investment-system?directory=216.

54. Chapter 133, P.L. 2001, S 2450, http://www.state.nj.us/treasury/pensions/pdf/laws/c133pl01.pdf.

55. Chapters 92 and 103, P.L. 2007 and Chapter 89, P.L. 2008 changed the enrollment and retirement criteria for PERS members enrolled at certain dates, creating membership tiers. Tier 1 members, those enrolled prior to July 1, 2007, and Tier 2 members, those eligible to enroll between July 1, 2007 and November 1, 2008, are eligible for retirement at age 60. Tier 3 members, those eligible to enroll after November 2, 2008 are eligible for retirement at age 62.

56. Chapter 1, P.L. 2010, http://www.state.nj.us/treasury/pensions/newlaw10.shtml#chap1, also, http://www.state.nj.us/treasury/pensions/epbam/exhibits/pdf/coltr0410-c….

57. The employee may have some option in choosing among authorized carriers including AIG-VALIC, AXA Financial (Equitable), The Hartford, ING Life Insurance and Annuity Co, MetLife and TIAA-CREF.

58. Chapter 92, P.L. 2007 and Chapter 103, P.L. 2007, expanded in Chapter 89, P.L. 2008.

59. See http://www.state.nj.us/treasury/pensions/epbam/exhibits/factsheets/fact….

60. This calculation is based on a model of the Social Security population and so could differ somewhat based on the characteristics of public sector employees and retirees. The reduction in plan liabilities is roughly linear and so could be scaled up or down.

61. The percentages are 4.6 percent for PERS, 5.5 percent for SPRS, 12.5 percent for JRS, and 18 percent for PERS. No value is reported for TPAF, though we can infer that it lies within that range.