- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

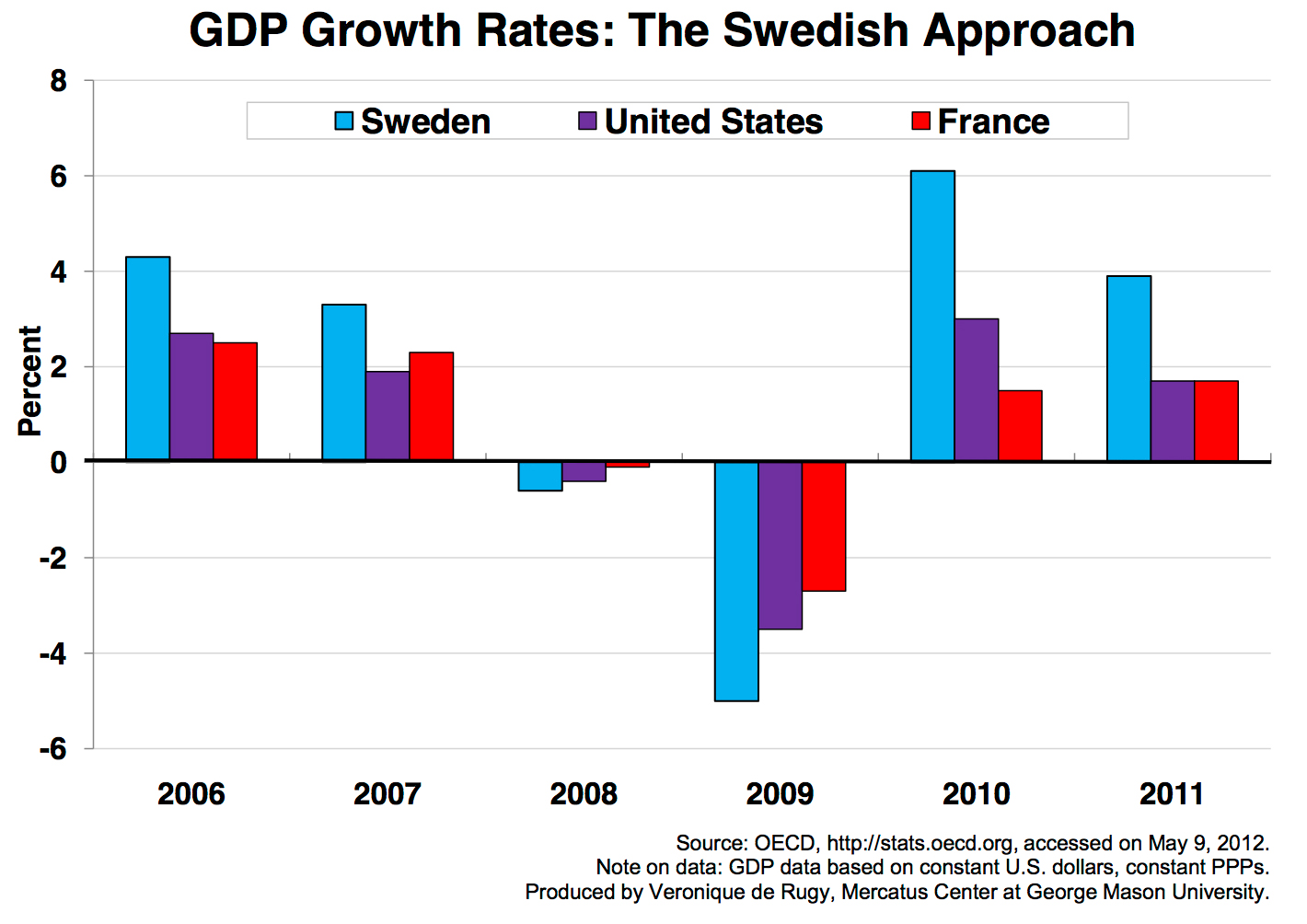

GDP Growth Rates: The Swedish Approach

While the debate over austerity continues, the evidence suggests that austerity can be successful so long as it isn't modeled after France’s so-called balanced approach. Other European countries and the United States should take heed and stop succumbing to the lure of an easy answer—to closing budget gaps with higher taxes.

While the debate over austerity continues, the evidence suggests that austerity can be successful so long as it isn't modeled after France’s so-called balanced approach. Other European countries and the United States should take heed and stop succumbing to the lure of an easy answer—to close budget gaps with higher taxes.

This week’s chart uses GDP growth rate data from the Organization for Economic Cooperation and Development (OECD) to illustrate the magnitudes of economic growth in Sweden, the United States, and France from 2006 to 2011.

The three-country comparison highlights that, while each recorded negative economic growth after the recession, Sweden not only took the largest hit but also experienced the largest rebound by 11 percent (from –5 percent in 2009 to 6.1 percent in 2010).

So what accounts for the difference in outcomes?

First and foremost, France has yet to cut spending. In fact, to the extent that the French are frustrated by so-called budget cuts, their only real complaint is that future increases in spending will not be as large as planned. (The same can be said about the U.S. budget.)

By contrast, Sweden has significantly cut government spending without equivalent increases in taxes. Sweden’s finance minister, Anders Borg, successfully reduced welfare spending and pursued economic stimulus through a permanent reduction in the country’s taxes, including a 20-point reduction in the top marginal income tax rate. As a result, Sweden’s economic growth has, of late, trumped every other European country’s.

Sweden’s commitment to reform has paid off in economic growth. While the “balanced approach” may give the appearance of pursuing fiscal solvency, in practice it stagnates the possibility of growth. Real fiscal reform comes from a commitment to cut spending and from structural changes to taxation and the regulatory environment.

Veronique de Rugy is a senior research fellow at the Mercatus Center at George Mason University. For media inquiries, contact [email protected]

Related Content

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

Key Assumptions Behind CBO's GDP Outlook

- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

Two Kinds of Austerity

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

European Austerity: Government Expenditures by Country

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations